Recognition: unknown

Identifying dynamical network markers of financial market instability

Pith reviewed 2026-05-08 13:45 UTC · model grok-4.3

The pith

Dynamical network markers from trader activities flag large price movements on a daily scale.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

By constructing multivariate time series from the trading activities of market participants identified via virtual server IDs, dynamical network markers associated with critical slowing down can identify early warning signals of large price movements on a daily time scale.

What carries the argument

Dynamical Network Marker (DNM) theory, which extracts critical slowing down indicators from high-dimensional systems of many interacting elements.

If this is right

- Early warning signals for large price movements become detectable on daily time scales using participant activity data.

- Refining the forecasting horizon and integrating multiple trading time series can support operational early-warning systems.

- Treating market participants as the interacting elements allows DNM theory to move beyond traditional change-point detection in market data.

Where Pith is reading between the lines

- The same participant-based time series construction could be tested on data from other exchanges to check if daily DNM signals generalize across markets.

- Daily-scale warnings open the possibility of building monitoring dashboards that combine DNM metrics with regulatory or trading-volume thresholds.

- If critical slowing down holds at this granularity, extensions to intraday or tick-level series might reveal shorter-horizon signals without changing the core participant-element model.

Load-bearing premise

The multivariate time series built from virtual server IDs capture the critical slowing down signatures expected before instability, with each ID representing a distinct interacting participant whose daily activity dynamics are observable.

What would settle it

A large price movement occurring without preceding DNM indicators in the participant time series, or repeated DNM signals that do not precede large movements, would undermine the detection claim.

Figures

read the original abstract

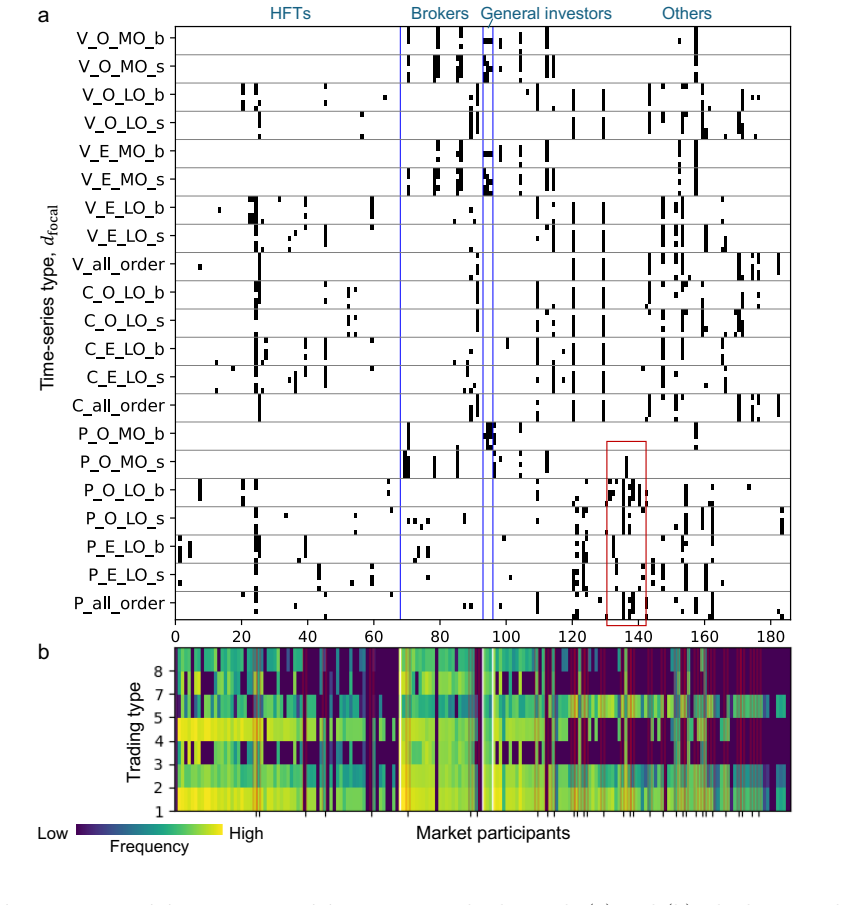

Market instability has been extensively studied using mathematical approaches to characterize complex trading dynamics and detect structural change points. This study explores the potential for early warning of market instability by applying the Dynamical Network Marker (DNM) theory to order placement and execution data from the Tokyo Stock Exchange. DNM theory identifies indicators associated with critical slowing down -- a precursor to critical transitions -- in high-dimensional systems of many interacting elements. In this study, market participants are identified using virtual server IDs from the trading system, and multivariate time series representing their trading activities are constructed. This framework treats each participant as an interacting element, thereby enabling the application of DNM theory to the resulting time series. The results suggest that early warning signals of large price movements can be detected on a daily time scale. These findings highlight the potential to develop practical DNM-based early-warning systems for large price movements by further refining forecasting horizons and integrating multiple time series capturing different aspects of trading behavior.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper applies Dynamical Network Marker (DNM) theory to order placement and execution data from the Tokyo Stock Exchange. Market participants are identified via virtual server IDs, and multivariate time series of their trading activities are constructed to detect indicators of critical slowing down as precursors to large price movements. The results suggest these early warning signals can be detected on a daily time scale, with potential for practical DNM-based forecasting systems after refining horizons and integrating additional series.

Significance. If the empirical link between DNM signatures and subsequent price moves holds after proper validation, the work could extend DNM applications to high-dimensional financial systems and demonstrate value in participant-level trading data for instability forecasting. It offers a framework for treating traders as interacting elements, which may inform real-time monitoring tools if quantitative robustness is established.

major comments (2)

- [Abstract] Abstract: The central claim that 'early warning signals of large price movements can be detected on a daily time scale' is unsupported by any quantitative details on DNM indicator calculations, threshold selection, statistical tests, out-of-sample performance, number of events analyzed, or how the multivariate series were constructed/normalized from virtual server data. This prevents evaluation of whether the data-to-claim link is sound.

- [Abstract] Data construction and timescale (implied in Abstract and methods description): Daily binning of high-frequency order data (ms-to-second scale) is used without justification or test that it preserves critical slowing down signatures (variance/autocorrelation increases). DNM theory requires sampling near the bifurcation timescale; aggregation over many relaxation events risks suppressing the predicted indicators, undermining the daily-resolution claim.

minor comments (1)

- [Abstract] Abstract: Consider adding one sentence on the specific DNM metrics (e.g., which combination of variance, autocorrelation, or network measures) and the forecast horizon tested to improve clarity for readers unfamiliar with the application.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed comments. We address each major point below and have revised the manuscript to improve clarity and support for the claims.

read point-by-point responses

-

Referee: [Abstract] Abstract: The central claim that 'early warning signals of large price movements can be detected on a daily time scale' is unsupported by any quantitative details on DNM indicator calculations, threshold selection, statistical tests, out-of-sample performance, number of events analyzed, or how the multivariate series were constructed/normalized from virtual server data. This prevents evaluation of whether the data-to-claim link is sound.

Authors: The abstract is intended as a concise summary; the quantitative details on DNM indicator calculations (variance and autocorrelation of the leading eigenvector from the participant covariance matrix), threshold selection (95th percentile of baseline periods), statistical tests (bootstrap and permutation tests for significance), out-of-sample performance (rolling-window validation), number of events (multiple large price movements across the dataset), and multivariate series construction (normalized trading volume and frequency per virtual server ID) are provided in the Methods and Results sections. To facilitate immediate evaluation of the claim, we have revised the abstract to incorporate key quantitative elements while remaining within length constraints. revision: yes

-

Referee: [Abstract] Data construction and timescale (implied in Abstract and methods description): Daily binning of high-frequency order data (ms-to-second scale) is used without justification or test that it preserves critical slowing down signatures (variance/autocorrelation increases). DNM theory requires sampling near the bifurcation timescale; aggregation over many relaxation events risks suppressing the predicted indicators, undermining the daily-resolution claim.

Authors: We acknowledge the importance of timescale alignment in DNM theory. Daily binning was selected to match the daily horizon of the target large price movements and to support practical forecasting applications. We have added a justification in the Methods section explaining that the slow dynamics associated with critical slowing down are captured at this aggregation level. We also include sensitivity tests comparing daily bins to finer intra-day aggregations, confirming that increases in variance and lag-1 autocorrelation remain detectable and are not suppressed, consistent with the theory when the sampling resolves the relevant relaxation timescale near the transition. revision: yes

Circularity Check

No significant circularity; empirical application of established DNM theory

full rationale

The paper constructs multivariate time series from virtual-server trading data and applies DNM theory to detect critical slowing down signatures before large price moves. The derivation relies on citing DNM predictions from prior literature and reporting empirical indicators on daily scales, without any visible equations that define a quantity in terms of itself, fit parameters to a subset then rename the fit as a prediction, or invoke self-citations as the sole justification for uniqueness or ansatz choices. The central result is an observational claim about detectable signals rather than a closed mathematical loop reducing to its inputs by construction.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption DNM theory identifies indicators associated with critical slowing down in high-dimensional systems of many interacting elements

Reference graph

Works this paper leans on

-

[1]

, author Flood, M

author Bisias, D. , author Flood, M. , author Lo, A. W. & author Valavanis, S. title A survey of systemic risk analytics . journal Annu. Rev. Financ. Econ. volume 4 , pages 255--296 ( year 2012 )

2012

-

[2]

author Jackson, M. O. & author Pernoud, A. title Systemic risk in financial networks: A survey . journal Annu. Rev. Econ. volume 13 , pages 171--202 ( year 2021 )

2021

-

[3]

author Battiston, S. et al. title Complexity theory and financial regulation . journal Science volume 351 , pages 818--819 ( year 2016 )

2016

-

[4]

& author Dro \.z d \.z , S

author Kwapie \'n , J. & author Dro \.z d \.z , S. title Physical approach to complex systems . journal Phys. Rep. volume 515 , pages 115--226 ( year 2012 )

2012

-

[5]

author May, R. M. , author Levin, S. A. & author Sugihara, G. title Ecology for bankers . journal Nature volume 451 , pages 893--894 ( year 2008 )

2008

-

[6]

, author Di Clemente, R

author Saracco, F. , author Di Clemente, R. , author Gabrielli, A. & author Squartini, T. title Detecting early signs of the 2007--2008 crisis in the world trade . journal Sci. Rep. volume 6 , pages 30286 ( year 2016 )

2007

-

[7]

author Abad, J. et al. title Shedding light on dark markets: First insights from the new EU-wide OTC derivatives dataset . journal ESRB: Occasional Paper Series ( year 2016 )

2016

-

[8]

author Bardoscia, M. et al. title The physics of financial networks . journal Nat. Rev. Phys. volume 3 , pages 490--507 ( year 2021 )

2021

-

[9]

author Yellen, J. L. title Interconnectedness and systemic risk: Lessons from the financial crisis and policy implications. Speech by Ms Janet L Yellen, Vice chair of the board of governments of the federal reserve system, at the American economic association/American finance association joint luncheon, San Diego, California. ( year 2013 ). ://www.federal...

2013

-

[10]

, author Lillo, F

author Bonanno, G. , author Lillo, F. & author Mantegna, R. N. title High-frequency cross-correlation in a set of stocks . journal Quant. Finance volume 1 , ( year 2001 )

2001

-

[11]

& author Franca, I

author Sandoval Jr., L. & author Franca, I. D. P. title Correlation of financial markets in times of crisis . journal Physica A: Stat. Mec. Appl. volume 391 , pages 187--208 ( year 2012 )

2012

-

[12]

, author Piilo, J

author Musciotto, F. , author Piilo, J. & author Mantegna, R. N. title High-frequency trading and networked markets . journal Proc. Natl. Acad. Sci. U.S.A. volume 118 , pages e2015573118 ( year 2021 )

2021

-

[13]

author Scheffer, M. et al. title Early-warning signals for critical transitions . journal Nature volume 461 , pages 53--59 ( year 2009 )

2009

-

[14]

author Drake, J. M. & author Griffen, B. D. title Early warning signals of extinction in deteriorating environments . journal Nature volume 467 , pages 456--459 ( year 2010 )

2010

-

[15]

, author Liu, R

author Aihara, K. , author Liu, R. , author Koizumi, K. , author Liu, X. & author Chen, L. title Dynamical network biomarkers: Theory and applications . journal Gene volume 808 , pages 145997 ( year 2022 )

2022

-

[16]

, author Liu, R

author Chen, L. , author Liu, R. , author Liu, Z. P. , author Li, M. & author Aihara, K. title Detecting early-warning signals for sudden deterioration of complex diseases by dynamical network biomarkers . journal Sci. Rep. volume 2 , pages 347 ( year 2012 )

2012

-

[17]

author Koizumi, K. et al. title Identifying pre-disease signals before metabolic syndrome in mice by dynamical network biomarkers . journal Sci. Rep. volume 9 , pages 8767 ( year 2019 )

2019

-

[18]

, author Hirshleifer, D

author Bikhchandani, S. , author Hirshleifer, D. & author Welch, I. title Learning from the behavior of others: Conformity, fads, and informational cascades . journal J. Econ. Perspect. volume 12 , pages 151--170 ( year 1998 )

1998

-

[19]

author Hawkes, A. G. title Hawkes processes and their applications to finance: a review . journal Quant. Finance volume 18 , pages 193--198 ( year 2018 )

2018

-

[20]

, author Wehrli, A

author Wheatley, S. , author Wehrli, A. & author Sornette, D. title The endo--exo problem in high frequency financial price fluctuations and rejecting criticality . journal Quant. Finance volume 19 , pages 1165--1178 ( year 2019 )

2019

-

[21]

, author Mastromatteo, I

author Bacry, E. , author Mastromatteo, I. & author Muzy, J.-F. title Hawkes processes in finance . journal Mark. Microstruct. Liq. volume 1 , pages 1550005 ( year 2015 )

2015

-

[22]

author Ito, M. I. , author Honma, Y. , author Ohnishi, T. , author Watanabe, T. & author Aihara, K. title Exogenous and endogenous factors affecting stock market transactions: A Hawkes process analysis of the Tokyo Stock Exchange during the COVID-19 pandemic . journal PLOS ONE volume 19 , pages e0301462 ( year 2024 )

2024

-

[23]

title Rational herds: Economic models of social learning ( publisher Cambridge University Press , year 2004 )

author Chamley, C. title Rational herds: Economic models of social learning ( publisher Cambridge University Press , year 2004 )

2004

-

[24]

, author Jotikasthira, C

author Ellul, A. , author Jotikasthira, C. & author Lundblad, C. T. title Regulatory pressure and fire sales in the corporate bond market . journal J. Financ. Econ. volume 101 , pages 596--620 ( year 2011 )

2011

-

[25]

, author Chen, P

author Liu, R. , author Chen, P. , author Aihara, K. & author Chen, L. title Identifying early-warning signals of critical transitions with strong noise by dynamical network markers . journal Sci. Rep. volume 5 , pages 17501 ( year 2015 )

2015

-

[26]

, author Aihara, K

author Oya, S. , author Aihara, K. & author Hirata, Y. title Forecasting abrupt changes in foreign exchange markets: method using dynamical network marker . journal New J. Phys. volume 16 , pages 115015 ( year 2014 )

2014

-

[27]

, author Wang, Y

author Liu, X. , author Wang, Y. , author Ji, H. , author Aihara, K. & author Chen, L. title Personalized characterization of diseases using sample-specific networks . journal Nucleic Acids Res. volume 44 , pages e164 ( year 2016 )

2016

-

[28]

, author Aihara, K

author Masuda, N. , author Aihara, K. & author MacLaren, N. G. title Anticipating regime shifts by mixing early warning signals from different nodes . journal Nat. Commun. volume 15 , pages 1086 ( year 2024 )

2024

-

[29]

, author Oku, M

author Nakagawa, T. , author Oku, M. & author Aihara, K. title Early warning signals by dynamical network markers (in Japanese) . journal SEISAN KENKYU volume 68 , pages 271--274 ( year 2016 )

2016

-

[30]

, author Tobe, R

author Goshima, K. , author Tobe, R. & author Uno, J. title Trader classification by cluster analysis: Interaction between HFTs and other traders . journal Waseda University Institute for Business and Finance, Working Paper Series pages 1--46 ( year 2019 )

2019

-

[31]

& author Tsuda, H

author Ohyama, A. & author Tsuda, H. title Arugorizumu-ka kijun ni yoru kohindotori-hiki (HFT) no tokusei bunseki (in Japanese) . journal JAFEE Journal volume 20 , pages 55--69 ( year 2022 )

2022

-

[32]

& author Kanazawa, K

author Sato, Y. & author Kanazawa, K. title Inferring microscopic financial information from the long memory in market-order flow: A quantitative test of the Lillo-Mike-Farmer model . journal Phys. Rev. Lett. volume 131 , pages 197401 ( year 2023 )

2023

-

[33]

title High frequency trading in the Japanese stock market (in Japanese)

author Yamada, M. title High frequency trading in the Japanese stock market (in Japanese) . journal TCER Working Paper Series pages 1--23 ( year 2023 )

2023

-

[34]

, author Jo, H

author Karsai, M. , author Jo, H. H. & author Kaski, K. title Bursty human dynamics ( publisher Springer , year 2018 )

2018

-

[35]

title Special quotation (SQ) (in Japanese)

author Japan Exchange Group . title Special quotation (SQ) (in Japanese) . howpublished https://www.jpx.co.jp/glossary/ta/326.html ( year n.d. ). note Accessed: 2025-12-01

2025

-

[36]

, author Podobnik, B

author Zheng, Z. , author Podobnik, B. , author Feng, L. & author Li, B. title Changes in cross-correlations as an indicator for systemic risk . journal Sci. Rep. volume 2 , pages 888 ( year 2012 )

2012

-

[37]

& author Li, H

author Song, S. & author Li, H. title Early warning signals for stock market crashes: empirical and analytical insights utilizing nonlinear methods . journal EPJ Data Sci. volume 13 , pages 16 ( year 2024 )

2024

-

[38]

title Ensemble methods: foundations and algorithms ( publisher CRC press , year 2025 )

author Zhou, Z.-H. title Ensemble methods: foundations and algorithms ( publisher CRC press , year 2025 )

2025

-

[39]

author Ito, M. I. & author Sasaki, A. title Casting votes of antecedents play a key role in successful sequential decision-making . journal PLOS ONE volume 18 , pages e0282062 ( year 2023 )

2023

-

[40]

, author Zlati \'c , V

author Klin c i \'c , L. , author Zlati \'c , V. , author Caldarelli, G. & author S tefan c i \'c , H. title Systemic risk measured by the resiliency of the system to initial shocks . journal Phys. Rev. E volume 108 , pages 044303 ( year 2023 )

2023

-

[41]

, author Slotine, J.-J

author Liu, Y.-Y. , author Slotine, J.-J. & author Barab \'a si, A.-L. title Controllability of complex networks . journal Nature volume 473 , pages 167--173 ( year 2011 )

2011

-

[42]

title Analysis of high-frequency trading at Tokyo Stock Exchange

author Hosaka, G. title Analysis of high-frequency trading at Tokyo Stock Exchange . journal JPX working paper pages 1--37 ( year 2014 )

2014

-

[43]

, author Okude, S

author Ohyama, A. , author Okude, S. , author Suzuki, K. & author Fukuyama, Y. title K \=o soku torihiki k \=o i no tokusei bunseki (in Japanese) . journal Financial Services Agency, Japan ( year 2021 ). note Available at: https://www.fsa.go.jp/frtc/report/honbun/2021/20210707_SR_HFT_Article.pdf

2021

-

[44]

, author Wang, D

author Podobnik, B. , author Wang, D. , author Horvatic, D. , author Grosse, I. & author Stanley, H. E. title Time-lag cross-correlations in collective phenomena . journal EPL volume 90 , pages 68001 ( year 2010 )

2010

-

[45]

& author Jo, H.-H

author Kim, E.-K. & author Jo, H.-H. title Measuring burstiness for finite event sequences . journal Phys. Rev. E volume 94 , pages 032311 ( year 2016 )

2016

-

[46]

& author Aihara, K

author Hirata, Y. & author Aihara, K. title Timing matters in foreign exchange markets . journal Physica A: Stat. Mech. Appl. volume 391 , pages 760--766 ( year 2012 )

2012

-

[47]

, author Fortunato, S

author Menczer, F. , author Fortunato, S. & author Davis, C. A. title A first course in network science ( publisher Cambridge University Press , year 2020 )

2020

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.