0

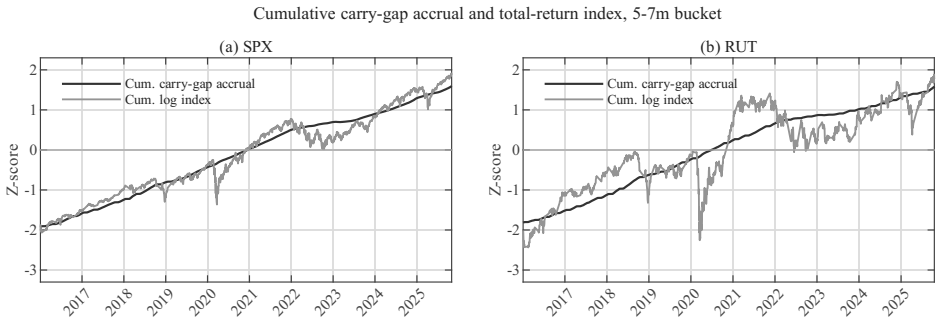

Drift term sharpens put-call parity fit in SPX options

The P behind Q: Empirical Evidence from Physical Drift in Put-Call Parity

Empirical tests show adding physical drift to the risk adjustment explains carry gaps better, indicating margin costs in enforcement.

full image

full image

abstract click to expand

Put-call parity is exact as a terminal-payoff identity, yet its market enforcement is path-dependent and capital-using. This paper examines whether physical-measure drift is reflected in the carry gap, defined as the annualized wedge between option-implied and OIS-implied discounting, using SPX and RUT European index options. I derive a drift-preserving extension of the GBM implementation-risk term that adds an (r\mu\tau) component to the standard (r\sigma\sqrt{\tau}) path-risk component. The drift input (\mu) is measured by a lagged rolling-OLS trend proxy and should not be interpreted as an observed expected return. Empirically, the drift term improves both in-sample and leave-one-year-out fit, especially for SPX, consistent with drift-sensitive margin burden in parity enforcement rather than a failure of no-arbitrage.