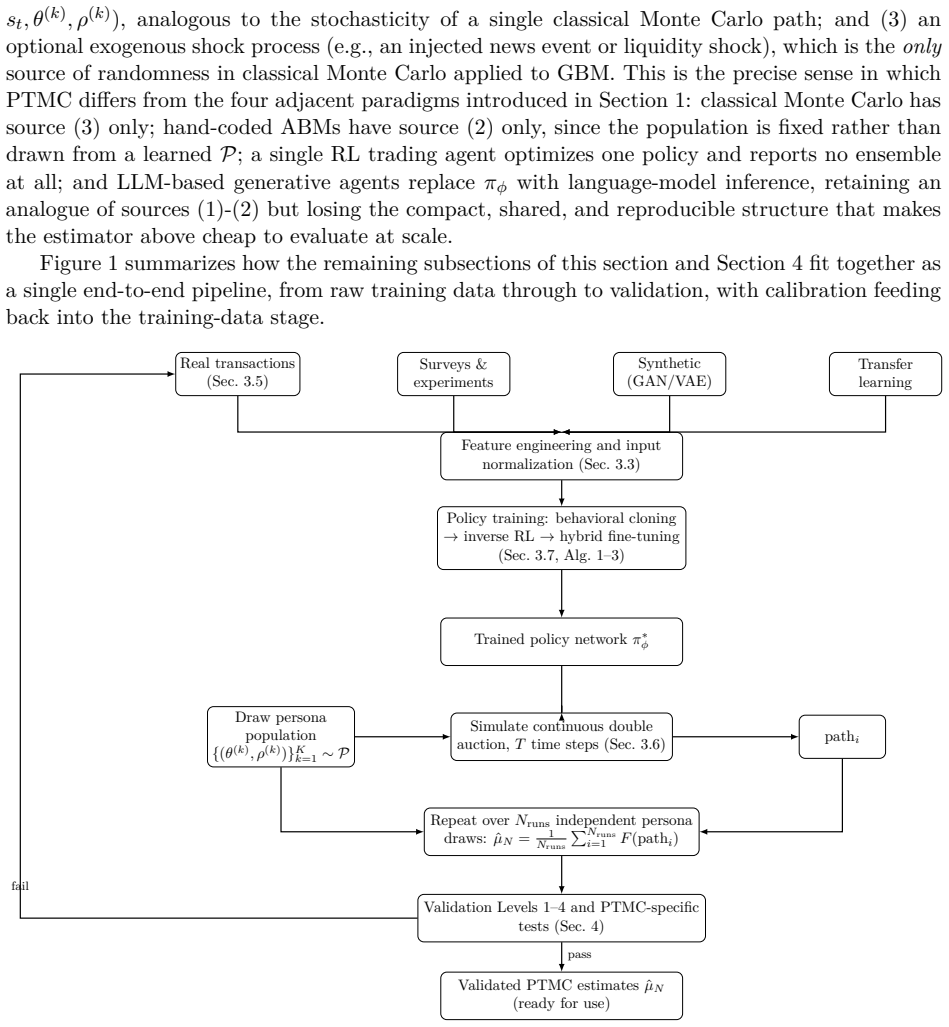

Persona-Trained Monte Carlo: Estimating Market-Outcome Distributions via Swarms of Persona-Conditioned Neural Policy Bots in a Limit Order Book

Pith reviewed 2026-06-30 07:33 UTC · model grok-4.3

The pith

PTMC estimates distributions of market outcomes by simulating limit-order-book interactions among swarms of persona-conditioned neural-policy bots.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The central claim is that an estimator for market-outcome distributions can be constructed by repeatedly running limit-order-book simulations in which many neural-policy bots, conditioned on individually sampled persona parameters drawn from a learned heterogeneity distribution, trade against one another; the aggregate statistics across independent population draws then approximate the target distribution, with the policy network and persona distribution together supplying the required behavioral diversity.

What carries the argument

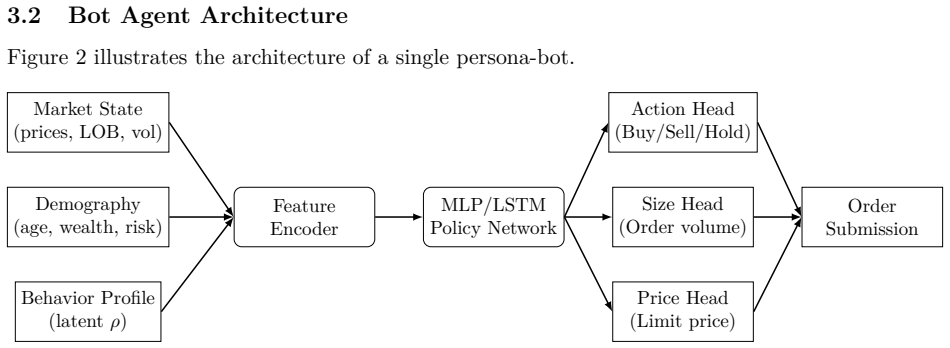

The persona-conditioned neural policy network, which receives sampled persona parameters from the learned trader-heterogeneity distribution and thereby produces heterogeneous trading actions inside the limit-order-book auction.

If this is right

- The estimator converges to the desired distribution as the number of independent persona-population draws increases.

- Uncertainty due to trader heterogeneity enters the Monte Carlo samples through the persona draws rather than only through price noise.

- Validation proceeds in stages from stylized-fact matching through microstructure checks to historical stress-test comparison against a zero-intelligence baseline.

- Design choices in the policy network and training data are justified by links to agent-based computational economics, behavioral finance, and market microstructure.

Where Pith is reading between the lines

- If the simulations succeed, PTMC could support regulatory stress testing by varying the persona distribution to explore different market-participant mixes.

- The approach could be extended to test whether strategic interactions among heterogeneous agents produce systemic-risk scenarios that hand-coded models miss.

- A direct next experiment would compare order-flow statistics from trained PTMC runs against empirical trading data to check calibration of the persona distribution.

- Incorporating exogenous news signals as additional conditioning inputs might allow the same framework to capture event-driven trading without changing the core estimator.

Load-bearing premise

The learned trader-heterogeneity distribution together with the persona-conditioned policy network will generate simulated price paths whose statistical properties are close enough to real markets for the Monte Carlo estimates to be useful.

What would settle it

Implementing the proposed bot architecture and training, then observing that the resulting simulated price paths fail to reproduce key statistical features of real limit-order-book data such as fat-tailed returns or volatility clustering would show the estimator does not deliver the intended distributions.

Figures

read the original abstract

We propose Persona-Trained Monte Carlo (PTMC), a method for estimating distributions of market-outcome statistics by repeatedly simulating limit-order-book interaction among swarms of persona-conditioned neural-policy trading bots. Each run instantiates many bots sharing one trained policy network but conditioned on heterogeneous, individually sampled persona parameters drawn from a learned trader-heterogeneity distribution; the bots interact in a continuous double auction, and the resulting price path is one Monte Carlo sample. Repeating this over independent persona-population draws yields an ensemble from which a target market statistic is estimated. Randomness enters through persona draws, within-run action sampling, and optional exogenous shocks, not solely through price as in classical Monte Carlo. We distinguish PTMC from adjacent paradigms, including classical Monte Carlo, hand-coded agent-based models, single-agent reinforcement learning, and large-language-model-based generative agents. To justify the design, we survey cross-disciplinary foundations -- agent-based computational economics, market microstructure, behavioral finance, deep reinforcement learning, generative/LLM-based agents, news-driven trading, systemic risk, econophysics, and game theory -- connecting each literature to a specific design choice in the policy network, training data, or validation protocol. We formalize the PTMC estimator and its convergence properties, specify a candidate bot architecture and training objective, and propose a four-level validation methodology: stylized-fact matching, microstructure- and agent-level checks, and historical stress-test comparison against a zero-intelligence baseline. The framework is proposed but not implemented: we contribute a formal estimator, a cross-disciplinary design justification, and a validation roadmap, and conclude with open research questions.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes Persona-Trained Monte Carlo (PTMC), a method for estimating distributions of market-outcome statistics via repeated simulations of limit-order-book interactions among swarms of persona-conditioned neural-policy trading bots. Each simulation draws heterogeneous persona parameters from a learned trader-heterogeneity distribution, conditions a shared policy network on those parameters, runs the bots in a continuous double auction, and treats the resulting price path as one Monte Carlo sample. The paper distinguishes PTMC from classical Monte Carlo, hand-coded ABMs, single-agent RL, and LLM agents; surveys cross-disciplinary literatures to justify design choices; formalizes the estimator and its convergence properties; specifies a candidate bot architecture and training objective; and outlines a four-level validation roadmap (stylized-fact matching, microstructure checks, agent-level checks, historical stress tests). It explicitly states that the framework is proposed but not implemented.

Significance. If the untested assumption that the learned heterogeneity distribution and conditioned policies can generate price paths whose moments, autocorrelations, and tail behavior match real LOB data holds, PTMC could supply a flexible, heterogeneity-aware estimator for market statistics that classical Monte Carlo cannot easily incorporate. The formal estimator, convergence claim, and cross-disciplinary design justification constitute the main contributions; however, the absence of any implementation, trained models, or numerical results leaves the practical significance prospective rather than demonstrated.

major comments (2)

- [Abstract] Abstract and validation-roadmap section: the central claim that PTMC yields useful Monte Carlo estimates requires that the persona-conditioned simulations reproduce real-market statistical properties at the level needed for the estimator; the manuscript supplies the formal estimator and convergence math but contains no implementation, no trained policies, and no empirical checks against stylized facts or historical data, so soundness cannot be evaluated from the text.

- [Persona sampling step] Persona sampling step: the trader-heterogeneity distribution is described as learned, yet no external data source, fitting procedure, or training corpus for the persona parameters is specified; this leaves the estimator dependent on quantities whose values are defined inside the proposal itself.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed review. The manuscript is explicitly a proposal for the PTMC framework rather than an implemented system, and we respond to each major comment below while revising the text to clarify scope and address the noted gaps.

read point-by-point responses

-

Referee: [Abstract] Abstract and validation-roadmap section: the central claim that PTMC yields useful Monte Carlo estimates requires that the persona-conditioned simulations reproduce real-market statistical properties at the level needed for the estimator; the manuscript supplies the formal estimator and convergence math but contains no implementation, no trained policies, and no empirical checks against stylized facts or historical data, so soundness cannot be evaluated from the text.

Authors: We agree that the practical soundness of PTMC as an estimator cannot be evaluated without implementation and empirical checks. The manuscript is presented as a proposal; the abstract and conclusion already state that 'the framework is proposed but not implemented' and that the validation roadmap is offered for future work. The core contributions are the formal estimator, convergence properties, cross-disciplinary justification, and the four-level validation plan. We have revised the abstract and validation-roadmap section to state more explicitly that the estimator's usefulness is conditional on the simulations reproducing the required market statistical properties, which the roadmap is designed to test. revision: yes

-

Referee: [Persona sampling step] Persona sampling step: the trader-heterogeneity distribution is described as learned, yet no external data source, fitting procedure, or training corpus for the persona parameters is specified; this leaves the estimator dependent on quantities whose values are defined inside the proposal itself.

Authors: We agree that the manuscript does not specify concrete data sources or a fitting procedure for the learned trader-heterogeneity distribution. The term 'learned' is used to distinguish the approach from hand-coded heterogeneity, but the paper focuses on the high-level architecture and estimator rather than implementation details. In revision we will add a subsection proposing candidate external data sources (e.g., historical limit-order-book records with trader identifiers) and outlining possible fitting methods such as variational inference or moment-matching on observed order-flow statistics, while noting that the precise procedure remains an open research question. revision: yes

Circularity Check

No circularity; proposal is a formal method with external validation roadmap

full rationale

The paper proposes PTMC as a formal estimator with convergence properties, distinguishes it from adjacent paradigms, surveys cross-disciplinary foundations to justify design choices, specifies a candidate architecture and training objective, and outlines a four-level validation methodology (stylized-fact matching, microstructure checks, agent-level checks, historical stress-test). No load-bearing step reduces by the paper's own equations or self-citation to its inputs by construction; the method is explicitly presented as unimplemented, with utility conditioned on future empirical matching to external real-market data that is not claimed to be already achieved. No fitted parameters are renamed as predictions, no uniqueness theorems are imported from self-citations, and no ansatz is smuggled via prior work. The derivation chain is therefore self-contained as a methodological proposal.

Axiom & Free-Parameter Ledger

free parameters (3)

- trader-heterogeneity distribution

- policy-network conditioning variables

- training objective for the shared policy

axioms (2)

- domain assumption The continuous double-auction mechanism produces well-defined price paths when populated by the described bots.

- standard math Convergence properties of the Monte Carlo estimator hold under the stated randomness sources.

invented entities (1)

-

persona-conditioned neural policy bot

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Systemic risk and stability in financial networks

Daron Acemoglu, Asuman Ozdaglar, and Alireza Tahbaz-Salehi. Systemic risk and stability in financial networks. American Economic Review, 105 0 (2): 0 564--608, 2015

2015

-

[2]

Financial contagion

Franklin Allen and Douglas Gale. Financial contagion. Journal of Political Economy, 108 0 (1): 0 1--33, 2000

2000

-

[3]

Optimal execution of portfolio transactions

Robert Almgren and Neil Chriss. Optimal execution of portfolio transactions. Journal of Risk, 3 0 (2): 0 5--40, 2001

2001

-

[4]

Andersen, Tim Bollerslev, Francis X

Torben G. Andersen, Tim Bollerslev, Francis X. Diebold, and Henrik Ebens. The distribution of realized stock return volatility. Journal of Financial Economics, 61 0 (1): 0 43--76, 2001. doi:10.1016/S0304-405X(01)00055-1

-

[5]

Anderson and Donald A

Theodore W. Anderson and Donald A. Darling. Asymptotic theory of certain goodness of fit criteria based on stochastic processes. Journal of the American Statistical Association, 49 0 (268): 0 765--769, 1952

1952

-

[6]

FinBERT: Financial Sentiment Analysis with Pre-trained Language Models

Dogu Araci. FinBERT : Financial sentiment analysis with pre-trained language models. arXiv preprint arXiv:1908.10063, 2019

work page internal anchor Pith review Pith/arXiv arXiv 1908

-

[7]

A survey of cross-validation procedures for model selection

Sylvain Arlot and Alain Celisse. A survey of cross-validation procedures for model selection. Statistics surveys, 4: 0 40--79, 2010

2010

-

[8]

Existence of an equilibrium for competitive economies

Kenneth Joseph Arrow and G \'e rard Debreu. Existence of an equilibrium for competitive economies. Econometrica, 1954

1954

-

[9]

W. B. Arthur, J. H. Holland, B. LeBaron, R. G. Palmer, and P. Tayler. Asset pricing under endogenous expectations in an artificial stock market, pages 15--44. Addison-Wesley, Reading, MA, 1997

1997

-

[10]

Probabilistic LSTM modeling for stock price prediction with Monte Carlo dropout long short-term memory network

Clement Asare, Derrick Asante, and John Fiifi Essel. Probabilistic LSTM modeling for stock price prediction with Monte Carlo dropout long short-term memory network. International Journal of Innovative Science and Research Technology, 8 0 (7), 2023

2023

-

[11]

Robert J. Aumann. Correlated equilibrium as an expression of B ayesian rationality. Econometrica, 55 0 (1): 0 1--18, 1987. doi:10.2307/1911154

-

[12]

Robert L. Axtell and J. Doyne Farmer. Agent-based modeling in economics and finance: Past, present, and future. Journal of Economic Literature, 63 0 (1): 0 197--287, 2025. doi:10.1257/jel.20221319

-

[13]

Self-organized criticality: A n explanation of 1/f noise

Per Bak, Chao Tang, and Kurt Wiesenfeld. Self-organized criticality: A n explanation of 1/f noise. Physical Review Letters, 59 0 (4): 0 381--384, 1987

1987

-

[14]

Verification, validation, and testing of computer simulation models

Osman Balci. Verification, validation, and testing of computer simulation models. Annals of Operations Research, 53 0 (1): 0 121--173, 1998

1998

-

[15]

Emergence of scaling in random networks

Albert-L \'a szl\'o Barab \'a si and R \'e ka Albert. Emergence of scaling in random networks. Science, 286 0 (5439): 0 509--512, 1999. doi:10.1126/science.286.5439.509

-

[16]

Brad M. Barber and Terrance Odean. Trading is hazardous to your wealth: T he common stock investment performance of individual investors. Journal of Finance, 55 0 (2): 0 773--806, 2000. doi:10.1111/0022-1082.00226

-

[17]

Nicholas Barberis and Richard H. Thaler. A survey of behavioral finance. Handbook of the Economics of Finance, 1: 0 1053--1128, 2003

2003

-

[18]

The physics of financial networks

Marco Bardoscia, Paolo Barucca, Stefano Battiston, Fabio Caccioli, Giulio Cimini, Diego Garlaschelli, Fabio Saracco, Tiziano Squartini, and Guido Caldarelli. The physics of financial networks. Nature Reviews Physics, 3: 0 490--507, 2021. doi:10.1038/s42254-021-00322-5

-

[19]

The Second Machine Age: Work, Progress, and Prosperity in a Time of Brilliant Technologies

Leonardo Bargigli, Giovanni di Iasio, Luigi Infante, Fabrizio Lillo, and Federico Pierobon. The multiplex structure of interbank networks. Quantitative Finance, 15 0 (4): 0 673--691, 2015. doi:10.1080/14697688.2014.968356

-

[20]

B asel III : A global regulatory framework for more resilient banks and banking systems

Basel Committee . B asel III : A global regulatory framework for more resilient banks and banking systems. Bank for International Settlements, 2010

2010

-

[21]

Relational inductive biases, deep learning, and graph networks

Peter W. Battaglia, Jessica B. Hamrick, Victor Bapst, Alvaro Sanchez-Gonzalez, Vinicius Zambaldi, Mateusz Malinowski, Andrea Tacchetti, Razvan Pascanu, Razvan Pascanu, Wojciech Zaremba, and Oriol Vinyals. Relational inductive biases, deep learning, and graph networks. arXiv preprint arXiv:1806.01261, 2018

work page internal anchor Pith review Pith/arXiv arXiv 2018

-

[22]

Liabilities create interdependencies in interbank networks

Stefano Battiston, Michelangelo Puliga, Rahul Kaushik, Paolo Tasca, and Guido Caldarelli. Liabilities create interdependencies in interbank networks. Scientific reports, 2 0 (1): 0 1--6, 2012

2012

-

[23]

Beaumont, Wenyang Zhang, and David J

Mark A. Beaumont, Wenyang Zhang, and David J. Balding. Approximate B ayesian computation in population genetics. Genetics, 162 0 (4): 0 2025--2035, 2002

2025

-

[24]

Beinhocker

Eric D. Beinhocker. The origin of wealth: E volution, complexity, and the radical remaking of economics. 2006

2006

-

[25]

Dynamic programming

Richard Bellman. Dynamic programming. 1957

1957

-

[26]

Herd behavior in financial markets

Sushil Bikhchandani and Sunil Sharma. Herd behavior in financial markets. IMF Staff Papers, 47 0 (3): 0 279--310, 2000

2000

-

[27]

The pricing of options and corporate liabilities

Fischer Black and Myron Scholes. The pricing of options and corporate liabilities. Journal of Political Economy, 81 0 (3): 0 637--654, 1973

1973

-

[28]

Evolution and market behavior

Lawrence Blume and David Easley. Evolution and market behavior. Journal of Economic Theory, 58 0 (1): 0 9--40, 1992

1992

-

[29]

Weight uncertainty in neural networks

Charles Blundell, Julien Cornebise, Koray Kavukcuoglu, and Daan Wierstra. Weight uncertainty in neural networks. In Proceedings of the 32nd International Conference on Machine Learning (ICML), volume 37, pages 1613--1622, 2015

2015

-

[30]

Generalized autoregressive conditional heteroskedasticity

Tim Bollerslev. Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31 0 (3): 0 307--327, 1986

1986

-

[31]

On the Opportunities and Risks of Foundation Models

Rishi Bommasani, Drew A. Hudson, Ehsan Adeli, Russ Altman, et al. On the opportunities and risks of foundation models. arXiv preprint arXiv:2108.07258, 2021

work page internal anchor Pith review Pith/arXiv arXiv 2021

-

[32]

George E. P. Box and Gwilym M. Jenkins. Time series analysis, forecasting and control. Journal of the Royal Statistical Society B, 1970

1970

-

[33]

Biologically Inspired Algorithms for Financial Modelling

Anthony Brabazon and Michael O'Neill. Biologically Inspired Algorithms for Financial Modelling. Springer, Berlin, 2006. doi:10.1007/978-3-540-31307-4

-

[34]

Brock and Cars H

William A. Brock and Cars H. Hommes. Heterogeneous beliefs and routes to chaos in a simple asset pricing model. Journal of Economic Dynamics and Control, 22 0 (8--9): 0 1235--1274, 1998

1998

-

[35]

Generative adversarial networks in time series: A survey and taxonomy, 2021

Eoin Brophy, Zhengwei Wang, Qi She, and Tomas Ward. Generative adversarial networks in time series: A survey and taxonomy, 2021. URL https://arxiv.org/abs/2107.11098

-

[36]

Language Models are Few-Shot Learners

Tom B. Brown, Benjamin Mann, Nick Ryder, Melanie Subbiah, Jared Kaplan, Prafulla Dhariwal, Arvind Neelakantan, Pranav Shyam, Girish Sastry, Amanda Askell, et al. Language models are few-shot learners. arXiv preprint arXiv:2005.14165, 2020

work page internal anchor Pith review Pith/arXiv arXiv 2005

-

[37]

Mark M. Carhart. On persistence in mutual fund performance. Journal of Finance, 52 0 (1): 0 57--82, 1997

1997

-

[38]

A probabilistic weak formulation of mean field games and applications

Ren\' e Carmona and Daniel Lacker. A probabilistic weak formulation of mean field games and applications. The Annals of Applied Probability, 25 0 (3): 0 1189--1231, 2015. doi:10.1214/14-AAP1020

-

[39]

Bayesian neural networks for stock price forecasting before and during COVID-19 pandemic

Rohitash Chandra and Yixuan He. Bayesian neural networks for stock price forecasting before and during COVID-19 pandemic. PLOS ONE, 16 0 (7): 0 e0253217, 2021. doi:10.1371/journal.pone.0253217

-

[40]

Genetic algorithms and genetic programming in tackling different types of market inefficiencies

Shu-Heng Chen and Chen-Chih Tai. Genetic algorithms and genetic programming in tackling different types of market inefficiencies. International Journal of Economics and Finance, 2 0 (9): 0 149, 2012

2012

-

[41]

A behavioural model of investor sentiment in limit order markets

Carl Chiarella, Xue-Zhong He, Lei Shi, and Lijian Wei. A behavioural model of investor sentiment in limit order markets. Quantitative Finance, 17 0 (1): 0 71--86, 2017. doi:10.1080/14697688.2016.1184756. URL https://doi.org/10.1080/14697688.2016.1184756

-

[42]

Empirical properties of asset returns: S tylized facts and statistical issues

Rama Cont. Empirical properties of asset returns: S tylized facts and statistical issues. Quantitative Finance, 1 0 (2): 0 223--236, 2001

2001

-

[43]

Herd behavior and aggregate fluctuations in financial markets

Rama Cont and Jean-Philippe Bouchaud. Herd behavior and aggregate fluctuations in financial markets. Macroeconomic Dynamics, 4 0 (2): 0 170--196, 2000

2000

-

[44]

Cox, Stephen A

John C. Cox, Stephen A. Ross, and Mark Rubinstein. Option pricing: A simplified approach. Journal of Financial Economics, 7 0 (3): 0 229--263, 1979

1979

-

[45]

Kent Daniel and Tobias J. Moskowitz. Momentum crashes. Journal of Financial Economics, 122 0 (2): 0 221--247, 2016. ISSN 0304-405X. doi:10.1016/j.jfineco.2015.12.002. URL https://www.sciencedirect.com/science/article/pii/S0304405X16301490

-

[46]

Investor psychology and security market under- and overreactions

Kent Daniel, David Hirshleifer, and Avanidhar Subrahmanyam. Investor psychology and security market under- and overreactions. Journal of Finance, 53 0 (6): 0 1839--1885, 1998. doi:10.1111/0022-1082.00077. URL https://onlinelibrary.wiley.com/doi/abs/10.1111/0022-1082.00077

-

[47]

W. F. M. De Bondt and R. H. Thaler. Does the stock market overreact? Journal of Finance, 40 0 (3): 0 793--805, 1985

1985

-

[48]

Bradford De Long , Andrei Shleifer, Lawrence H

J. Bradford De Long , Andrei Shleifer, Lawrence H. Summers, and Robert J. Waldmann. Noise trader risk in financial markets. Journal of Political Economy, 98 0 (4): 0 703--738, 1990

1990

-

[49]

Benedetto De Martino, Colin F. Camerer, and Ralph Adolphs. Amygdala damage eliminates monetary loss aversion. Proceedings of the National Academy of Sciences, 107 0 (8): 0 3788--3792, 2010. doi:10.1073/pnas.0910230107

-

[50]

Michael A. H. Dempster and Yazid Z. Romahi. Intraday FX trading: An evolutionary reinforcement learning approach. In Intelligent Data Engineering and Automated Learning --- IDEAL 2002 , volume 2412 of Lecture Notes in Computer Science, pages 347--358. Springer, 2002. doi:10.1007/3-540-45675-9_52

-

[51]

Jacob Devlin, Ming-Wei Chang, Kenton Lee, and Kristina Toutanova. BERT : P re-training of deep bidirectional transformers for language understanding. In Proceedings of the 2019 Conference of the North American Chapter of the Association for Computational Linguistics: Human Language Technologies, pages 4171--4186, Minneapolis, Minnesota, 2019. Association ...

-

[52]

Time series analysis by state space methods

James Durbin and Siem Jan Koopman. Time series analysis by state space methods. Oxford University Press, 2012

2012

-

[53]

Differential privacy: A survey of results

Cynthia Dwork. Differential privacy: A survey of results. In Theory and Applications of Models of Computation, pages 1--19, Berlin, Heidelberg, 2008. Springer Berlin Heidelberg. ISBN 978-3-540-79228-4. doi:10.1007/978-3-540-79228-4_1

-

[54]

Price, trade size, and information in securities markets

David Easley and Maureen O'Hara. Price, trade size, and information in securities markets. Journal of Financial Economics, 19 0 (1): 0 69--90, 1987. ISSN 0304-405X. doi:10.1016/0304-405X(87)90029-8. URL https://www.sciencedirect.com/science/article/pii/0304405X87900298

-

[55]

Handbook of E conomic F orecasting , volume 2

Graham Elliott and Allan Timmermann, editors. Handbook of E conomic F orecasting , volume 2. Elsevier, Amsterdam, 2013

2013

- [56]

-

[57]

Bounded strategic reasoning explains crisis emergence in multi-agent market games

Benjamin Patrick Evans and Mikhail Prokopenko. Bounded strategic reasoning explains crisis emergence in multi-agent market games. Royal Society Open Science, 10 0 (2): 0 221164, 2023. doi:10.1098/rsos.221164

-

[58]

Gianluca Fabiani, Nikolaos Evangelou, Tianqi Cui, Juan M. Bello-Rivas, Cristina P. Martin-Linares, Constantinos Siettos, and Ioannis G. Kevrekidis. Task-oriented machine learning surrogates for tipping points of agent-based models. Nature Communications, 15: 0 4117, 2024. doi:10.1038/s41467-024-48024-7

-

[59]

On the problem of calibrating an agent based model for financial markets

Annalisa Fabretti. On the problem of calibrating an agent based model for financial markets. Journal of Economic Interaction and Coordination, 8 0 (2): 0 277--293, 2013. doi:10.1007/s11403-012-0096-3

-

[60]

Macroeconomic policy in DSGE and agent-based models redux: New developments and challenges ahead

Giorgio Fagiolo and Andrea Roventini. Macroeconomic policy in DSGE and agent-based models redux: New developments and challenges ahead. Journal of Artificial Societies and Social Simulation, 20 0 (1): 0 1, 2017. doi:10.18564/jasss.3280

-

[61]

A critical guide to empirical validation of agent-based models

Giorgio Fagiolo, Alessio Moneta, and Paul Windrum. A critical guide to empirical validation of agent-based models. Computational Economics, 30 0 (3): 0 195--226, 2007. ISSN 1572-9974. doi:10.1007/s10614-007-9104-4. URL https://doi.org/10.1007/s10614-007-9104-4

-

[62]

Validation of agent-based models in economics and finance

Giorgio Fagiolo, Mattia Guerini, Francesco Lamperti, Alessio Moneta, and Andrea Roventini. Validation of agent-based models in economics and finance. In Claus Beisbart and Nicole J. Saam, editors, Computer Simulation Validation: Fundamental Concepts, Methodological Frameworks, and Philosophical Perspectives, pages 763--787. Springer International Publishi...

- [63]

-

[64]

Eugene F. Fama and Kenneth R. French. Common risk factors in the returns of stocks and bonds. Journal of Financial Economics, 33 0 (1): 0 3--56, 1993. ISSN 0304-405X. doi:10.1016/0304-405X(93)90023-5. URL https://www.sciencedirect.com/science/article/pii/0304405X93900235

-

[65]

J. Doyne Farmer and Duncan Foley. The economy needs agent-based modelling. Nature, 460: 0 685--686, 2009. doi:10.1038/460685a

-

[66]

The price dynamics of common trading strategies

J. Doyne Farmer and Shareen Joshi. The price dynamics of common trading strategies. Journal of Economic Behavior and Organization, 49 0 (2): 0 149--171, 2002. URL https://arxiv.org/abs/cond-mat/0012419

work page internal anchor Pith review Pith/arXiv arXiv 2002

-

[67]

J. Doyne Farmer and Thomas Lux. Introduction to the special issue on A pplications of S tatistical P hysics in E conomics and F inance. Journal of Economic Dynamics and Control, 32 0 (1): 0 1--6, 2008. doi:10.1016/j.jedc.2007.09.001

-

[68]

Front-page news: The effect of news positioning on financial markets

Anastassia Fedyk. Front-page news: The effect of news positioning on financial markets. The Journal of Finance, 79 0 (1): 0 5--33, 2024. doi:10.1111/jofi.13287

-

[69]

Model inversion attacks that exploit confidence information and basic countermeasures

Matt Fredrikson, Somesh Jha, and Thomas Ristenpart. Model inversion attacks that exploit confidence information and basic countermeasures. pages 1322--1333, 2015

2015

-

[70]

Dropout as a bayesian approximation: Representing model uncertainty in deep learning

Yarin Gal and Zoubin Ghahramani. Dropout as a bayesian approximation: Representing model uncertainty in deep learning. In Proceedings of the 33rd International Conference on Machine Learning (ICML), volume 48, pages 1050--1059, 2016. URL https://proceedings.mlr.press/v48/gal16.html

2016

-

[71]

Schoenholz, Patrick F

Justin Gilmer, Samuel S. Schoenholz, Patrick F. Riley, Oriol Vinyals, and George E. Dahl. Neural message passing for quantum chemistry. pages 1263--1272, 2017. URL https://proceedings.mlr.press/v70/gilmer17a.html

2017

-

[72]

Paul Glasserman and H. Peyton Young. How likely is contagion in financial networks? Journal of Banking and Finance, 50: 0 383--399, 2015. doi:10.1016/j.jbankfin.2014.02.006

-

[73]

Paul Glasserman, Harry Mamaysky, and Jimmy Qin. New news is bad news. arXiv preprint arXiv:2309.05560, 2023

-

[74]

Lawrence R. Glosten and Paul R. Milgrom. Bid, ask and transaction prices in a specialist market with heterogeneously informed traders. Journal of Financial Economics, 14 0 (1): 0 71--100, 1985. ISSN 0304-405X. doi:10.1016/0304-405X(85)90044-3. URL https://www.sciencedirect.com/science/article/pii/0304405X85900443

-

[75]

Darren K. Gode and Shyam Sunder. Allocative efficiency of markets with zero-intelligence traders: M arket as a partial substitute for individual rationality. Journal of Political Economy, 101 0 (1): 0 119--137, 1993. doi:10.1086/261868

-

[76]

Generative adversarial nets

Ian Goodfellow, Jean Pouget-Abadie, Mehdi Mirza, Bing Xu, David Warde-Farley, Sherjil Ozair, Aaron Courville, and Yoshua Bengio. Generative adversarial nets. Advances in Neural Information Processing Systems (NIPS), pages 2672--2680, 2014. URL https://proceedings.neurips.cc/paper_files/paper/2014/file/f033ed80deb0234979a61f95710dbe25-Paper.pdf

2014

-

[77]

Martin D. Gould, Mason A. Porter, Stacy Williams, Mark McDonald, Daniel J. Fenn, and Sam D. Howison. Limit order books. Quantitative Finance, 13 0 (11): 0 1709--1742, 2013. doi:10.1080/14697688.2013.803148

-

[78]

Graph embedding techniques, applications, and performance: A survey

Palash Goyal and Emilio Ferrara. Graph embedding techniques, applications, and performance: A survey. Knowledge-Based Systems, 151: 0 78--94, 2018. ISSN 0950-7051. doi:10.1016/j.knosys.2018.03.022. URL https://www.sciencedirect.com/science/article/pii/S0950705118301540

-

[79]

Green and Jean-Jacques Laffont

Jerry R. Green and Jean-Jacques Laffont. Partially verifiable information and mechanism design. The Review of Economic Studies, 53 0 (3): 0 447--456, 1986. ISSN 0034-6527. doi:10.2307/2297639. URL https://doi.org/10.2307/2297639

-

[80]

Allan W. Gregory and Gregor W. Smith. Business cycle theory and econometrics. The Economic Journal, 105 0 (433): 0 1597--1608, 1995. ISSN 0013-0133. doi:10.2307/2235121. URL https://doi.org/10.2307/2235121

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.