Redrawing the AI Map: A Theory of Accountability Boundaries in Agentic Ecosystems

Pith reviewed 2026-05-25 04:47 UTC · model grok-4.3

The pith

Verification cost and responsibility transferability determine whether AI execution boundaries and accountability boundaries move together in agentic ecosystems.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

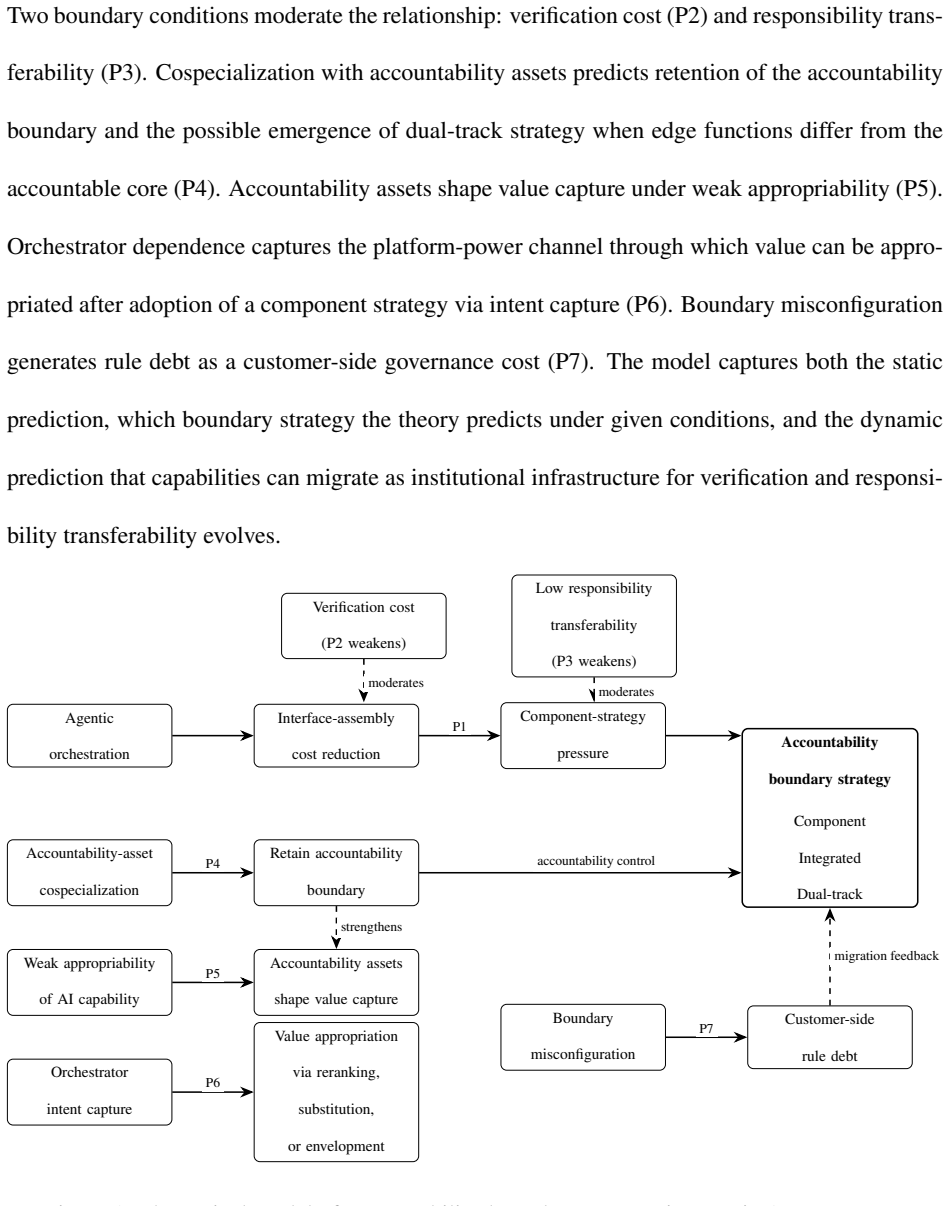

In agentic ecosystems, accountability boundaries are placed according to the presence of accountability assets together with verification cost and responsibility transferability. When verification costs are low and responsibility is transferable, execution and accountability boundaries can separate, supporting a component strategy; otherwise integrated or dual-track strategies result. The theory generates seven propositions that link agentic assembly-cost reductions, accountability assets, appropriability, orchestrator intent capture, and boundary misconfiguration to choices among the three strategies, to value appropriation, and to the accumulation of rule debt.

What carries the argument

Accountability assets: complementary assets that make AI-supported outputs legitimate, auditable, reviewable, and assignable to a responsible party.

If this is right

- Low verification cost and high responsibility transferability allow agentic assembly to reduce costs and produce component boundary strategies.

- High verification cost or low transferability keeps accountability boundaries integrated even when technical interfaces modularize.

- Rule debt accumulates when organizational decision rules migrate from formal systems into ungoverned agentic execution environments.

- Boundary misconfiguration reduces value appropriation by orchestrators or component providers.

- The three identified strategies (component, integrated, dual-track) produce distinct patterns of organizational disaggregation.

Where Pith is reading between the lines

- The same logic could be tested in domains outside the five illustrations, such as autonomous vehicle control or financial trading agents.

- Firms may need new internal governance mechanisms specifically designed to track and reduce rule debt.

- Regulators could use verification cost and transferability as observable criteria when deciding whether to require integrated human oversight for particular AI uses.

Load-bearing premise

Accountability assets function as identifiable complementary assets whose presence or absence, combined with verification cost and responsibility transferability, are the primary determinants of boundary placement across the listed domains.

What would settle it

An empirical case in one of the five domains where execution and accountability boundaries fully separate despite high verification costs and low responsibility transferability would falsify the central claim.

Figures

read the original abstract

Agentic AI orchestrators reduce the interface and assembly costs of composing information systems capabilities across organizational boundaries, seemingly accelerating modularization and organizational disaggregation. Yet AI-enabled capabilities whose outputs require evidence, review, signoff, or assignable responsibility may retain integrated accountability boundaries even when their technical interfaces become modular. We develop a capability-level theory of accountability-boundary placement in agentic ecosystems. We introduce accountability assets: complementary assets that make AI-supported outputs legitimate, auditable, reviewable, and assignable to a responsible party. We argue that verification cost and responsibility transferability determine whether the execution and accountability boundaries can move together. The theory identifies three boundary strategies: component, integrated, and dual-track. It also introduces rule debt, the governance burden that accrues when organizational decision rules migrate from formal information systems into ungoverned agentic execution environments. Integrating digital innovation, transaction cost, complementary-assets, digital platform governance, and IS control perspectives, we develop seven propositions linking agentic assembly-cost reductions, accountability assets, appropriability, orchestrator intent capture, and boundary misconfiguration to boundary strategy, value appropriation, and rule debt. The theory explains when digital modularization extends to organizational disaggregation and when accountability keeps capabilities integrated. Structured illustrations across document processing, legal services, audit, clinical decision support, and procurement discipline the boundary logic.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript develops a capability-level theory of accountability-boundary placement in agentic AI ecosystems. It introduces accountability assets (complementary assets enabling legitimacy, auditability, and assignability of AI outputs) and rule debt (governance burden from migrating decision rules into ungoverned agentic environments). The core argument is that verification cost and responsibility transferability determine whether execution and accountability boundaries align, yielding three strategies (component, integrated, dual-track). Seven propositions integrate digital innovation, transaction cost, complementary-assets, platform governance, and IS control perspectives; these are illustrated via structured examples in document processing, legal services, audit, clinical decision support, and procurement.

Significance. If the propositions hold, the framework would usefully explain limits to AI-driven modularization and disaggregation, showing why accountability requirements can keep capabilities integrated even when technical interfaces modularize. The explicit linkage of boundary strategies to value appropriation and rule debt, plus the domain illustrations, could bridge AI systems research with organizational governance literatures and support more precise predictions about when agentic orchestrators produce organizational change versus persistence of integration.

major comments (3)

- [Abstract / Theory Development] Abstract and theory section: the claim that verification cost and responsibility transferability 'determine whether the execution and accountability boundaries can move together' is asserted without explicit derivation steps, counter-examples, or formal mapping from the integrated perspectives; this leaves the central propositions vulnerable to the charge that they restate rather than extend transaction-cost and complementary-assets logic.

- [Abstract / Theory Development] Definition of accountability assets (Abstract): these are introduced as 'complementary assets that make AI-supported outputs legitimate, auditable, reviewable, and assignable,' yet the text does not demonstrate operational distinctions or incremental explanatory power beyond Teece-style complementary assets; the seven propositions therefore risk circularity by re-applying the cited frameworks without independent grounding.

- [Illustrations] Illustrations section: the mapping of domains (e.g., clinical decision support, procurement) to the three boundary strategies assumes accountability assets, verification cost, and responsibility transferability are the primary determinants, but no alternative explanations (regulatory mandates, liability rules) or falsification criteria are supplied, weakening the claim that the theory 'explains when digital modularization extends to organizational disaggregation.'

minor comments (2)

- [Theory Development] The term 'rule debt' is introduced without an explicit contrast to technical debt or other debt metaphors, which may reduce clarity for readers familiar with those literatures.

- [References] Ensure all citations to the five integrated perspectives receive complete bibliographic entries; several key works on complementary assets and platform governance appear referenced only at a high level.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed comments. We address each major comment point by point below, indicating where the manuscript will be revised to strengthen the theoretical grounding and illustrations.

read point-by-point responses

-

Referee: [Abstract / Theory Development] Abstract and theory section: the claim that verification cost and responsibility transferability 'determine whether the execution and accountability boundaries can move together' is asserted without explicit derivation steps, counter-examples, or formal mapping from the integrated perspectives; this leaves the central propositions vulnerable to the charge that they restate rather than extend transaction-cost and complementary-assets logic.

Authors: We accept that the derivation of the boundary-alignment claim requires more explicit steps. In revision we will insert a new subsection that (a) derives the interaction of verification cost and responsibility transferability from the five cited perspectives, (b) supplies two counter-examples in which low verification cost nevertheless produces boundary misalignment, and (c) presents a concise mapping table linking each antecedent to the three boundary strategies. These additions will clarify the incremental contribution beyond transaction-cost and complementary-assets logic. revision: yes

-

Referee: [Abstract / Theory Development] Definition of accountability assets (Abstract): these are introduced as 'complementary assets that make AI-supported outputs legitimate, auditable, reviewable, and assignable,' yet the text does not demonstrate operational distinctions or incremental explanatory power beyond Teece-style complementary assets; the seven propositions therefore risk circularity by re-applying the cited frameworks without independent grounding.

Authors: We agree that operational distinctions must be made explicit. The revised manuscript will define accountability assets by three measurable attributes—audit-trail completeness, sign-off protocol formality, and liability-assignability index—that are not reducible to Teece’s general complementary-asset categories. We will also add a short paragraph showing how these attributes generate distinct predictions for rule debt and value appropriation that are not derivable from the original frameworks alone. revision: yes

-

Referee: [Illustrations] Illustrations section: the mapping of domains (e.g., clinical decision support, procurement) to the three boundary strategies assumes accountability assets, verification cost, and responsibility transferability are the primary determinants, but no alternative explanations (regulatory mandates, liability rules) or falsification criteria are supplied, weakening the claim that the theory 'explains when digital modularization extends to organizational disaggregation.'

Authors: We will revise the illustrations section to acknowledge regulatory mandates and liability rules as potential moderators that can shift the thresholds of verification cost and responsibility transferability. Because the paper is conceptual rather than empirical, we cannot supply full falsification criteria; we will therefore add an explicit limitations paragraph stating that the propositions are subject to future empirical test and outlining observable indicators that would falsify each boundary strategy. revision: partial

Circularity Check

No significant circularity; integrative theory with independent conceptual content

full rationale

The paper constructs a capability-level theory by synthesizing established perspectives (digital innovation, transaction cost, complementary assets, platform governance, IS control) into seven propositions about accountability boundaries, verification cost, responsibility transferability, and accountability assets. No equations, fitted parameters, or self-referential definitions appear. No load-bearing self-citations, uniqueness theorems imported from the authors' prior work, or ansatzes smuggled via citation are present in the provided text. The central claims rest on logical integration and structured illustrations across domains rather than reductions to the paper's own inputs by construction. This is a standard honest finding for a conceptual theory paper; the derivation chain remains self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Verification cost and responsibility transferability are the key determinants of whether execution and accountability boundaries align.

- domain assumption Accountability assets act as complementary assets enabling legitimate, auditable, and assignable outputs.

invented entities (2)

-

accountability assets

no independent evidence

-

rule debt

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Formal Opinion 512: Generative artificial intelligence tools , year =

- [2]

-

[3]

Berente, Nicholas and Gu, Bin and Recker, Jan and Santhanam, Radhika , title =. MIS Quarterly , volume =

- [4]

- [5]

-

[6]

Information Systems Research , volume =

Choudhury, Vivek and Sabherwal, Rajiv , title =. Information Systems Research , volume =

- [7]

- [8]

-

[9]

OOPSLA 1992 Experience Report , year =

Cunningham, Ward , title =. OOPSLA 1992 Experience Report , year =

work page 1992

-

[10]

Strategic Management Journal , volume =

Eisenmann, Thomas and Parker, Geoffrey and Van Alstyne, Marshall , title =. Strategic Management Journal , volume =

-

[11]

Information and Organization , volume =

Faraj, Samer and Pachidi, Stella and Sayegh, Karla , title =. Information and Organization , volume =

-

[12]

Clinical decision support software: Guidance for industry and. 2026 , note =

work page 2026

- [13]

-

[14]

Grossman, Sanford J. and Hart, Oliver D. , title =. Journal of Political Economy , volume =

-

[15]

Journal of Political Economy , volume =

Hart, Oliver and Moore, John , title =. Journal of Political Economy , volume =

-

[16]

Henfridsson, Ola and Bygstad, Bendik , title =. MIS Quarterly , volume =

-

[17]

and Cennamo, Carmelo and Gawer, Annabelle , title =

Jacobides, Michael G. and Cennamo, Carmelo and Gawer, Annabelle , title =. Strategic Management Journal , volume =

- [18]

- [19]

-

[20]

Klein, Benjamin and Crawford, Robert G. and Alchian, Armen A. , title =. Journal of Law and Economics , volume =

- [21]

-

[22]

Specification, version 2025-11-25 , year =

work page 2025

-

[23]

and Srinivasan, Arati , title =

McIntyre, David P. and Srinivasan, Arati , title =. Strategic Management Journal , volume =

-

[24]

Orlikowski, Wanda J. and Iacono, C. Suzanne , title =. Information Systems Research , volume =

-

[25]

Parker, Geoffrey and Van Alstyne, Marshall and Jiang, Xiaoyue , title =. MIS Quarterly , volume =

-

[26]

Sambamurthy, V. and Zmud, Robert W. , title =. MIS Quarterly , volume =

-

[27]

Sculley, D. and Holt, Gary and Golovin, Daniel and Davydov, Eugene and Phillips, Todd and Ebner, Dietmar and Chaudhary, Vinay and Young, Michael and Crespo, Jean-Fran. Hidden technical debt in machine learning systems , booktitle =

-

[28]

Robo-advisers , year =

-

[29]

Strong, Diane M. and Volkoff, Olga , title =. MIS Quarterly , volume =

- [30]

-

[31]

Harvard Business Review Digital , month = mar, year =

Telang, Rahul and Hydari, Muhammad Zia and Iqbal, Raja , title =. Harvard Business Review Digital , month = mar, year =

-

[32]

Digital infrastructures: The missing

Tilson, David and Lyytinen, Kalle and S. Digital infrastructures: The missing. Information Systems Research , volume =

-

[33]

Tiwana, Amrit , title =

- [34]

-

[35]

Harvard Business Review , month = nov, year =

Van Hoek, Remko and DeWitt, Michael and Lacity, Mary and Johnson, Travis , title =. Harvard Business Review , month = nov, year =

- [36]

-

[37]

Wiener, Martin and M. Control configuration and control enactment in information systems projects: Review and expanded theoretical framework , journal =

- [38]

-

[39]

Information Systems Research , volume =

Yoo, Youngjin and Henfridsson, Ola and Lyytinen, Kalle , title =. Information Systems Research , volume =

-

[40]

Strategic Management Journal , volume =

Zhu, Feng and Liu, Qihong , title =. Strategic Management Journal , volume =

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.