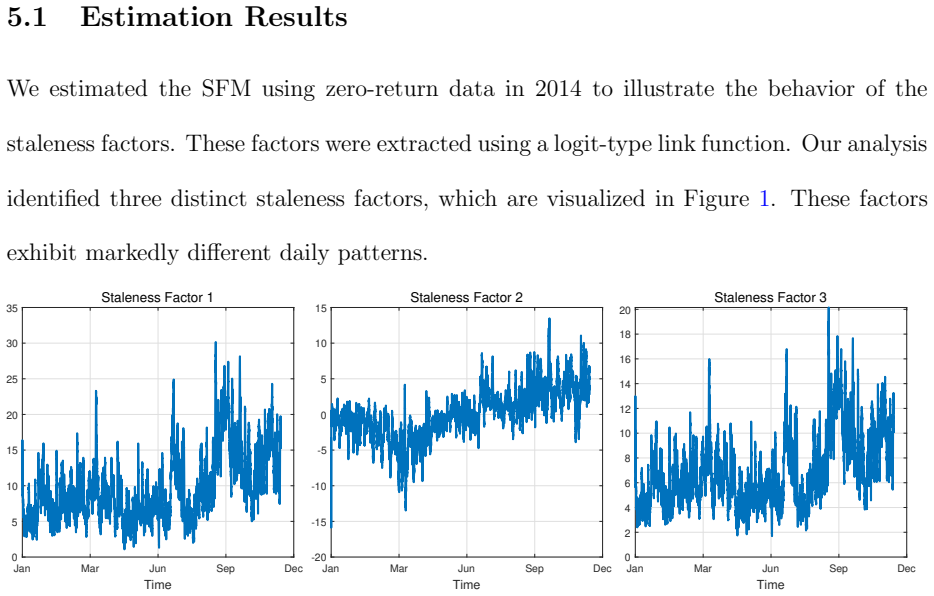

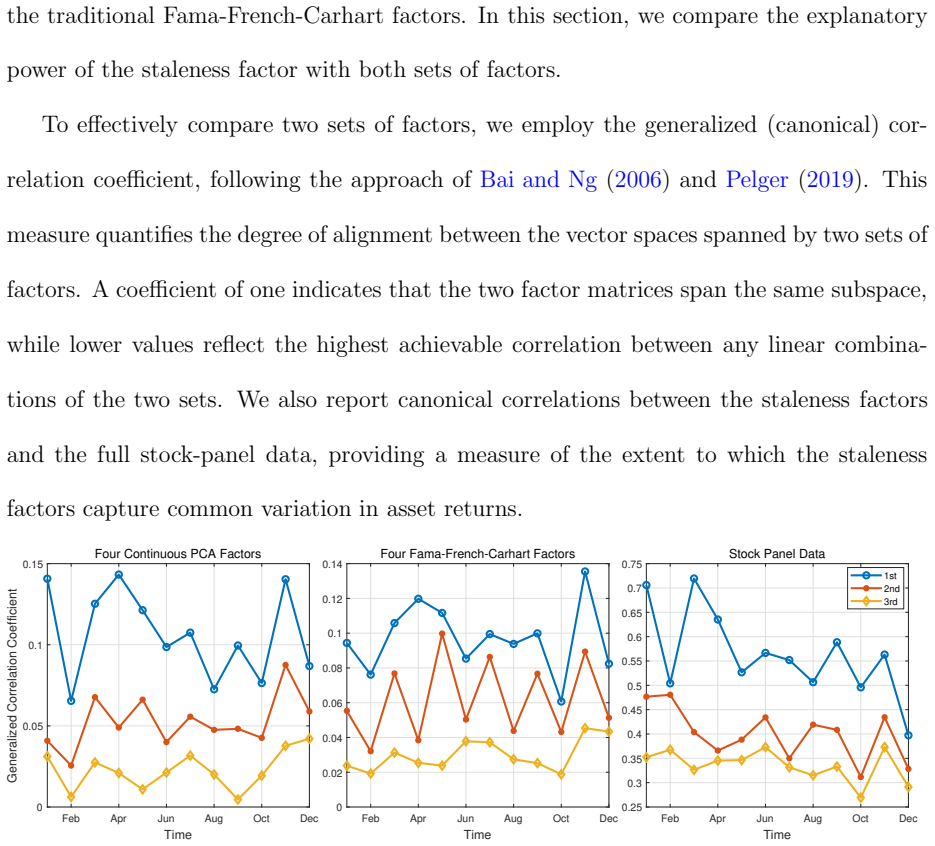

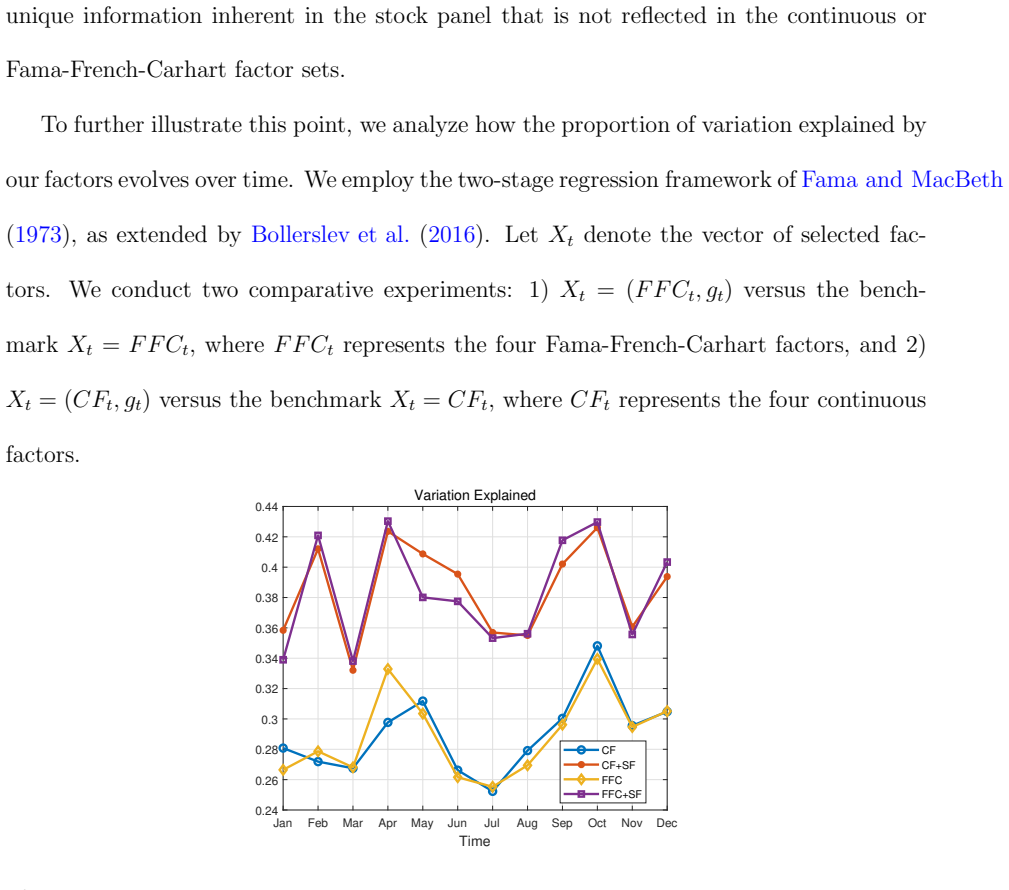

Staleness Factors and Volatility Estimation at High Frequencies

Pith reviewed 2026-05-23 19:31 UTC · model grok-4.3

The pith

A price staleness factor model removes downward bias from high-frequency co-volatility estimates and remains robust as both assets and observations grow large.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

We propose a price staleness factor model that accounts for pervasive market friction across assets and incorporates relevant covariates. Using large-panel high-frequency data, we derive the maximum likelihood estimators of the regression coefficients, the nonstationary factors, and their loading parameters. These estimators recover the time-varying price staleness probabilities. We develop asymptotic theory in which both the dimension d and the sampling frequency n tend to infinity. Using a local principal component analysis approach, we find that the efficient price co-volatilities are biased downward due to the presence of staleness. We provide bias-corrected estimators for both the spot,

What carries the argument

The price staleness factor model, which expresses the probability of a stale price observation as a low-dimensional nonstationary factor structure plus covariates and supplies the MLE that feeds into local-PCA bias correction for co-volatilities.

If this is right

- Bias-corrected estimators deliver consistent spot and integrated systematic and idiosyncratic co-volatilities even when prices are stale.

- Integrated plug-in estimates converge at rate n to the minus one half without further correction terms.

- Local PCA estimates converge at the slower rate n to the minus one fourth yet remain consistent after the staleness adjustment.

- The recovered staleness factor carries explanatory power for cross-sectional risk premia.

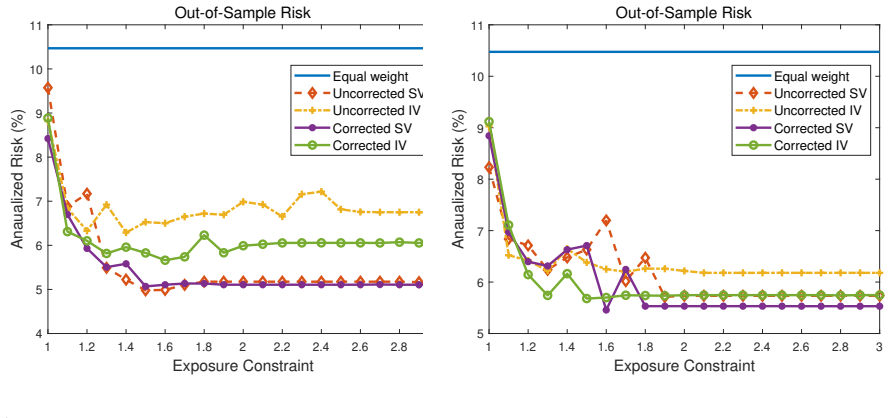

- Staleness correction lowers out-of-sample portfolio risk relative to uncorrected estimates.

Where Pith is reading between the lines

- Portfolio optimizers that ingest the corrected covariance matrices may achieve lower realized tracking error in markets where trading halts are frequent.

- The same factor structure could be tested on lower-frequency daily data to check whether staleness effects persist outside the high-frequency regime.

- Risk premia regressions could be re-run with the staleness factor included as an additional regressor to quantify its incremental pricing contribution.

- The convergence-rate distinction between plug-in and LPCA versions suggests that aggregation over time may be more efficient than local estimation when staleness is present.

Load-bearing premise

The price staleness process is pervasive across assets and admits a low-dimensional factor structure plus observed covariates that permits consistent MLE recovery of time-varying probabilities.

What would settle it

If the bias-corrected co-volatility matrices, when used in out-of-sample portfolio construction on the same high-frequency panel, produce higher realized risk than the uncorrected versions, the claimed robustness would be refuted.

Figures

read the original abstract

In this paper, we propose a price staleness factor model that accounts for pervasive market friction across assets and incorporates relevant covariates. Using large-panel high-frequency data, we derive the maximum likelihood estimators of the regression coefficients, the nonstationary factors, and their loading parameters. These estimators recover the time-varying price staleness probabilities. We develop asymptotic theory in which both the dimension $d$ and the sampling frequency $n$ tend to infinity. Using a local principal component analysis (LPCA) approach, we find that the efficient price co-volatilities (systematic and idiosyncratic) are biased downward due to the presence of staleness. We provide bias-corrected estimators for both the spot and integrated systematic and idiosyncratic co-volatilities, and prove that these estimators are robust to data staleness. Interestingly, besides their dependence on the dimensionality $d$, the integrated plug-in estimates converge at a rate of $n^{-1/2}$ without requiring correcting term, whereas the local PCA estimates converge at a slower rate of $n^{-1/4}$. This validates the aggregation efficiency achieved through nonlinear, nonstationary factor analysis via maximum likelihood estimation. Numerical experiments justify our theoretical findings. Empirically, we demonstrate that the staleness factor provides unique explanatory power for cross-sectional risk premia, and that the staleness correction reduces out-of-sample portfolio risk.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a price staleness factor model incorporating covariates and a low-dimensional pervasive factor structure for high-frequency data. It derives MLEs for regression coefficients, nonstationary factors, and loadings to recover time-varying staleness probabilities under joint d,n→∞ asymptotics. Using LPCA, it identifies downward bias in efficient-price co-volatilities due to staleness and constructs bias-corrected estimators for both spot and integrated systematic/idiosyncratic co-volatilities, proving robustness. It asserts convergence rates of n^{-1/2} for integrated plug-in estimators (no correction term needed) versus n^{-1/4} for LPCA estimators. Numerical experiments support the theory, and empirical results claim the staleness factor explains cross-sectional risk premia while the correction reduces out-of-sample portfolio risk.

Significance. If the results hold, the work provides a structured way to correct for pervasive data staleness in large-panel high-frequency volatility estimation, a practically relevant issue. The explicit rate distinction between plug-in and LPCA estimators, together with the MLE treatment of nonstationary factors, is a technical contribution. The empirical link to risk premia offers a potential new covariate for asset-pricing models.

major comments (2)

- [Abstract (model statement) and asymptotic theory section] The central robustness claim for the bias-corrected co-volatility estimators (both spot and integrated) and the asserted rates (n^{-1/2} plug-in vs. n^{-1/4} LPCA) rest on consistent MLE recovery of the time-varying staleness probabilities. This recovery is possible only under the exact low-dimensional pervasive factor structure plus observed covariates; the manuscript supplies no separate identification result or robustness-to-misspecification analysis for this modeling assumption.

- [Empirical application section] The empirical claim that the staleness factor supplies unique explanatory power for cross-sectional risk premia is obtained by fitting the same factor model to the same high-frequency panel used for the volatility estimation; this introduces circularity that weakens the interpretation of incremental explanatory power.

minor comments (2)

- [Abstract] The abstract states that MLE, asymptotic theory, and bias-corrected estimators are derived and proved robust, yet the supporting derivations, data-exclusion rules, and error-bar details are not visible in the provided text; these should be supplied explicitly.

- [Notation and definitions] Notation for spot versus integrated co-volatilities and for the distinction between systematic and idiosyncratic components should be made uniform across sections to avoid reader confusion.

Simulated Author's Rebuttal

We thank the referee for the constructive comments. We address the two major comments point by point below, clarifying the role of the model assumptions and the structure of the empirical analysis.

read point-by-point responses

-

Referee: [Abstract (model statement) and asymptotic theory section] The central robustness claim for the bias-corrected co-volatility estimators (both spot and integrated) and the asserted rates (n^{-1/2} plug-in vs. n^{-1/4} LPCA) rest on consistent MLE recovery of the time-varying staleness probabilities. This recovery is possible only under the exact low-dimensional pervasive factor structure plus observed covariates; the manuscript supplies no separate identification result or robustness-to-misspecification analysis for this modeling assumption.

Authors: The consistency of the MLE for recovering the time-varying staleness probabilities, and therefore the robustness and rates of the bias-corrected co-volatility estimators, is established under the maintained price staleness factor model that includes the low-dimensional pervasive factor structure together with the observed covariates. Identification of the parameters is obtained directly through the likelihood equations and the joint d, n → ∞ asymptotics developed in the asymptotic theory section; the MLE procedure itself delivers the required consistency without a separate identification theorem being stated apart from the convergence results. The paper does not contain a robustness-to-misspecification analysis, which would constitute an extension beyond the present scope. We will add a brief remark in the revised manuscript emphasizing that all claims are conditional on correct specification of the factor structure. revision: partial

-

Referee: [Empirical application section] The empirical claim that the staleness factor supplies unique explanatory power for cross-sectional risk premia is obtained by fitting the same factor model to the same high-frequency panel used for the volatility estimation; this introduces circularity that weakens the interpretation of incremental explanatory power.

Authors: The staleness factor model is estimated on the high-frequency panel solely to produce the bias-corrected volatility measures. The estimated time-varying staleness probabilities are then used as a covariate in a distinct cross-sectional regression that examines their ability to explain risk premia. This two-step separation keeps the volatility-correction exercise independent of the asset-pricing test. While the same underlying panel is necessarily employed, the risk-premia regression is not a re-application of the factor model for volatility purposes but rather an out-of-sample economic validation. We will revise the empirical section to make this separation explicit and to report the incremental R-squared relative to benchmark factors. revision: partial

Circularity Check

No circularity; derivation follows from model assumptions and standard asymptotics

full rationale

The paper defines a staleness factor model, derives MLE for its parameters under joint d,n asymptotics, applies LPCA to obtain bias-corrected co-volatility estimators, and states convergence rates that follow directly from the model and standard high-dimensional theory. No step reduces by construction to a fitted input renamed as prediction, a self-citation chain, or a self-definitional equivalence. The empirical application of the fitted factors to risk premia is a separate demonstration rather than a load-bearing prediction forced by the estimation procedure itself. The derivation chain is therefore self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

free parameters (2)

- regression coefficients

- loading parameters

axioms (2)

- domain assumption Both dimension d and sampling frequency n tend to infinity

- domain assumption Staleness is pervasive across assets and admits a factor-plus-covariate structure

invented entities (1)

-

price staleness factor

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Ait-Sahalia, Y. and D. Xiu (2017). Using principal component analysis to estimate a high dimensional factor model with high-frequency data. Journal of Econometrics 201 (2), 384–399. A ¨ ıt-Sahalia, Y. and D. Xiu (2019). Principal component analysis of h igh-frequency data. Journal of the American Statistical Association 114 (525), 287–303

work page 2017

-

[2]

Bai, J. and S. Ng (2006). Evaluating latent and observed factors in macroeconomics and finance. Journal of Econometrics 131 (1-2), 507–537

work page 2006

-

[3]

Bandi, F. M., A. Kolokolov, D. Pirino, and R. Ren` o (2020). Zeros. Management Sci- ence 66 (8), 3466–3479. 33

work page 2020

-

[4]

Bandi, F. M., A. Kolokolov, D. Pirino, and R. Ren` o (2023). Discontinu ous trading in continuous-time econometrics. Available at SSRN 4351618

work page 2023

-

[5]

Bandi, F. M., D. Pirino, and R. Reno (2017). Excess idle time. Econometrica 85 (6), 1793–1846

work page 2017

-

[6]

Bandi, F. M., D. Pirino, and R. Ren` o (2024). Systematic staleness. Journal of Economet- rics 238 (1), 105522

work page 2024

-

[7]

Bollerslev, T., S. Z. Li, and V. Todorov (2016). Roughing up beta: Co ntinuous versus discontinuous betas and the cross section of expected stock ret urns. Journal of Financial Economics 120 (3), 464–490

work page 2016

-

[8]

Chen, D. (2024). High frequency principal component analysis bas ed on correlation ma- trix that is robust to jumps, microstructure noise and asynchron ous observation times. Journal of Econometrics 240 (1), 105701

work page 2024

-

[9]

Chen, D., L. Feng, P. A. Mykland, and L. Zhang (2024). High dimensio nal regression coefficient test with high frequency data. Journal of Econometrics , 105812

work page 2024

-

[10]

Chen, D., P. A. Mykland, and L. Zhang (2020). The five trolls under t he bridge: Principal component analysis with asynchronous and noisy high frequency da ta. Journal of the American Statistical Association 115 (532), 1960–1977

work page 2020

-

[11]

Fama, E. F. and J. D. MacBeth (1973). Risk, return, and equilibrium : Empirical tests. Journal of Political Economy 81 (3), 607–636

work page 1973

- [12]

-

[13]

Fan, J., Y. Liao, and M. Mincheva (2013). Large covariance estimat ion by thresholding principal orthogonal complements. Journal of the Royal Statistical Society Series B: Statistical Methodology 75 (4), 603–680

work page 2013

-

[14]

Hall, P. and C. C. Heyde (2014). Martingale limit theory and its application . Academic press. 34

work page 2014

-

[15]

Hu, J., W. Li, Z. Liu, and W. Zhou (2019). High-dimensional covarianc e matrices in elliptical distributions with application to spherical test. The Annals of Statistics 47 (1), 527–555

work page 2019

-

[16]

Jacod, J. and M. Rosenbaum (2013). Quarticity and other functio nals of volatility: Efficient estimation. The Annals of Statistics 41 (3), 1462–1484

work page 2013

-

[17]

Jacod, J. and V. Todorov (2014). Efficient estimation of integrate d volatility in presence of infinite variation jumps. The Annals of Statistics 42 (3), 1029–1069

work page 2014

-

[18]

Kim, D., X. Kong, C. Li, and Y. Wang (2018). Adaptive thresholding fo r large volatility ma- trix estimation based on high-frequency financial data. Journal of Econometrics 203 (1), 69–79

work page 2018

-

[19]

Kolokolov, A., G. Livieri, and D. Pirino (2020). Statistical inferences for price staleness. Journal of Econometrics 218 (1), 32–81

work page 2020

-

[20]

Kong, X. (2017). On the number of common factors with high-freq uency data. Biometrika 104 (2), 397–410

work page 2017

-

[21]

Kong, X. (2018). On the systematic and idiosyncratic volatility with la rge panel high- frequency data. The Annals of Statistics 46 (3), 1077–1108

work page 2018

-

[22]

Kong, X., J. Lin, C. Liu, and G. Liu (2023). Discrepancy between glob al and local prin- cipal component analysis on large-panel high-frequency data. Journal of the American Statistical Association 118 (542), 1333–1344

work page 2023

-

[23]

Li, D., O. Linton, and H. Zhang (2024). Estimating factor-based sp ot volatility matrices with noisy and asynchronous high-frequency data. arXiv preprint arXiv:2403.06246

-

[24]

Li, J., Y. Liu, and D. Xiu (2019). Efficient estimation of integrated vola tility functionals via multiscale jackknife. The Annals of Statistics 47 (1), 156–176

work page 2019

-

[25]

Liu, C. and C. Y. Tang (2014). A quasi-maximum likelihood approach fo r integrated covariance matrix estimation with high frequency data. Journal of Econometrics 180 (2), 217–232. 35

work page 2014

-

[26]

Liu, Z. and H. Zhu (2024). Bias-corrected realized covariation in th e presence of price staleness. Available at SSRN 4777396

work page 2024

-

[27]

Mancini, C. (2009). Non-parametric threshold estimation for mode ls with stochastic diffu- sion coefficient and jumps. Scandinavian Journal of Statistics 36 (2), 270–296

work page 2009

-

[28]

Mykland, P. A. and L. Zhang (2009). Inference for continuous se mimartingales observed at high frequency. Econometrica 77 (5), 1403–1445

work page 2009

-

[29]

Pelger, M. (2019). Large-dimensional factor modeling based on hig h-frequency observations. Journal of Econometrics 208 (1), 23–42

work page 2019

-

[30]

Pelger, M. (2020). Understanding systematic risk: A high-freque ncy approach. The Journal of Finance 75 (4), 2179–2220

work page 2020

-

[31]

Wang, Y. and J. Zou (2010). Vast volatility matrix estimation for high -frequency financial data. The Annals of Statistics 38 (2), 943–978

work page 2010

-

[32]

Zhu, H. and Z. Liu (2024). On bivariate time-varying price staleness . Journal of Business & Economic Statistics 42 (1), 229–242. 36

work page 2024

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.