A Taxonomy of Real-World Asset Tokenization for Blockchain-Based Financial Infrastructure

Pith reviewed 2026-06-27 17:50 UTC · model grok-4.3

The pith

Real-world asset tokenization predominantly uses hybrid architectures with on-chain tokens and off-chain legal structures.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The classification shows that current RWA tokenization is predominantly implemented through hybrid architectures: blockchain tokens support representation, transfer control, redemption workflows, pricing, and composability, while core legal guarantees remain anchored in off-chain legal wrappers, custodial arrangements, compliance processes, and verification mechanisms.

What carries the argument

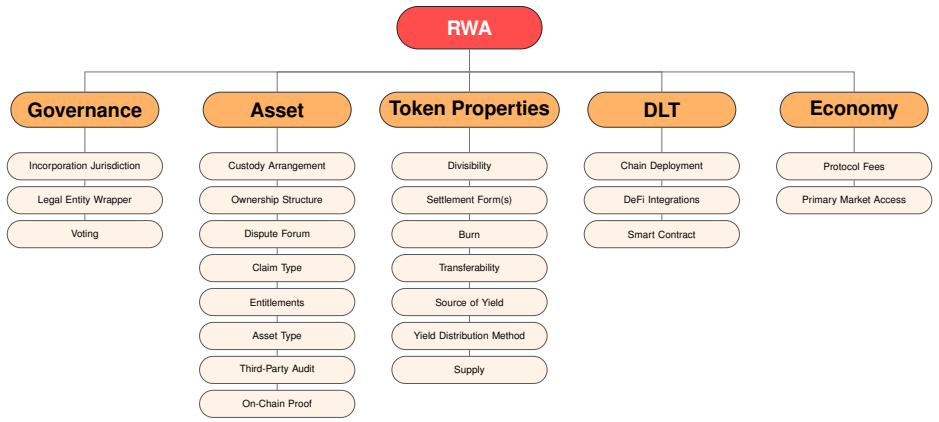

A systems-level taxonomy with five components—governance, asset structure, token properties, distributed ledger technology, and economy—comprising twenty-three dimensions that classify how off-chain assets are represented on-chain.

If this is right

- The taxonomy enables systematic comparison of RWA systems across different asset classes and implementation models.

- Recurring documentation gaps are identified in voting rights, dispute forums, burn mechanics, supply constraints, and reserve verification.

- Design patterns and limitations become visible that can guide future development of blockchain-based financial infrastructure.

- Token mechanics are shown to focus on operational functions while legal guarantees remain off-chain.

Where Pith is reading between the lines

- The hybrid pattern implies that advancing toward more decentralized finance will require corresponding changes in off-chain legal and regulatory systems.

- Regulators could apply the taxonomy dimensions to evaluate compliance and operational risks across different RWA projects.

- Industry standards for project documentation could address the identified gaps in areas such as voting rights and reserve verification.

- New RWA initiatives might prioritize reducing off-chain dependencies to improve transparency and auditability.

Load-bearing premise

The twenty major RWA systems selected by market capitalization are representative of the field and the iterative taxonomy-development method produces dimensions that comprehensively and without selection bias capture the legal, economic, and technical aspects of RWA tokenization.

What would settle it

Application of the same taxonomy to a broader set of RWA systems outside the top twenty by market capitalization that consistently show fully on-chain legal structures without off-chain wrappers would falsify the claim of predominant hybrid architectures.

Figures

read the original abstract

Real-world asset (RWA) tokenization has emerged as a prominent application of blockchain technology, enabling off-chain financial and non-financial assets to be represented through blockchain-based instruments. However, deployed RWA systems remain difficult to compare because legal claims, custody arrangements, token mechanics, verification processes, and on-chain integrations are often described separately. This paper develops a systems-level taxonomy of RWA tokenization to classify how off-chain assets are legally, economically, and technically represented on-chain. Following an iterative taxonomy-development method, we organize twenty-three dimensions into five components: governance, asset structure, token properties, distributed ledger technology, and economy. We apply the taxonomy to twenty major RWA systems selected by market capitalization and compare their design choices across asset classes and implementation models. The classification shows that current RWA tokenization is predominantly implemented through hybrid architectures: blockchain tokens support representation, transfer control, redemption workflows, pricing, and composability, while core legal guarantees remain anchored in off-chain legal wrappers, custodial arrangements, compliance processes, and verification mechanisms. The analysis also reveals recurring documentation gaps concerning voting rights, dispute forums, burn mechanics, supply constraints, and reserve verification. Overall, the taxonomy provides a structured basis for comparing RWA systems, identifying design patterns and limitations, and supporting future research on blockchain-based financial infrastructure.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops a systems-level taxonomy for real-world asset (RWA) tokenization, organizing 23 dimensions into five components (governance, asset structure, token properties, distributed ledger technology, and economy) via an iterative method. It applies the taxonomy to twenty major RWA systems selected by market capitalization, finding that hybrid architectures predominate: on-chain tokens handle representation, transfer, redemption, pricing, and composability while legal guarantees, custody, compliance, and verification remain off-chain. The work also identifies recurring documentation gaps in areas such as voting rights and reserve verification, positioning the taxonomy as a basis for future comparisons of blockchain-based financial infrastructure.

Significance. If the classification and hybrid predominance finding hold under a more transparent methodology, the taxonomy supplies a concrete, multi-dimensional framework for comparing RWA implementations that integrates legal, economic, and technical features. The systematic application to twenty systems supplies empirical grounding that distinguishes this work from purely conceptual taxonomies and could support subsequent research on design patterns, limitations, and infrastructure evolution.

major comments (2)

- [Abstract] Abstract: the central generalization that 'current RWA tokenization is predominantly implemented through hybrid architectures' rests on the classification of twenty systems; however, the selection criterion (market capitalization) is stated without explicit inclusion/exclusion rules, sensitivity checks against alternative samples, or discussion of how it might over-weight established projects with particular custody and compliance setups, directly affecting the robustness of the predominance claim.

- [Abstract] Abstract (methods description): the iterative taxonomy-development method is described only at high level ('following an iterative taxonomy-development method, we organize twenty-three dimensions'); without documented criteria for dimension refinement, iteration stopping rules, or safeguards against constructing dimensions that fit the observed sample, it is not possible to evaluate whether the five components and hybrid pattern are independent of the twenty-system sample.

minor comments (2)

- [Abstract] Abstract: the phrase 'recurring documentation gaps concerning voting rights, dispute forums, burn mechanics, supply constraints, and reserve verification' would be strengthened by a summary table or appendix listing which systems exhibit which gaps.

- [Abstract] The abstract states the taxonomy 'provides a structured basis for comparing RWA systems'; consider adding a brief forward-looking paragraph on how the taxonomy could be extended or tested on non-market-cap samples.

Simulated Author's Rebuttal

We thank the referee for these constructive comments on methodological transparency. Both points identify areas where additional detail will strengthen the paper without changing its core claims or findings. We commit to revisions that address the concerns directly.

read point-by-point responses

-

Referee: [Abstract] Abstract: the central generalization that 'current RWA tokenization is predominantly implemented through hybrid architectures' rests on the classification of twenty systems; however, the selection criterion (market capitalization) is stated without explicit inclusion/exclusion rules, sensitivity checks against alternative samples, or discussion of how it might over-weight established projects with particular custody and compliance setups, directly affecting the robustness of the predominance claim.

Authors: We agree that the sample selection process requires explicit documentation to support the robustness of the hybrid predominance finding. In the revised manuscript we will add a dedicated methods subsection specifying: inclusion criteria (top 20 RWA projects by reported market capitalization as of a fixed date, sourced from DefiLlama and project disclosures), explicit exclusion rules (projects lacking verifiable on-chain token contracts or public documentation), the full list of twenty systems, and a short sensitivity discussion. The discussion will note that market-cap weighting may favor projects with mature legal wrappers yet the hybrid pattern remains consistent when the sample is stratified by asset class. We will also report a brief check using an alternative selection by total value locked. revision: yes

-

Referee: [Abstract] Abstract (methods description): the iterative taxonomy-development method is described only at high level ('following an iterative taxonomy-development method, we organize twenty-three dimensions'); without documented criteria for dimension refinement, iteration stopping rules, or safeguards against constructing dimensions that fit the observed sample, it is not possible to evaluate whether the five components and hybrid pattern are independent of the twenty-system sample.

Authors: We acknowledge that the current high-level description of the iterative method limits evaluability of independence from the sample. The revised manuscript will expand the methods section with: (i) refinement criteria requiring each new dimension to address a distinct legal, economic, or technical facet not already captured; (ii) stopping rules based on saturation after an initial pilot of ten systems, with confirmation that the remaining ten introduced no additional dimensions; and (iii) safeguards consisting of cross-referencing candidate dimensions against established literature on blockchain governance and financial infrastructure prior to finalization. These additions will demonstrate that the five-component structure and hybrid finding are not sample-specific artifacts. revision: yes

Circularity Check

No circularity: purely descriptive taxonomy with no derivations or self-referential reductions

full rationale

The paper constructs a taxonomy by applying an iterative classification process to 20 observed RWA systems selected by market capitalization, organizing features into 23 dimensions across five components. No equations, fitted parameters, predictions, or derivations exist that could reduce to inputs by construction. The central claim of hybrid architecture predominance follows directly from the classification results rather than from any self-definition, self-citation chain, or renamed known result. The method is self-contained against external benchmarks as a standard descriptive exercise in systems analysis.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Iterative taxonomy-development method yields dimensions that comprehensively cover governance, asset structure, token properties, DLT, and economy for RWA systems

Reference graph

Works this paper leans on

-

[1]

Sok of rwa tokenization: A systematization of concepts, architectures, and legal interoperability,

J. Luo, X. Xiong, Z. Li, H. Kang, X. Liu, W. J. Knottenbelt, and K. Tinn, “Sok of rwa tokenization: A systematization of concepts, architectures, and legal interoperability,”arXiv preprint arXiv:2604.06608, 2026

Pith/arXiv arXiv 2026

-

[2]

Legal structures of tokenised assets,

X. Lavayssi `ere, “Legal structures of tokenised assets,” European Journal of Risk Regulation, pp. 1–13, 2024

2024

-

[3]

Tokenisation in the context of money and other assets: Concepts and implications for central banks,

C. on Payments, M. Infrastructures, and B. for International Settlements, “Tokenisation in the context of money and other assets: Concepts and implications for central banks,” Bank for International Settlements, Tech. Rep., oct 2024. [Online]. Available: https: //www.bis.org/cpmi/publ/d225.htm

2024

-

[4]

Tokenization and financial market inef- ficiencies,

I. Agur, G. Villegas-Bauer, T. Mancini-Griffoli, and M. S. Martinez Peria, “Tokenization and financial market inef- ficiencies,” International Monetary Fund, Fintech Notes 2025/001, jan 2025

2025

-

[5]

The financial stability implications of tokenisation,

F. S. Board, “The financial stability implications of tokenisation,” FSB statement / web publication, oct

-

[6]

Available: https://www.fsb.org/2024/10/ the-financial-stability-implications-of-tokenisation/

[Online]. Available: https://www.fsb.org/2024/10/ the-financial-stability-implications-of-tokenisation/

2024

-

[7]

Foundations of cryp- toeconomic systems,

S. V oshmgir, M. Zarghamet al., “Foundations of cryp- toeconomic systems,”Research Institute for Cryptoeco- nomics, Vienna, Working Paper Series/Institute for Cryp- toeconomics/Interdisciplinary Research, vol. 1, 2019

2019

-

[8]

De- crypting distributed ledger design—taxonomy, classifi- cation and blockchain community evaluation,

M. C. Ballandies, M. M. Dapp, and E. Pournaras, “De- crypting distributed ledger design—taxonomy, classifi- cation and blockchain community evaluation,”Cluster computing, vol. 25, no. 3, pp. 1817–1838, 2022

2022

-

[9]

Real World Assets,

DefiLlama, “Real World Assets,” 2026, accessed: 2026- 05-11. [Online]. Available: https://defillama.com/rwa

2026

-

[10]

A general approach to tokens and non-fungible tokens,

M. C. Ballandies, P. K. Makode, and C. J. Tessone, “A general approach to tokens and non-fungible tokens,” in Routledge Handbook of NFT Law. Routledge, 2025, pp. 3–16

2025

-

[11]

A taxonomy for blockchain- based decentralized physical infrastructure networks (de- pin),

M. C. Ballandies, H. Wang, A. C. C. Law, J. C. Yang, C. G¨osken, and M. Andrew, “A taxonomy for blockchain- based decentralized physical infrastructure networks (de- pin),” in2023 IEEE 9th World Forum on Internet of Things (WF-IoT). IEEE, 2023, pp. 1–6

2023

-

[12]

On tokenizing securities in contemporary decentralized finance ecosystems,

Z. Li, Z. Li, K. Wu, D. Zhang, K. Zhang, D. Liu, Z. Guo, C. Zhou, H. Guan, and J. Niu, “On tokenizing securities in contemporary decentralized finance ecosystems,” in 2024 IEEE International Conference on Blockchain Research & Applications for Innovative Networks and Services (BRAINS). IEEE, 2024, pp. 1–9. [Online]. Available: https://doi.org/10.1109/BRAI...

-

[13]

Tokenizing assets with dividend payouts—a legally compliant and flexible design,

V . Zhitomirskiy, H. Franken, N. Schmidt, T. Schiller, and M. Hanke, “Tokenizing assets with dividend payouts—a legally compliant and flexible design,”Digital Finance, vol. 5, no. 3–4, pp. 1–18, 2023. [Online]. Available: https: //link.springer.com/article/10.1007/s42521-023-00094-w

-

[14]

Tokenisation of assets and distributed ledger technologies in financial markets: Potential impediments to market development and policy implications,

OECD, “Tokenisation of assets and distributed ledger technologies in financial markets: Potential impediments to market development and policy implications,” OECD Publishing, Paris, OECD Business and Finance Policy Papers 75, jan 2025

2025

-

[15]

Tokenization of financial assets,

I. O. of Securities Commissions, “Tokenization of financial assets,” International Organization of Securities Commissions, Final Report FR/17/2025, nov

2025

-

[16]

Available: https://www.iosco.org/library/ pubdocs/pdf/IOSCOPD809.pdf

[Online]. Available: https://www.iosco.org/library/ pubdocs/pdf/IOSCOPD809.pdf

-

[17]

Tokenization and the future of property investment: A new paradigm for real estate,

A. El Jaouhari, T. ˇSeˇsplaukis, L. L ´azaro-Touza, A. Dagilyt ˙e, and M. Sk ¨ardi, “Tokenization and the future of property investment: A new paradigm for real estate,”International Journal of Strategic Property Management, vol. 29, no. 4, pp. 297–315, 2025. [Online]. Available: https://journals.vilniustech.lt/index. php/IJSPM/article/view/24814

2025

-

[18]

Tokenizing patents and intellectual property assets: Using blockchain-based systems and non-fungible tokens to promote financialization,

S. M. H. Bamakan, S. H. Khajavi, S. D. Manshadi, and M. Motlagh, “Tokenizing patents and intellectual property assets: Using blockchain-based systems and non-fungible tokens to promote financialization,”Scien- tific Reports, vol. 12, p. 2178, 2022. [Online]. Available: https://www.nature.com/articles/s41598-022-05920-6

2022

-

[19]

P. C ¸ . Aksoy, L. Dimatteo, and S. Hufnagel,Routledge Handbook of NFT Law. Taylor & Francis, 2025

2025

-

[20]

To token or not to token: Tools for understanding blockchain tokens,

L. Oliveira, L. Zavolokina, I. Bauer, and G. Schwabe, “To token or not to token: Tools for understanding blockchain tokens,” inProceedings of the 39th International Confer- ence on Information Systems, 2018

2018

-

[21]

Crypto tokens and token systems,

J. Schwiderowski, A. B. Pedersen, and R. Beck, “Crypto tokens and token systems,”Information Systems Fron- tiers, vol. 26, no. 1, pp. 319–332, 2024

2024

-

[22]

A unified framework and comparative study of de- centralized finance derivatives protocols,

L. Pennella, P. Saggese, F. Pinelli, and L. Galletta, “A unified framework and comparative study of de- centralized finance derivatives protocols,”arXiv preprint arXiv:2512.19113, 2025

Pith/arXiv arXiv 2025

-

[23]

Exploration on real world assets and tokenization,

W. Xia, Y . Zhang, and Y . Cheng, “Exploration on real world assets and tokenization,” may 2025. [Online]. Available: https://arxiv.org/abs/2503.01111

arXiv 2025

-

[24]

A method for uncovering tokenisation archetypes and their effects: Thus spoke switzerland,

A. Plepi and P. Schwendner, “A method for uncovering tokenisation archetypes and their effects: Thus spoke switzerland,” SSRN Working Paper, nov 2024, sSRN eLibrary, accessed 2026-01-21

2024

-

[25]

A taxonomy of tokenisation methods for real- world assets,

N. Aliyev, “A taxonomy of tokenisation methods for real- world assets,”Available at SSRN 5214610, 2023

2023

-

[26]

Crypto-asset tax- onomy for investors and regulators,

X. Zhang, J. I. Iba ˜nez, and J. Xu, “Crypto-asset tax- onomy for investors and regulators,”arXiv preprint arXiv:2602.05098, 2026

arXiv 2026

-

[27]

Exploring trust in decentralized finance intermediaries: a taxonomy and archetypes for guiding blockchain-based investment de- cisions on the web,

C. Zeiß, L. Straub, M. Greiner, M. Neis, N. Neis, A. Winkelmann, and U. Lechner, “Exploring trust in decentralized finance intermediaries: a taxonomy and archetypes for guiding blockchain-based investment de- cisions on the web,”Internet Research, vol. 35, no. 7, pp. 133–152, 2025

2025

-

[28]

A method for taxonomy development and its application in information systems,

R. C. Nickerson, U. Varshney, and J. Muntermann, “A method for taxonomy development and its application in information systems,”European journal of information systems, vol. 22, no. 3, pp. 336–359, 2013. APPENDIXA TAXONOMYMATRIX TABLE VI: RW A taxonomy components, dimensions, definitions, and permitted characteristics. Component Dimension Definition Permi...

2013

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.