Recognition: unknown

Vault as a credit instrument

Pith reviewed 2026-05-10 05:40 UTC · model grok-4.3

The pith

DeFi lending vault depositors require five new credit risk metrics because six on-chain features create loss channels absent from traditional frameworks.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

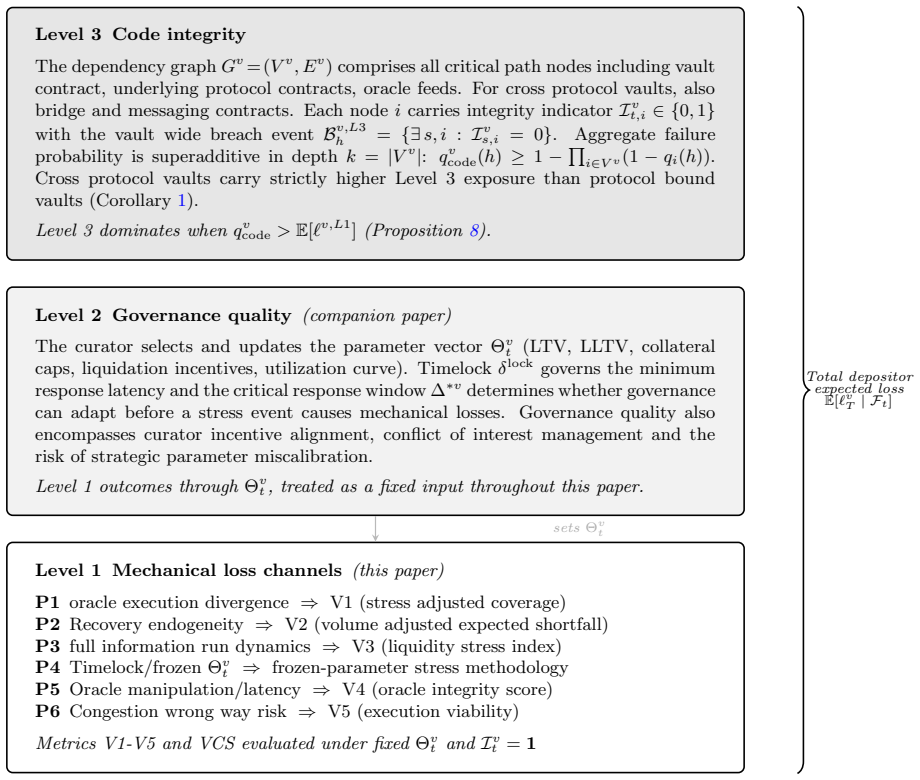

We derive five tractable credit risk metrics for DeFi lending vault depositors, grounded in a formal three level decomposition of vault risk into mechanical loss channels (Level 1), governance quality (Level 2) and smart contract code integrity (Level 3). For Level 1, we show that six structural features of onchain execution break canonical TradFi analogies and generate depositor loss channels absent from standard credit frameworks. Vault credit risk metrics translate these channels into measurable risk components which are aggregated into a vault credit score, supported by an implementable estimation architecture that specifies required onchain data, identification strategies, partial-ident

What carries the argument

The three-level decomposition that isolates mechanical loss channels from governance quality and code integrity, turning on-chain execution traits into aggregated credit scores.

If this is right

- Depositors obtain a single vault credit score that combines the five component metrics for direct risk comparison.

- Platforms can implement the supplied estimation architecture to report on-chain data and parameter bounds.

- Risk managers gain a stress-scenario method that explicitly includes the six mechanical channels.

- Transparency standards can be defined by the data items needed to compute the metrics.

- Partial identification bounds allow risk statements even when some parameters remain uncertain.

Where Pith is reading between the lines

- Similar layered decompositions could be applied to other on-chain products such as derivatives or insurance pools.

- Depositors might begin requiring platforms to publish the specific data fields listed for metric calculation.

- Regulators could adopt the three-level structure as a template for disclosure rules on decentralized lending.

- The approach opens a route to compare total credit risk across TradFi and DeFi instruments on a common numerical basis.

Load-bearing premise

The six listed on-chain features produce depositor loss channels that standard credit frameworks cannot already capture and that the three-level split is complete enough to yield usable metrics.

What would settle it

Collect historical loss events from DeFi lending vaults and check whether every loss is preceded by at least one of the six mechanical features; if losses occur without them, or if the five metrics show no relation to realized losses, the decomposition does not hold.

Figures

read the original abstract

We derive five tractable credit risk metrics for DeFi lending vault depositors, grounded in a formal three level decomposition of vault risk into mechanical loss channels (Level 1), governance quality (Level 2) and smart contract code integrity (Level 3). For Level 1, we show that six structural features of onchain execution (oracle execution divergence, endogenous recovery, full information run dynamics, timelock constrained governance, oracle manipulation and congestion driven liquidation failure) break canonical TradFi analogies and generate depositor loss channels absent from standard credit frameworks. Vault credit risk metrics translate these channels into measurable risk components which are aggregated into a vault credit score. The empirical contribution is an implementable estimation architecture for credit risk metrics, including required onchain data, identification strategies for core parameters, partial identification bounds and a coherent stress scenario methodology. The results have direct implications for vault risk management and for minimum transparency standards necessary for depositor risk assessment.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a three-level decomposition of vault risk in DeFi lending: mechanical loss channels at Level 1, governance quality at Level 2, and smart contract code integrity at Level 3. It identifies six on-chain structural features that create unique depositor loss channels not found in traditional finance frameworks. From this, five tractable credit risk metrics are derived and aggregated into a vault credit score. Additionally, an implementable estimation architecture is outlined, including on-chain data requirements, identification strategies, partial identification bounds, and stress scenario methods, with implications for risk management and transparency standards.

Significance. If the formal derivation holds and the six features indeed generate loss channels absent from standard credit frameworks, this could be a significant contribution by providing a structured, on-chain-specific approach to credit risk assessment in DeFi vaults. The estimation architecture, if implementable with clear identification strategies and bounds, would offer practical value for depositors, risk managers, and regulators seeking transparency standards.

major comments (2)

- [Abstract] Abstract: The abstract asserts a 'formal three level decomposition' and 'formal derivation' of five tractable metrics but supplies no equations, identification proofs, or validation steps. This makes it impossible to check whether the claimed metrics follow from the stated decomposition or whether they are independent of the parameters used to define the loss channels, which is load-bearing for the central claim.

- [Level 1] Level 1 section: The claim that the six structural features (oracle execution divergence, endogenous recovery, full information run dynamics, timelock constrained governance, oracle manipulation, and congestion driven liquidation failure) 'break canonical TradFi analogies and generate depositor loss channels absent from standard credit frameworks' is central but lacks specific comparisons to TradFi models (e.g., Merton structural model or reduced-form intensity models) or derivations showing the differences in loss distributions.

minor comments (2)

- [Abstract] Abstract: The five metrics are referenced but neither named nor described explicitly; providing their names and brief definitions would improve readability and allow readers to connect them to the six features.

- [Abstract] Abstract: The term 'onchain' appears as a single word; consistent use of 'on-chain' aligns with standard academic and technical writing conventions.

Simulated Author's Rebuttal

We thank the referee for the constructive comments on the abstract and the Level 1 analysis. We agree that enhancing the formal presentation and providing explicit comparisons to TradFi models will strengthen the paper. We address each point below and commit to the corresponding revisions.

read point-by-point responses

-

Referee: [Abstract] Abstract: The abstract asserts a 'formal three level decomposition' and 'formal derivation' of five tractable metrics but supplies no equations, identification proofs, or validation steps. This makes it impossible to check whether the claimed metrics follow from the stated decomposition or whether they are independent of the parameters used to define the loss channels, which is load-bearing for the central claim.

Authors: We appreciate the referee's observation regarding the abstract. As is conventional, the abstract provides a high-level overview without mathematical formalism. The three-level decomposition is formally defined in Section 2, with Level 1 features and their unique loss channels derived in Section 3. The five credit risk metrics are formally derived in Section 4, including equations that map the mechanical features to measurable components and their aggregation into the vault credit score. Section 5 details the estimation architecture with identification strategies and partial identification bounds. To address the concern, we will revise the abstract to reference the relevant sections and key equations, enabling readers to verify the derivations directly from the main text. revision: yes

-

Referee: [Level 1] Level 1 section: The claim that the six structural features (oracle execution divergence, endogenous recovery, full information run dynamics, timelock constrained governance, oracle manipulation, and congestion driven liquidation failure) 'break canonical TradFi analogies and generate depositor loss channels absent from standard credit frameworks' is central but lacks specific comparisons to TradFi models (e.g., Merton structural model or reduced-form intensity models) or derivations showing the differences in loss distributions.

Authors: The referee raises a valid point about the need for more explicit contrasts with traditional credit risk frameworks. The manuscript in Section 3 explains how each of the six on-chain features generates loss channels not present in standard models by violating key assumptions, such as perfect information and continuous trading in the Merton structural model or exogenous default timing in reduced-form intensity models. For instance, timelock constrained governance introduces delays that can amplify runs in ways not modeled in standard frameworks. We will add a dedicated subsection in the Level 1 section that provides specific comparisons, including derivations of altered loss distributions (e.g., showing increased variance or additional jump components due to oracle divergence) and references to the Merton (1974) model and Jarrow-Turnbull reduced-form model. This will include analytical arguments and bounds demonstrating the differences. revision: yes

Circularity Check

No significant circularity in derivation chain

full rationale

The paper outlines a three-level decomposition of vault risk and derives five metrics from six on-chain structural features that purportedly break TradFi analogies. The abstract and summary describe this as a formal grounding followed by an implementable estimation architecture using onchain data, identification strategies, partial identification bounds, and stress scenarios. No equations, self-citations, or fitted parameters are shown reducing the claimed metrics to the input features by construction. The central claims remain logically independent of the listed inputs, with no evidence of self-definitional loops, renamed known results, or load-bearing self-citations in the provided text.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Canonical TradFi credit frameworks provide a valid baseline against which on-chain loss channels can be compared.

Reference graph

Works this paper leans on

-

[1]

Adamyk, B., & Benson, V., et al. (2025). Risk management in DeFi: Analyses of the innovative tools and platforms for tracking DeFi transactions. Journal of Risk and Financial Management, 18(1): 38. DOI: https://doi.org/10.3390/jrfm18010038

-

[2]

Altman, E. I., & Resti, A., et al. (2004). Default recovery rates in credit risk modelling: A review of the literature and empirical evidence. Economic Notes, 33(2), 183--208. DOI: https://doi.org/10.1111/j.0391-5026.2004.00129.x

-

[3]

Angeris, G., & Chitra, T. (2020). Improved price oracles: Constant function market makers. In Proceedings of the 2nd ACM Conference on Advances in Financial Technologies (AFT 2020), pp. 80--91. ACM. DOI: https://doi.org/10.1145/3419614.3423251

-

[4]

Angeris, G., & Kao, H. T., et al. (2020). An analysis of Uniswap markets. Cryptoeconomic Systems, 1(1). DOI: https://doi.org/10.48550/arXiv.1911.03380

-

[5]

Appel, I., & Grennan, J., et al. (2025). Holding the bag: Depositor reactions to a crypto shadow bank collapse. Working paper. University of Virginia (Darden), Emory University, Vanderbilt University, University of Nevada Reno. DOI: https://doi.org/10.2139/ssrn.5551339

-

[6]

R., et al

Arora, N., & Bohn, J. R., et al. (2006). Reduced form versus structural models of credit risk: A case study of three models. In H. G. Fong (Ed.), The Credit Market Handbook: Advanced Modeling Issues (pp. 132--164). Hoboken, NJ: John Wiley & Sons. (Reprinted from Journal of Investment Management.)

2006

-

[7]

Bertomeu, J., & Martin, X., et al. (2024). Measuring DeFi risk. Finance Research Letters, 63: 105321. DOI: https://doi.org/10.1016/j.frl.2024.105321

-

[8]

Brunnermeier, M. K., & Pedersen, L. H. (2009). Market liquidity and funding liquidity. Review of Financial Studies, 22(6), 2201--2238. DOI: https://doi.org/10.1093/rfs/hhn098

-

[9]

Cantor, R., & Packer, F., et al. (1997). Split ratings and the pricing of credit risk. Journal of Fixed Income, 7(3), 72--82. DOI: https://doi.org/10.3905/jfi.1997.408194

-

[10]

Carey, M., & Hrycay, M. (2001). Parameterizing credit risk models with rating data. Journal of Banking & Finance, 25(1), 197--270. DOI: https://doi.org/10.1016/S0378-4266(00)00140-1

-

[11]

Credora Methodology: Ratings and Risk Metrics Drive Informed Decisions

Credora (2025). Credora Methodology: Ratings and Risk Metrics Drive Informed Decisions. Technical Document. Available at: https://docs.credora.io [Retrieved April 2025.]

2025

-

[12]

Daian, P., & Goldfeder, S., et al. (2020). Flash boys 2.0: Frontrunning in decentralized exchanges, miner extractable value, and consensus instability. In 2020 IEEE Symposium on Security and Privacy (SP), pp. 910--927. DOI: https://doi.org/10.1109/SP40000.2020.00040

-

[13]

Diamond, D. W., & Dybvig, P. H. (1983). Bank runs, deposit insurance, and liquidity. Journal of Political Economy, 91(3), 401--419. DOI: https://doi.org/10.1086/261155

-

[14]

Duffie, D., & Eckner, A., et al. (2009). Frailty correlated default. Journal of Finance, 64(5), 2089--2123. DOI: https://doi.org/10.1111/j.1540-6261.2009.01495.x

-

[15]

Duley, C., & Gambacorta, L., et al. (2023). The oracle problem and the future of DeFi. BIS Bulletin, No. 76. Bank for International Settlements, September 7, 2023. Available at: https://www.bis.org/publ/bisbull76.htm

2023

-

[16]

Eldomiaty, T., & Azzam, I., et al. (2025). Determinants of stochastic distance to default. Journal of Risk and Financial Management, 18(2): 91. DOI: https://doi.org/10.3390/jrfm18020091

-

[17]

The Financial Stability Implications of Tokenisation

Financial Stability Board (2024). The Financial Stability Implications of Tokenisation. FSB Report. October 22, 2024. Available at: https://www.fsb.org/2024/10/the-financial-stability-implications-of-tokenisation/

2024

-

[18]

Garc\'ia-C\'espedes, R., & Moreno, M. (2022). The generalized Vasicek credit risk model: A machine learning approach. Finance Research Letters, 47: 102669. DOI: https://doi.org/10.1016/j.frl.2021.102669

-

[19]

Ghosh, R., & Datta, A., et al. (2025). Onchain credit risk score in decentralized finance. arXiv preprint, q-fin.RM. DOI: https://doi.org/10.48550/arXiv.2412.00710

-

[20]

Goldstein, I., & Pauzner, A. (2005). Demand deposit contracts and the probability of bank runs. Journal of Finance, 60(3), 1293--1327. DOI: https://doi.org/10.1111/j.1540-6261.2005.00762.x

-

[21]

Gordy, M. B. (2000). A comparative anatomy of credit risk models. Journal of Banking & Finance, 24(1--2), 119--149. DOI: https://doi.org/10.1016/S0378-4266(99)00050-X

-

[22]

Gorton, G., & Metrick, A. (2012). Securitized banking and the run on repo. Journal of Financial Economics, 104(3), 425--451. DOI: https://doi.org/10.1016/j.jfineco.2011.03.016

-

[23]

Gudgeon, L., & Perez, D., et al. (2020). The decentralized financial crisis. arXiv preprint, cs.CR. DOI: https://doi.org/10.48550/arXiv.2002.08099

-

[24]

Gudgeon, L., & Werner, S., et al. (2020). DeFi protocols for loanable funds: Interest rates, liquidity and market efficiency. In Proceedings of the 2nd ACM Conference on Advances in Financial Technologies (AFT 2020), pp. 92--112. ACM. DOI: https://doi.org/10.1145/3419614.3423249

-

[25]

Iftikhar, E., & Wei, W., et al. (2025). Automated risk management mechanisms in DeFi lending protocols: A crosschain comparative analysis of Aave and Compound. In Proceedings of the 7th IEEE Conference on Blockchain Research & Applications for Innovative Networks and Services (BRAINS 2025). IEEE. DOI: https://doi.org/10.1109/BRAINS67003.2025.11302928

-

[26]

Ikeda, N., & Watanabe, S. (1989). Stochastic Differential Equations and Diffusion Processes.2nd edition. North-Holland & Kodansha

1989

-

[27]

Kiri s ci, M. (2025). An integrated decision-making process for risk analysis of decentralized finance. Neural Computing and Applications, 37: 6021--6051. DOI: https://doi.org/10.1007/s00521-024-10839-2

-

[28]

Klages-Mundt, A., & Harz, D., et al. (2020). Stablecoins 2.0: Economic foundations and risk based models. In Proceedings of the 2nd ACM Conference on Advances in Financial Technologies (AFT 2020), pp. 59--79. ACM. DOI: https://doi.org/10.1145/3419614.3423261

-

[29]

J., & Frey, R., et al

McNeil, A. J., & Frey, R., et al. (2005). Quantitative Risk Management: Concepts, Techniques and Tools. Princeton University Press

2005

-

[30]

Merton, R. C. (1974). On the pricing of corporate debt: The risk structure of interest rates. Journal of Finance, 29(2), 449--470. DOI: https://doi.org/10.1111/j.1540-6261.1974.tb03058.x

-

[31]

Moallemi, Tim Roughgarden, and Anthony Lee Zhang

Milionis, J., & Moallemi, C. C., et al. (2022). Automated market making and loss versus rebalancing. arXiv preprint. [Published in Proceedings of the 2023 ACM Conference on Computer and Communications Security (CCS 2023), pp. 3342--3356.] DOI: https://doi.org/10.48550/arXiv.2208.06046

-

[32]

Moody's Global Approach to Rating Collateralized Loan Obligations

Moody's Investors Service (2021). Moody's Global Approach to Rating Collateralized Loan Obligations. Moody's Rating Methodology. March 19, 2021. Available at: https://www.scribd.com/document/980539217/Moody-s-Rating-Methdology-for-CDOs

-

[33]

Morris, S., & Shin, H. S. (1998). Unique equilibrium in a model of self-fulfilling currency attacks. American Economic Review, 88(3), 587--597. DOI: https://doi.org/10.1257/aer.88.3.587

-

[34]

Müller, A., & Scarsini, M. (2000). Some remarks on the supermodular order. Journal of multivariate analysis, 73(1), 107--119. DOI: https://doi.org/10.1006/jmva.1999.1867

-

[35]

Palaiokrassas, G., & Scherrers, S., et al. (2024). Machine learning in DeFi: Credit risk assessment and liquidation prediction. In Proceedings of the 2024 IEEE International Conference on Blockchain and Cryptocurrency (ICBC). IEEE. DOI: https://doi.org/10.1109/ICBC59979.2024.10634435

-

[36]

Parhizkari, B., & Iannillo, A. K., et al. (2025). Onchain risk signals: Predicting security threats in DeFi projects. In Proceedings of the 2025 IEEE 24th International Conference on Trust, Security and Privacy in Computing and Communications (TrustCom 2025). IEEE. DOI: https://doi.org/10.1109/Trustcom66490.2025.00112

-

[37]

M., et al

Perez, D., & Werner, S. M., et al. (2021). Liquidations: DeFi on a knife edge. In Financial Cryptography and Data Security 2021, Lecture Notes in Computer Science, vol. 12676, pp. 457--476. Springer

2021

-

[38]

Qin, K., & Zhou, L., et al. (2021a). An empirical study of DeFi liquidations: Incentives, risks, and instabilities. In Proceedings of the 2021 ACM Internet Measurement Conference (IMC 2021), pp. 336--350. ACM. DOI: https://doi.org/10.1145/3487552.3487811

-

[39]

Qin, K., & Zhou, L., et al. (2021b). Attacking the DeFi ecosystem with flash loans for fun and profit. In Financial Cryptography and Data Security 2021, Lecture Notes in Computer Science, vol. 12674, pp. 3--32. Springer

2021

-

[40]

Global Methodology and Assumptions for Collateralized Loan Obligations

S&P Global Ratings (2019). Global Methodology and Assumptions for Collateralized Loan Obligations. S&P Global Ratings Criteria. October 8, 2019. Avaliable at: https://www.maalot.co.il/Publications/MT20200319132739.PDF

2019

-

[41]

Treacy, W. F., & Carey, M. (2000). Credit risk rating systems at large US banks. Journal of Banking & Finance, 24(1--2), 167--201. DOI: https://doi.org/10.1016/S0378-4266(99)00056-4

-

[42]

Vasicek, O. A. (1987). Probability of loss on loan portfolio. KMV Corporation working paper. [Republished as: Vasicek, O. A. (2002). Loan portfolio value. Risk, 15(12), 160--162.]

1987

-

[43]

In Proceedings of the 4th ACM Conference on Advances in Financial Technolo- gies

Werner, S. M., & Perez, D., et al. (2022). SoK: Decentralized finance (DeFi). In Proceedings of the 4th ACM Conference on Advances in Financial Technologies (AFT 2022). ACM. DOI: https://doi.org/10.1145/3558535.3559780

-

[44]

Zetzsche, D. A., & Arner, D. W., et al. (2020). Decentralized finance. Journal of Financial Regulation, 6(2): 172--203. DOI: https://doi.org/10.1093/jfr/fjaa010

-

[45]

Zhang, S., & Wang, Z., et al. (2026). Systemic risk in DeFi: A network based fragility analysis of TVL dynamics. arXiv preprint, q-fin.RM. DOI: https://doi.org/10.48550/arXiv.2601.08540

-

[46]

Zhou, P., & Zhang, Y. (2026). Major conundrums and possible solutions in DeFi insurance. International Journal of Finance & Economics, 31: 489--501. DOI: https://doi.org/10.1002/ijfe.3154

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.