Solving 2D Black Scholes Equation via Hermitian Block Embedding and Generalised Quantum Signal Processing

Pith reviewed 2026-06-28 19:02 UTC · model grok-4.3

The pith

A Hermitian block embedding lets generalised quantum signal processing solve the two-dimensional Black-Scholes equation.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

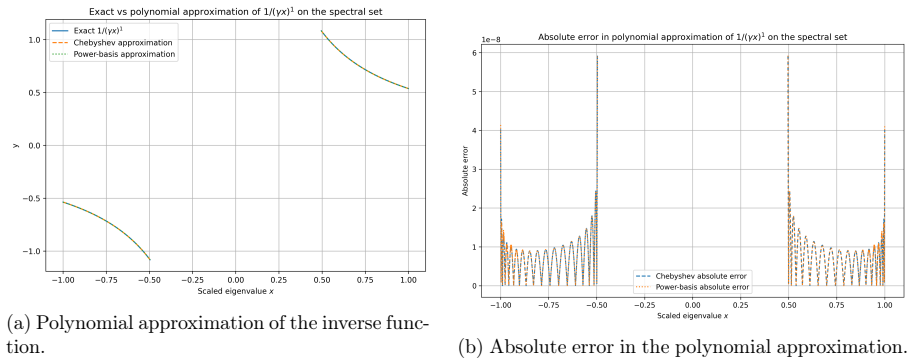

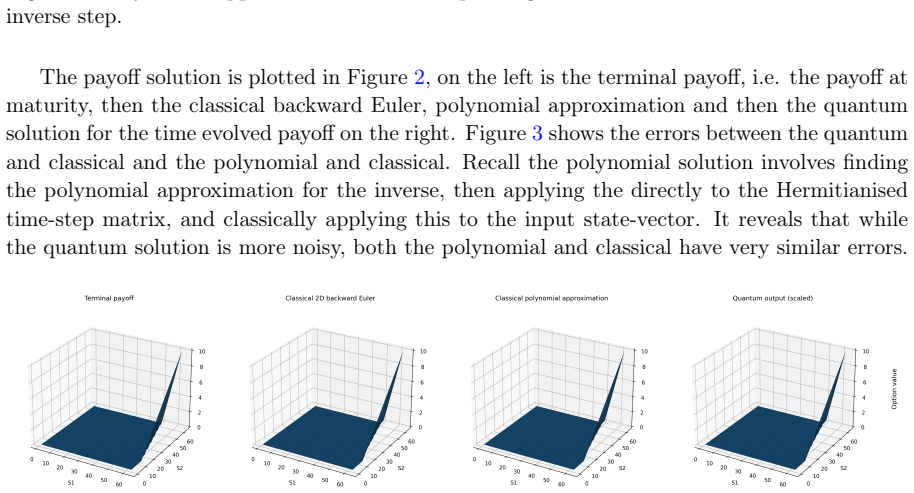

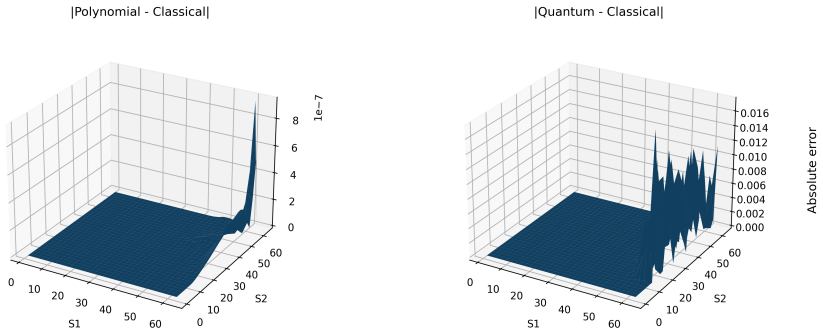

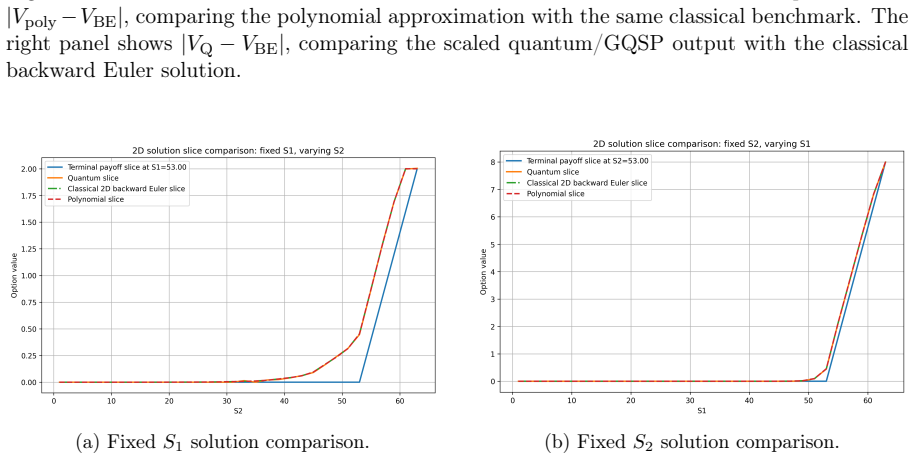

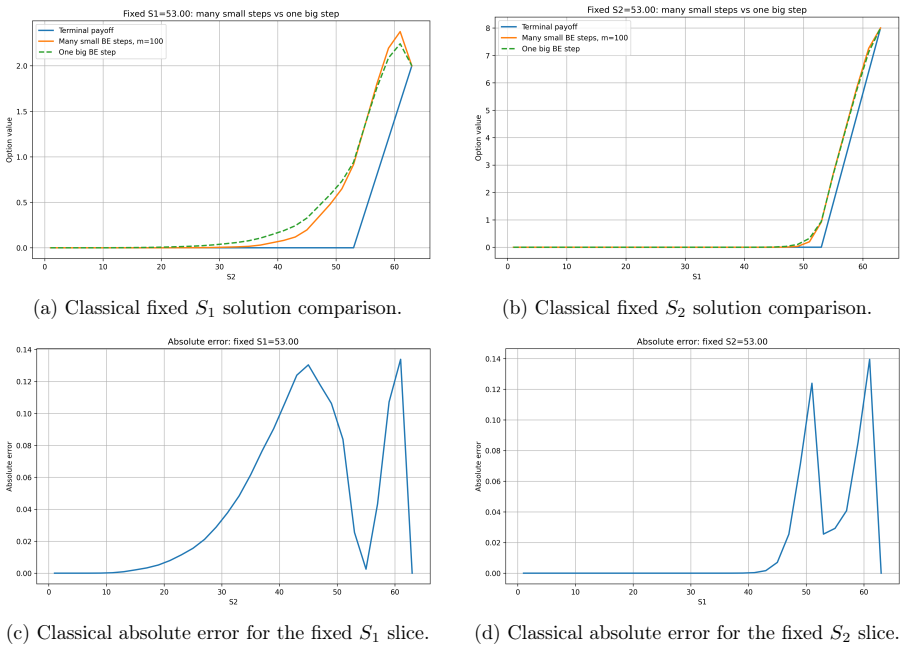

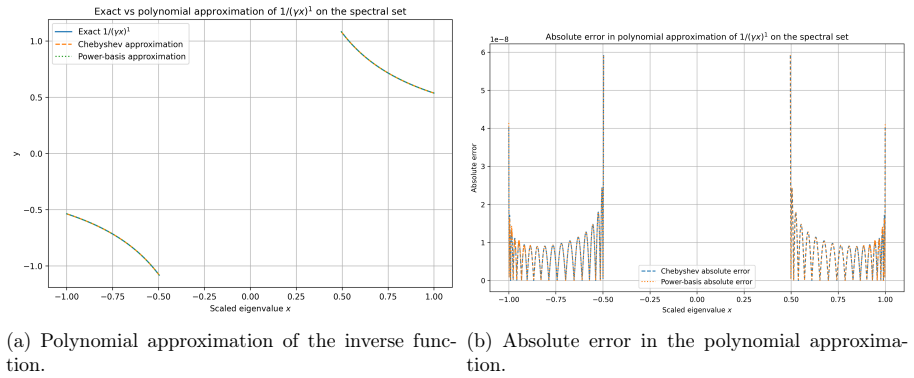

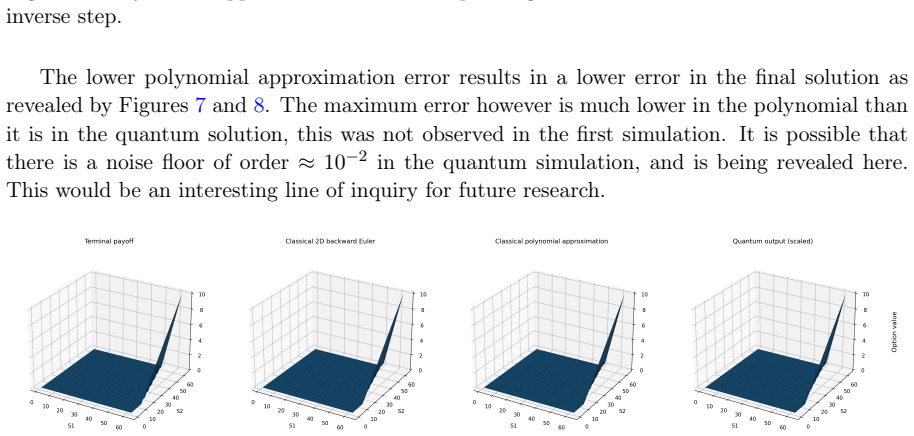

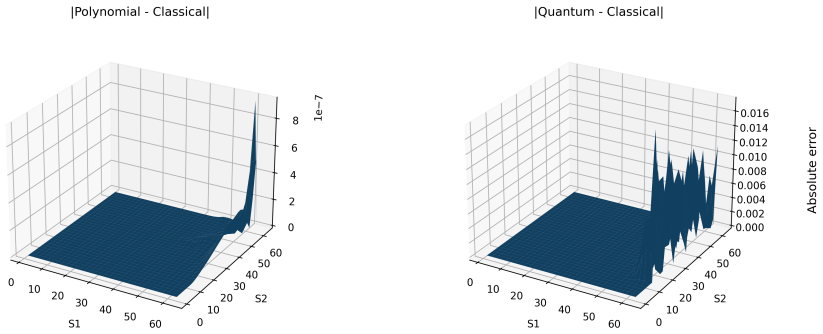

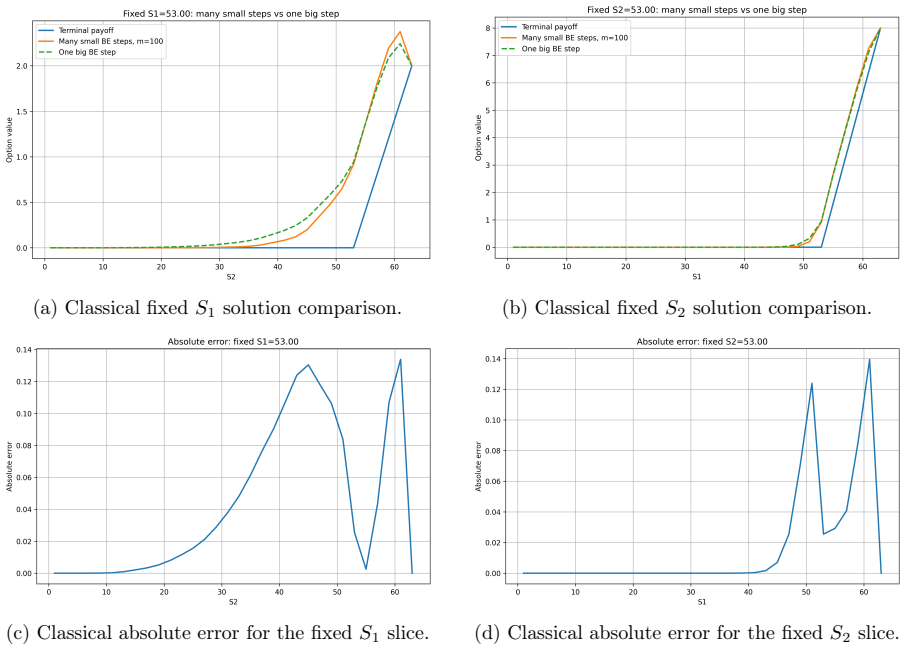

The authors construct a Hermitian block embedding of the non-Hermitian time-step matrix that appears after finite-difference discretisation of the two-dimensional Black-Scholes equation, thereby making the matrix amenable to generalised quantum signal processing; numerical solutions obtained this way for two-asset European calls agree closely with the classical polynomial approximation of the backward-Euler method, indicating that the embedding accurately reproduces the original operator's action.

What carries the argument

Hermitian block embedding of the non-Hermitian time-step matrix, which produces a larger Hermitian operator whose polynomial transformations via GQSP recover the desired matrix function.

If this is right

- GQSP can now be applied to the matrix functions that arise in multidimensional Black-Scholes pricing after finite-difference discretisation.

- The same embedding construction supplies a proof-of-principle route for other quantum linear-algebra primitives to act on non-Hermitian financial PDE operators.

- Benchmarking against the classical polynomial-plus-backward-Euler pipeline becomes a practical verification method for future quantum implementations.

- Extension to higher-dimensional or path-dependent options follows once the embedding is validated on the two-dimensional case.

Where Pith is reading between the lines

- If the embedding generalises, quantum algorithms could eventually tackle the linear systems that appear in stochastic-volatility or multi-factor models that remain expensive on classical hardware.

- The approach may also apply to other parabolic PDEs whose spatial operators are non-Hermitian after discretisation, such as certain advection-diffusion problems in physics.

- A natural next test would be to measure the actual quantum circuit depth or query complexity required once the embedding is combined with amplitude amplification or other cost-reduction techniques.

Load-bearing premise

Agreement between the embedded quantum solution and the classical polynomial approximation on two-asset European calls, for one particular discretisation and polynomial degree, is enough to conclude that the embedding faithfully captures the dynamics of the original non-Hermitian operator in general 2D Black-Scholes problems.

What would settle it

A direct computation, for a different payoff or grid resolution, in which the Hermitian-embedded GQSP result deviates measurably from the exact inverse of the non-Hermitian time-step matrix would show the embedding fails to preserve the required dynamics.

Figures

read the original abstract

The Black Scholes equation provides a fundamental model for the no arbitrage pricing of financial derivatives. After finite difference discretisation, the pricing problem can be formulated as a finite dimensional linear algebra problem involving the inverse of a non Hermitian time step matrix. Recent advances in quantum linear algebra algorithms, particularly the generalised quantum signal processing (GQSP)algorithm, enable matrix functions to be implemented through polynomial transformations of a suitable unitary or Hermitian form. In this paper, we develop a Hermitian block embedding method that enables GQSP to be applied to the two dimensional Black Scholes equation. Numerical simulations for two asset European call options are performed to evaluate the proposed approach. GQSP based solutions are benchmarked against the classical polynomial approximation with backward Euler finite difference method, showing close agreement. This indicates that the Hermitian block embedding construction accurately captures the dynamics of the original non Hermitian operator. These results demonstrate the feasibility of combining Hermitian block embeddings with GQSP for multidimensional Black Scholes problems and provide a proof of principle for applying modern quantum linear algebra techniques to option pricing.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops a Hermitian block embedding to recast the non-Hermitian time-step matrix arising from finite-difference discretization of the 2D Black-Scholes PDE into a form amenable to Generalised Quantum Signal Processing (GQSP). It reports numerical simulations for two-asset European call options in which the GQSP solutions agree closely with a classical polynomial approximation to the backward-Euler finite-difference solution, and concludes that this agreement shows the embedding accurately captures the original operator dynamics.

Significance. If the embedding is shown to preserve the relevant operator action beyond the specific test cases, the construction would supply a concrete route for applying modern quantum linear-algebra primitives to multidimensional option-pricing problems. The work supplies a proof-of-principle demonstration that GQSP can be combined with block embeddings for this class of PDEs.

major comments (2)

- [Numerical simulations section] The central claim that the Hermitian block embedding 'accurately captures the dynamics of the original non Hermitian operator' rests entirely on numerical agreement for two-asset European calls under one discretisation and one polynomial degree (Numerical simulations section). No algebraic identity, operator-norm bound, or spectrum-preservation argument is supplied to show that the embedding reproduces the action of the original non-Hermitian matrix for arbitrary payoffs, boundary conditions, or correlation values; agreement on a single payoff class could arise from accidental cancellation and does not establish general correctness.

- [Numerical simulations section] No quantitative error metrics (maximum absolute error, L2 norm, dependence on grid size or polynomial degree), no statement of the GQSP polynomial degree or approximation error, and no comparison against the exact matrix inverse are reported. Without these, the phrase 'close agreement' cannot be evaluated for robustness or post-hoc selection (Numerical simulations section).

minor comments (1)

- [Abstract] The abstract and introduction would benefit from an explicit statement of the grid sizes, time-step parameters, and correlation values used in the reported experiments.

Simulated Author's Rebuttal

We thank the referee for their careful reading and constructive comments on the numerical validation. We address each point below and will revise the manuscript to improve quantitative reporting and clarify the scope of our claims.

read point-by-point responses

-

Referee: [Numerical simulations section] The central claim that the Hermitian block embedding 'accurately captures the dynamics of the original non Hermitian operator' rests entirely on numerical agreement for two-asset European calls under one discretisation and one polynomial degree (Numerical simulations section). No algebraic identity, operator-norm bound, or spectrum-preservation argument is supplied to show that the embedding reproduces the action of the original non-Hermitian matrix for arbitrary payoffs, boundary conditions, or correlation values; agreement on a single payoff class could arise from accidental cancellation and does not establish general correctness.

Authors: We agree that the manuscript relies on numerical evidence for specific test cases rather than a general algebraic proof. The work is framed as a proof-of-principle demonstration of the embedding construction combined with GQSP. In revision we will moderate the language in the abstract and conclusions to state that the observed agreement supports correctness for the reported instances, and we will expand the numerical section with additional simulations using varied correlation values and boundary conditions. A full operator-theoretic analysis lies outside the present scope. revision: partial

-

Referee: [Numerical simulations section] No quantitative error metrics (maximum absolute error, L2 norm, dependence on grid size or polynomial degree), no statement of the GQSP polynomial degree or approximation error, and no comparison against the exact matrix inverse are reported. Without these, the phrase 'close agreement' cannot be evaluated for robustness or post-hoc selection (Numerical simulations section).

Authors: We will revise the Numerical simulations section to report the GQSP polynomial degree and its approximation error, include quantitative metrics (maximum absolute error and L2 norm) together with their dependence on grid size, and add direct comparisons to the exact matrix inverse for the small grids employed. These additions will make the degree of agreement transparent and reproducible. revision: yes

Circularity Check

No circularity: embedding construction and numerical benchmark are independent of target result

full rationale

The paper introduces a Hermitian block embedding to allow GQSP on the discretized 2D Black-Scholes operator and validates it via direct numerical comparison to a classical polynomial approximation of backward-Euler finite differences on two-asset European calls. No equation is shown to equal its own input by definition, no fitted parameter is relabeled as a prediction, and no load-bearing premise reduces to a self-citation whose content is itself unverified. The agreement is presented as external evidence rather than a tautological consequence of the embedding definition, so the derivation chain remains self-contained.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption After finite difference discretisation, the pricing problem can be formulated as a finite dimensional linear algebra problem involving the inverse of a non Hermitian time step matrix.

Reference graph

Works this paper leans on

-

[1]

Black and M

F. Black and M. Scholes, ‘The pricing of options and corporate liabilities,’Journal of Political Economy, vol. 81, no. 3, pp. 637–654, 1973

1973

-

[2]

J. C. Hull,Options, Futures, and Other Derivatives, 11th ed. Harlow, UK: Pearson, 2021, Global Edition,isbn: 978-1292410654

2021

-

[3]

Wilmott,Paul Wilmott Introduces Quantitative Finance, 2nd ed

P. Wilmott,Paul Wilmott Introduces Quantitative Finance, 2nd ed. Chichester, UK: John Wiley & Sons, 2007,isbn: 978-0-470-31958-1

2007

-

[4]

Y. Wu, J. Wang and Y. li,Quantum computing for option portfolio analysis, Jun. 2024. doi:10.48550/arXiv.2406.00486 23

-

[5]

K. Miyamoto and K. Kubo, ‘Pricing multi-asset derivatives by finite difference method on a quantum computer,’ arXiv.org, Papers 2109.12896, Sep. 2021.doi:None[Online]. Available:https://ideas.repec.org/p/arx/papers/2109.12896.html

-

[6]

J. Kim et al., ‘A practical finite difference method for the three-dimensional black–scholes equation,’European Journal of Operational Research, vol. 252, no. 1, pp. 183–190, 2016, issn: 0377-2217.doi:https://doi.org/10.1016/j.ejor.2015.12.012[Online]. Avail- able:https://www.sciencedirect.com/science/article/pii/S0377221715011212

-

[7]

Chen, ‘Numerical methods for pricing multi-asset options,’ 2018

Y. Chen, ‘Numerical methods for pricing multi-asset options,’ 2018. [Online]. Available: https://api.semanticscholar.org/CorpusID:44048998

2018

-

[8]

D. Černá and K. Fiňková,Option pricing under multifactor black-scholes model using or- thogonal spline wavelets, 2022. arXiv:2211.13890 [math.NA]. [Online]. Available:https: //arxiv.org/abs/2211.13890

-

[9]

G. H. Low and I. L. Chuang, ‘Optimal hamiltonian simulation by quantum signal pro- cessing,’Phys. Rev. Lett., vol. 118, p. 010501, 1 Jan. 2017.doi:10.1103/PhysRevLett. 118.010501[Online]. Available:https://link.aps.org/doi/10.1103/PhysRevLett. 118.010501

-

[10]

A. Gilyén, Y. Su, G. H. Low and N. Wiebe, ‘Quantum singular value transformation and beyond: Exponential improvements for quantum matrix arithmetics,’ inProceed- ings of the 51st Annual ACM SIGACT Symposium on Theory of Computing, ser. STOC 2019, Phoenix, AZ, USA: Association for Computing Machinery, 2019, pp. 193–204,isbn: 9781450367059.doi:10.1145/33132...

-

[11]

J. M. Martyn, Z. M. Rossi, A. K. Tan and I. L. Chuang, ‘Grand unification of quantum algorithms,’PRX Quantum, vol. 2, p. 040203, 4 Dec. 2021.doi:10.1103/PRXQuantum.2. 040203[Online]. Available:https://link.aps.org/doi/10.1103/PRXQuantum.2.040203

-

[12]

D. Motlagh and N. Wiebe, ‘Generalized quantum signal processing,’PRX Quantum, vol. 5, p. 020368, 2 Jun. 2024.doi:10.1103/PRXQuantum.5.020368[Online]. Available:https: //link.aps.org/doi/10.1103/PRXQuantum.5.020368

-

[13]

J. W. Greenwell et al.,Quantum option pricing through hermitian transformation of the black–scholes operator, Submitted to IEEE Quantum Week, 2026

2026

-

[14]

Hermitian Matrix Function Synthesis without Block-Encoding

A. Mahasinghe, K. D. Silva, X. Cadet, P. Chin, F. Cadet and J. Wang,Hermitian matrix function synthesis without block-encoding, 2025. arXiv:2512.18249 [quant-ph]. [Online]. Available:https://arxiv.org/abs/2512.18249 24

work page internal anchor Pith review Pith/arXiv arXiv 2025

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.