Pivotal and identification-robust nonparametric inference in linear IV models

Pith reviewed 2026-06-27 07:42 UTC · model grok-4.3

The pith

A modified test statistic for linear IV models is asymptotically pivotal under weak identification and unknown heteroskedasticity.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

By modifying an existing test statistic to directly account for heteroskedasticity of unknown form, the resulting statistic becomes asymptotically pivotal, which enables straightforward inference on parameters of endogenous variables, subvector inference without knowledge of identification strength, and a pure specification test in linear IV models that are nonparametric in the first stage.

What carries the argument

The modified test statistic that directly accounts for heteroskedasticity of unknown form and becomes asymptotically pivotal for the parameters of interest.

If this is right

- Inference on parameters of endogenous explanatory variables can use standard asymptotic critical values without further adjustment.

- Subvector inference remains valid without requiring knowledge of identification strength for the remaining parameters.

- A pure specification test can be performed that stays conservative under weak identification.

- The procedures remain computationally straightforward and can be applied with nonparametric first-stage estimation.

Where Pith is reading between the lines

- These pivotal statistics might be adapted to other semiparametric IV settings where heteroskedasticity interacts with identification.

- Applied researchers could apply the methods to recheck conclusions in areas prone to weak instruments, such as demand estimation or policy evaluation.

- Extensions could examine whether similar modifications improve robustness in panel or time-series IV contexts.

Load-bearing premise

The linear IV model must be correctly specified with valid instruments and the nonparametric first-stage estimator must satisfy the regularity conditions needed for asymptotic pivotality.

What would settle it

A correctly specified data-generating process with heteroskedasticity and weak instruments in which the new statistic's finite-sample rejection rate under the null deviates substantially from the nominal level would falsify the asymptotic pivotality claim.

Figures

read the original abstract

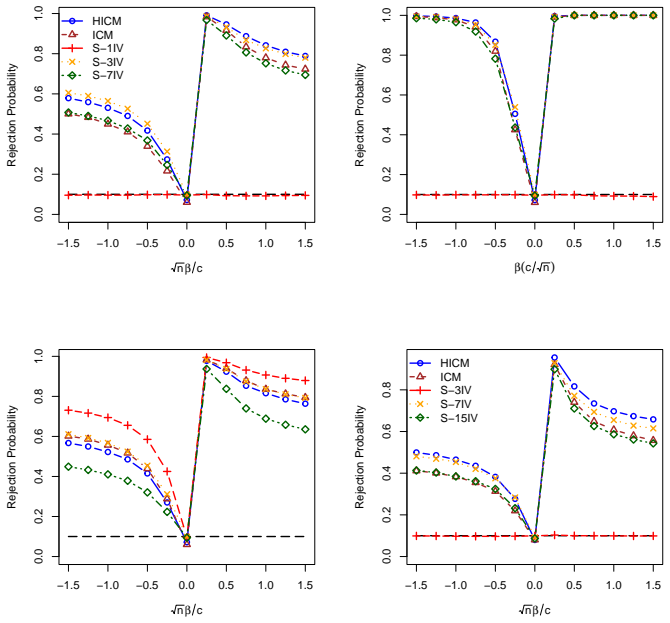

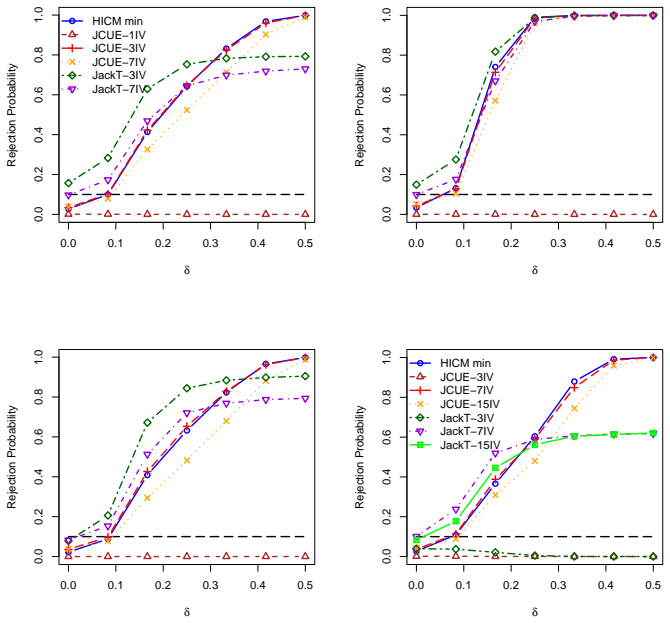

We develop new inference procedures for a linear IV model that are robust to identification strength and heteroskedasticity of unknown form, and nonparametric with respect to the first-stage equation. Our first test is tailored for inference on parameters of endogenous explanatory variables. Our new statistic modifies that of Antoine and Lavergne (2003) to directly account for heteroskedasticity of unknown form. As a result, it is asymptotically pivotal, so that inference is greatly facilitated in practice. We also develop (i) an identification-robust subvector inference procedure that does not rely on the knowledge of identification strength for the remaining parameters, and (ii) a pure specification test. In both cases, the tests are conservative but powerful. We show that our procedures are computationally friendly and competitive with existing ones in simulations and an application.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript develops inference procedures for linear IV models that are robust to identification strength and heteroskedasticity of unknown form, while treating the first-stage equation nonparametrically. The core contribution modifies the Antoine and Lavergne (2003) statistic to incorporate heteroskedasticity directly, yielding an asymptotically pivotal test for parameters on endogenous regressors. Additional procedures include an identification-robust subvector test (conservative but powerful, without requiring knowledge of identification strength for other parameters) and a pure specification test. The methods are claimed to be computationally friendly and to perform competitively in simulations and an empirical application.

Significance. If the asymptotic pivotality and robustness results hold under the stated regularity conditions, the work supplies practical tools for IV inference that avoid nuisance-parameter estimation and remain valid under weak identification. The nonparametric first-stage broadens applicability beyond parametric assumptions. Credit is due for emphasizing computational feasibility alongside simulation and application evidence.

minor comments (3)

- [Abstract] Abstract: the statement that the modified statistic 'is asymptotically pivotal, so that inference is greatly facilitated in practice' would benefit from a brief parenthetical reference to the specific limiting distribution (e.g., standard normal or chi-squared) to make the practical advantage immediately clear.

- The regularity conditions on the nonparametric first-stage estimator are invoked for both strong and weak identification; a short table or paragraph summarizing the key rate and smoothness requirements would aid readers who wish to verify applicability to their data.

- The subvector and specification-test procedures are described as conservative; explicit finite-sample or local-power comparisons with existing conservative methods (e.g., Anderson-Rubin or Kleibergen) would strengthen the claim of competitiveness.

Simulated Author's Rebuttal

We thank the referee for the constructive and positive report, which recognizes the paper's contributions to asymptotically pivotal and identification-robust inference in linear IV models under nonparametric first-stage and unknown heteroskedasticity. We appreciate the recommendation for minor revision and will incorporate any editorial suggestions in the revised version.

Circularity Check

Minor self-citation to 2003 base statistic; central heteroskedasticity modification is independent

full rationale

The paper modifies the Antoine-Lavergne (2003) statistic to incorporate unknown heteroskedasticity, yielding an asymptotically pivotal test under stated regularity conditions. This modification is presented as a new derivation rather than a direct reuse or fit of prior results. The 2003 citation serves as the starting point for extension but is not load-bearing for the pivotal property itself, which follows from the new accounting for heteroskedasticity. No self-definitional loops, fitted inputs renamed as predictions, or uniqueness theorems imported from the authors' own prior work appear in the abstract or claimed chain. The derivation remains self-contained against external benchmarks once the nonparametric first-stage regularity conditions are granted.

Axiom & Free-Parameter Ledger

axioms (2)

- standard math Standard regularity conditions for asymptotic theory in nonparametric estimation and weak identification

- domain assumption Linear IV model is correctly specified with valid instruments

Reference graph

Works this paper leans on

-

[1]

Andrews, Donald W. K. and Moreira, Marcelo J. and Stock, James H. , journal =. Optimal Two-Sided Invariant Similar Tests for Instrumental Variables Regression , year =. doi:10.1111/j.1468-0262.2006.00680.x , keywords =

-

[2]

Anderson, T. W. and Rubin, Herman , journal =. The Asymptotic Properties of Estimates of the Parameters of a Single Equation in a Complete System of Stochastic Equations , year =

-

[3]

Conditional Inference With a Functional Nuisance Parameter , year =

Andrews, Isaiah and Mikusheva, Anna , journal =. Conditional Inference With a Functional Nuisance Parameter , year =. doi:10.3982/ECTA12868 , file =

-

[4]

A Geometric Approach to Nonlinear Econometric Models , year =

Andrews, Isaiah and Mikusheva, Anna , journal =. A Geometric Approach to Nonlinear Econometric Models , year =. doi:10.3982/ECTA12030 , file =

-

[5]

Andrews, Donald W. K. and Guggenberger, Patrik , journal =. Identification and Singularity-Robust Inference for Moment Condition Models , year =. doi:10.3982/QE1219 , file =

-

[6]

Andrews, Donald W. K. , journal =. Nonparametric Kernel Estimation for Semiparametric Models , year =. doi:10.1017/S0266466600009427 , file =

-

[7]

Andrews, Donald W. K. and Marmer, Vadim and Yu, Zhengfei , journal =. On Optimal Inference in the Linear IV Model , year =. doi:10.3982/QE1082 , file =

-

[8]

Andrews, Donald W. K. and Cheng, Xu , journal =. Estimation and Inference With Weak, Semi-Strong, and Strong Identification , year =. doi:10.3982/ECTA9456 , keywords =

-

[9]

Conditional Linear Combination Tests for Weakly Identified Models , year =

Andrews, Isaiah , journal =. Conditional Linear Combination Tests for Weakly Identified Models , year =. doi:10.3982/ECTA12407 , keywords =

-

[10]

Andrews, Donald W. K. , booktitle =. Empirical Process Methods in Econometrics , year =. doi:10.1016/S1573-4412(05)80006-6 , issn =

-

[11]

Antoine and P

B. Antoine and P. Lavergne , journal =. Conditional Moment Models under Semi-Strong Identification , year =

-

[12]

Anderson, T. W. and Rubin, Herman , journal =. Estimation of the Parameters of a Single Equation in a Complete System of Stochastic Equations , year =

-

[13]

D. W. K. Andrews and J. H. Stock , booktitle =. Inference with Weak Instruments , year =

-

[14]

Bierens , journal =

H.J. Bierens , journal =. Consistent Model Specification Tests , year =

-

[15]

Bierens , journal =

Herman J. Bierens , journal =. A Consistent Conditional Moment Test of Functional Form , year =

-

[16]

Bierens and Werner Ploberger , journal =

Herman J. Bierens and Werner Ploberger , journal =. Asymptotic Theory of Integrated Conditional Moment Tests , year =

-

[17]

Burbage and Lonnie Magee and A

John B. Burbage and Lonnie Magee and A. Leslie Robb , journal =. Alternative Transformations to Handle Extreme Values of the Dependent Variable , year =

-

[18]

Cattaneo, Matias D. and Farrell, Max H. , journal =. Optimal Convergence Rates, Bahadur Representation, and Asymptotic Normality of Partitioning Estimators , year =. doi:10.1016/j.jeconom.2013.02.002 , file =

-

[19]

The Reduced Form: A Simple Approach to Inference with Weak Instruments , year =

Victor Chernozhukov and Christian Hansen , journal =. The Reduced Form: A Simple Approach to Inference with Weak Instruments , year =. doi:10.1016/j.econlet.2007.11.012 , keywords =

-

[20]

Admissible Invariant Similar Tests for Instrumental Variables Regression , year =

Chernozhukov, Victor and Hansen, Christian and Jansson, Michael , journal =. Admissible Invariant Similar Tests for Instrumental Variables Regression , year =. doi:10.1017/S0266466608090312 , file =

-

[21]

de Wet, T. and Venter, J. H. , journal =. Asymptotic Distributions for Quadratic Forms with Applications to Tests of Fit , year =. doi:10.1214/aos/1176342378 , fjournal =

-

[22]

Dieterle, Steven G. and Snell, Andy , journal =. A Simple Diagnostic to Investigate Instrument Validity and Heterogeneous Effects When Using a Single Instrument , year =. doi:10.1016/j.labeco.2016.08. , fjournal =

-

[23]

I. Dreier and S. Kotz , journal =. A Note on the Characteristic Function of the T-Distribution , year =. doi:10.1016/S0167-7152(02)00032-9 , fjournal =

-

[24]

Dufour , journal =

J.-M. Dufour , journal =. Identification, Weak Instruments, and Statistical Inference in Econometrics , year =

-

[25]

Dufour, Jean-Marie and Taamouti, Mohamed , journal =. Further Results on Projection-Based Inference in IV Regressions with Weak, Collinear or Missing Instruments , year =. doi:10.1016/j.jeconom.2006.06.008 , file =

-

[26]

Dufour, Jean-Marie and Taamouti, Mohamed , journal =. Projection-. 2005 , issn =. doi:10.1111/j.1468-0262.2005.00618.x , file =

-

[27]

Dufour , journal =

J.-M. Dufour , journal =. Some Impossibility Theorems in Econometrics with Applications to Structural and Dynamic Models. , year =

-

[28]

Han and P.C.B

C. Han and P.C.B. Phillips , journal =. GMM with Many Moment Conditions , year =

-

[29]

Hausman, Jerry A. and Newey, Whitney K. and Woutersen, Tiemen and Chao, John C. and Swanson, Norman R. , journal =. Instrumental Variable Estimation with Heteroskedasticity and Many Instruments , year =. doi:10.3982/QE89 , file =

-

[30]

Hahn and J

J. Hahn and J. Hausman , journal =. Weak Instruments: Diagnosis and Cures in Empirical Economics , year =

-

[31]

Hansen and J.A

C. Hansen and J.A. Hausman and W.K. Newey , journal =. Estimation With Many Instrumental Variables , year =

-

[32]

and Kotz, S

Johnson, N.L. and Kotz, S. and Balakrishnan, N. , publisher =. Continuous Univariate Distributions , year =

-

[33]

Jun, S. J. and Pinkse, J. , journal =. Testing Under Weak Identification with Conditional Moment Restrictions , year =. doi:10.1017/s0266466612000138 , fjournal =

-

[34]

Uniformity and the Delta Method , year =

Kasy, Maximilian , journal =. Uniformity and the Delta Method , year =. doi:10.1515/jem-2018-0001 , file =

-

[35]

Kleibergen , journal =

F. Kleibergen , journal =. Testing Parameters in. 2005 , pages =

2005

-

[36]

Kleibergen, Frank , journal =. Generalizing Weak Instrument Robust IV Statistics Towards Multiple Parameters, Unrestricted Covariance Matrices and Identification Statistics , year =. doi:10.1016/j.jeconom.2006.06.010 , file =

-

[37]

Pivotal Statistics for Testing Structural Parameters in Instrumental Variables Regression , year =

Kleibergen, Frank , journal =. Pivotal Statistics for Testing Structural Parameters in Instrumental Variables Regression , year =. doi:10.1111/1468-0262.00353/full , file =

-

[38]

2008 , Series =

Introduction to Empirical Processes and Semiparametric Inference , Author =. 2008 , Series =

2008

-

[39]

and Romano, J.P

Lehmann, E.L. and Romano, J.P. , publisher =. Testing Statistical Hypotheses , year =

-

[40]

Lavergne, Pascal and Patilea, Valentin , journal =. Smooth Minimum Distance Estimation and Testing with Conditional Estimating Equations: Uniform in Bandwidth Theory , year =. doi:10.1016/j.jeconom.2013.05.006 , type =

-

[41]

and Alix-Garcia, Jennifer , journal =

Sellars, Emily A. and Alix-Garcia, Jennifer , journal =. Labor scarcity, land tenure, and historical legacy: Evidence from Mexico , year =. doi:10.1016/j.jdeveco.2018.07.014 , file =

-

[42]

Robust Confidence Sets in the Presence of Weak Instruments , year =

Anna Mikusheva , journal =. Robust Confidence Sets in the Presence of Weak Instruments , year =. doi:10.1016/j.jeconom.2009.12.003 , keywords =

-

[43]

M. J. Moreira , journal =. A Conditional Likelihood Ratio Test for Structural Models , year =

-

[44]

Moreira, Humberto and Moreira, Marcelo J. , journal =. Optimal Two-Sided Tests for Instrumental Variables Regression with Heteroskedastic and Autocorrelated Errors , year =. doi:10.1016/j.jeconom.2019.04.038 , keywords =

-

[45]

Working paper, FPG , title =. 2017 , month = apr, adsnote =. arXiv , doi =:1705.00231 , keywords =

arXiv 2017

-

[46]

Nonparametric Covariance Model , year =

Jianxin Yin and Zhi Geng and Runze Li and Hansheng Wang , journal =. Nonparametric Covariance Model , year =

-

[47]

W.K. Newey and F. Windmeijer , journal =. Generalized Method of Moments With Many Weak Moment Conditions , year =. doi:10.3982/ECTA6224 , file =

-

[48]

Rice, John , journal =. Bandwidth Choice for Nonparametric Regression , year =. doi:10.1214/aos/1176346788 , fjournal =

-

[49]

Adaptive nonparametric confidence sets , volume =

Robins, James and van der Vaart, Aad , journal =. Adaptive Nonparametric Confidence Sets , year =. doi:10.1214/009053605000000877 , file =

-

[50]

Limit Theorems for Polylinear Forms , year =

V.I Rotar' , journal =. Limit Theorems for Polylinear Forms , year =. doi:10.1016/0047-259X(79)90055-1 , keywords =

-

[51]

Nonparametric Estimation of Residual Variance Revisited , year =

Burkhardt Seifert and Theo Gasser and Andreas Wolf , journal =. Nonparametric Estimation of Residual Variance Revisited , year =

-

[52]

Staiger and J

D. Staiger and J. H. Stock , journal =. Instrumental Variables Regression with Weak Instruments , year =

-

[53]

and White, Halbert , journal =

Stinchcombe, Maxwell B. and White, Halbert , journal =. Consistent Specification Testing With Nuisance Parameters Present Only Under the Alternative , year =

-

[54]

J. H. Stock and J. H. Wright , journal =. 2000 , pages =

2000

-

[55]

J. H. Stock and J. H. Wright and M. Yogo , journal =. A Survey of Weak Instruments and Weak Identification in Generalized Method of Moments , year =

-

[56]

van der Vaart, A. W. and Wellner, Jon A , publisher =. Weak Convergence and Empirical Processes: with Applications to Statistics , year =

-

[57]

Bracketing Smooth Functions , year =

van der Vaart, Aad , journal =. Bracketing Smooth Functions , year =

-

[58]

2017 , author =

Generalized Additive Models: An Introduction with R , publisher =. 2017 , author =

2017

-

[59]

Escanciano, Juan Carlos , journal =. A simple and robust estimator for linear regression models with strictly exogenous instruments , year =. doi:10.1111/ectj.12087 , file =

-

[60]

Dominguez, Manuel A. and Lobato, Ignacio N. , journal =. Consistent Estimation of Models Defined by Conditional Moment Restrictions , year =. doi:10.1111/j.1468-0262.2004.00545.x , file =

-

[61]

2021 , month = jan, abstract =

Chen, Xiaohong and Lee, Sokbae and Seo, Myung Hwan , title =. 2021 , month = jan, abstract =. arxiv , doi =:2008.11140 , file =

arXiv 2021

-

[62]

Economet

Montiel Olea, Jos. Economet. Theor. , title =. 2020 , pages =

2020

-

[63]

Mathematical Statistics , year =

Jun Shao , publisher =. Mathematical Statistics , year =

-

[64]

Identification-robust nonparametric inference in a linear

Antoine, Bertille and Lavergne, Pascal , journal =. Identification-robust nonparametric inference in a linear. 2023 , issn =. doi:10.1016/j.jeconom.2022.01.011 , file =

-

[65]

On the instrument functional form with a binary endogenous explanatory variable , year =

Xu, Ruonan , journal =. On the instrument functional form with a binary endogenous explanatory variable , year =. doi:10.1016/j.econlet.2021.109993 , file =

-

[66]

Jiang, Feiyu and Tsyawo, Emmanuel Selorm , journal =. A Consistent. 2024 , abstract =. arxiv , doi =:2208.13370 , file =

arXiv 2024

-

[67]

Feasible IV regression without excluded instruments , year =

Tsyawo, Emmanuel Selorm , journal =. Feasible IV regression without excluded instruments , year =. doi:10.1093/ectj/utac032 , file =

-

[68]

Instrumental variable estimation with first-stage heterogeneity , year =

Abadie, Alberto and Gu, Jiaying and Shen, Shu , journal =. Instrumental variable estimation with first-stage heterogeneity , year =. doi:10.1016/j.jeconom.2023.02.005 , file =

-

[69]

J. D. Angrist and G. W. Imbens and A. B. Krueger , journal =. Jackknife instrumental variables estimation , year =

-

[70]

Guggenberger and F

P. Guggenberger and F. Kleibergen and S. Mavroeidis , journal =. A more powerful subvector Anderson-Rubin test in linear variables regression , year =

-

[71]

Tanaka and C

T. Tanaka and C. Camerer and Q. Ngyuen , journal =. Risk and Time Preferences: Linking Experimental and Household Survey Data from Vietnam , year =

-

[72]

Antoine and D

B. Antoine and D. Frazier and E. Renault , journal =. Coordinated Testing for Identification Failure and Correct Model Specification , year =

-

[73]

Kleibergen and Z

F. Kleibergen and Z. Zhan , journal =. Double robust inference for continuous updating. 2025 , pages =

2025

-

[74]

Chen, Xiaohong and Lee, Sokbae and Seo, Myung Hwan and Song, Myunghyun , journal =. Inference for Parameters Identified by Conditional Moment Restrictions Using a Generalized Bierens Maximum Statistic , year =. doi:10.1162/rest_a_01550 , fjournal =

-

[75]

Inference with Many Weak Instruments , year =

Mikusheva, Anna and Sun, Liyang , journal =. Inference with Many Weak Instruments , year =. doi:10.1093/restud/rdab097 , file =

-

[76]

Chao, John C. and Hausman, Jerry A. and Newey, Whitney K. and Swanson, Norman R. and Woutersen, Tiemen , journal =. Testing overidentifying restrictions with many instruments and heteroskedasticity , year =. doi:10.1016/j.jeconom.2013.08.003 , file =

-

[77]

Andrews, Isaiah and Stock, James H. and Sun, Liyang , journal =. Weak. 2019 , number =. doi:10.1146/annurev-economics-080218-025643 , file =

-

[78]

A uniformly valid test for instrument exogeneity , year =

Dovonon, Prosper and Gospodinov, Nikolay , journal =. A uniformly valid test for instrument exogeneity , year =. doi:10.1016/j.jeconom.2026.106231 , file =

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.