Risk-aware stochastic scheduling of multi-market energy storage systems

Pith reviewed 2026-05-18 03:08 UTC · model grok-4.3

The pith

Risk-constrained stochastic scheduling for energy storage trades lower expected profits for up to 1.5 million dollars in net risk benefits.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The paper claims that embedding conditional value-at-risk constraints inside a two-stage stochastic program for multi-market energy storage produces larger optimal capacities in integrated hydrogen systems and, in both hydrogen and battery case studies, yields risk-reduction benefits up to 1.5 million dollars that exceed the accompanying 500 thousand dollar decline in expected profits or rise in expected costs compared with risk-neutral optimization.

What carries the argument

Two-stage stochastic program with conditional value-at-risk (CVaR) constraints that fixes first-stage decisions such as unit capacities and then adjusts second-stage charge and discharge schedules once price scenarios are revealed while enforcing a chosen tail-risk probability limit.

If this is right

- Risk constraints force larger installed capacities in the integrated hydrogen system, raising capital cost while adding inventory that buffers price swings.

- Expected operating costs rise or expected profits fall as the risk-aversion parameter is tightened.

- The quantified risk-reduction value reaches up to 1.5 million dollars and exceeds the corresponding loss in expected reward in both studied systems.

Where Pith is reading between the lines

- The same scenario-generation and CVaR structure could be reused for storage assets that also face renewable-generation uncertainty.

- Regulated utilities might adopt the explicit risk limit to demonstrate compliance with financial-stability rules without needing proprietary risk models.

- Live testing with rolling price forecasts would reveal whether the modeled net benefit survives forecast error and market rule changes.

Load-bearing premise

A modest number of generated price trajectories must capture the essential range of future uncertainty and the chosen CVaR threshold must match the operator's actual tolerance for downside outcomes.

What would settle it

Running the resulting schedules on out-of-sample historical price series and finding that the realized reduction in tail losses falls short of the modeled 1.5 million dollar net benefit relative to risk-neutral operation would falsify the claimed advantage.

Figures

read the original abstract

Energy storage promotes the integration of renewables by operating with charge and discharge policies that balance an intermittent power supply. A key challenge in this emerging sector is how to optimize the operation of storage assets given future price uncertainties and the need to recover the costs of project finance while ensuring an attractive return on equity and hedging against downside risk. This study investigates the scheduling of energy storage assets under price uncertainty, with a focus on electricity markets. A two-stage stochastic risk-constrained approach is employed, whereby electricity price trajectories or specific power markets are observed, allowing for recourse in the schedule. Conditional value-at-risk is used to quantify risk in the optimization problems; this allows for explicit specification of a probabilistic risk limit. The proposed approach is tested in an integrated hydrogen system (IHS) and a battery energy storage system (BESS). In the joint design and operation context for the IHS, the risk constraint results in large installed unit capacities, increasing capital cost but enabling more inventory to buffer price uncertainty. In both case studies, there is an operational trade-off between risk and expected reward; this is reflected in higher expected costs (or lower expected profits) with increasing risk aversion. Despite the decrease in expected reward (up to 500\$k), both systems exhibit substantial benefits of increasing risk aversion (up to 1.5\$mn) with respect to risk-neutral settings. This work provides a general method to address uncertainties in energy storage scheduling, allowing operators to input their level of risk tolerance on asset decisions.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript develops a two-stage stochastic programming model incorporating CVaR risk constraints for the scheduling of energy storage assets across electricity markets under price uncertainty. It applies the framework to an integrated hydrogen system (IHS) in a joint design-operation setting and to a battery energy storage system (BESS), reporting that higher risk aversion increases expected costs or reduces expected profits (by up to $500k) while delivering risk-reduction benefits of up to $1.5mn relative to risk-neutral operation.

Significance. If the numerical results are robust, the work supplies a concrete, operator-tunable method for risk-aware multi-market storage scheduling that directly quantifies monetary trade-offs in two realistic case studies. The explicit CVaR formulation and reported dollar deltas provide actionable insight for hedging and project-finance decisions in renewable integration.

major comments (2)

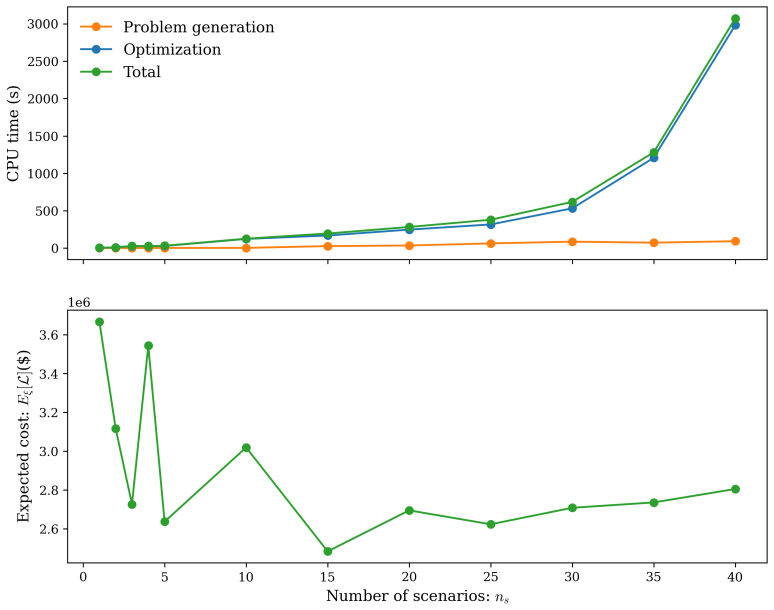

- [Risk-constrained approach and case studies] The headline monetary claims (up to $1.5mn risk-reduction benefit) rest on CVaR evaluated over a finite scenario set. The manuscript must supply the scenario-generation procedure, the number of trajectories, and out-of-sample price validation; absent these, the reported benefits cannot be distinguished from artifacts of scenario choice (see abstract paragraph on risk-constrained approach and the case-study results).

- [Model formulation and numerical experiments] The free parameters CVaR level alpha and scenario probabilities directly control the magnitude of the reported $500k penalty and $1.5mn benefit. The paper should state how these values were chosen and whether they were tuned to the observed outcomes rather than fixed a priori.

minor comments (2)

- [Abstract] The abstract refers to 'specific power markets' without naming them; adding the market names would clarify the multi-market scope.

- [Mathematical model] Notation for the recourse decisions and the CVaR auxiliary variables should be introduced once and used consistently in all equations and tables.

Simulated Author's Rebuttal

We thank the referee for the constructive comments, which help improve the clarity and robustness of our work. We address each major comment below and will revise the manuscript accordingly.

read point-by-point responses

-

Referee: [Risk-constrained approach and case studies] The headline monetary claims (up to $1.5mn risk-reduction benefit) rest on CVaR evaluated over a finite scenario set. The manuscript must supply the scenario-generation procedure, the number of trajectories, and out-of-sample price validation; absent these, the reported benefits cannot be distinguished from artifacts of scenario choice (see abstract paragraph on risk-constrained approach and the case-study results).

Authors: We agree that additional methodological transparency is needed to substantiate the reported monetary benefits. The current manuscript describes the two-stage stochastic program and CVaR formulation at a high level but does not fully detail the scenario generation or validation steps. In the revision we will add a dedicated subsection specifying the scenario-generation procedure (historical price sampling with ARIMA simulation followed by fast-forward reduction), the number of trajectories (100 generated, reduced to 50), and out-of-sample validation results on a held-out set of 100 price paths. These additions will confirm that the up-to-$1.5mn risk-reduction benefits are robust and not artifacts of the in-sample scenarios. revision: yes

-

Referee: [Model formulation and numerical experiments] The free parameters CVaR level alpha and scenario probabilities directly control the magnitude of the reported $500k penalty and $1.5mn benefit. The paper should state how these values were chosen and whether they were tuned to the observed outcomes rather than fixed a priori.

Authors: We concur that explicit justification of parameter choices is required. The CVaR level alpha was fixed at 0.95 a priori, following standard values in the energy-risk literature to capture the worst 5% of outcomes, and scenario probabilities were set uniformly after reduction. Neither parameter was tuned post-hoc to match the $500k or $1.5mn figures. In the revised manuscript we will state these choices explicitly in the model section and include a sensitivity table for alpha in {0.90, 0.95, 0.99} to demonstrate the trade-off behavior without outcome-driven adjustment. revision: yes

Circularity Check

No significant circularity; results are direct numerical outputs of stochastic optimization

full rationale

The paper formulates a two-stage stochastic risk-constrained optimization model using CVaR on a finite set of price trajectories, then solves it numerically for an integrated hydrogen system and a battery energy storage system. The reported trade-offs (higher expected costs or lower profits with increasing risk aversion, up to $500k reward penalty offset by up to $1.5mn risk-reduction benefit versus risk-neutral cases) are computed directly as differences between model solutions at varying risk levels. No parameters are fitted to data subsets and then renamed as predictions of related quantities; no self-citations provide load-bearing uniqueness theorems; no ansatzes are smuggled in; and the central claims do not reduce by construction to the input scenarios or risk parameters. The derivation chain is self-contained against the explicit modeling choices and external benchmarks of the case-study instances.

Axiom & Free-Parameter Ledger

free parameters (2)

- CVaR risk level alpha

- Scenario probabilities

axioms (2)

- standard math CVaR is a coherent risk measure and can be represented by a linear program when scenarios are discrete.

- domain assumption Price trajectories are exogenous and can be sampled independently of the storage decisions.

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

two-stage stochastic risk-constrained approach … Conditional value-at-risk is used to quantify risk … min c⊤X + Σ πs v(X,Ys,ξs) s.t. ζ + 1/(1-α) Σ πs ηs ≤ ε

-

IndisputableMonolith/Foundation/RealityFromDistinction.leanreality_from_one_distinction unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

risk-reward trade-off … higher expected costs … substantial benefits of increasing risk aversion (up to 1.5$mn)

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

IEA, Global energy review 2025, 2025.https://www.iea.org/reports/ global-energy-review-2025[Acessed: 2025-06-16]

work page 2025

-

[2]

D. S. Mallapragada, N. A. Sepulveda, J. D. Jenkins, Long-run system value of battery energy storage in future grids with increasing wind and solar generation, Applied Energy 275 (2020) 115390

work page 2020

-

[3]

S. Koohi-Fayegh, M. A. Rosen, A review of energy storage types, appli- cations and recent developments, Journal of Energy Storage 27 (2020) 101047

work page 2020

-

[4]

European Commission, Energy storage - underpinning a decarbonised and secure eu energy system, 2023. https://energy.ec.europa. eu/topics/research-and-technology/energy-storage_en [Acessed: 2025-06-16]

work page 2023

-

[5]

https://www.gov.uk/government/publications/ clean-power-2030-action-plan[Acessed: 2025-06-16]

UK Department for Energy Security and Net Zero, Clean power 2030 action plan, 2025. https://www.gov.uk/government/publications/ clean-power-2030-action-plan[Acessed: 2025-06-16]

work page 2030

-

[6]

A. Ajanovic, M. Sayer, R. Haas, The economics and the environmen- tal benignity of different colors of hydrogen, International Journal of Hydrogen Energy 47 (2022) 24136–24154. 33

work page 2022

-

[7]

D. S. Mallapragada, Y. Dvorkin, M. A. Modestino, D. V. Esposito, W. A. Smith, B.-M. Hodge, M. P. Harold, V. M. Donnelly, A. Nuz, C. Bloomquist, et al., Decarbonization of the chemical industry through electrification: Barriers and opportunities, Joule 7 (2023) 23–41

work page 2023

-

[8]

F. Ueckerdt, C. Bauer, A. Dirnaichner, J. Everall, R. Sacchi, G. Luderer, Potential and risks of hydrogen-based e-fuels in climate change mitigation, Nature Climate Change 11 (2021) 384–393

work page 2021

-

[9]

B. Lee, L. R. Winter, H. Lee, D. Lim, H. Lim, M. Elimelech, Pathways to a green ammonia future, ACS Energy Letters 7 (2022) 3032–3038

work page 2022

- [10]

- [11]

-

[12]

E. Pusceddu, B. Zakeri, G. C. Gissey, Synergies between energy arbitrage and fast frequency response for battery energy storage systems, Applied Energy 283 (2021) 116274

work page 2021

-

[13]

D. Krishnamurthy, C. Uckun, Z. Zhou, P. R. Thimmapuram, A. Botterud, Energy storage arbitrage under day-ahead and real-time price uncertainty, IEEE Transactions on Power Systems 33 (2017) 84–93

work page 2017

-

[14]

H. Nezamabadi, V. Vahidinasab, Arbitrage strategy of renewable-based microgrids via peer-to-peer energy-trading, IEEE Transactions on Sus- tainable Energy 12 (2020) 1372–1382

work page 2020

-

[15]

S. Nan, M. Zhou, G. Li, Optimal residential community demand response scheduling in smart grid, Applied Energy 210 (2018) 1280–1289

work page 2018

-

[16]

K. Oikonomou, M. Parvania, R. Khatami, Optimal demand response scheduling for water distribution systems, IEEE Transactions on Indus- trial Informatics 14 (2018) 5112–5122

work page 2018

-

[17]

C. Tsay, A. Kumar, J. Flores-Cerrillo, M. Baldea, Optimal demand response scheduling of an industrial air separation unit using data-driven dynamic models, Computers & Chemical Engineering 126 (2019) 22–34. 34

work page 2019

-

[18]

J. Li, B. Yang, J. Huang, Z. Guo, J. Wang, R. Zhang, Y. Hu, H. Shu, Y. Chen, Y. Yan, Optimal planning of electricity–hydrogen hybrid energy storage system considering demand response in active distribution network, Energy 273 (2023) 127142

work page 2023

- [19]

-

[20]

R. Tang, S. Wang, Model predictive control for thermal energy storage and thermal comfort optimization of building demand response in smart grids, Applied Energy 242 (2019) 873–882

work page 2019

- [21]

-

[22]

W. B. Powell, A unified framework for stochastic optimization, European journal of operational research 275 (2019) 795–821

work page 2019

-

[23]

C. Li, I. E. Grossmann, A review of stochastic programming methods for optimization of process systems under uncertainty, Frontiers in Chemical Engineering 2 (2021) 622241

work page 2021

-

[24]

J. J. Torres, C. Li, R. M. Apap, I. E. Grossmann, A review on the per- formance of linear and mixed integer two-stage stochastic programming software, Algorithms 15 (2022) 103

work page 2022

-

[25]

C. Filippi, G. Guastaroba, M. G. Speranza, Conditional value-at-risk beyond finance: a survey, International Transactions in Operational Research 27 (2020) 1277–1319

work page 2020

-

[26]

J. C. Do Prado, U. Chikezie, A decision model for an electricity retailer with energy storage and virtual bidding under daily and hourly cvar assessment, IEEE access 9 (2021) 106181–106191

work page 2021

-

[27]

R. Herding, E. Ross, W. R. Jones, E. Endler, V. M. Charitopoulos, L. G. Papageorgiou, Risk-aware microgrid operation and participation in the day-ahead electricity market, Advances in Applied Energy 15 (2024) 100180. 35

work page 2024

- [28]

-

[29]

Y. Haimes, On a bicriterion formulation of the problems of integrated system identification and system optimization, IEEE transactions on systems, man, and cybernetics (1971) 296–297

work page 1971

-

[30]

Y. Wang, W. Dong, Q. Yang, Multi-stage optimal energy management of multi-energy microgrid in deregulated electricity markets, Applied Energy 310 (2022) 118528

work page 2022

- [31]

-

[32]

R. A. Al-Lawati, J. L. Crespo-Vazquez, T. I. Faiz, X. Fang, M. Noor-E- Alam, Two-stage stochastic optimization frameworks to aid in decision- making under uncertainty for variable resource generators participating in a sequential energy market, Applied Energy 292 (2021) 116882

work page 2021

-

[33]

S. Kim, R. Pasupathy, S. G. Henderson, A guide to sample average approximation, Handbook of simulation optimization (2014) 207–243

work page 2014

-

[34]

C. Tsay, R. C. Pattison, M. Baldea, A dynamic optimization approach to probabilistic process design under uncertainty, Industrial & Engineering Chemistry Research 56 (2017) 8606–8621

work page 2017

-

[35]

R. M. Patel, J. Dumouchelle, E. Khalil, M. Bodur, Neur2sp: Neural two-stage stochastic programming, Advances in Neural Information Processing Systems 35 (2022) 23992–24005

work page 2022

-

[36]

L. M. Ghilardi, G. D. Patrón, A. Alcántara, C. Tsay, Integrated design and scheduling of hydrogen processes under uncertainty: A quantile neural network approach, Industrial & Engineering Chemistry Research (2025)

work page 2025

-

[37]

P. Artzner, F. Delbaen, J.-M. Eber, D. Heath, Coherent measures of risk, Mathematical finance 9 (1999) 203–228. 36

work page 1999

- [38]

-

[39]

R. T. Rockafellar, S. Uryasev, Optimization of conditional value-at-risk, Journal of Risk 2 (2000) 21–42

work page 2000

-

[40]

C. Tsay, S. Qvist, Integrating process and power grid models for optimal design and demand response operation of giga-scale green hydrogen, AIChE Journal 69 (2023) e18268

work page 2023

- [41]

-

[42]

U. R. Nair, M. Sandelic, A. Sangwongwanich, T. Dragičević, R. Costa- Castello, F. Blaabjerg, An analysis of multi objective energy scheduling in pv-bess system under prediction uncertainty, IEEE Transactions on Energy Conversion 36 (2021) 2276–2286

work page 2021

-

[43]

K. S. Ng, C.-S. Moo, Y.-P. Chen, Y.-C. Hsieh, Enhanced coulomb counting method for estimating state-of-charge and state-of-health of lithium-ion batteries, Applied energy 86 (2009) 1506–1511

work page 2009

-

[44]

X.Gao, B.Knueven, J.D.Siirola, D.C.Miller, A.W.Dowling, Multiscale simulation of integrated energy system and electricity market interactions, Applied energy 316 (2022) 119017

work page 2022

-

[45]

A. W. Dowling, R. Kumar, V. M. Zavala, A multi-scale optimization framework for electricity market participation, Applied Energy 190 (2017) 147–164

work page 2017

-

[46]

J. R. Birge, The value of the stochastic solution in stochastic linear programs with fixed recourse, Mathematical programming 24 (1982) 314–325

work page 1982

-

[47]

G. L. Bounitsis, L. G. Papageorgiou, V. M. Charitopoulos, Data-driven scenario generation for two-stage stochastic programming, Chemical Engineering Research and Design 187 (2022) 206–224. 37

work page 2022

-

[48]

https://www.eia.gov/electricity/ wholesalemarkets/data.php?rto=isone[Acessed: 2025-04-29]

United States Energy Information Administration, Wholesale electric- ity market data by rto, 2025. https://www.eia.gov/electricity/ wholesalemarkets/data.php?rto=isone[Acessed: 2025-04-29]

work page 2025

-

[49]

F. Lejarza, M. T. Kelley, M. Baldea, Feedback-based deterministic optimization is a robust approach for supply chain management under demand uncertainty, Industrial & Engineering Chemistry Research 61 (2022) 12153–12168

work page 2022

-

[50]

R. D. McAllister, J. B. Rawlings, C. T. Maravelias, The inherent robustness of closed-loop scheduling, Computers & Chemical Engineering 159 (2022) 107678

work page 2022

-

[51]

M. J. Risbeck, J. B. Rawlings, Economic model predictive control for time-varying cost and peak demand charge optimization, IEEE Transactions on Automatic Control 65 (2019) 2957–2968

work page 2019

- [52]

-

[53]

A. Alcántara, C. Ruiz, C. Tsay, A quantile neural network framework for two-stage stochastic optimization, Expert Systems with Applications (2025) 127876

work page 2025

-

[54]

T. Matsumoto, D. Bunn, Y. Yamada, Pricing electricity day-ahead cap futures with multifactor skew-t densities, Quantitative Finance 22 (2022) 835–860

work page 2022

- [55]

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.