Trends in tail dependence of heteroscedastic extremes

Pith reviewed 2026-05-10 14:47 UTC · model grok-4.3

The pith

A nonparametric estimator for the integrated tail copula works for data with smoothly varying tail dependence and heteroscedastic margins.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

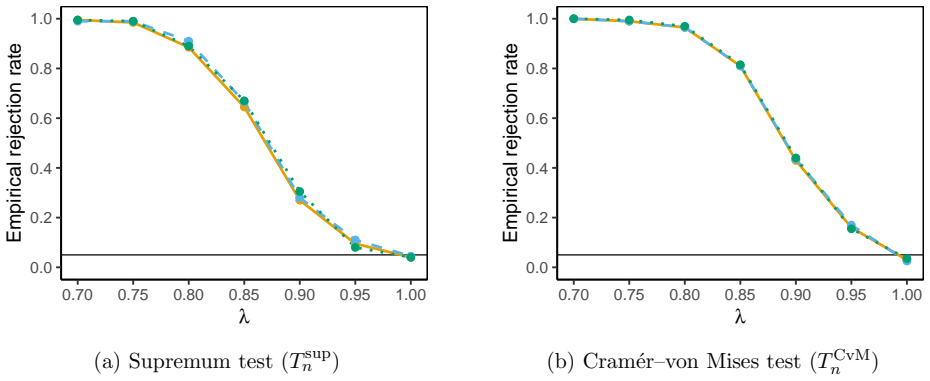

We propose a nonparametric estimator for the integrated tail copula and establish its asymptotic behavior. Notably, the heteroscedastic marginals do not affect the limiting processes. We use the main result for the integrated tail copula to test for a constant tail copula across all observations.

What carries the argument

The integrated tail copula, formed by integrating the tail dependence function over the sample index to summarize overall dependence trends.

If this is right

- The estimator converges at the standard nonparametric rate with a Gaussian limit that ignores marginal scale variation.

- A Cramér-von Mises type statistic built from the estimator provides a consistent test for constancy of the tail copula.

- Finite-sample simulations confirm that the asymptotic approximations are accurate and that the test has substantial power against smooth alternatives.

- The same limiting process can be used to construct confidence bands for the integrated tail copula itself.

Where Pith is reading between the lines

- The method could be extended to estimate time-localized versions of the tail copula by inserting a kernel weight around each time point.

- Existing estimators for the tail dependence function in the stationary case might inherit similar robustness to marginal non-stationarity once integrated in the same way.

- Risk measures that depend on joint tail probabilities could be updated in real time by tracking the running integral of the estimated tail copula.

Load-bearing premise

The tail copulas change smoothly with the observation index.

What would settle it

Generate data from a process whose tail dependence jumps discontinuously at a fixed fraction of the sample; the estimator would then fail to converge at the stated rate or the test would reject at the wrong rate.

Figures

read the original abstract

We consider multivariate extreme value statistics for independent but nonidentically distributed random vectors. In particular, the data may have varying tail copulas and also heteroscedastic marginal distributions. Assuming smoothly changing tail copulas, we propose a nonparametric estimator for the integrated tail copula and establish its asymptotic behavior. Notably, the heteroscedastic marginals do not affect the limiting processes. We use the main result for the integrated tail copula to test for a constant tail copula across all observations. Finally, a simulation study shows the good finite-sample behavior of our limit theorems as well as high power of the test.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper addresses multivariate extreme value statistics for independent but non-identically distributed random vectors, allowing for varying tail copulas and heteroscedastic marginal distributions. Assuming smoothly changing tail copulas, the authors propose a nonparametric estimator for the integrated tail copula and derive its asymptotic behavior. Importantly, the limiting processes are unaffected by the heteroscedastic marginals. They apply this to develop a test for constant tail copula across observations and support the theory with simulations showing good finite-sample performance and test power.

Significance. If the results hold, this contributes to the literature on non-stationary extremes by providing a nonparametric way to estimate and test trends in tail dependence without the marginal heteroscedasticity interfering with the asymptotics. This is useful for applications in climate science, finance, and risk management where both marginal scales and dependence may change over time. The use of the integrated tail copula is a clever choice that facilitates the analysis. The simulation study is a strength, demonstrating practical applicability. The paper ships clear asymptotic results and a simulation study with evidence of good finite-sample behavior.

minor comments (3)

- [Abstract and §2] The abstract and introduction refer to 'smoothly changing tail copulas' without immediately stating the precise regularity class (e.g., Hölder continuity with a specific exponent); this should be made explicit in §2 to allow readers to assess the rate conditions.

- [Simulation study] In the simulation section, the choice of bandwidth sequences is presented but a more systematic sensitivity table (varying the constant factor in the bandwidth by factors of 0.5 and 2) would strengthen the finite-sample claims.

- [Introduction] Notation for the integrated tail copula estimator could be introduced with a short display equation in the introduction to improve readability before the technical sections.

Simulated Author's Rebuttal

We thank the referee for the positive assessment of our manuscript, which accurately reflects the contributions on nonparametric estimation of the integrated tail copula under smoothly varying tail dependence and heteroscedastic margins, along with the associated test and simulation results. The recommendation for minor revision is appreciated.

Circularity Check

No significant circularity; derivation self-contained in standard EVT framework

full rationale

The paper defines a nonparametric estimator for the integrated tail copula under the explicit modeling assumption of smoothly varying tail dependence, then derives its limiting distribution (unaffected by heteroscedastic marginals) and applies it to a constancy test. No quoted step reduces a claimed result to a fitted parameter renamed as prediction, a self-definitional loop, or a load-bearing self-citation whose validity is presupposed. The smoothness condition is stated upfront as the nonparametric modeling choice rather than smuggled in; asymptotics and simulations are presented as independent verifications. This is the normal case of a self-contained statistical derivation with no internal reduction to inputs by construction.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Smoothly changing tail copulas

Reference graph

Works this paper leans on

-

[1]

Alexander, K. S. (1984). Probability inequalities for empirical processes and a law of the iterated logarithm.The Annals of Probability 12(4), 1041–1067

work page 1984

-

[2]

Beirlant, J., Y. Goegebeur, J. Segers, and J. L. Teugels (2006).Statistics of extremes: theory and applications. John Wiley & Sons

work page 2006

-

[3]

Drees, H. (2023). Statistical inference on a changing extreme value dependence structure. The Annals of Statistics 51(4), 1824–1849

work page 2023

-

[4]

Einmahl, J. H. J., L. de Haan, and D. Li (2006). Weighted approximations of tail copula processes with application to testing the bivariate extreme value condition

work page 2006

-

[5]

Einmahl, J. H. J., L. de Haan, and C. Zhou (2016). Statistics of heteroscedastic extremes. Journal of the Royal Statistical Society Series B: Statistical Methodology 78(1), 31–51

work page 2016

-

[6]

Einmahl, J. H. J., A. Krajina, and J. Segers (2012). An m-estimator for tail dependence in arbitrary dimensions

work page 2012

-

[7]

Einmahl, J. H. J. and J. Segers (2021). Empirical tail copulas for functional data.The Annals of Statistics 49(5), 2672–2696

work page 2021

-

[8]

Einmahl, J. H. J. and C. Zhou (2026). Tail copula estimation for heteroscedastic extremes. Econometrics and Statistics. de Haan, L. and A. Ferreira (2006).Extreme value theory: an introduction. Springer. de Haan, L. and C. Zhou (2021). Trends in extreme value indices.Journal of the American Statistical Association 116(535), 1265–1279

work page 2026

-

[9]

Hu, Y. and Y. Hou (2028). Two sample tests for bivariate heteroscedastic extremes with a changing tail copula.Statistica Sinica. 39 0.00 0.05 0.10 100200300 500 700 1000 k Empirical size (a)θ= 0.5, M1 (constant) 0.00 0.05 0.10 100200300 500 700 1000 k Empirical size (b)θ= 0.9, M1 (constant) 0.00 0.05 0.10 100200300 500 700 1000 k Empirical size (c)θ= 0.5,...

work page 2028

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.