Inference in Tightly Identified and Large-Scale Sign-Restricted SVARs

Pith reviewed 2026-05-22 10:22 UTC · model grok-4.3

The pith

A reparameterization turns inequality restrictions in large sign-restricted SVARs into continuously differentiable mappings for direct Hamiltonian Monte Carlo sampling.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

We propose a new approach to inference in tightly identified and large-scale structural vector autoregressions based on a reparameterization that enables imposing identifying inequality restrictions through continuously differentiable mappings. Permitted inequality restrictions include shape and ranking restrictions as well as bounds on economically relevant elasticities, and the approach is also able to accommodate zero restrictions in a straightforward manner. We implement a Hamiltonian Monte Carlo algorithm and show how the posterior density can be rapidly evaluated under the reparameterization, thus facilitating inference in high-dimensional settings. Two empirical applications show that

What carries the argument

Reparameterization of the structural parameters via continuously differentiable mappings that send the restricted space to an unrestricted domain, preserving the posterior while enabling rapid density evaluation and gradient-based Hamiltonian Monte Carlo sampling.

If this is right

- Shape, ranking, and elasticity-bound restrictions can be imposed alongside sign restrictions without changing the sampler.

- Zero restrictions integrate directly into the same continuously differentiable framework.

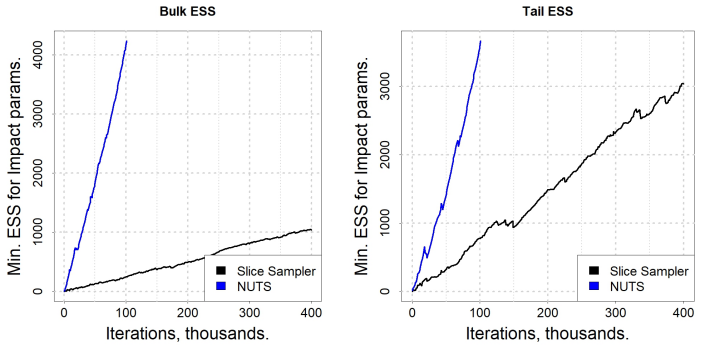

- Markov chains exhibit reduced serial dependence, raising effective sample sizes in high-dimensional models.

- Overall computation time drops, making previously intractable large-scale SVARs feasible for applied work.

Where Pith is reading between the lines

- The same reparameterization idea could transfer to other Bayesian models that impose inequality constraints on parameters, such as certain DSGE specifications.

- Numerical stability in very large systems would encourage economists to use denser sets of identifying assumptions in policy studies.

- Pairing the mappings with automatic differentiation libraries might further reduce the need for manual gradient coding in even bigger models.

Load-bearing premise

The continuously differentiable mappings must preserve the original posterior distribution exactly and remain numerically stable when the number of variables and restrictions grows large.

What would settle it

Apply both the new Hamiltonian Monte Carlo sampler and a standard method to the same large SVAR model with many tight sign restrictions and compare effective sample size per unit of computation time; if the new sampler does not produce larger values, the efficiency claim fails.

Figures

read the original abstract

We propose a new approach to inference in tightly identified and large-scale structural vector autoregressions based on a reparameterization that enables imposing identifying inequality restrictions through continuously differentiable mappings. Permitted inequality restrictions include shape and ranking restrictions as well as bounds on economically relevant elasticities, and the approach is also able to accommodate zero restrictions in a straightforward manner. We implement a Hamiltonian Monte Carlo algorithm and show how the posterior density can be rapidly evaluated under the reparameterization, thus facilitating inference in high-dimensional settings. Two empirical applications demonstrate that our approach tends to result in lower serial dependence in Markov chains, larger effective sample sizes and reduced computation time relative to existing methods.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes a reparameterization of the parameter space in sign-restricted SVARs that imposes identifying inequality restrictions (sign, ranking, elasticity bounds) through continuously differentiable mappings. This enables direct evaluation of the posterior density for Hamiltonian Monte Carlo sampling, with zero restrictions handled by fixing coordinates. Two empirical applications are used to demonstrate lower serial dependence, larger effective sample sizes, and reduced computation time relative to existing methods in large-scale, tightly identified settings.

Significance. If the reparameterization is a diffeomorphism that exactly preserves the target posterior via the change-of-variables formula (with Jacobian folded into the density) and remains stable at scale, the contribution would be a meaningful advance for Bayesian SVAR inference. Explicit constructions for common restrictions and the use of Householder/Givens-based parameterizations to avoid explicit inversions are strengths that support the efficiency claims.

minor comments (3)

- §3 (reparameterization construction): while the skeptic note confirms the mapping is invertible and the Jacobian is incorporated, an explicit worked example for the ranking restriction (including the derivative) would improve verifiability for readers implementing the method.

- §5 (empirical applications): report the exact dimensions of each application (number of endogenous variables, number of sign/ranking restrictions, sample size) to allow direct assessment of how performance scales with problem size.

- Notation: ensure the transformed parameter vector and its Jacobian determinant are denoted consistently across the density evaluation and HMC implementation sections to avoid reader confusion.

Simulated Author's Rebuttal

We thank the referee for their positive and accurate summary of our manuscript and for recommending minor revision. The referee correctly identifies the core contribution of the differentiable reparameterization for imposing sign, ranking, and elasticity restrictions in SVARs while enabling efficient HMC sampling. We appreciate the recognition of the strengths in explicit constructions and Householder/Givens-based parameterizations.

Circularity Check

No significant circularity; derivation is self-contained

full rationale

The paper's central contribution is an explicit reparameterization of the SVAR parameter space via continuously differentiable mappings (e.g., Householder or Givens rotations) that enforce sign, ranking, and elasticity restrictions while preserving the target posterior exactly through the change-of-variables formula and explicit Jacobian evaluation. This construction is presented as a modeling choice whose validity follows directly from the diffeomorphism property and standard HMC density evaluation; no step reduces a reported performance gain (lower serial dependence, larger ESS, reduced runtime) to a quantity fitted inside the same model or to an unverified self-citation. The empirical comparisons are external benchmarks against existing methods, and the numerical stability claims rest on the algebraic properties of the chosen parameterizations rather than on any fitted input renamed as a prediction. The derivation chain therefore contains no load-bearing self-definition, fitted-input-as-prediction, or self-citation reduction.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption The reparameterization mappings are continuously differentiable and map the unrestricted parameter space onto the region defined by the identifying restrictions.

Lean theorems connected to this paper

-

IndisputableMonolith/Foundation/RealityFromDistinction.leanreality_from_one_distinction unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

reparameterization that enables imposing identifying inequality restrictions through continuously differentiable mappings... Hamiltonian Monte Carlo algorithm

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

Jacobian determinant folded into the density evaluation for HMC

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

Amir Ahmadi, P., and Drautzburg, T. (2021). Identification and inference with ranking restrictions.Quantitative Economics,12(1), 1–39. Antolín-Díaz, J., and Rubio-Ramírez, J. F. (2018). Narrative sign restrictions for svars. The American Economic Review,108(10), 2802–2829. Arias, J. E., Rubio-Ramirez, J. F., and Shin, M. (2025).A Gibbs Sampler for Efficie...

work page internal anchor Pith review Pith/arXiv arXiv 2021

-

[2]

Uhlig, H. (2017). Shocks, sign restrictions, and identification.Advances in Economics and Econometrics,2,

work page 2017

-

[3]

Vats, D., Flegal, J. M., and Jones, G. L. (2019). Multivariate output analysis for Markov chain Monte Carlo.Biometrika,106(2), 321–337. 32 Vehtari, A., Gelman, A., Simpson, D., Carpenter, B., and Bürkner, P.-C. (2021). Rank- normalization, folding, and localization: An improvedˆRfor assessing convergence of MCMC (with discussion).Bayesian Analysis,16(2). ...

work page 2019

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.