Who Restores the Peg? A Mean-Field Game Approach to Model Stablecoin Market Dynamics

Pith reviewed 2026-05-16 10:32 UTC · model grok-4.3

The pith

Primary-market arbitrage restores the peg in a mean-field game model of stablecoin dynamics

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

We develop a dynamic, agent-based mean-field game framework for fiat-collateralized stablecoins in which arbitrageurs and retail traders strategically interact across primary and secondary markets during a de-peg episode. The equilibrium formulation maps market frictions into a market-clearing price path and implied net order flows, allowing attribution of peg-reverting pressure by channel. Using three historical de-peg events, the calibrated equilibrium reproduces observed recovery half-lives and shows system-wide stress is predominantly stabilized by primary-market arbitrage. A quantitative sensitivity analysis identifies a non-linear breakdown threshold beyond which a de-peg becomes-markd

What carries the argument

The mean-field game equilibrium that endogenously determines the market-clearing price path and net order flows from strategic interactions of agents facing market frictions.

Load-bearing premise

The mean-field equilibrium and friction parameters calibrated to three events continue to describe out-of-sample de-peg behavior, with primary and secondary market flows cleanly separable in the data.

What would settle it

Observing a new de-peg event where the recovery half-life differs substantially from the model's prediction or where secondary-market flows dominate the order flow decomposition.

Figures

read the original abstract

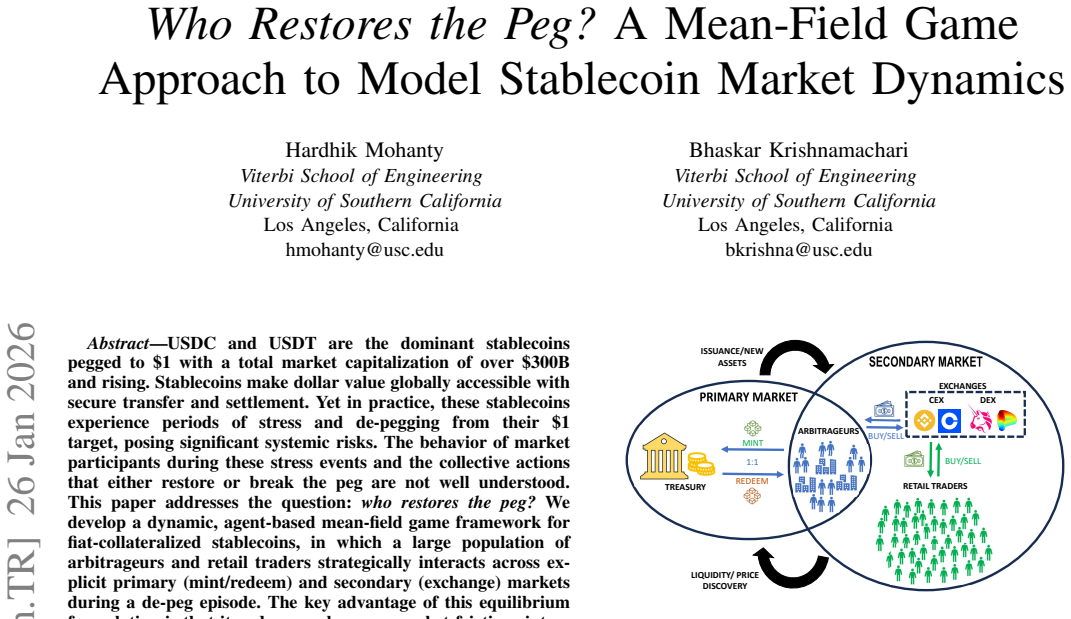

USDC and USDT are the dominant stablecoins pegged to \$1 with a total market capitalization of over \$300B and rising. Stablecoins make dollar value globally accessible with secure transfer and settlement. Yet in practice, these stablecoins experience periods of stress and de-pegging from their \$1 target, posing significant systemic risks. The behavior of market participants during these stress events and the collective actions that either restore or break the peg are not well understood. This paper addresses the question: who restores the peg?. We develop a dynamic, agent-based mean-field game framework for fiat-collateralized stablecoins, in which a large population of arbitrageurs and retail traders strategically interact across primary and secondary markets during a de-peg episode. The key advantage of this equilibrium formulation is that it endogenously maps market frictions into a market-clearing price path and implied net order flows, allowing us to attribute peg-reverting pressure by channel and to stress-test when a given infrastructure becomes insufficient for recovery. Using three historical de-peg events, we show that the calibrated equilibrium reproduces observed recovery half-lives and yields an order flow decomposition in which system-wide stress is predominantly stabilized by primary-market arbitrage. Finally, a quantitative sensitivity analysis identifies a non-linear breakdown threshold, beyond which a de-peg becomes markedly slower to reverse.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops a dynamic mean-field game framework for fiat-collateralized stablecoins in which arbitrageurs and retail traders interact strategically across primary and secondary markets during de-peg episodes. The equilibrium endogenously determines a market-clearing price path and net order flows from market frictions. Calibrated to three historical de-peg events, the model reproduces observed recovery half-lives and decomposes order flows to conclude that primary-market arbitrage supplies the dominant restoring pressure; a sensitivity analysis identifies a nonlinear breakdown threshold beyond which recovery slows markedly.

Significance. If the primary-market attribution and breakdown threshold prove robust, the framework would offer a useful quantitative tool for attributing stabilization channels and stress-testing stablecoin infrastructure. The endogenous mapping from frictions to flows is a conceptual strength, but the current calibration-to-validation design on the same three events limits the strength of the decomposition claim.

major comments (3)

- [§4] §4 (Calibration and Results): The friction and cost parameters are fitted to the identical three de-peg episodes whose half-lives are subsequently reported as reproduced. Because the equilibrium map from these parameters to price paths and net flows is continuous, any event-specific features absorbed in calibration will be attributed to the channel labeled “primary-market arbitrage,” undermining the claim that the decomposition is structural rather than fitted.

- [§5] §5 (Sensitivity Analysis): The reported nonlinear breakdown threshold is obtained from the same calibrated parameter set; without a hold-out event or parameter-stability check across additional episodes, it is unclear whether the threshold reflects a genuine market feature or an artifact of the three-event sample.

- [Abstract, §3] Abstract and §3 (Model): The abstract states that the equilibrium “yields an order flow decomposition in which system-wide stress is predominantly stabilized by primary-market arbitrage,” yet no out-of-sample test or cross-validation procedure is described to separate this attribution from the calibration procedure itself.

minor comments (2)

- [§3] Notation for the mean-field distribution and the distinction between primary- and secondary-market flows should be introduced earlier and used consistently; several equations in §3 reuse symbols without redefinition.

- [Figures 2-4] Figure captions for the price-path and flow-decomposition plots should explicitly state the data sources and any filtering rules applied to the three events.

Simulated Author's Rebuttal

We thank the referee for the constructive comments. We address each major point below, acknowledging the calibration limitations while defending the structural role of the equilibrium. We propose targeted revisions to qualify claims and add robustness checks.

read point-by-point responses

-

Referee: [§4] The friction and cost parameters are fitted to the identical three de-peg episodes whose half-lives are subsequently reported as reproduced. Because the equilibrium map from these parameters to price paths and net flows is continuous, any event-specific features absorbed in calibration will be attributed to the channel labeled “primary-market arbitrage,” undermining the claim that the decomposition is structural rather than fitted.

Authors: We agree that using the same three events for calibration and reported reproduction limits out-of-sample strength. However, the mean-field game imposes optimality conditions and market-clearing constraints that restrict the admissible mappings from parameters to flows, providing identification beyond arbitrary fitting. In revision we will expand §4 with an explicit identification discussion, report decomposition results under leave-one-event-out recalibrations, and qualify the primary-market attribution as holding in the calibrated equilibria for these episodes. revision: partial

-

Referee: [§5] The reported nonlinear breakdown threshold is obtained from the same calibrated parameter set; without a hold-out event or parameter-stability check across additional episodes, it is unclear whether the threshold reflects a genuine market feature or an artifact of the three-event sample.

Authors: We acknowledge the sample-size concern. The revised §5 will include a parameter-stability exercise that perturbs calibrated values within bootstrap confidence intervals, recomputes the breakdown threshold, and reports the range of thresholds obtained. We will also add text noting that the nonlinearity is a feature of the calibrated model and that broader validation requires additional de-peg episodes. revision: yes

-

Referee: [Abstract, §3] The abstract states that the equilibrium “yields an order flow decomposition in which system-wide stress is predominantly stabilized by primary-market arbitrage,” yet no out-of-sample test or cross-validation procedure is described to separate this attribution from the calibration procedure itself.

Authors: We will revise the abstract to read that the calibrated equilibrium suggests primary-market arbitrage supplies the dominant restoring pressure. In §3 we will insert a short paragraph clarifying that the decomposition is structural within the equilibrium but that quantitative attribution relies on calibration to the observed episodes, thereby aligning wording with the methodology. revision: yes

Circularity Check

Calibration to three de-peg events makes reproduction of half-lives and order-flow decomposition tautological by construction

specific steps

-

fitted input called prediction

[Abstract]

"Using three historical de-peg events, we show that the calibrated equilibrium reproduces observed recovery half-lives and yields an order flow decomposition in which system-wide stress is predominantly stabilized by primary-market arbitrage."

Parameters (transaction costs, inventory penalties, etc.) are fitted to the three events; the equilibrium is then shown to reproduce the half-lives and flows from those identical events. The reproduction and decomposition are therefore outputs of the same fitting procedure, not independent predictions.

full rationale

The central empirical result calibrates friction parameters of the mean-field game to three historical events and then reports that the resulting equilibrium reproduces the observed recovery half-lives of those same events while decomposing order flows. Because the equilibrium price path and net flows are continuous functions of the fitted parameters, any match to the calibration targets is guaranteed by construction rather than an independent test. The attribution of stabilization to primary-market arbitrage therefore inherits the same dependence on the three-event sample. No parameter-free prediction, hold-out validation, or external benchmark is indicated in the abstract or skeptic summary.

Axiom & Free-Parameter Ledger

free parameters (1)

- friction and cost parameters

axioms (1)

- domain assumption Mean-field limit for large population of agents

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

Both agent types solve a discounted LQ optimization problem to minimize a cost functional that combines mispricing exposure, inventory risk, execution costs, and congestion costs.

-

IndisputableMonolith/Foundation/RealityFromDistinction.leanreality_from_one_distinction unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

We calibrate our model by testing it against real-world de-peg events... θ* = arg min_θ L(θ) ... Differential Evolution

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

G. B. Gorton and J. Y . Zhang, “Taming wildcat stablecoins,”University of Chicago Law Review, vol. 90, no. 3, pp. 909–972, 2023

work page 2023

-

[2]

Crypto lending and stablecoin de-pegging: Key risks and challenges,

M. Abraham, “Crypto lending and stablecoin de-pegging: Key risks and challenges,”International Journal of Cryptocurrency Research, vol. 4, no. 1, pp. 79–100, 2024

work page 2024

-

[3]

What keeps stablecoins stable?

R. K. Lyons and G. Viswanath-Natraj, “What keeps stablecoins stable?” Journal of International Money and Finance, vol. 131, p. 102777, 2023

work page 2023

-

[4]

What drives the (in)stability of a stablecoin?

Y . Potter, K. Pongmala, K. Qin, A. Klages-Mundt, P. Jovanovic, C. Par- lour, A. Gervais, and D. Song, “What drives the (in)stability of a stablecoin?” in2024 IEEE International Conference on Blockchain and Cryptocurrency (ICBC). IEEE, 2024, pp. 316–324

work page 2024

-

[5]

Solving continuous mean field games: Deep reinforcement learning for non- stationary dynamics,

L. Magnino, K. Shao, Z. Wu, J. Shen, and M. Lauriere, “Solving continuous mean field games: Deep reinforcement learning for non- stationary dynamics,” inThe Thirty-Ninth Annual Conference on Neural Information Processing Systems, 2025

work page 2025

-

[6]

A policy iteration method for mean field games,

S. Cacace, F. Camilli, and A. Goffi, “A policy iteration method for mean field games,”ESAIM: Control, Optimisation and Calculus of Variations, vol. 27, p. 85, 2021

work page 2021

-

[7]

Learning in mean field games: A survey.arXiv preprint arXiv:2205.12944, 2022

M. Lauri `ere, S. Perrin, J. P ´erolat, S. Girgin, P. Muller, R. ´Elie, M. Geist, and O. Pietquin, “Learning in mean field games: A survey,”arXiv preprint arXiv:2205.12944, 2022

-

[8]

Linear- quadratic mean field games,

A. Bensoussan, K. C. J. Sung, S. C. P. Yam, and S.-P. Yung, “Linear- quadratic mean field games,”Journal of Optimization Theory and Applications, vol. 169, no. 2, pp. 496–529, 2016

work page 2016

-

[9]

Primary and secondary markets for stablecoins,

C. Watsky, J. Allen, H. Daud, J. Demuth, D. Little, M. Rodden, and A. Seira, “Primary and secondary markets for stablecoins,”FEDS Notes, 2024, board of Governors of the Federal Reserve System

work page 2024

-

[10]

Daisim: A computational simulator for the makerdao stablecoin,

S. Bhat, A. B. Kahya, B. Krishnamachari, and R. Kumar, “Daisim: A computational simulator for the makerdao stablecoin,” in4th Interna- tional Symposium on Foundations and Applications of Blockchain 2021 (FAB 2021). Schloss Dagstuhl–Leibniz-Zentrum f ¨ur Informatik, 2021, pp. 3:1–3:13

work page 2021

-

[11]

Algorithmic stablecoins: A simulator for the dual-token model in normal and panic scenarios,

F. Calandra, F. P. Rossi, F. Fabris, and M. Bernardo, “Algorithmic stablecoins: A simulator for the dual-token model in normal and panic scenarios,” in2025 IEEE International Conference on Blockchain and Cryptocurrency (ICBC). IEEE, 2025, pp. 1–9

work page 2025

-

[12]

Trading and arbitrage in cryptocurrency markets,

I. Makarov and A. Schoar, “Trading and arbitrage in cryptocurrency markets,”Journal of Financial Economics, vol. 135, no. 2, pp. 293– 319, 2020

work page 2020

-

[13]

Liquidity shocks, token returns and market capitalization in decentralized finance (defi) markets,

L. Ante, “Liquidity shocks, token returns and market capitalization in decentralized finance (defi) markets,” Blockchain Research Lab, BRL Working Paper Series 26, 2022

work page 2022

-

[14]

On stablecoin price processes and arbitrage,

I. G. A. Pernice, “On stablecoin price processes and arbitrage,” in International Conference on Financial Cryptography and Data Security. Springer, 2021, pp. 124–135

work page 2021

-

[15]

Market impact and efficiency in cryptoassets markets,

E. Barucci, G. Giuffra Moncayo, and D. Marazzina, “Market impact and efficiency in cryptoassets markets,”Digital Finance, vol. 5, no. 3, pp. 519–562, 2023

work page 2023

-

[16]

K. Cortez, M. d. P. Rodriguez-Garcia, and S. Mongrut, “Exchange market liquidity prediction with the k-nearest neighbor approach: Crypto vs. fiat currencies,”Mathematics, vol. 9, no. 1, p. 56, 2020

work page 2020

-

[17]

Decentralised finance and auto- mated market making: Execution and speculation,

´A. Cartea, F. Drissi, and M. Monga, “Decentralised finance and auto- mated market making: Execution and speculation,”Journal of Economic Dynamics and Control, p. 105134, 2025

work page 2025

-

[18]

J.-M. Lasry and P.-L. Lions, “Mean field games,”Japanese Journal of Mathematics, vol. 2, no. 1, pp. 229–260, 2007

work page 2007

-

[19]

Reinforce- ment learning in non-stationary discrete-time linear-quadratic mean-field games,

M. A. Uz Zaman, K. Zhang, E. Miehling, and T. Bas ¸ar, “Reinforce- ment learning in non-stationary discrete-time linear-quadratic mean-field games,” in2020 59th IEEE Conference on Decision and Control (CDC). IEEE, 2020, pp. 2278–2284

work page 2020

-

[20]

Mean field games of timing and models for bank runs,

R. Carmona, F. Delarue, and D. Lacker, “Mean field games of timing and models for bank runs,”Applied Mathematics & Optimization, vol. 76, no. 1, pp. 217–260, 2017

work page 2017

-

[21]

Mean field game of controls and an application to trade crowding,

P. Cardaliaguet and C.-A. Lehalle, “Mean field game of controls and an application to trade crowding,”Mathematics and Financial Economics, vol. 12, no. 3, pp. 335–363, 2018

work page 2018

-

[22]

Optimal execution with nonlinear impact functions and trading-enhanced risk,

R. F. Almgren, “Optimal execution with nonlinear impact functions and trading-enhanced risk,”Applied Mathematical Finance, vol. 10, no. 1, pp. 1–18, 2003

work page 2003

-

[23]

Generalized autoregressive conditional heteroskedastic- ity,

T. Bollerslev, “Generalized autoregressive conditional heteroskedastic- ity,”Journal of Econometrics, vol. 31, no. 3, pp. 307–327, 1986

work page 1986

-

[24]

A com- mon protocol for agent-based social simulation,

M. G. Richiardi, R. Leombruni, N. J. Saam, and M. Sonnessa, “A com- mon protocol for agent-based social simulation,”Journal of Artificial Societies and Social Simulation, vol. 9, no. 1, 2006

work page 2006

-

[25]

R. Storn and K. Price, “Differential evolution: A simple and efficient heuristic for global optimization over continuous spaces,”Journal of Global Optimization, vol. 11, no. 4, pp. 341–359, 1997

work page 1997

-

[26]

Binance.US, “Historical market data,” https://www.binance.us/ institutions/market-history, 2025

work page 2025

-

[27]

R. S. Tsay,Analysis of Financial Time Series, 3rd ed. Hoboken, NJ: John Wiley & Sons, 2010

work page 2010

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.