Equilibrium singular dividend control under ambiguity aggregation of heterogeneous discount rates

Pith reviewed 2026-06-25 21:07 UTC · model grok-4.3

The pith

Time-homogeneous equilibrium dividend laws exist and are unique under linear and exponential aggregation of heterogeneous discount rates, but do not exist under power or logarithmic aggregation.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Under linear and exponential ambiguity aggregation functions a unique barrier-type time-homogeneous equilibrium dividend law exists for the singular control problem; under power-type and logarithmic aggregation functions no such equilibrium law exists. The verification theorem and necessary conditions characterize candidate equilibria, and the linear case yields convergence of bounded-rate equilibria to the singular barrier as the bound tends to infinity.

What carries the argument

The time-homogeneous equilibrium dividend law, defined by a partition of the state space into waiting and dividend-paying regions, which resolves the time inconsistency created by the aggregation function phi.

If this is right

- The verification theorem confirms optimality of candidate equilibrium laws.

- Necessary conditions restrict the form of any equilibrium law.

- Bounded-rate equilibria converge to the singular barrier equilibrium under linear aggregation as the bound tends to infinity.

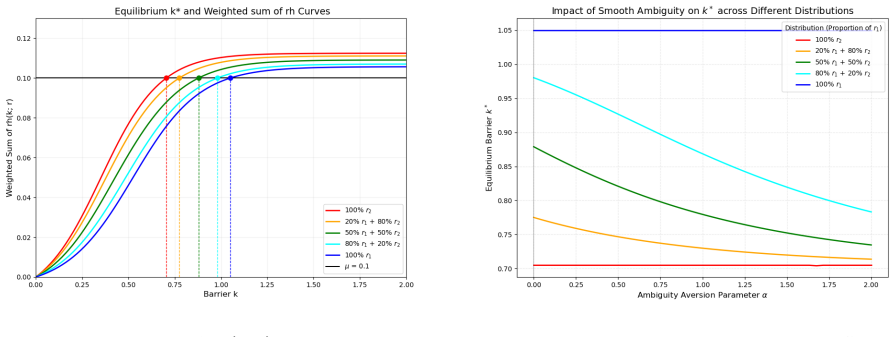

- Numerical examples quantify how discount-rate heterogeneity and ambiguity aversion shift the equilibrium barrier.

Where Pith is reading between the lines

- The existence result is tightly tied to the functional form of the aggregator, so other common aggregators may require different equilibrium concepts.

- Non-existence for power and log aggregators indicates that time inconsistency cannot always be resolved by time-homogeneous barriers.

- The convergence result suggests that bounded-rate models can serve as approximations to the singular case under linear aggregation.

Load-bearing premise

That a time-homogeneous equilibrium dividend law exists and can be characterized by a partition of the state space into waiting and dividend-paying regions.

What would settle it

A concrete calculation showing either that a barrier equilibrium exists for some power-type aggregation function or that no equilibrium exists for linear aggregation.

Figures

read the original abstract

This paper studies a singular dividend control problem for a firm with heterogeneous shareholders whose discount rates follow a given distribution. The central planner aggregates expected discounted payoffs using an ambiguity aggregation function $phi$, which captures shareholder heterogeneity and ambiguity attitudes but also leads to time inconsistency. To address this issue, we seek a time-homogeneous equilibrium dividend law characterized by a partition of the state space into waiting and dividend-paying regions. We provide a rigorous mathematical characterization by proving a verification theorem and deriving necessary conditions for the equilibrium law. We then analyze barrier-type equilibria, showing non-existence for a class of aggregation functions that includes power-type and logarithmic aggregation functions, and establishing existence and uniqueness under linear and exponential aggregation. In the linear case, the bounded-rate equilibrium is shown to converge to the singular barrier-type equilibrium as the dividend rate bound tends to infinity. Numerical examples illustrate the effects of discount-rate heterogeneity and ambiguity aversion on the equilibrium barrier.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper studies a singular dividend control problem where a firm’s shareholders have heterogeneous discount rates drawn from a given distribution. These are aggregated via an ambiguity function ϕ that induces time inconsistency. The authors seek time-homogeneous equilibrium dividend policies characterized by a partition of the state space into waiting and dividend-paying regions. They prove a verification theorem, derive necessary conditions for the equilibrium law, establish non-existence of barrier-type equilibria for power-type and logarithmic aggregators, and prove existence and uniqueness for linear and exponential aggregators. In the linear case they show convergence of bounded-rate equilibria to the singular barrier equilibrium as the rate bound tends to infinity, and they provide numerical illustrations.

Significance. If the verification theorem and the existence/non-existence results hold, the work supplies a rigorous stochastic-control framework for time-inconsistent singular control arising from heterogeneous discounting and ambiguity aggregation. This is a non-trivial extension of classical dividend problems and could serve as a template for other time-inconsistent control problems with heterogeneous agents.

major comments (2)

- [Introduction / Model formulation] The central modeling step—that a time-homogeneous equilibrium exists and takes the form of a simple partition of the state space into waiting and paying regions—is invoked to resolve the time inconsistency generated by ϕ. This assumption is load-bearing for all subsequent results (verification theorem, necessary conditions, barrier analysis) yet receives only heuristic justification in the abstract; a precise statement of the equilibrium concept and a proof that the partition form is without loss of generality are required.

- [Barrier-type equilibria section] The non-existence claim for power-type and logarithmic aggregation functions is stated as a theorem. Because the proof is not reproduced in the provided material, it is impossible to verify whether the argument relies only on the model primitives or inadvertently uses properties that are special to the barrier ansatz.

minor comments (2)

- [Abstract] Notation for the aggregation function ϕ and the distribution of discount rates should be introduced once and used consistently; several passages in the abstract repeat the same definitions.

- [Numerical section] The numerical examples are said to “illustrate the effects,” but no description of the discretization scheme, convergence checks, or parameter values is supplied in the abstract; these details belong in the main text or an appendix.

Simulated Author's Rebuttal

We thank the referee for the careful reading and constructive feedback. We address the major comments point by point below.

read point-by-point responses

-

Referee: [Introduction / Model formulation] The central modeling step—that a time-homogeneous equilibrium exists and takes the form of a simple partition of the state space into waiting and paying regions—is invoked to resolve the time inconsistency generated by ϕ. This assumption is load-bearing for all subsequent results (verification theorem, necessary conditions, barrier analysis) yet receives only heuristic justification in the abstract; a precise statement of the equilibrium concept and a proof that the partition form is without loss of generality are required.

Authors: We agree that a precise formal statement of the equilibrium concept and a justification for the partition form are essential. The manuscript introduces the equilibrium notion in Section 2, but the presentation in the introduction is indeed somewhat informal. In the revision we will add an explicit definition of the time-homogeneous equilibrium (including the precise notion of best response) and supply a short argument showing that, for time-homogeneous Markovian strategies, any equilibrium must induce a partition of the state space into waiting and paying regions; this follows directly from the Markov property and the continuity of the value function. revision: yes

-

Referee: [Barrier-type equilibria section] The non-existence claim for power-type and logarithmic aggregation functions is stated as a theorem. Because the proof is not reproduced in the provided material, it is impossible to verify whether the argument relies only on the model primitives or inadvertently uses properties that are special to the barrier ansatz.

Authors: The complete proof of the non-existence result (Theorem 4.1) appears in full in Section 4 of the manuscript. It proceeds by substituting the candidate barrier strategy into the necessary conditions derived in Proposition 3.2 and obtaining a contradiction that depends only on the functional form of ϕ (power or logarithmic) and the standard assumptions on the cash-reserve dynamics; no extra properties of the barrier ansatz are invoked beyond those already stated in the general equilibrium definition. revision: no

Circularity Check

No significant circularity; derivation self-contained

full rationale

The paper proves a verification theorem and derives necessary conditions for the time-homogeneous equilibrium dividend law from the model primitives (ambiguity aggregation function phi and heterogeneous discount rates). It then establishes explicit non-existence for power/logarithmic aggregators and existence/uniqueness for linear/exponential cases, plus a convergence result in the linear case. These steps rely on standard stochastic control arguments applied to the stated setup rather than reducing any prediction or central claim to a fitted input, self-definition, or load-bearing self-citation chain. The partition assumption for the state space is invoked to resolve time inconsistency but does not create a definitional loop in the reported results.

Axiom & Free-Parameter Ledger

free parameters (2)

- distribution of discount rates

- aggregation function phi

axioms (1)

- domain assumption A time-homogeneous equilibrium dividend law exists and is characterized by a partition of the state space into waiting and dividend-paying regions.

invented entities (1)

-

ambiguity aggregation function phi

no independent evidence

Reference graph

Works this paper leans on

-

[1]

SIAM Journal on Control and Optimization , volume=

Equilibria for time-inconsistent singular control problems , author=. SIAM Journal on Control and Optimization , volume=. 2024 , publisher=

2024

-

[2]

Stackelberg reinsurance and premium decisions with

Liang, Zongxia and Luo, Xiaodong , year =. Stackelberg reinsurance and premium decisions with. SIAM Journal on Financial Mathematics , volume =

-

[3]

2026 , journal =

Equilibrium strategies for singular dividend control problems under the mean-variance criterion , author =. 2026 , journal =

2026

-

[4]

2014 , publisher=

Brownian motion and stochastic calculus , author=. 2014 , publisher=

2014

-

[5]

Insurance: Mathematics and Economics , volume=

On dividend strategies with non-exponential discounting , author=. Insurance: Mathematics and Economics , volume=. 2014 , publisher=

2014

-

[6]

2012 , publisher=

Aspects of risk theory , author=. 2012 , publisher=

2012

-

[7]

Mathematics of Operations Research , year=

On time-consistent equilibrium stopping under aggregation of diverse discount rates , author=. Mathematics of Operations Research , year=

-

[8]

A general theory of

Björk, Tomas and Murgoci, Agatha , journal=. A general theory of

-

[9]

Mathematical Methods of Operations Research , volume=

Optimal risk and dividend distribution control models for an insurance company , author=. Mathematical Methods of Operations Research , volume=. 2000 , publisher=

2000

-

[10]

Transactions of the XVth International Congress of Actuaries , volume=

Su un’impostazione alternativa della teoria collettiva del rischio , author=. Transactions of the XVth International Congress of Actuaries , volume=. 1957 , organization=

1957

-

[11]

Insurance: Mathematics and Economics , volume=

Controlled diffusion models for optimal dividend pay-out , author=. Insurance: Mathematics and Economics , volume=. 1997 , publisher=

1997

-

[12]

Russian Mathematical Surveys , volume=

Optimization of the flow of dividends , author=. Russian Mathematical Surveys , volume=

-

[13]

North American Actuarial Journal , volume=

Strategies for dividend distribution: A review , author=. North American Actuarial Journal , volume=. 2009 , publisher=

2009

-

[14]

RACSAM-Revista de la Real Academia de Ciencias Exactas, Fisicas y Naturales

Optimality results for dividend problems in insurance , author=. RACSAM-Revista de la Real Academia de Ciencias Exactas, Fisicas y Naturales. Serie A. Matematicas , volume=. 2009 , publisher=

2009

-

[15]

Estimating individual discount rates in

Harrison, Glenn W and Lau, Morten I and Williams, Melonie B , journal=. Estimating individual discount rates in. 2002 , publisher=

2002

-

[16]

American Economic Review , volume=

The personal discount rate: Evidence from military downsizing programs , author=. American Economic Review , volume=. 2001 , publisher=

2001

-

[17]

Journal of Economic Literature , volume=

Time discounting and time preference: A critical review , author=. Journal of Economic Literature , volume=. 2002 , publisher=

2002

-

[18]

American Economic Review , volume=

Gamma discounting , author=. American Economic Review , volume=. 2001 , publisher=

2001

-

[19]

Econometrica , volume=

A smooth model of decision making under ambiguity , author=. Econometrica , volume=. 2005 , publisher=

2005

-

[20]

Journal of Economic Theory , volume=

Recursive smooth ambiguity preferences , author=. Journal of Economic Theory , volume=. 2009 , publisher=

2009

-

[21]

Journal of Economic Theory , volume=

Weighted discounting—on group diversity, time-inconsistency, and consequences for investment , author=. Journal of Economic Theory , volume=. 2020 , publisher=

2020

-

[22]

American Economic Journal: Microeconomics , volume=

Collective dynamic choice: the necessity of time inconsistency , author=. American Economic Journal: Microeconomics , volume=. 2015 , publisher=

2015

-

[23]

Journal of Economic Theory , volume=

Time consistency and time invariance in collective intertemporal choice , author=. Journal of Economic Theory , volume=. 2018 , publisher=

2018

-

[24]

The Review of Financial Studies , author =

Dynamic Mean-Variance Asset Allocation , volume =. The Review of Financial Studies , author =. 2010 , pages =

2010

-

[25]

Management Science , author =

A Dynamic Mean-Variance Analysis for Log Returns , volume =. Management Science , author =. 2021 , pages =

2021

-

[26]

Mathematical Finance , volume =

Björk, Tomas and Murgoci, Agatha and Zhou, Xun Yu , title =. Mathematical Finance , volume =

-

[27]

Available at SSRN 4958481 , year=

Dynamic mean-variance portfolio selection with transaction costs , author=. Available at SSRN 4958481 , year=

-

[28]

arXiv preprint arXiv:2507.04836 , year=

Time-inconsistent singular control problems: Reflection and Absolutely continuous controls with exploding rates , author=. arXiv preprint arXiv:2507.04836 , year=

-

[29]

Stochastic Processes: Selected Papers of Hiroshi Tanaka , volume=

Stochastic differential equations with reflecting boundary condition in convex regions , author=. Stochastic Processes: Selected Papers of Hiroshi Tanaka , volume=. 1979 , publisher=

1979

-

[30]

On optimal periodic dividend and capital injection strategies for spectrally negative

Noba, Kei and P. On optimal periodic dividend and capital injection strategies for spectrally negative. Journal of Applied Probability , volume=. 2018 , publisher=

2018

-

[31]

Optimal dividend policies for compound

Azcue, Pablo and Muler, Nora , journal=. Optimal dividend policies for compound. 2012 , publisher=

2012

-

[32]

Optimal dividend distribution under

Jiang, Zhengjun and Pistorius, Martijn , journal=. Optimal dividend distribution under. 2012 , publisher=

2012

-

[33]

Scandinavian Actuarial Journal , volume=

Optimal reinsurance and dividends with transaction costs and taxes under thinning structure , author=. Scandinavian Actuarial Journal , volume=. 2021 , publisher=

2021

-

[34]

Applied Mathematics & Optimization , volume=

Optimal dividend payout with path-dependent drawdown constraint , author=. Applied Mathematics & Optimization , volume=. 2026 , publisher=

2026

-

[35]

SIAM Journal on Financial Mathematics , volume=

Optimal dividends under model uncertainty , author=. SIAM Journal on Financial Mathematics , volume=. 2023 , publisher=

2023

-

[36]

Insurance: Mathematics and Economics , volume=

Optimal dividends under Markov-modulated bankruptcy level , author=. Insurance: Mathematics and Economics , volume=. 2022 , publisher=

2022

-

[37]

Mathematics of Operations Research , volume=

Dynamic optimal reinsurance and dividend payout in finite time horizon , author=. Mathematics of Operations Research , volume=. 2023 , publisher=

2023

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.