The Coevolution of Banks and Corporate Securities Markets: The Financing of Belgium's Industrial Take-Off in the 1830s

Pith reviewed 2026-05-25 15:09 UTC · model grok-4.3

The pith

Banks in 1830s Belgium developed secondary securities markets by securitizing corporate debt while also acting as market-makers whose own balance sheets responded to market swings.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

In the 1830s Belgian setting, banks functioned simultaneously as securitizers that expanded secondary markets for corporate securities and as market-makers whose balance sheets absorbed the effects of those same markets. Market conditions therefore fed back into bank operations, indicating that alterations in financial architecture arise from cyclical as well as structural causes.

What carries the argument

The dual role of banks as securitizers and market-makers that generates bidirectional feedback between banks and securities markets.

If this is right

- Secondary markets for corporate securities can form through active bank intermediation rather than emerging independently of banks.

- Price movements in securities markets can alter bank balance sheets and lending behavior through market-making activities.

- Financial architecture evolves through repeated interactions between intermediaries and markets instead of remaining fixed by initial conditions.

- Short-term economic fluctuations can shift the relative roles of banks and markets in financing industrial activity.

Where Pith is reading between the lines

- The same feedback pattern could be tested in other nineteenth-century cases of rapid corporate financing.

- Contemporary episodes of securitization might be examined for similar market-making effects on intermediary stability.

- Regulatory design could account for how market conditions propagate back to the institutions that create securities.

Load-bearing premise

The mechanisms of bank securitization and market-making observed in one short historical episode represent general processes that operate across different economies and periods.

What would settle it

A documented case from another early-industrializing country in which banks issued corporate securities yet did not subsequently trade or hold those securities in response to price changes.

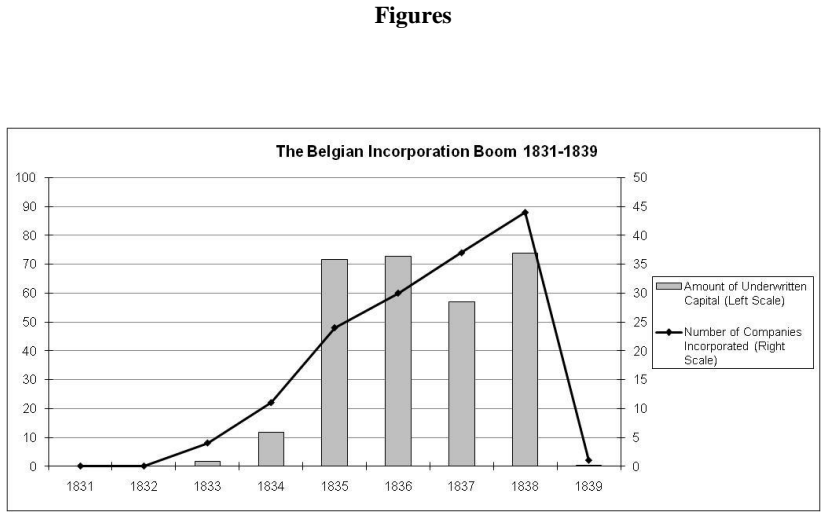

Figures

read the original abstract

Recent developments in the literature on financial architecture suggest that banks and markets not only coexist, but also coevolve in ways that are non-neutral from the viewpoint of optimality. This article aims to analyse the concrete mechanisms of this coevolution by focusing on a very relevant case study: Belgium (the first Continental country to industrialize) at the time of the very first emergence of a modern financial system (the 1830s). The article shows that intermediaries played a crucial role in developing secondary securities markets (as banks acted as securitizers), but market conditions also had a strong feedback on banks' balance sheets and activities (as banks also acted as market-makers for the securities they had issued). The findings suggest that not only structural, but also cyclical factors can be important determinants of changes in financial architecture.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper examines the coevolution of banks and corporate securities markets during Belgium's industrial take-off in the 1830s. It argues that banks acted as securitizers, playing a crucial role in developing secondary securities markets, while also serving as market-makers for the securities they issued; this created feedback effects on banks' balance sheets and activities. The analysis suggests that both structural and cyclical factors shape changes in financial architecture.

Significance. If supported by the archival evidence, the case study supplies a concrete historical illustration of non-neutral bank-market coevolution, documenting specific mechanisms of securitization and market-making with balance-sheet feedbacks. This adds to the literature on financial architecture by showing how cyclical conditions can influence institutional development alongside structural factors, without advancing formal models or universality claims.

minor comments (3)

- The abstract and introduction would benefit from an explicit statement of the primary archival sources and selection criteria used to document the securitizer and market-maker roles.

- A timeline table or figure summarizing key events, bank activities, and market developments in the 1830s would improve readability and help readers track the coevolutionary sequence.

- The discussion of cyclical versus structural factors could be sharpened by distinguishing which observed mechanisms are tied to the specific 1830s Belgian context versus those presented as potentially portable.

Simulated Author's Rebuttal

We thank the referee for their positive assessment of the manuscript and the recommendation for minor revision. The referee's summary correctly captures the paper's core argument on the coevolution of banks and securities markets through securitization and market-making in 1830s Belgium.

Circularity Check

No significant circularity in qualitative historical case study

full rationale

The paper is a qualitative historical narrative documenting specific mechanisms of bank-market coevolution in 1830s Belgium based on archival evidence. It contains no equations, formal derivations, fitted parameters, or quantitative models. Claims about banks acting as securitizers and market-makers with feedback effects rest on historical documentation rather than self-definitional reductions, fitted inputs renamed as predictions, or load-bearing self-citation chains. The cautious suggestion that cyclical factors can matter is an interpretation of the single case, not a derivation that reduces to prior inputs by construction. The argument is self-contained against external benchmarks of archival evidence.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Securitization without Risk Transfer

- Acharya, Viral V., Philipp Schnabl, and Gustavo Suarez (2013), “Securitization without Risk Transfer”, Journal of Financial Economics, 107, pp. 515-36. - Allen, Franklin, and Douglas Gale (2000), Comparing Financial Systems , Cambridge (Mass.): MIT Press. - Amihud, Yakov, Haim Mendelson, and Lasse H. Pedersen (2005), “Liquidity and Asset Prices”, Founda...

work page 2013

-

[2]

Financial Markets in Development, and the Development of Financial Markets

- Greenwood, Jeremy, and Bruce D. Smith (1997), “Financial Markets in Development, and the Development of Financial Markets”, Journal of Economic Dyn amics and Control, 21, pp. 145-81. - Gurley, John G., and Edward S. Shaw (1955), “Financial Aspects of Economic Development”, American Economic Review, 45:4, pp. 515-38. 32 - Hellmann, Thomas, Laura Lindsey,...

work page 1997

-

[3]

- Mokyr, Joel (1976), Industrialization in the Low Countries 1795 -1850, New Haven - London: Yale University Press. - O’Hara, Maureen (200 3), “Liquidity and Price Discovery”, Journal of Finance, 58:4, pp. 1335-1354. - Petersen, Mitchell A., and Raghuram G. Rajan (1995), “The Effect of Credit Market Competition on Lending Relationships”, Quarterly Journal...

work page 1976

-

[4]

- Sylla, Richard (1991), “The Role of Banks”, in Richard Sylla and Gianni Toniolo (eds.), Patterns of European Industrializ ation: The Nineteenth Century , London and New York: Routledge, pp. 45-63. - Tilly, Richard (1966), Financial Institutions and Industrialization in the Rhineland 1815-1870, Madison and Milwaukee: University of Wisconsin Press. - Ugol...

work page 1991

-

[5]

Finances, 307/1/15, A Table 1: Summary of series and sources in author’s database

BdB: Breakdown of loans on securities by type of collateral 1 bank, 1 date 1838 Archives Générales du Royaume (Brussels), Fonds Min. Finances, 307/1/15, A Table 1: Summary of series and sources in author’s database. 37 Mons Brussels Rest of Belgium TOTAL 1830 63.3 27.3 13.7 104.3 1831 20.5 35.9 0.0 56.4 1832 8.9 24.6 1.3 34.8 1833 6.0 22.6 1.6 30.2 1834 5...

work page 1974

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.