Particle Methods with Deep Learning for Stochastic Control under Partial Observation

Pith reviewed 2026-06-27 15:53 UTC · model grok-4.3

The pith

Particle approximations replace conditional distributions in partially observed stochastic control and converge under suitable assumptions.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Under suitable assumptions the fully discretized particle approximation converges to the original continuous-time partially observed control problem; the particle reformulation remains permutation-invariant and therefore compatible with symmetric neural networks, which in turn support both a direct optimization method for feedback controls and a Deep BSDE method, with the same framework extending to partially observed mean-field control.

What carries the argument

The weighted particle system that approximates the conditional distribution of the hidden state, which carries the argument by converting the infinite-dimensional filtering state into a finite-dimensional, permutation-invariant object.

If this is right

- The method applies directly to linear-quadratic partially observed problems and to nonlinear partially observed mean-field control.

- Symmetric neural networks can be trained on the particle representation for both feedback control optimization and backward stochastic differential equation problems.

- The same particle-plus-deep-learning pipeline extends to financial applications including portfolio liquidation and asset allocation.

- Convergence holds once the common-noise-adapted control limit theory is combined with the particle discretization.

Where Pith is reading between the lines

- The same particle replacement might apply to other filtering-based decision problems outside stochastic control, such as sequential estimation tasks.

- Permutation-invariant architectures could reduce sample complexity in additional high-dimensional control settings that possess exchangeable structure.

- Explicit error rates between the particle system and the true filter would make the method easier to calibrate in practice.

Load-bearing premise

The particle system can faithfully replace the conditional distribution of the hidden state under the chosen discretization.

What would settle it

A numerical test in which the computed value or control fails to approach the known optimum as the number of particles increases and the time step decreases would falsify the convergence claim.

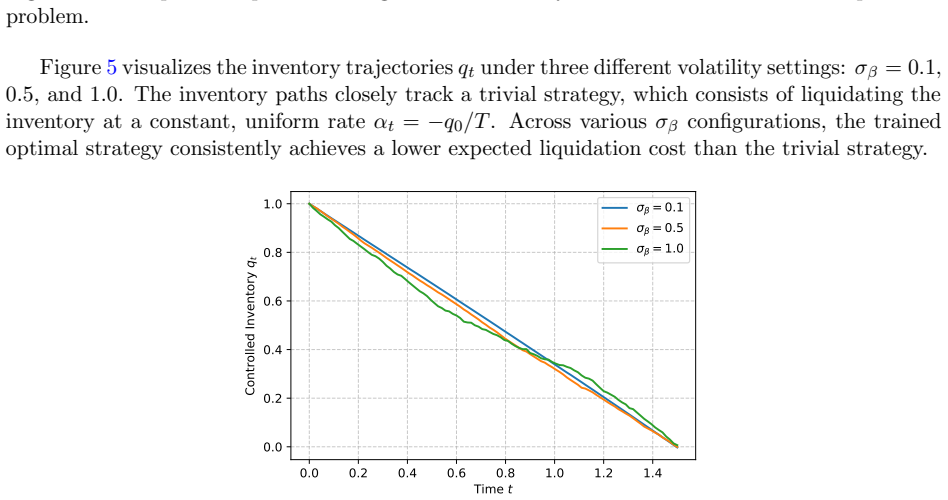

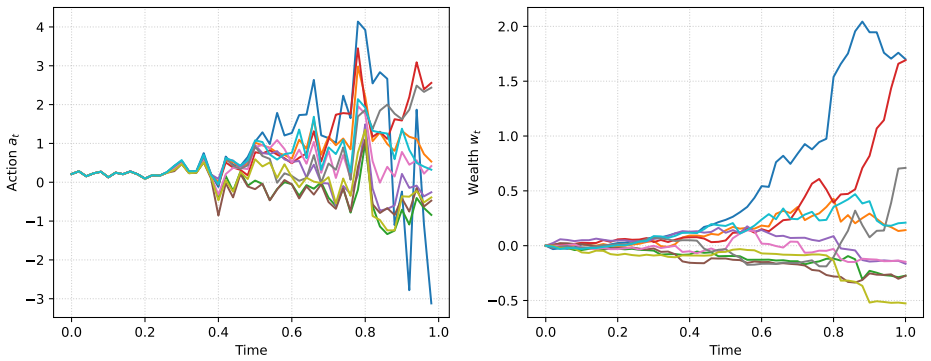

Figures

read the original abstract

Numerical computation of stochastic control problems under partial observation is challenging because the dynamic programming formulation is naturally posed on the conditional distribution of the hidden state. We propose particle-based methods that replace this infinite-dimensional filtering state by a finite-dimensional weighted particle system, building on recent limit theory for mean-field control with common-noise-adapted controls. We prove, under suitable assumptions, convergence of the fully discretized particle approximation to the original continuous-time partially observed control problem. The particle reformulation is high-dimensional but permutation-invariant, a structure that can be exploited by symmetric neural network architectures. We develop two deep learning algorithms: a direct optimization method for feedback controls and a Deep BSDE method for particle problems admitting a backward stochastic differential equation representation. We also extend the computational framework to partially observed mean-field control problems, which have been studied theoretically but remain less developed numerically. Numerical experiments on a linear--quadratic benchmark, a nonlinear partially observed mean-field control problem, and two financial applications, portfolio liquidation and asset allocation, demonstrate the accuracy and practical utility of the approach.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops particle-based numerical methods combined with deep learning for stochastic control problems under partial observation. It replaces the infinite-dimensional conditional distribution of the hidden state by a finite weighted particle system, builds on mean-field control limit theory with common-noise-adapted controls, proves convergence of the fully discretized approximation to the original continuous-time problem under suitable assumptions, proposes a direct optimization algorithm and a Deep BSDE algorithm exploiting permutation invariance via symmetric networks, extends the framework to partially observed mean-field control, and reports numerical results on an LQ benchmark, a nonlinear mean-field example, and two financial applications (portfolio liquidation and asset allocation).

Significance. If the convergence result holds with the stated assumptions, the work supplies a practical, scalable route to high-dimensional partially observed control problems by marrying particle approximations with permutation-invariant neural architectures. The explicit extension to mean-field control and the two distinct deep-learning algorithms are concrete contributions that could be adopted in finance and engineering applications where filtering and control must be solved jointly.

major comments (3)

- [convergence theorem] Convergence theorem (the statement that the fully discretized particle system converges to the original continuous-time partially observed control problem): the argument transfers limit theory for mean-field control with common-noise-adapted controls, yet the manuscript supplies no explicit verification or auxiliary lemma showing that the chosen time discretization, particle-weight update rule, and neural-network approximation of the control preserve the required measurability and regularity properties with respect to the common noise. This transfer is load-bearing for the central claim.

- [Deep BSDE algorithm] Deep BSDE algorithm section: the reformulation of the particle problem as a backward stochastic differential equation is asserted but the derivation of the BSDE coefficients (especially the driver that incorporates the particle approximation of the filter) is not displayed; without this step it is impossible to confirm that the neural-network approximation remains adapted to the correct filtration.

- [numerical experiments] Numerical experiments (linear-quadratic benchmark and financial examples): the reported accuracy figures are given without accompanying error bounds derived from the convergence theorem, without a statement of the precise discretization parameters (time step, number of particles, network width), and without an explicit rule for data exclusion or out-of-sample testing; these omissions make it difficult to assess whether the observed performance is consistent with the theoretical guarantee.

minor comments (2)

- Notation for the particle weights and the empirical measure should be introduced once with a single consistent symbol rather than redefined in each algorithm subsection.

- [introduction] The abstract states that the reformulation is 'high-dimensional but permutation-invariant'; a short paragraph in the introduction clarifying how the symmetry is exploited by the chosen network architecture would improve readability.

Simulated Author's Rebuttal

We thank the referee for the thorough review and constructive suggestions. The comments identify areas where additional detail will strengthen the presentation of the convergence result, the Deep BSDE derivation, and the numerical experiments. We address each point below and will revise the manuscript accordingly.

read point-by-point responses

-

Referee: [convergence theorem] Convergence theorem (the statement that the fully discretized particle system converges to the original continuous-time partially observed control problem): the argument transfers limit theory for mean-field control with common-noise-adapted controls, yet the manuscript supplies no explicit verification or auxiliary lemma showing that the chosen time discretization, particle-weight update rule, and neural-network approximation of the control preserve the required measurability and regularity properties with respect to the common noise. This transfer is load-bearing for the central claim.

Authors: We agree that an explicit verification step would make the transfer of the mean-field limit theory fully rigorous. The time discretization, particle-weight updates, and neural-network controls are constructed to satisfy the measurability and regularity conditions of the referenced common-noise mean-field control framework, but this is currently implicit. In the revision we will insert an auxiliary lemma that directly checks these properties for the fully discretized scheme. revision: yes

-

Referee: [Deep BSDE algorithm] Deep BSDE algorithm section: the reformulation of the particle problem as a backward stochastic differential equation is asserted but the derivation of the BSDE coefficients (especially the driver that incorporates the particle approximation of the filter) is not displayed; without this step it is impossible to confirm that the neural-network approximation remains adapted to the correct filtration.

Authors: We accept that the derivation of the BSDE driver, including the explicit dependence on the particle filter, must be written out. The driver is obtained by substituting the empirical measure of the weighted particles into the original generator and verifying that the resulting process remains adapted to the observation filtration. The revised manuscript will contain this step-by-step derivation together with a short argument confirming the required adaptation property. revision: yes

-

Referee: [numerical experiments] Numerical experiments (linear-quadratic benchmark and financial examples): the reported accuracy figures are given without accompanying error bounds derived from the convergence theorem, without a statement of the precise discretization parameters (time step, number of particles, network width), and without an explicit rule for data exclusion or out-of-sample testing; these omissions make it difficult to assess whether the observed performance is consistent with the theoretical guarantee.

Authors: We will augment the numerical section with the exact discretization parameters used in each example, a brief discussion of how the observed errors align with the convergence result (noting that the theorem currently yields qualitative rather than quantitative rates), and a clear description of the train/test split and out-of-sample evaluation protocol. These additions will allow readers to relate the reported performance directly to the theoretical framework. revision: yes

Circularity Check

No circularity: convergence claim rests on external mean-field limit theory

full rationale

The paper's central result is a convergence theorem for the discretized particle approximation to the partially observed control problem. This is explicitly stated to build on 'recent limit theory for mean-field control with common-noise-adapted controls' and to hold 'under suitable assumptions.' No equations or steps in the provided abstract reduce a claimed prediction or uniqueness result to a fitted parameter, self-definition, or self-citation chain internal to the paper. The particle reformulation is presented as a modeling choice whose convergence is proved externally rather than by construction. This matches the default expectation of a self-contained derivation against external benchmarks.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Recent limit theory for mean-field control with common-noise-adapted controls holds and transfers to the partially observed setting.

Reference graph

Works this paper leans on

-

[1]

Bachouch, C

A. Bachouch, C. Hur \'e , N. Langren \'e , and H. Pham , Deep neural networks algorithms for stochastic control problems on finite horizon: numerical applications , Methodology and Computing in Applied Probability, 24 (2022), pp. 143--178

2022

-

[2]

Balata, C

A. Balata, C. Hur \'e , M. Lauri \`e re, H. Pham, and I. Pimentel , A class of finite-dimensional numerically solvable M ckean-- V lasov control problems , ESAIM: Proceedings and Surveys, 65 (2019), pp. 114--144

2019

- [3]

-

[4]

Bensoussan , Stochastic control of partially observable systems , Cambridge University Press, Cambridge, 1992

A. Bensoussan , Stochastic control of partially observable systems , Cambridge University Press, Cambridge, 1992

1992

-

[5]

Bensoussan and J

A. Bensoussan and J. H. van Schuppen , Optimal control of partially observable stochastic systems with an exponential-of-integral performance index , SIAM Journal on Control and Optimization, 23 (1985), pp. 599--613

1985

-

[6]

B. Bouchard and X. Tan , Limit theory for mean-field control problems with common noise adapted controls , arXiv preprint arXiv:2509.14734, (2025)

-

[7]

Buckdahn, J

R. Buckdahn, J. Li, and J. Ma , A mean-field stochastic control problem with partial observations , The Annals of Applied Probability, (2017)

2017

-

[8]

2004--2023

height 2pt depth -1.6pt width 23pt, A general conditional M ckean-- V lasov stochastic differential equation , The Annals of Applied Probability, 33 (2023), pp. 2004--2023

2023

-

[9]

Carmona and M

R. Carmona and M. Lauri \`e re , Convergence analysis of machine learning algorithms for the numerical solution of mean field control and games , The Annals of Applied Probability, 32 (2022), pp. 4065--4105

2022

-

[10]

M. H. Davis and P. Varaiya , Dynamic programming conditions for partially observable stochastic systems , SIAM Journal on Control, 11 (1973), pp. 226--261

1973

-

[11]

G. Dayanikli, M. Lauri \`e re, and J. Zhang , Deep learning for population-dependent controls in mean field control problems with common noise , arXiv preprint arXiv:2306.04788, (2023)

- [12]

-

[13]

El Karoui, D

N. El Karoui, D. H. Nguyen, and M. Jeanblanc-Picqu \'e , Existence of an optimal M arkovian filter for the control under partial observations , SIAM journal on control and optimization, 26 (1988), pp. 1025--1061

1988

-

[14]

W. H. Fleming , Measure-valued processes in the control of partially-observable stochastic systems , Applied Mathematics and Optimization, 6 (1980), pp. 271--285

1980

-

[15]

M. Fuhrman, H. Pham, and S. Ruda , Optimal control of M ckean- V lasov systems under partial observation and hidden markov switching , arXiv preprint arXiv:2601.09311, (2026)

-

[16]

Germain, M

M. Germain, M. Lauri \`e re, H. Pham, and X. Warin , Deepsets and their derivative networks for solving symmetric PDE s , Journal of Scientific Computing, 91 (2022), p. 63

2022

-

[17]

Gozzi and A

F. Gozzi and A. \'S wiech , H amilton-- J acobi-- B ellman equations for the optimal control of the duncan--mortensen--zakai equation , Journal of Functional Analysis, 172 (2000), pp. 466--510

2000

-

[18]

Graham and D

C. Graham and D. Talay , Stochastic simulation and M onte C arlo methods: mathematical foundations of stochastic simulation , vol. 68, Springer Science & Business Media, 2013

2013

-

[19]

Deep Learning Approximation for Stochastic Control Problems

J. Han and W. E , Deep learning approximation for stochastic control problems , Deep Reinforcement Learning Workshop, NIPS, arXiv preprint arXiv:1611.07422, (2016)

work page internal anchor Pith review Pith/arXiv arXiv 2016

-

[20]

Han and R

J. Han and R. Hu , Recurrent neural networks for stochastic control problems with delay , Mathematics of Control, Signals, and Systems, 33 (2021), pp. 775--795

2021

-

[21]

J. Han, A. Jentzen, and W. E , Solving high-dimensional partial differential equations using deep learning , Proceedings of the National Academy of Sciences, 115 (2018), pp. 8505--8510

2018

-

[22]

Han and J

J. Han and J. Long , Convergence of the deep BSDE method for coupled FBSDE s , Probability, Uncertainty and Quantitative Risk, 5 (2020), p. 5

2020

-

[23]

Y. Li, X. Tan, and S. Tang , Discrete-time approximation of stochastic optimal control with partial observation , SIAM Journal on Control and Optimization, 62 (2024), pp. 326--350

2024

-

[24]

Lions , Viscosity solutions of fully nonlinear second-order equations and optimal stochastic control in infinite dimensions

P.-L. Lions , Viscosity solutions of fully nonlinear second-order equations and optimal stochastic control in infinite dimensions. iii. uniqueness of viscosity solutions for general second-order equations , Journal of Functional Analysis, 86 (1989), pp. 1--18

1989

-

[25]

Pham , Portfolio optimization under partial observation: theoretical and numerical aspects , (2008)

H. Pham , Portfolio optimization under partial observation: theoretical and numerical aspects , (2008)

2008

-

[26]

H. Wan, G. Wang, and J. Xiong , Discrete--time partially observable stochastic optimal control problems of M ckean-- V lasov type and branching particle system approximations , IEEE Transactions on Automatic Control, (2025)

2025

-

[27]

Zhang , Backward stochastic differential equations , in Backward Stochastic Differential Equations: From Linear to Fully Nonlinear Theory, Springer, 2017, pp

J. Zhang , Backward stochastic differential equations , in Backward Stochastic Differential Equations: From Linear to Fully Nonlinear Theory, Springer, 2017, pp. 79--99

2017

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.