Insurance Pricing Optimization via Off-Policy Evaluation

Pith reviewed 2026-06-29 09:57 UTC · model grok-4.3

The pith

A kernelized inverse propensity score estimator reduces variance in off-policy value estimates to support optimal insurance pricing that accounts for customer price sensitivity.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

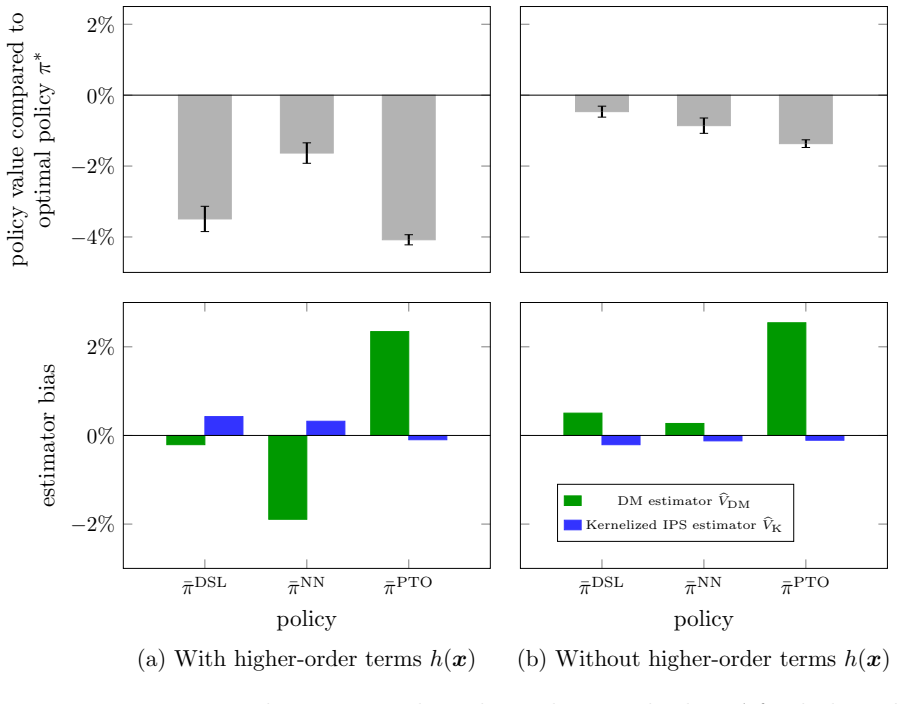

The authors propose a kernelized inverse propensity score estimator that exploits local structure in the action space and yields variance reduction compared to the classical inverse propensity score estimator. Building on these value estimates, they investigate policy optimization and present two practical approaches for computing optimal pricing rules: an interpretable data-shared Lasso formulation and a flexible policy parameterization based on neural networks. Using a controlled synthetic travel insurance environment, they empirically confirm the theoretical results and show that neural networks outperform existing techniques for policy optimization.

What carries the argument

kernelized inverse propensity score estimator that exploits local structure in the action space to reduce variance in off-policy value estimates

If this is right

- Historical pricing data can be reused to evaluate and improve new pricing rules without additional randomized experiments.

- The data-shared Lasso produces pricing rules that remain interpretable while borrowing strength across segments.

- Neural-network policies can capture more complex price-response surfaces than linear or simple parametric alternatives.

- Variance reduction in value estimates translates directly into more stable policy selection during optimization.

Where Pith is reading between the lines

- The same kernelized estimator could be applied to continuous-action pricing problems in retail or dynamic advertising.

- Live A/B tests comparing the learned policies against current company rules would provide the next empirical check.

- If the variance reduction holds, the approach may allow tighter control of combined loss and demand risk in actuarial portfolios.

Load-bearing premise

The controlled synthetic travel insurance environment sufficiently captures real policyholder price sensitivity and response dynamics.

What would settle it

Running the kernelized estimator on the synthetic data and finding no measurable variance reduction relative to the classical estimator, or finding that the optimized policies produce no improvement in simulated revenue or loss metrics, would falsify the central claims.

Figures

read the original abstract

Traditional insurance pricing relies on risk-based principles that ensure actuarial fairness and solvency but do not explicitly account for policyholders' price sensitivity. We formulate insurance pricing as a decision-making problem and study it using tools from off-policy evaluation and stochastic control. We propose a kernelized inverse propensity score estimator that exploits local structure in the action space and yields variance reduction compared to the classical inverse propensity score estimator. Building on these value estimates, we investigate policy optimization and present two practical approaches for computing optimal pricing rules: an interpretable data-shared Lasso formulation and a flexible policy parameterization based on neural networks. Using a controlled synthetic travel insurance environment, we empirically confirm the theoretical results and show that neural networks outperform existing techniques for policy optimization.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper formulates insurance pricing as a decision-making problem using off-policy evaluation and stochastic control. It proposes a kernelized inverse propensity score (IPS) estimator that exploits local structure in the action space to achieve variance reduction relative to classical IPS. Building on the resulting value estimates, it develops two policy optimization approaches—an interpretable data-shared Lasso formulation and a neural-network parameterization—and evaluates them in a controlled synthetic travel insurance environment, where the neural-network optimizer is reported to outperform existing techniques.

Significance. If the kernelized IPS estimator delivers the claimed variance reduction and the optimization procedures produce superior pricing rules, the work would usefully extend OPE methods to a domain where price sensitivity has traditionally been handled separately from risk-based actuarial pricing. The dual presentation of an interpretable Lasso method alongside a flexible neural-network method is a constructive feature. The explicit empirical confirmation on synthetic data is a standard methodological step, but the absence of any reported linkage to real insurance records or sensitivity checks on demand parameters restricts the immediate transferability of the performance gains.

major comments (2)

- [Experiments] Experiments section: All reported variance-reduction and outperformance results are obtained exclusively inside one controlled synthetic travel-insurance simulator. Because the central claim is that the proposed estimators and optimizers are practically useful, the fidelity of this simulator to real policyholder price sensitivity (heterogeneity, dynamics, and response to pricing actions) is load-bearing; no validation against historical records, no sensitivity sweeps over demand parameters, and no comparison to empirical elasticities from the insurance literature are described.

- [Abstract / Experiments] Abstract and Experiments section: The assertions of variance reduction for the kernelized IPS estimator and outperformance of the neural-network optimizer supply no quantitative details on experiment design (number of replications, confidence intervals, statistical tests) or sensitivity to modeling choices, making the empirical support for the main claims difficult to evaluate.

minor comments (2)

- [§3] The notation distinguishing the kernel bandwidth from the propensity-score model parameters could be clarified when the kernelized IPS estimator is first introduced.

- [Figures in Experiments] Figure captions for the synthetic-environment results should explicitly state the number of independent runs and any error bars used.

Simulated Author's Rebuttal

We thank the referee for the constructive comments. We address each major point below, indicating planned revisions where feasible.

read point-by-point responses

-

Referee: [Experiments] Experiments section: All reported variance-reduction and outperformance results are obtained exclusively inside one controlled synthetic travel-insurance simulator. Because the central claim is that the proposed estimators and optimizers are practically useful, the fidelity of this simulator to real policyholder price sensitivity (heterogeneity, dynamics, and response to pricing actions) is load-bearing; no validation against historical records, no sensitivity sweeps over demand parameters, and no comparison to empirical elasticities from the insurance literature are described.

Authors: We agree that additional sensitivity analysis would strengthen the empirical support. We will revise the experiments section to include sensitivity sweeps over key demand parameters (e.g., price elasticity) and comparisons to elasticities reported in the insurance literature. However, we do not have access to proprietary historical insurance records, so direct validation against real data cannot be performed. revision: partial

-

Referee: [Abstract / Experiments] Abstract and Experiments section: The assertions of variance reduction for the kernelized IPS estimator and outperformance of the neural-network optimizer supply no quantitative details on experiment design (number of replications, confidence intervals, statistical tests) or sensitivity to modeling choices, making the empirical support for the main claims difficult to evaluate.

Authors: We will revise both the abstract and experiments section to report the number of replications (100 independent runs), 95% confidence intervals, results of statistical tests (paired t-tests), and sensitivity analyses with respect to modeling choices such as kernel bandwidth and neural-network hyperparameters. revision: yes

- Direct validation against historical insurance records, as we lack access to such proprietary data.

Circularity Check

No circularity: new estimators and optimizers introduced independently of fitted inputs

full rationale

The paper introduces a kernelized inverse propensity score estimator and two policy optimization methods (Lasso and neural networks) as novel constructs. These are applied to a synthetic environment for empirical confirmation, but the reported performance does not reduce by the paper's own equations to quantities already fitted inside the study. No self-definitional steps, fitted inputs renamed as predictions, or load-bearing self-citations appear in the derivation chain. The central claims remain independent of the inputs by construction.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption The synthetic travel insurance environment accurately models policyholder price sensitivity and response dynamics.

Reference graph

Works this paper leans on

-

[1]

Alley, M., Biggs, M., Hariss, R., Herrmann, C., Li, M. L., and Perakis, G. (2023). Pricing for heterogeneous products: Analytics for ticket reselling.Manufacturing & Service Operations Management, 25(2):409–426. Baardman, L., Boroujeni, S. B., Cohen-Hillel, T., Panchamgam, K., and Perakis, G. (2023). De- tecting customer trends for optimal promotion targe...

-

[2]

Chen, X., Owen, Z., Pixton, C., and Simchi-Levi, D. (2022). A statistical learning approach to personalization in revenue management.Management Science, 68(3):1923–1937. Dud´ ık, M., Erhan, D., Langford, J., and Li, L. (2014). Doubly robust policy evaluation and optimization.Statistical Science, 29(4):485–511. Elmachtoub, A. N. and Grigas, P. (2022). Smar...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.