Optimal Cash Transfers and Microinsurance to Reduce Social Protection Costs

Pith reviewed 2026-05-18 03:49 UTC · model grok-4.3

The pith

Cash transfers minimize total costs when provided before households reach the poverty line rather than after.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Solving the optimal control problem for capital injections yields a value function that satisfies the associated Hamilton-Jacobi-Bellman equation in the viscosity sense, and numerical results indicate that the cost-minimizing policy injects capital at a level strictly above the poverty threshold.

What carries the argument

The Hamilton-Jacobi-Bellman equation obtained from the dynamic programming principle applied to the problem of choosing injection amounts to minimize expected discounted costs of staying above the poverty line.

If this is right

- Social protection budgets in low-income countries can be used more efficiently by shifting toward preventive capital injections.

- Closed-form solutions for the optimal injection amounts exist in certain simplified versions of the capital process.

- Microinsurance products can serve as a complement that reduces the frequency or size of needed capital transfers.

Where Pith is reading between the lines

- The same optimization approach could be adapted to design timing rules for other aid types such as food or health support.

- Collecting local data on how capital actually fluctuates would allow testing whether the modeled loss process matches observed poverty entries.

- Combining the injection policy with insurance uptake incentives might produce a hybrid program with even lower overall costs.

Load-bearing premise

Household capital changes over time according to a specific stochastic process that includes sudden proportional losses capable of driving it below the poverty line.

What would settle it

If direct cost calculations or real household data show that injecting capital exactly at or below the poverty line produces lower total expected spending than the policy of acting above it, the optimality claim would not hold.

Figures

read the original abstract

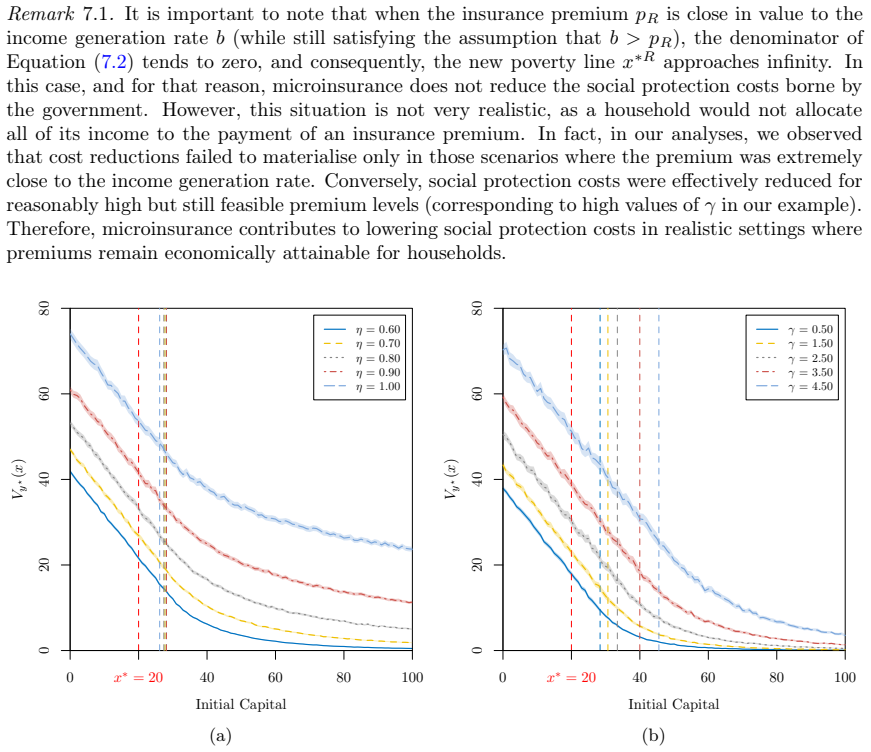

Design and implementation of appropriate social protection strategies is one of the main targets of the United Nation's Sustainable Development Goal (SDG) 1: No Poverty. Cash transfer (CT) programmes are considered one of the main social protection strategies and an instrument for achieving SDG 1. Targeting consists of establishing eligibility criteria for beneficiaries of CT programmes. In low-income countries, where resources are limited, proper targeting of CTs is essential for an efficient use of resources. Given the growing importance of microinsurance as a complementary tool to social protection strategies, this study examines its role as a supplement to CT programmes. In this article, we adopt the piecewise-deterministic Markov process introduced in Kovacevic and Pflug (2011) to model the capital of a household, which when exposed to proportional capital losses (in contrast to the classical Cram\'er-Lundberg model) can push them into the poverty area. Striving for cost-effective CT programmes, we optimise the expected discounted cost of keeping the household's capital above the poverty line by means of injection of capital (as a direct capital transfer). Using dynamic programming techniques, we derive the Hamilton-Jacobi-Bellman (HJB) equation associated with the optimal control problem of determining the amount of capital to inject over time. We show that this equation admits a viscosity solution that can be approximated numerically. Moreover, in certain special cases, we obtain closed-form expressions for the solution. Numerical examples show that there is an optimal level of injection above the poverty threshold, suggesting that efficient use of resources is achieved when CTs are preventive rather than reactive, since injecting capital into households when their capital levels are above the poverty line is less costly than to do so only when it falls below the threshold.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper models household capital via the piecewise-deterministic Markov process with proportional losses from Kovacevic and Pflug (2011). It formulates a stochastic control problem to minimize the expected discounted cost of capital injections (cash transfers) that keep capital above a poverty threshold, derives the associated HJB equation via dynamic programming, establishes that the equation admits a viscosity solution approximable numerically, obtains closed-form solutions in special cases, and presents numerical examples indicating that the optimal policy injects capital above the threshold (preventive rather than reactive CTs). Microinsurance is examined as a complementary instrument.

Significance. If the numerical findings are reliable, the work supplies a rigorous justification for preferring preventive cash transfers over purely reactive ones in resource-constrained settings, with potential implications for cost-effective implementation of SDG 1. The derivation of the HJB equation from first principles and the existence result for the viscosity solution constitute a solid technical contribution; the closed-form expressions in special cases are a clear analytical strength.

major comments (1)

- [Numerical examples] Numerical examples section: the approximation of the viscosity solution to the HJB equation is described only as 'can be approximated numerically,' with no specification of the discretization scheme (finite differences, policy iteration, etc.), spatial or temporal grid resolution, treatment of the proportional-loss jumps, or any convergence verification, a posteriori error bounds, or sensitivity checks. Because the central claim—that an optimal injection level exists above the poverty threshold and that preventive CTs are less costly than reactive ones—rests directly on these examples, the absence of these details prevents independent confirmation that the reported policy is a property of the true value function rather than a numerical artifact.

minor comments (2)

- [Abstract] The abstract states that closed forms exist 'in certain special cases' but does not indicate which parameter regimes or sections contain these expressions.

- [Model] A short self-contained recap of the key parameters of the Kovacevic–Pflug PDMP (intensity of proportional losses, discount rate) in the model section would improve readability.

Simulated Author's Rebuttal

We thank the referee for the positive assessment of our technical contributions and the potential policy implications. We address the single major comment below and will revise the manuscript accordingly.

read point-by-point responses

-

Referee: Numerical examples section: the approximation of the viscosity solution to the HJB equation is described only as 'can be approximated numerically,' with no specification of the discretization scheme (finite differences, policy iteration, etc.), spatial or temporal grid resolution, treatment of the proportional-loss jumps, or any convergence verification, a posteriori error bounds, or sensitivity checks. Because the central claim—that an optimal injection level exists above the poverty threshold and that preventive CTs are less costly than reactive ones—rests directly on these examples, the absence of these details prevents independent confirmation that the reported policy is a property of the true value function rather than a numerical artifact.

Authors: We agree that additional details are required for reproducibility and to confirm that the reported optimal policy is not a numerical artifact. In the revised manuscript we will expand the numerical examples section to describe the discretization scheme (a finite-difference approximation of the HJB equation solved via policy iteration), the spatial grid (uniform partition of the capital domain with explicit step size and number of points), the handling of proportional-loss jumps (by direct evaluation of the jump integral on the grid), convergence verification (results under successive grid refinements), and sensitivity checks with respect to the discount rate and loss intensity. These additions will directly address the referee’s concern and strengthen the numerical support for the advantage of preventive injections. revision: yes

Circularity Check

No circularity; derivation uses external model and standard dynamic programming

full rationale

The paper adopts the piecewise-deterministic Markov process directly from the external reference Kovacevic and Pflug (2011) without modification or self-referential fitting. It then applies standard dynamic programming to formulate the optimal control problem of minimizing expected discounted injection costs, derives the associated HJB equation, proves existence of a viscosity solution, obtains closed-form expressions in special cases, and performs numerical approximation in others. The reported finding of an optimal injection level above the poverty threshold is a computed outcome of this optimization rather than a quantity defined by or equivalent to the inputs by construction. No self-citations appear as load-bearing premises, no parameters are fitted to subsets of data and then relabeled as predictions, and no ansatz or uniqueness result is smuggled in via the authors' prior work. The derivation chain is therefore self-contained against the external benchmark model.

Axiom & Free-Parameter Ledger

free parameters (2)

- discount rate

- proportional loss intensity

axioms (2)

- domain assumption Household capital evolves as a piecewise-deterministic Markov process with proportional losses

- standard math The associated HJB equation admits a viscosity solution that can be approximated numerically

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

We optimise the expected discounted cost of keeping the household's capital above the poverty line by means of injection of capital... derive the Hamilton-Jacobi-Bellman (HJB) equation... admits a viscosity solution that can be approximated numerically.

-

IndisputableMonolith/Foundation/AlphaCoordinateFixation.leanJ_uniquely_calibrated_via_higher_derivative unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

Numerical examples show that there is an optimal level of injection above the poverty threshold

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

Albrecher, H., H. U. Gerber, and E. S. W. Shiu (2011). The Optimal Dividend Barrier in the Gamma–Omega Model.European Actuarial Journal 1(1), 43–55

work page 2011

-

[2]

Asmussen, S. and H. Albrecher (2010).Ruin Probabilities. Singapore: World Scientific

work page 2010

-

[3]

Azaïs, R. and A. Genadot (2015). Semi-Parametric Inference for the Absorption Features of a Growth-Fragmentation Model.TEST 24(2), 341–360. 34

work page 2015

-

[4]

Azcue, P. and N. Muler (2014).Stochastic Optimization in Insurance: A Dynamic Programming Approach. New York Heidelberg Dordrecht London: Springer

work page 2014

-

[5]

Systems & Control: Foundations & Applications

Bardi, M.andI.Capuzzo-Dolcetta(1997).Optimal Control and Viscosity Solutions of Hamilton- Jacobi-Bellman Equations. Systems & Control: Foundations & Applications. New York: Springer Science+Business Media

work page 1997

-

[6]

Bellman, R. (1954). Dynamic Programming and a New Formalism in the Calculus of Variations. Proceedings of the National Academy of Sciences 40(4), 231–235

work page 1954

-

[7]

(2006).Protecting the Poor: A Microinsurance Compendium — Volume I

Churchill, C. (2006).Protecting the Poor: A Microinsurance Compendium — Volume I. Geneva, Switzerland: International Labour Organization (ILO)

work page 2006

-

[8]

Churchill, C. and M. Matul (2012).Protecting the Poor: A Microinsurance Compendium — Volume II. Geneva, Switzerland: International Labour Organization (ILO)

work page 2012

-

[9]

Crandall, M. G. and P.-L. Lions (1983). Viscosity Solutions of Hamilton-Jacobi Equations. Transactions of the American Mathematical Society 277(1), 1–42

work page 1983

-

[10]

Social Protection in Poor Coun- tries.Social Protection Briefing Note Series 1

Department for International Development (DFID) (2006). Social Protection in Poor Coun- tries.Social Protection Briefing Note Series 1

work page 2006

-

[11]

Farrington, J. and R. Slater (2006). Introduction: Cash Transfers: Panacea for Poverty Re- duction or Money Down the Drain?Development Policy Review 24(5), 499–511

work page 2006

- [12]

-

[13]

Fleming, W. H. and H. M. Soner (2006).Controlled Markov Processes and Viscosity Solutions. United States of America: Springer Science+Business Media, Inc

work page 2006

-

[14]

Flores-Contró, J. M. (2025). The Gerber-Shiu Expected Discounted Penalty Function: An Application to Poverty Trapping.Scandinavian Actuarial Journal, 1–22

work page 2025

-

[15]

Flores-Contró, J. M. and S. Arnold (2024). The Role of Direct Capital Cash Transfers Towards Poverty and Extreme Poverty Alleviation - An Omega Risk Process.Scandinavian Actuarial Journal 2024(8), 781–812

work page 2024

-

[16]

Flores-Contró, J. M., K. Henshaw, S.-H. Loke, S. Arnold, and C. Constantinescu (2025). Subsidizing Inclusive Insurance to Reduce Poverty.North American Actuarial Journal 29(1), 44–73

work page 2025

-

[17]

Garcia, M. and C. M. T. Moore (2012).The Cash Dividend: The Rise of Cash Transfer Programs in Sub-Saharan Africa. Directions in Development - Human Development. Washington, D.C.: The World Bank

work page 2012

-

[18]

Habimana, D., J. Haughton, J. Nkurunziza, and D. M.-A. Haughton (2021). Measuring the Impact of Unconditional Cash Transfers on Consumption and Poverty in Rwanda.World Devel- opment Perspectives 23, 100341

work page 2021

-

[19]

Handa, S. and B. Davis (2006). The Experience of Conditional Cash Transfers in Latin America and the Caribbean.Development Policy Review 24(5), 513–536. 35

work page 2006

-

[20]

(2005).Cash and Vouchers in Emergencies

Harvey, P. (2005).Cash and Vouchers in Emergencies. London, United Kingdom: Overseas Development Institute

work page 2005

-

[21]

Henshaw, K., J. M. Ramirez, J. M. Flores-Contró, E. A. Thomann, S. H. Loke, and C. D. Constantinescu (2023). On the Impact of Insurance on Households Susceptible to Random Pro- portional Losses: An Analysis of Poverty Trapping.Working Paper

work page 2023

-

[22]

Issues Paper on Conduct of Business in Inclusive Insurance

International Association of Insurance Supervisors (IAIS) (2015). Issues Paper on Conduct of Business in Inclusive Insurance

work page 2015

-

[23]

Keen, M. (1992). Needs and Targeting.The Economic Journal 102(410), 67–79

work page 1992

-

[24]

Kovacevic, R. M. and G. C. Pflug (2011). Does Insurance Help to Escape the Poverty Trap? — A Ruin Theoretic Approach.Journal of Risk and Insurance 78(4), 1003–1027

work page 2011

-

[25]

Owusu-Addo, E., A. M. N. Renzaho, P. Sarfo-Mensah, Y. A. Sarpong, W. Niyuni, and B. J. Smith (2023). Sustainability of Cash Transfer Programs: A Realist Case Study.Poverty & Public Policy 15(2), 173–198

work page 2023

-

[26]

(1992).Stochastic Integration and Differential Equations: A New Approach

Protter, P. (1992).Stochastic Integration and Differential Equations: A New Approach. New York: Springer-Verlag Berlin Heidelberg

work page 1992

-

[27]

(2007).Stochastic Control in Insurance

Schmidli, H. (2007).Stochastic Control in Insurance. London: Springer

work page 2007

-

[28]

Slater, R. (2011). Cash Transfers, Social Protection and Poverty Reduction.International Journal of Social Welfare 20(3), 250–259

work page 2011

-

[29]

Slater, R. and J. Farrington (2010).Appropriate, Achievable and Acceptable: A Practical Tool for Good Targeting. London: ODI

work page 2010

-

[30]

Soner, H. M. (1988). Optimal Control of Jump-Markov Processes and Viscosity Solutions. InStochastic Differential Systems, Stochastic Control Theory and Applications, pp. 501–511. Springer-Verlag

work page 1988

-

[31]

Tabor, S. R. (2002). Assisting the Poor with Cash: Design and Implementation of Social Transfer Programs.World Bank Social Protection Discussion Paper 223, 79–97

work page 2002

-

[32]

United Nations (2015).Transforming Our World: The 2030 Agenda for Sustainable Develop- ment. Number A/RES/70/1. New York: United Nations. Appendices A Mathematical Proofs A.1 Proof of Lemma 3.1 Proof.BydefinitionC(x)isnon-increasingandnon-negative. Letusshownowthatlim x→∞ C(x) =

work page 2015

-

[33]

nX k=1 C(X τk)e −δτk 1 τ=τ k # ≤C(0)·E

We have the following, E e−δτn 1 {τ≥τ n} ≤E e−δτn =E " e −δ nP i=1 (τi−τi−1) # = E e−δτ1 n = δ δ+λ n , 36 which yields:lim n→∞ E e−δτn 1 {τ≥τ n} = 0. SinceC(x)is non-increasing, we have, C(x)≤ nX k=1 C(X τk)e −δτk 1 τ=τ k +C(0)·E e−δτn 1 τ >τn , which leads to the following inequality, 0≤C(x)≤lim n→∞ E " nX k=1 C(X τk)e −δτk 1 {τ=τ k} # . Now, if τ≥τ 1, X...

work page 1992

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.