Optimal investment and consumption under forward utilities with relative performance concerns

Pith reviewed 2026-05-19 08:14 UTC · model grok-4.3

The pith

Forward relative performance processes with CRRA wealth utility necessarily have consumption utility of the same form and risk aversion.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The consistency assumption defining forward relative performance processes leads to a sufficient characterization of such processes with the mean of Stochastic HJB equations, which highlights the link between wealth and consumption utility. In particular, forward relative performance processes with a wealth utility of CRRA type and separable time and space dependence necessarily have a consumption utility of the same form, with the same risk aversion parameter. This characterization gives a better understanding of the drift condition ensuring time consistency. In this setting, closed forms of the Nash equilibrium are established for both the n-player and mean-field problems.

What carries the argument

The mean of Stochastic HJB equations arising from the consistency assumption on forward relative performance processes, which links the wealth and consumption utilities.

If this is right

- Closed-form Nash equilibrium strategies for the finite n-player game with relative performance concerns.

- Closed-form Nash equilibrium in the corresponding mean-field limit.

- Explicit drift condition that ensures time consistency of the forward processes.

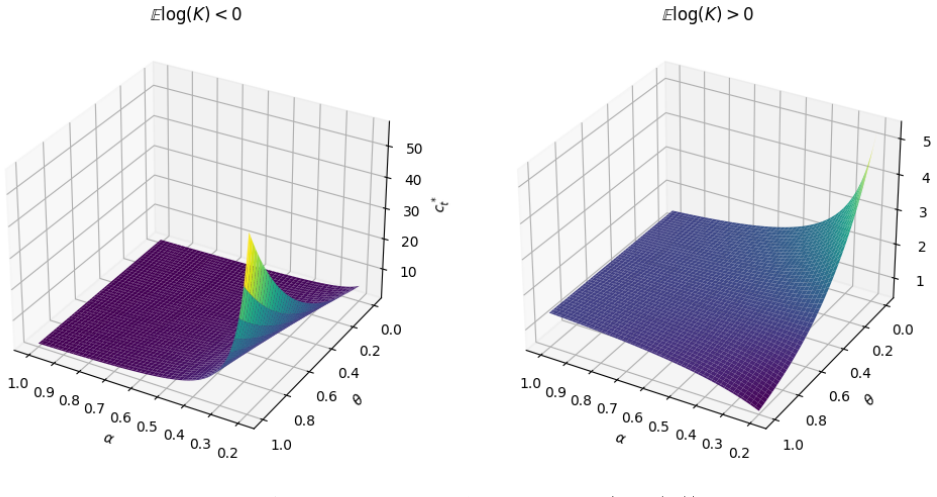

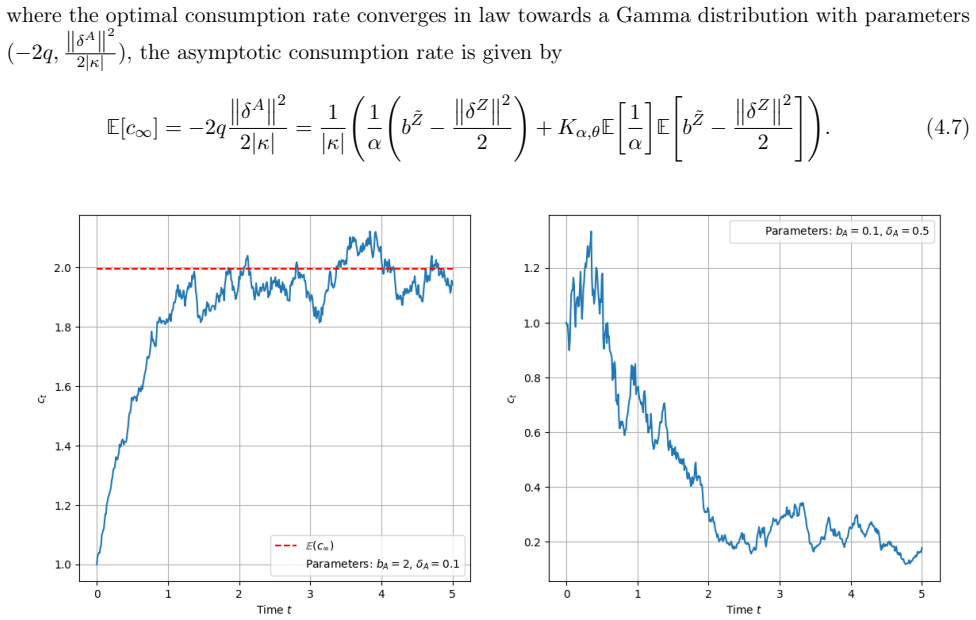

- Numerical examples of optimal investment and consumption paths under the linked utilities.

Where Pith is reading between the lines

- The same-form requirement may simplify solving dynamic consumption problems in other competitive market settings.

- The mean-field limit supplies an approximation for large populations of investors facing relative performance concerns.

- The utility link could be checked against data on whether consumption patterns align with wealth risk aversion in competitive environments.

Load-bearing premise

The consistency assumption defining forward relative performance processes is sufficient to characterize the processes via the mean of Stochastic HJB equations and to link wealth and consumption utilities.

What would settle it

A counter-example showing a forward relative performance process with CRRA wealth utility of separable time and space dependence but consumption utility of different form or risk aversion parameter would disprove the necessity of the link.

Figures

read the original abstract

We study a n-player and mean-field portfolio optimization problem under relative performance concerns with non-zero volatility, for wealth and consumption. The consistency assumption defining forward relative performance processes leads to a sufficient characterization of such processes with mean of a Stochastic HJB equations, which highlights the link between wealth and consumption utility, and also characterizes the optimal strategies. In particular, forward relative performance processes with a wealth utility of CRRA type and separable time and space dependence necessarily have a consumption utility of the same form, with the same risk aversion parameter. This characterization gives a better understanding of the drift condition ensuring time consistency. In this setting, we establish closed form of the Nash equilibrium for both the n-player and mean eld problems. We also provide some numerical examples.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript studies n-player and mean-field portfolio optimization problems involving both investment and consumption under relative performance concerns with non-zero volatility. Using a consistency assumption for forward relative performance processes, it provides a characterization through the mean of stochastic HJB equations that links the wealth and consumption utilities. In particular, it asserts that CRRA wealth utilities with separable time and space dependence imply consumption utilities of the same CRRA form with the same risk aversion parameter. Closed-form expressions for the Nash equilibria in both the finite and mean-field settings are derived, along with numerical examples.

Significance. If the central characterization holds, the paper offers a valuable contribution to stochastic control and mean-field games in finance by clarifying the structure of time-consistent forward utilities with relative concerns and delivering explicit optimal strategies. This could facilitate further analysis of competitive consumption-investment problems. The provision of closed-form solutions and numerical illustrations strengthens the practical relevance of the results.

major comments (2)

- [Abstract and characterization via mean of stochastic HJB] Abstract and the main characterization result: the claim that forward relative performance processes with a wealth utility of CRRA type and separable time and space dependence necessarily have a consumption utility of the same form with the same risk aversion parameter is asserted to follow from taking the mean of the stochastic HJB equations. However, with non-zero volatility in relative performance, the cross terms in the generator could permit other consumption utility forms (or different risk aversion) that still satisfy the drift condition for consistency, and the manuscript does not supply an explicit uniqueness argument for the resulting PDE system to exclude such possibilities.

- [Section on stochastic HJB mean and consistency condition] The link between wealth and consumption utilities is derived directly from the consistency assumption itself. To establish that this link is not tautological, an independent verification is required showing that the mean equation uniquely pins down the consumption utility to the claimed CRRA form whenever the wealth utility is separable CRRA, particularly when volatilities couple the processes non-separably.

minor comments (2)

- [Notation and preliminaries] The notation for the relative performance processes and the precise definition of the 'mean' operator applied to the stochastic HJB equations would benefit from additional explicit definitions early in the manuscript.

- [Numerical examples] In the numerical examples section, further discussion of how the equilibria respond to changes in the relative performance volatility parameters would improve interpretability of the figures.

Simulated Author's Rebuttal

We are grateful to the referee for the insightful comments on our paper. These have helped us clarify the presentation of our main results. We respond to the major comments point by point below.

read point-by-point responses

-

Referee: Abstract and the main characterization result: the claim that forward relative performance processes with a wealth utility of CRRA type and separable time and space dependence necessarily have a consumption utility of the same form with the same risk aversion parameter is asserted to follow from taking the mean of the stochastic HJB equations. However, with non-zero volatility in relative performance, the cross terms in the generator could permit other consumption utility forms (or different risk aversion) that still satisfy the drift condition for consistency, and the manuscript does not supply an explicit uniqueness argument for the resulting PDE system to exclude such possibilities.

Authors: We thank the referee for this observation. The mean of the stochastic HJB equations provides a deterministic PDE that the consumption utility must satisfy to ensure consistency. Given the CRRA form and separability in time and space for the wealth utility, this PDE can be solved explicitly, and the only solution that holds for the given structure, including the volatility cross terms, is the matching CRRA consumption utility with the same risk aversion. While the manuscript derives this directly, we acknowledge that an explicit uniqueness statement would strengthen the argument. We have revised the manuscript to include a brief uniqueness verification in the relevant section. revision: yes

-

Referee: The link between wealth and consumption utilities is derived directly from the consistency assumption itself. To establish that this link is not tautological, an independent verification is required showing that the mean equation uniquely pins down the consumption utility to the claimed CRRA form whenever the wealth utility is separable CRRA, particularly when volatilities couple the processes non-separably.

Authors: The consistency assumption is the starting point, but the specific form is pinned down by solving the resulting mean PDE under the separability hypothesis. The non-separable coupling through volatilities is incorporated into the generator, yet the CRRA structure ensures that the consumption utility must take the same form to balance the equation. To address the concern about tautology, we have added an independent verification step in the revised version, demonstrating uniqueness for the PDE system. revision: yes

Circularity Check

Consistency assumption directly yields consumption utility form via stochastic HJB mean

specific steps

-

self definitional

[Abstract]

"The consistency assumption defining forward relative performance processes leads to a sufficient characterization of such processes with mean of a Stochastic HJB equations, which highlights the link between wealth and consumption utility... In particular, forward relative performance processes with a wealth utility of CRRA type and separable time and space dependence necessarily have a consumption utility of the same form, with the same risk aversion parameter."

The consistency assumption is the definition of the forward processes; the paper then asserts that this assumption plus the mean of the stochastic HJB necessarily produces the identical CRRA consumption utility. The 'necessarily' claim therefore reduces to a restatement of the assumption's consequences rather than an independent derivation that could be falsified outside the assumption.

full rationale

The paper states that the consistency assumption defining forward relative performance processes leads to a characterization via the mean of stochastic HJB equations, which in turn forces the consumption utility to match the CRRA form and risk aversion of the wealth utility under separability. This link is presented as a necessary consequence, but the derivation reduces to the assumption itself enforcing the drift condition for time-consistency. No independent uniqueness theorem or external verification is quoted to show that other forms are excluded when relative performance volatility is non-zero. The central claim therefore has partial circular character as the result is largely by construction from the defining assumption rather than an independent derivation.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Consistency assumption defining forward relative performance processes

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

forward relative performance processes with a wealth utility of CRRA type and separable time and space dependence necessarily have a consumption utility of the same form, with the same risk aversion parameter

-

IndisputableMonolith/Foundation/ArithmeticFromLogic.leanLogicNat ≃ Nat recovery unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

consistency assumption defining forward relative performance processes leads to a sufficient characterization ... with mean of a Stochastic HJB equations

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

Competition in fund man- agement and forward relative performance criteria

Michail Anthropelos, Tianran Geng, and Thaleia Zariphopoulou. Competition in fund man- agement and forward relative performance criteria. SIAM Journal on Financial Mathematics, 13(4):1271–1301, 2022

work page 2022

-

[2]

Dirk Becherer and Stefanie Hesse. Common noise by random measures: Mean-field equilibria for competitive investment and hedging.arXiv preprint arXiv:2408.01175, 2024

-

[3]

Epstein-zin preferences under for- ward performance

Zakaria Bensaid, Anis Matoussi, and Thaleia Zariphopoulou. Epstein-zin preferences under for- ward performance. Workingpaper, 2025

work page 2025

-

[4]

René Carmona, François Delarue, et al.Probabilistic theory of mean fieldgames with applications I-II. Springer, 2018

work page 2018

-

[5]

Mean field games with common noise.The Annals of Probability, 44(6):3740–3803, 2016

René Carmona, François Delarue, and Daniel Lacker. Mean field games with common noise.The Annals of Probability, 44(6):3740–3803, 2016

work page 2016

-

[6]

Wing Fung Chong. Pricing and hedging equity-linked life insurance contracts beyond the clas- sical paradigm: The principle of equivalent forward preferences. Insurance: Mathematics and Economics, 88:93–107, 2019

work page 2019

-

[7]

Jodi Dianetti, Frank Riedel, and Lorenzo Stanca. Optimal consumption and investment under relative performance criteria with epstein-zin utility.arXiv preprint arXiv:2402.07698, 2024

-

[8]

Forward utilities and mean-field games under relative performance concerns

Goncalo Dos Reis and Vadim Platonov. Forward utilities and mean-field games under relative performance concerns. InFrom Particle Systems to Partial Differential Equations: International Conference,ParticleSystemsandPDEsVI,VII andVIII, 2017-2019VIII,pages227–251.Springer, 2021

work page 2017

-

[9]

Forward utility and market adjustments in relative investment-consumption games of many players

Goncalo Dos Reis and Vadim Platonov. Forward utility and market adjustments in relative investment-consumption games of many players. SIAM Journal on Financial Mathematics, 13(3):844–876, 2022

work page 2022

-

[10]

Nicole El Karoui, Caroline Hillairet, and Mohamed Mrad. Consistent utility of investment and consumption: a forward/backward spde viewpoint.Stochastics, 90(6):927–954, 2018

work page 2018

-

[11]

Nicole El Karoui, Caroline Hillairet, and Mohamed Mrad. Ramsey rule with forward/backward utility for long-term yield curves modeling.Decisions in Economics and Finance, 45(1):375–414, 2022

work page 2022

-

[12]

Nicole El Karoui and Mohamed Mrad. An exact connection between two solvable SDEs and a nonlinear utility stochastic PDE.SIAM Journal on Financial Mathematics, 4(1):697–736, 2013

work page 2013

-

[13]

Optimal investment under relative performance con- cerns

Gilles-Edouard Espinosa and Nizar Touzi. Optimal investment under relative performance con- cerns. Mathematical Finance, 25(2):221–257, 2015

work page 2015

-

[14]

Mean field portfolio games.Finance and Stochastics, 27(1):189–231, 2023

Guanxing Fu and Chao Zhou. Mean field portfolio games.Finance and Stochastics, 27(1):189–231, 2023. 40

work page 2023

-

[15]

Jean-Sébastien Giet, Pierre Vallois, and Sophie Wantz-Mézieres. The logistic sde. Theory of Stochastic Processes, 20(1):28–62, 2015

work page 2015

-

[16]

Caroline Hillairet, Sarah Kaakai, and Mohamed Mrad. Time-consistent pension policy with min- imum guarantee and sustainability constraint.Probability, Uncertainty and Quantitative Risk, pages 1–30, 2024

work page 2024

-

[17]

N-player and mean-field games in itô-diffusion markets with competitive or homophilous interaction

Ruimeng Hu and Thaleia Zariphopoulou. N-player and mean-field games in itô-diffusion markets with competitive or homophilous interaction. In Stochastic Analysis, Filtering, and Stochastic Optimization: A Commemorative Volume to Honor Mark HA Davis’sContributions, pages 209–

-

[18]

Minyi Huang, Roland P Malhamé, and Peter E Caines. Large population stochastic dy- namic games: closed-loop mckean-vlasov systems and the nash certainty equivalence principle. Communications in Information & Systems, 6(3):221 – 252, 2006

work page 2006

-

[19]

Nobuyuki Ikeda and Shinzo Watanabe.Stochastic differential equations and diffusion processes. Elsevier, 2014

work page 2014

-

[20]

A note on nonautonomous logistic equation with random perturbation

Daqing Jiang and Ningzhong Shi. A note on nonautonomous logistic equation with random perturbation. Journal of Mathematical Analysis and Applications, 303(1):164–172, 2005

work page 2005

-

[21]

Sigrid Kallblad. Black’s inverse investment problem and forward criteria with consumption.SIAM Journal on Financial Mathematics, 11(2):494–525, 2020

work page 2020

-

[22]

Ioannis Karatzas and Steven E Shreve.Methods of mathematical finance, volume 39. Springer, 1998

work page 1998

-

[23]

Stochastic flows and stochastic differential equations, volume 24

Hiroshi Kunita. Stochastic flows and stochastic differential equations, volume 24. Cambridge university press, 1997

work page 1997

-

[24]

Daniel Lacker and Agathe Soret. Many-player games of optimal consumption and investment under relative performance criteria.Mathematics and Financial Economics, 14(2):263–281, 2020

work page 2020

-

[25]

Daniel Lacker and Thaleia Zariphopoulou. Mean field and n-agent games for optimal investment under relative performance criteria.Mathematical Finance, 29(4):1003–1038, 2019

work page 2019

-

[26]

Guangqiang Lan and Jiang-Lun Wu. New sufficient conditions of existence, moment estimations and non confluence for sdes with non-lipschitzian coefficients. Stochastic Processes and their Applications, 124(12):4030–4049, 2014

work page 2014

-

[27]

Mean field games.Japanese journal of mathematics, 2(1):229–260, 2007

Jean-Michel Lasry and Pierre-Louis Lions. Mean field games.Japanese journal of mathematics, 2(1):229–260, 2007

work page 2007

-

[28]

Ambiguity aversion and incompleteness of financial markets

Sujoy Mukerji and Jean-Marc Tallon. Ambiguity aversion and incompleteness of financial markets. The Review of Economic Studies, 68(4):883–904, 2001

work page 2001

-

[29]

Investments and forward utilities.Technicalreport, 2006

Marek Musiela and Thaleia Zariphopoulou. Investments and forward utilities.Technicalreport, 2006. 41

work page 2006

-

[30]

Stochastic partial differential equations and portfolio choice

Marek Musiela and Thaleia Zariphopoulou. Stochastic partial differential equations and portfolio choice. InContemporary Quantitative Finance: Essays in Honour of Eckhard Platen, pages 195–

-

[31]

Kenneth Tsz Hin Ng and Wing Fung Chong. Optimal investment in defined contribution pension schemes with forward utility preferences.Insurance: Mathematics and Economics, 114:192–211, 2024

work page 2024

-

[32]

Wolf Wagner. Systemic liquidation risk and the diversity–diversification trade-off.The Journal of Finance, 66(4):1141–1175, 2011

work page 2011

-

[33]

Mean field and many-player games in ito-diffusion markets under forward performance criteria

Thaleia Zariphopoulou. Mean field and many-player games in ito-diffusion markets under forward performance criteria. Probability,Uncertainty and Quantitative Risk, 9(2):123–148, 2024. 42

work page 2024

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.