Option prices from operational-time reaction-boundary lattices

Pith reviewed 2026-06-27 14:07 UTC · model grok-4.3

The pith

An operational-time Markov lattice on log-prices yields a generalized European option pricing PDE that recovers Black-Scholes-Merton under risk-neutral drift and constant volatility.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

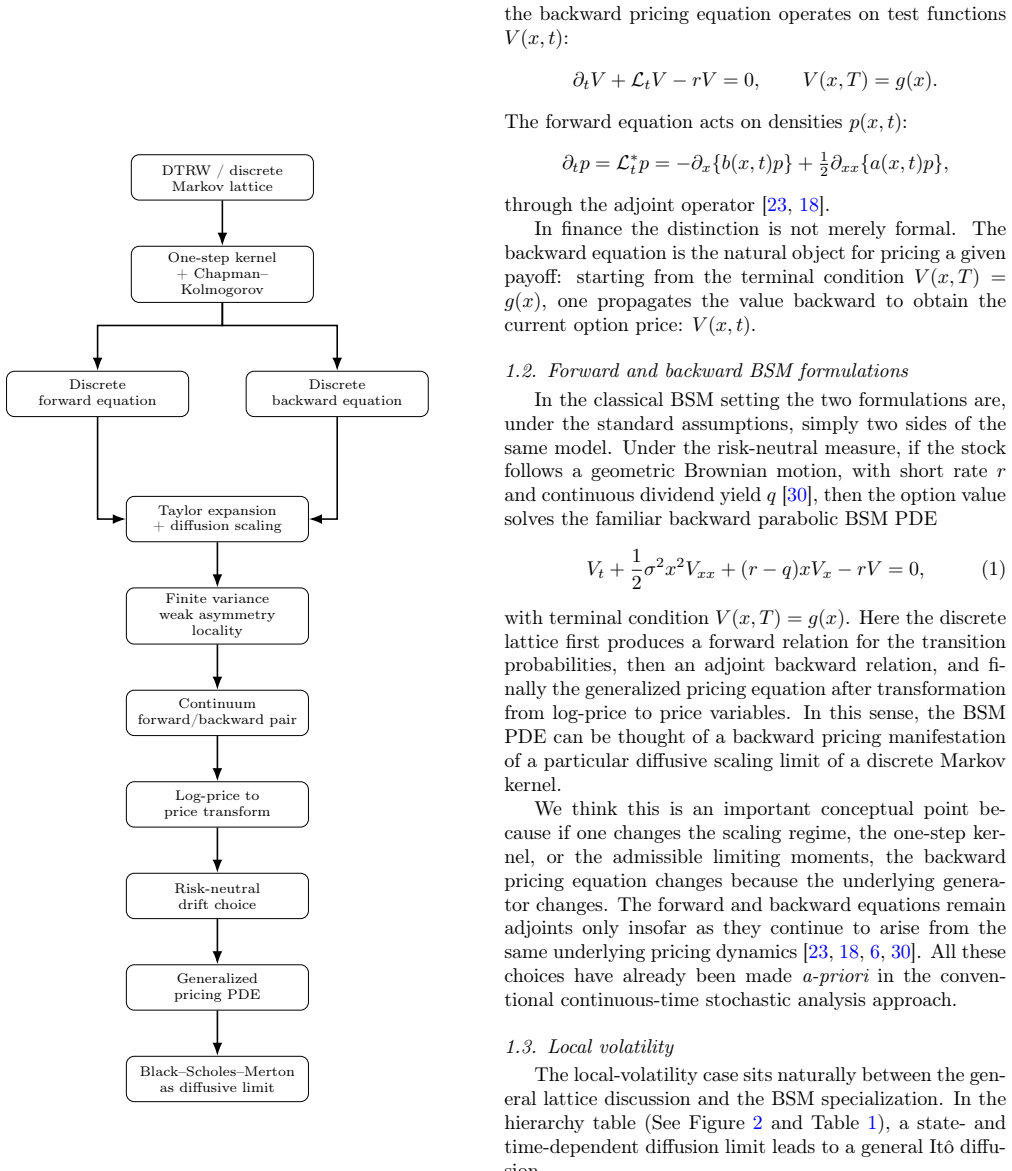

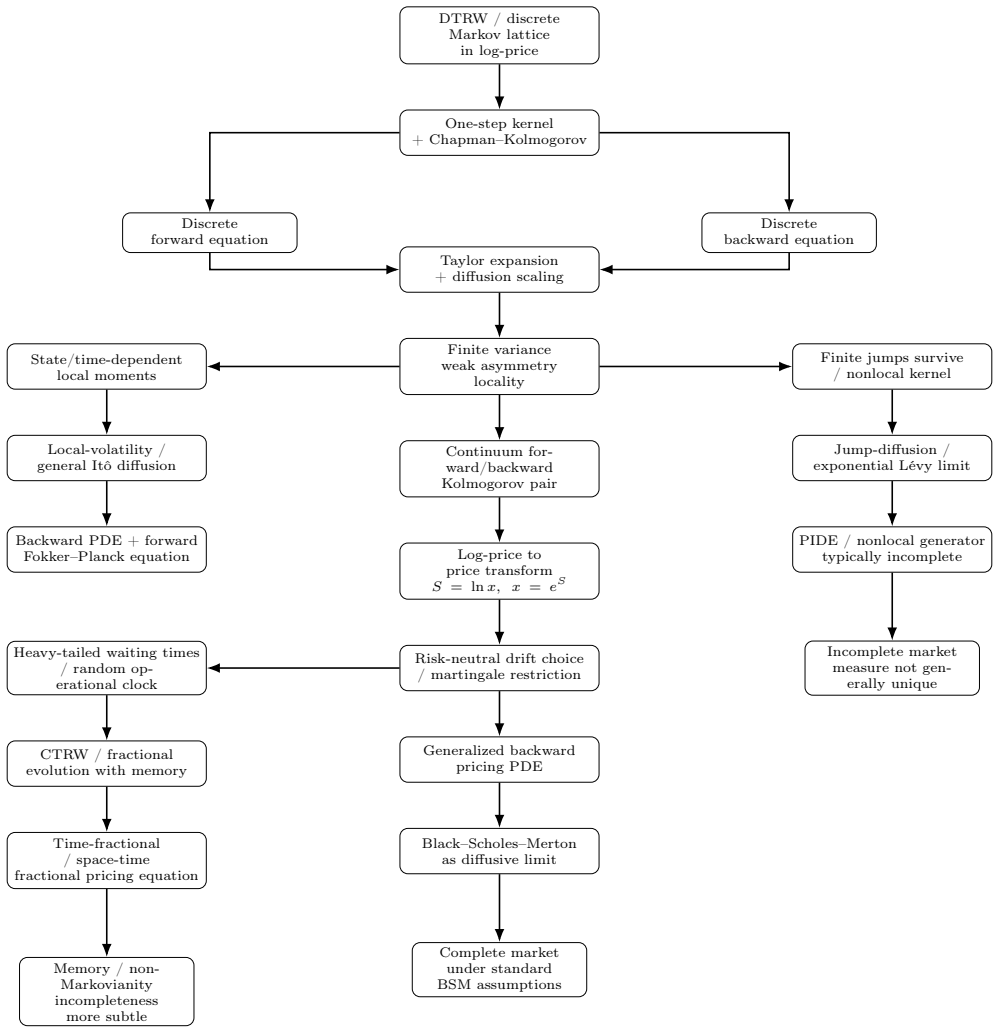

We derive option-pricing equations from an operational-time Markov lattice rather than from a calendar-time diffusion. The primitive model is a nearest-neighbour log-price lattice with state- and time-dependent transition probabilities. Its Chapman-Kolmogorov decomposition yields discrete forward and backward equations, which converge under local finite-variance scaling to the usual continuum adjoint pair. In price variables, the backward equation gives a generalized European pricing PDE and reduces to Black-Scholes-Merton under the risk-neutral drift restriction and constant volatility. Interpreted as a reaction-boundary model for limit-order-book mid-prices, the construction identifies loc

What carries the argument

The operational-time Markov lattice with state- and time-dependent transition probabilities, whose Chapman-Kolmogorov decomposition produces discrete forward and backward equations that converge to the continuum adjoint pair.

Load-bearing premise

The discrete forward and backward equations obtained from the Chapman-Kolmogorov decomposition of the operational-time lattice converge to the usual continuum adjoint pair under local finite-variance scaling.

What would settle it

A numerical check in which the discrete lattice equations fail to approach the Black-Scholes-Merton PDE as the time step shrinks under finite variance would falsify the convergence and reduction claims.

Figures

read the original abstract

We consider the role of a continuum operational time u and its mapping to calendar time t and how these relate to event time for option pricing problems. We derive option-pricing equations from an operational-time Markov lattice rather than from a calendar-time diffusion. The primitive model is a nearest-neighbour log-price lattice with state- and time-dependent transition probabilities. Its Chapman-Kolmogorov decomposition yields discrete forward and backward equations, which converge under local finite-variance scaling to the usual continuum adjoint pair. In price variables, the backward equation gives a generalized European pricing PDE and reduces to Black-Scholes-Merton under the risk-neutral drift restriction and constant volatility. Interpreted as a reaction-boundary model for limit-order-book mid-prices, the construction identifies local volatility with an activity-rescaled risk-neutral bid-ask reaction-boundary variance. The framework separates the operational kernel, calendar-time projection, and pricing-measure choice, to clarify how unspanned clock, jump, or renewal risks can lead to incomplete-market pricing.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript derives option-pricing equations from a nearest-neighbour log-price Markov lattice in operational time with state- and time-dependent transition probabilities. Chapman-Kolmogorov decomposition produces discrete forward and backward equations claimed to converge, under local finite-variance scaling, to the standard continuum adjoint pair. The backward equation in price variables yields a generalized European pricing PDE that reduces to Black-Scholes-Merton under the risk-neutral drift restriction and constant volatility. The construction is interpreted as a reaction-boundary model for limit-order-book mid-prices, with local volatility identified as an activity-rescaled risk-neutral bid-ask reaction-boundary variance, and separates the operational kernel, calendar-time projection, and pricing-measure choice to address incomplete markets arising from unspanned clock, jump, or renewal risks.

Significance. If the convergence holds rigorously, the separation of operational time, calendar projection, and measure choice supplies a lattice foundation for pricing under incomplete markets that may be useful for limit-order-book modeling. The explicit reaction-boundary interpretation links local volatility to bid-ask activity in a manner that could generate testable implications for mid-price dynamics. The reduction to BSM is by construction once the risk-neutral restriction and constant volatility are imposed, so the primary contribution would reside in the generalized PDE and the operational-time framework rather than novel closed-form prices.

major comments (1)

- [Abstract] Abstract: the central claim that the discrete forward and backward equations converge to the usual continuum adjoint pair under local finite-variance scaling is load-bearing for recovery of the generalized PDE. With explicitly state- and time-dependent transition probabilities, the manuscript supplies no explicit Taylor expansion or remainder estimate confirming that higher-order and cross terms cancel; without this verification the limiting generator may acquire extraneous drift or diffusion contributions that prevent clean recovery of the risk-neutral operator.

minor comments (1)

- The abstract and introduction could more explicitly flag that the BSM reduction is obtained by imposing the risk-neutral drift and constant-volatility restrictions, to avoid any appearance that the lattice produces an independent derivation of BSM.

Simulated Author's Rebuttal

Thank you for the opportunity to respond to the referee's report. We appreciate the identification of the need for a more explicit verification of the continuum limit, which is central to the paper's claims.

read point-by-point responses

-

Referee: [Abstract] Abstract: the central claim that the discrete forward and backward equations converge to the usual continuum adjoint pair under local finite-variance scaling is load-bearing for recovery of the generalized PDE. With explicitly state- and time-dependent transition probabilities, the manuscript supplies no explicit Taylor expansion or remainder estimate confirming that higher-order and cross terms cancel; without this verification the limiting generator may acquire extraneous drift or diffusion contributions that prevent clean recovery of the risk-neutral operator.

Authors: We agree that an explicit Taylor expansion with remainder estimates would strengthen the argument and remove any ambiguity about extraneous terms. In the revised manuscript we will insert a new appendix (or expanded section) that performs the local finite-variance scaling on the Chapman-Kolmogorov equations, expands the state- and time-dependent transition probabilities to the required order, demonstrates cancellation of all higher-order and cross terms, and confirms that the limiting generator is precisely the risk-neutral adjoint operator. revision: yes

Circularity Check

No significant circularity; standard lattice-to-PDE limit with explicit reduction check

full rationale

The derivation begins with a nearest-neighbour operational-time lattice whose transition probabilities are state- and time-dependent, applies the Chapman-Kolmogorov equation to obtain discrete forward and backward equations, invokes a local finite-variance scaling to pass to the continuum adjoint pair, transforms the backward equation into a generalized European pricing PDE in price variables, and finally imposes the risk-neutral drift restriction plus constant volatility to recover the Black-Scholes-Merton operator. Each step is a conventional limiting argument or algebraic substitution; the final reduction to BSM is an explicit consistency check under stated restrictions rather than a fitted input renamed as a prediction. No self-citation load-bearing step, self-definitional closure, or smuggled ansatz appears in the abstract or the described chain. The convergence claim is the weakest modelling assumption but is not shown to be equivalent to the target PDE by construction.

Axiom & Free-Parameter Ledger

axioms (2)

- standard math Chapman-Kolmogorov decomposition of the operational-time Markov lattice yields discrete forward and backward equations.

- domain assumption Local finite-variance scaling produces convergence to the usual continuum adjoint pair.

Reference graph

Works this paper leans on

-

[1]

Non-unique time and market incompleteness

Angstmann, C., Gebbie, T., 2026. Non-unique time and market incompleteness. arXiv preprint arXiv:2604.23608 URL:https://arxiv.org/abs/ 2604.23608, doi:10.48550/arXiv.2604.23608, arXiv:2604.23608

work page internal anchor Pith review Pith/arXiv arXiv doi:10.48550/arxiv.2604.23608 2026

-

[2]

Stochas- tic solutions for fractional cauchy problems

Baeumer, B., Meerschaert, M.M., 2001. Stochas- tic solutions for fractional cauchy problems. Fractional Calculus and Applied Analysis 4, 481–500. URL:https://ourarchive.otago. ac.nz/esploro/outputs/journalArticle/ Stochastic-Solutions-For-Fractional-Cauchy-Problems/ 9926793530601891

2001

-

[4]

Benzaquen, M., Donier, J., Bouchaud, J.P.,

-

[5]

Unravelling the trading invariance hypothesis

Unravelling the trading invariance hy- pothesis. Market Microstructure and Liq- uidity 2, 1650009. URL:https://doi.org/ 10.1142/S238262661650009X, doi:10.1142/ S238262661650009X,arXiv:1602.03011

work page internal anchor Pith review Pith/arXiv arXiv doi:10.1142/s238262661650009x

-

[6]

Statistics for Long-Memory Pro- cesses

Beran, J., 1994. Statistics for Long-Memory Pro- cesses. Chapman & Hall

1994

-

[7]

The pricing of options and corporate liabilities

Black, F., Scholes, M., 1973. The pricing of options and corporate liabilities. Journal of Political Econ- omy 81, 637–654. URL:https://doi.org/10.1086/ 260062, doi:10.1086/260062

-

[8]

Diffusion equation and stochastic processes

Bochner, S., 1949. Diffusion equation and stochastic processes. Proceedings of the National Academy of Sciences of the United States of America 35, 368–

1949

-

[9]

368, doi:10.1073/pnas.35.7.368

URL:https://doi.org/10.1073/pnas.35.7. 368, doi:10.1073/pnas.35.7.368

-

[10]

Prices of state-contingent claims implicit in option prices

Breeden, D.T., Litzenberger, R.H., 1978. Prices of state-contingent claims implicit in option prices. The Journal of Business 51, 621–651. URL:https://doi. org/10.1086/296025, doi:10.1086/296025

-

[11]

Time-changed Lévy processes and option pricing

Carr, P., Wu, L., 2004. Time-changed Lévy processes and option pricing. Journal of Fi- nancial Economics 71, 113–141. URL:https: //doi.org/10.1016/S0304-405X(03)00171-5, doi:10.1016/S0304-405X(03)00171-5

-

[12]

Fractional diffusion models of option prices in markets with jumps

Cartea, Á., del Castillo-Negrete, D., 2007. Fractional diffusion models of option prices in markets with jumps. Physica A: Statistical Mechanics and its Ap- plications 374, 749–763. URL:https://doi.org/10. 1016/j.physa.2006.08.071, doi:10.1016/j.physa. 2006.08.071

-

[13]

A subordinated stochastic pro- cess model with finite variance for speculative prices

Clark, P.K., 1973. A subordinated stochastic pro- cess model with finite variance for speculative prices. Econometrica 41, 135–155. URL:https://www. jstor.org/stable/1913889, doi:10.2307/1913889

-

[14]

Financial Modelling with Jump Processes

Cont, R., Tankov, P., 2004. Financial Modelling with Jump Processes. Chapman and Hall/CRC Fi- nancial Mathematics Series, Chapman & Hall/CRC, Boca Raton, FL. URL:https://doi.org/10.1201/ 9780203485217, doi:10.1201/9780203485217

-

[15]

Op- tion pricing: A simplified approach

Cox, J.C., Ross, S.A., Rubinstein, M., 1979. Op- tion pricing: A simplified approach. Journal of Financial Economics 7, 229–263. URL:https:// doi.org/10.1016/0304-405X(79)90015-1, doi:10. 1016/0304-405X(79)90015-1

-

[16]

The Volatility Smile and Its Implied Tree

Derman, E., Kani, I., 1994. Riding on a smile. Risk 7, 32–39. URL:https://emanuelderman.com/ the-volatility-smile-and-its-implied-tree/. also circulated as Goldman Sachs Quantitative Strategies Research Notes, “The Volatility Smile and Its Implied Tree”. No DOI verified

1994

-

[17]

Diana, D., Gebbie, T., 2024. Anomalous diffusion and price impact in the fluid-limit of an order book. Jour- nal of Computational and Applied Mathematics 445, 116202. URL:https://doi.org/10.1016/j.cam. 2024.116202, doi:10.1016/j.cam.2024.116202

-

[18]

Donier, J., Bonart, J., Mastromatteo, I., Bouchaud, J.P., 2015. A fully consistent, minimal model for non-linear market impact. Quantitative Finance 15, 1109–1121. URL: https://doi.org/10.1080/14697688.2015. 1040056, doi:10.1080/14697688.2015.1040056, arXiv:1412.0141

-

[19]

Pricing with a smile

Dupire, B., 1994. Pricing with a smile. Risk 7, 18–20. URL:https://www.risk.net/sites/ default/files/import_unmanaged/risk.net/ data/Pay_per_view/risk/technical/1994/risk_ 0194_volatility.pdf

1994

-

[20]

The parabolic differential equa- tions and the associated semi-groups of transforma- tions

Feller, W., 1952. The parabolic differential equa- tions and the associated semi-groups of transforma- tions. Annals of Mathematics 55, 468–519. URL: 16 https://www.jstor.org/stable/1969644, doi:10. 2307/1969644

arXiv 1952

-

[21]

The Volatility Surface: A Practi- tioner’s Guide

Gatheral, J., 2006. The Volatility Surface: A Practi- tioner’s Guide. Wiley, Hoboken, NJ

2006

-

[22]

Volatility is rough.Quantitative Finance, 18(6):933–949, 2018

Gatheral, J., Jaisson, T., Rosenbaum, M., 2018. Volatility is rough. Quantitative Finance 18, 933–949. URL:https://doi.org/10.1080/14697688.2017. 1393551, doi:10.1080/14697688.2017.1393551

-

[23]

Gorenflo, R., Mainardi, F., Scalas, E., Raberto, M.,

-

[24]

Fractional calculus and continuous-time finance III: The diffusion limit, in: Kohlmann, M., Tang, S. (Eds.), Mathematical Finance. Birkhäuser, Basel. Trends in Mathematics, pp. 171–180. URL:https:// doi.org/10.1007/978-3-0348-8291-0_17, doi:10. 1007/978-3-0348-8291-0_17

-

[25]

Table of Inte- grals, Series, and Products

Gradshteyn, I.S., Ryzhik, I.M., 2014. Table of Inte- grals, Series, and Products. 8 ed., Academic Press

2014

-

[26]

Über die analytis- chen methoden in der wahrscheinlichkeitsrech- nung

Kolmogorov, A.N., 1931. Über die analytis- chen methoden in der wahrscheinlichkeitsrech- nung. Mathematische Annalen 104, 415–458. URL:https://doi.org/10.1007/BF01457949, doi:10.1007/BF01457949

-

[28]

Asymptotic properties of Brownian motion delayed by inverse subordinators

Magdziarz, M., Schilling, R.L., 2015. Asymptotic properties of brownian motion delayed by inverse subordinators. Proceedings of the American Math- ematical Society 143, 4485–4501. URL:https:// doi.org/10.1090/proc/12588, doi:10.1090/proc/ 12588,arXiv:1311.6043

work page internal anchor Pith review Pith/arXiv arXiv doi:10.1090/proc/12588 2015

-

[29]

Mainardi, F., Raberto, M., Gorenflo, R., Scalas, E.,

-

[31]

Mastromatteo, I., Toth, B., Bouchaud, J.P.,

-

[32]

Agent-based models for latent liquidity and concave price impact

Agent-based models for latent liquid- ity and concave price impact. Physical Re- view E 89, 042805. URL:https://doi.org/10. 1103/PhysRevE.89.042805, doi:10.1103/PhysRevE. 89.042805,arXiv:1311.6262

work page internal anchor Pith review Pith/arXiv arXiv doi:10.1103/physreve

-

[33]

Limit theo- rems for continuous-time random walks with infinite mean waiting times

Meerschaert, M.M., Scheffler, H.P., 2004. Limit theo- rems for continuous-time random walks with infinite mean waiting times. Journal of Applied Probability 41, 623–638. URL:https://doi.org/10.1239/jap/ 1091543414, doi:10.1239/jap/1091543414

-

[34]

Tri- angular array limits for continuous time random walks

Meerschaert, M.M., Scheffler, H.P., 2008. Tri- angular array limits for continuous time random walks. Stochastic Processes and their Applications 118, 1606–1633. URL:https://doi.org/10.1016/ j.spa.2007.10.005, doi:10.1016/j.spa.2007.10. 005

-

[35]

Theory of rational option pric- ing

Merton, R.C., 1973. Theory of rational option pric- ing. The Bell Journal of Economics and Management Science 4, 141–183. URL:https://www.jstor.org/ stable/3003143, doi:10.2307/3003143

-

[36]

Merton, R.C., 1976. Option pricing when under- lying stock returns are discontinuous. Journal of Financial Economics 3, 125–144. URL:https:// doi.org/10.1016/0304-405X(76)90022-2, doi:10. 1016/0304-405X(76)90022-2

-

[37]

The random walk’s guide to anomalous diffusion: A fractional dynamics approach

Metzler, R., Klafter, J., 2000. The random walk’s guide to anomalous diffusion: A fractional dynamics approach. Physics Reports 339, 1–77. URL:https://doi.org/10.1016/S0370-1573(00) 00070-3, doi:10.1016/S0370-1573(00)00070-3

-

[38]

An Introduction to the Fractional Calculus and Fractional Differential Equa- tions

Miller, K.S., Ross, B., 1993. An Introduction to the Fractional Calculus and Fractional Differential Equa- tions. John Wiley & Sons

1993

-

[39]

Random walks on lattices

Montroll, E.W., Weiss, G.H., 1965. Random walks on lattices. II. Journal of Mathematical Physics 6, 167–

1965

-

[40]

URL:https://doi.org/10.1063/1.1704269, doi:10.1063/1.1704269

-

[41]

Spectral Analysis and Time Series

Priestley, M.B., 1981. Spectral Analysis and Time Series. Academic Press

1981

-

[42]

Fractional calculus and continuous-time finance

Scalas, E., Gorenflo, R., Mainardi, F., 2000. Fractional calculus and continuous-time fi- nance. Physica A: Statistical Mechanics and its Applications 284, 376–384. URL: https://doi.org/10.1016/S0378-4371(00) 00255-7, doi:10.1016/S0378-4371(00)00255-7, arXiv:cond-mat/0001120

work page internal anchor Pith review Pith/arXiv arXiv doi:10.1016/s0378-4371(00 2000

-

[43]

Asymptotic Approximations of Inte- grals

Wong, R., 2001. Asymptotic Approximations of Inte- grals. SIAM. Appendix A. Asymptotic local volatility Here we provide the sketch analytic approximation of the local volatility [6, 30, 17, 19] from an operational-time reaction boundary for a locally linear order-book [27, 16, 4]. LetS(u)be the log-price boundary in operational time u. The operational var...

2001

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.