Routed Closure: Rethinking Value Capture in Decentralized Ecosystems

Pith reviewed 2026-06-29 20:06 UTC · model grok-4.3

The pith

Decentralized ecosystems require captured value to follow verifiable routes to critical incentive recipients in sufficient amounts, unlike systems with centralized reallocation pools.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

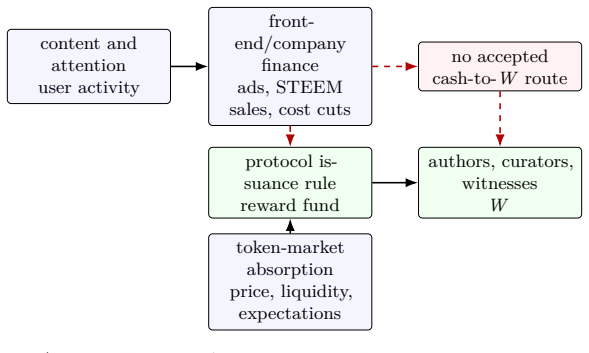

Decentralized ecosystems can capture value yet fail to fund their critical participants because they lack a centralized reallocation pool; therefore captured value must satisfy routed closure by passing through a verifiable route to a specified critical incentive recipient and reaching a level sufficient relative to that recipient's reward requirement. Route-Admissible Value is the formalization of value that meets this condition, operationalized through the External Value Routing Closure protocol. Standard indicators such as protocol revenue, fee collection, token burns, or market capitalization do not establish that this routing and sufficiency have occurred.

What carries the argument

Routed closure, the requirement that captured value must pass through a verifiable route to a specified critical incentive recipient and meet that recipient's reward requirement.

If this is right

- Protocol revenue or fee collection alone cannot be treated as proof that miners, validators, or suppliers receive adequate compensation.

- Token burns or price increases do not substitute for explicit routing of value to the actors whose continued participation keeps the system running.

- Market capitalization or total value locked figures do not indicate whether captured value reaches the specific recipients whose reward requirements must be met.

- Designs that rely on discretionary or centralized redistribution, as in some content platforms, are structurally unavailable in permissionless decentralized settings.

- Evaluation of incentive sustainability must check both the existence of a route and the sufficiency of the amount that travels along it.

Where Pith is reading between the lines

- Designers of new decentralized protocols may need to embed explicit routing checks into token or fee mechanics from the start rather than assuming capture metrics will suffice later.

- Audits of existing chains could apply the routed-closure test to determine whether current reward flows actually reach the participants whose exit would threaten system operation.

- The distinction may extend to non-blockchain decentralized systems where value is generated but distribution depends on voluntary or indirect paths.

- Comparisons across ecosystems could quantify how often standard capture metrics coincide with actual routed closure, producing a clearer map of which designs currently satisfy the condition.

Load-bearing premise

Decentralized systems have no mechanism that can substitute for a centralized reallocation pool when directing captured value to the right participants.

What would settle it

A documented case of a decentralized ecosystem in which fees or token value are captured but never routed to critical participants such as validators or storage providers, yet the system continues to attract and retain those participants at required levels.

Figures

read the original abstract

A decentralized ecosystem can capture value and still fail to fund the actors who keep it running. Users may pay fees, tokens may appreciate, issuers may earn revenue, and protocols may burn value, but none of these facts by itself shows that authors, miners, validators, suppliers, storage providers, or other critical participants are actually compensated. This paper argues that traditional value-capture analysis often assumes a centralized pool: once value is captured, it can be reallocated through budgets, contracts, payroll, or managerial discretion. Decentralized ecosystems do not have this default pool. They require routed closure: captured value must pass through a verifiable route to a specified critical incentive recipient, and it must be sufficient relative to that recipient's reward requirement. We formalize this distinction through Route-Admissible Value and operationalize it with the External Value Routing Closure protocol. A contrast set including YouTube, Steem/Steemit, Bitcoin, Ethereum, Aave, Filecoin, USDC, and XRP shows why revenue, fees, burns, token prices, or market capitalization should not be mistaken for sustainable incentive funding.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims that decentralized ecosystems can capture value (via fees, token appreciation, revenue, or burns) without necessarily compensating critical participants like miners, validators, or storage providers, because they lack the centralized reallocation pool assumed in traditional value-capture analysis. It argues that such systems require 'routed closure,' where captured value must pass through a verifiable route to a specified recipient in sufficient quantity relative to that recipient's needs. The authors introduce Route-Admissible Value and the External Value Routing Closure protocol to formalize and operationalize this distinction, using a contrast set of examples (YouTube, Steem/Steemit, Bitcoin, Ethereum, Aave, Filecoin, USDC, XRP) to show that standard metrics do not guarantee sustainable incentives.

Significance. If the distinction holds and the formalization identifies a genuine structural gap not covered by existing incentive mechanisms, the work could provide a useful conceptual lens for evaluating long-term viability and incentive alignment in decentralized protocols and blockchain systems. The contrast-set approach offers a method to test whether captured value actually reaches the actors maintaining the ecosystem.

major comments (3)

- [Abstract] Abstract: The load-bearing claim that 'decentralized ecosystems do not have this default pool' and therefore require routed closure is asserted rather than derived; the contrast set is invoked to show that revenue/fees/burns do not imply routed closure, yet no explicit mapping of each protocol's payment routes or sufficiency checks against recipient reward requirements is provided, leaving the necessity of new concepts like Route-Admissible Value unanchored.

- [Formalization] Formalization section: The manuscript states that it formalizes the distinction 'through Route-Admissible Value' and operationalizes it with the External Value Routing Closure protocol, but supplies no equations, axioms, definitions, or derivations; without these, it is not possible to verify how the new formalization differs from or improves upon existing direct-routing mechanisms in the cited protocols.

- [Contrast set] Contrast set: The paper concludes that the listed systems (Bitcoin, Ethereum, Filecoin, Aave, etc.) illustrate why common metrics should not be mistaken for sustainable incentive funding, but without concrete analysis showing that their actual routes fail the sufficiency condition for named recipients (miners, validators, storage providers), the structural-problem premise versus existing incentive designs is not substantiated.

minor comments (1)

- [Abstract] Abstract: The inclusion of 'authors' among critical participants is unclear in the context of the decentralized protocols discussed and may confuse readers.

Simulated Author's Rebuttal

We thank the referee for the constructive comments, which highlight areas where the manuscript's claims require stronger anchoring. We address each major point below and commit to revisions that add explicit mappings, formal definitions, and concrete analysis while preserving the paper's conceptual focus.

read point-by-point responses

-

Referee: [Abstract] Abstract: The load-bearing claim that 'decentralized ecosystems do not have this default pool' and therefore require routed closure is asserted rather than derived; the contrast set is invoked to show that revenue/fees/burns do not imply routed closure, yet no explicit mapping of each protocol's payment routes or sufficiency checks against recipient reward requirements is provided, leaving the necessity of new concepts like Route-Admissible Value unanchored.

Authors: We agree the abstract presents the distinction as a premise rather than deriving it step-by-step from the contrast set. In revision we will shorten the abstract's claim and add a clause referencing the body’s contrast-set analysis, while expanding the introduction to include a brief table mapping each example protocol to its primary payment route and a qualitative sufficiency check against named recipients (e.g., miners in Bitcoin). This will anchor the necessity of Route-Admissible Value without lengthening the abstract beyond journal limits. revision: yes

-

Referee: [Formalization] Formalization section: The manuscript states that it formalizes the distinction 'through Route-Admissible Value' and operationalizes it with the External Value Routing Closure protocol, but supplies no equations, axioms, definitions, or derivations; without these, it is not possible to verify how the new formalization differs from or improves upon existing direct-routing mechanisms in the cited protocols.

Authors: The current draft presents the formalization at a descriptive level. We accept that explicit definitions are needed for verifiability. Revision will add a new subsection containing: (1) a set-theoretic definition of Route-Admissible Value as a tuple (route, recipient, quantity, sufficiency predicate); (2) axioms distinguishing it from discretionary reallocation; and (3) a high-level protocol specification for External Value Routing Closure in pseudocode. These will be contrasted with direct-routing examples from the cited protocols to show the incremental contribution. revision: yes

-

Referee: [Contrast set] Contrast set: The paper concludes that the listed systems (Bitcoin, Ethereum, Filecoin, Aave, etc.) illustrate why common metrics should not be mistaken for sustainable incentive funding, but without concrete analysis showing that their actual routes fail the sufficiency condition for named recipients (miners, validators, storage providers), the structural-problem premise versus existing incentive designs is not substantiated.

Authors: The contrast set is currently illustrative. We will revise by adding, for each protocol, a short paragraph or table entry that (a) identifies the verifiable route(s) to the named recipient and (b) notes whether publicly observable data or protocol rules satisfy or fail the sufficiency condition relative to that recipient’s documented reward requirement. Where data are incomplete we will flag the limitation rather than over-claim. This strengthens the structural distinction without converting the paper into an empirical survey. revision: partial

Circularity Check

Central distinction between centralized pools and decentralized 'routed closure' is asserted by definition rather than derived from explicit mapping of existing protocol routes.

specific steps

-

self definitional

[Abstract]

"Decentralized ecosystems do not have this default pool. They require routed closure: captured value must pass through a verifiable route to a specified critical incentive recipient, and it must be sufficient relative to that recipient's reward requirement."

The absence of a centralized pool is stipulated as the defining property of decentralized systems; routed closure is then introduced as the required property whose definition exactly supplies what the stipulation says is missing. The 'requirement' is therefore true by the paper's own framing rather than shown via external analysis of payment flows in the listed protocols.

full rationale

The paper's core argument proceeds by defining decentralized systems as lacking a default reallocation pool and then stating that they therefore require routed closure (with the new formalization of Route-Admissible Value following directly from that definition). No equations, fitted parameters, or self-citations appear in the provided text. The contrast set is invoked to illustrate the gap, but the necessity claim reduces to the initial definitional premise without an independent demonstration that existing direct-routing mechanisms (staking, fee splits, burns to validators) fail the sufficiency check. This produces moderate circularity confined to the problem-statement step; the remainder of the paper is a conceptual proposal rather than a derivation that collapses to its inputs.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Decentralized ecosystems lack a default centralized pool for value reallocation through budgets or managerial discretion.

invented entities (2)

-

Route-Admissible Value

no independent evidence

-

External Value Routing Closure protocol

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Amit, R., and C. Zott. 2001. Value creation in e-business.Strategic Management Journal 22(6–7):493–520.https://doi.org/10.1002/smj.187

-

[2]

Budish, E. 2018. The economic limits of Bitcoin and the blockchain.NBER Working Paper No. 24717.https://doi.org/10.3386/w24717. 12

-

[3]

Catalini, C., A. de Gortari, and N. Shah. 2022. Some simple economics of stablecoins. Annual Review of Financial Economics14:117–135.https://doi.org/10.1146/annure v-financial-111621-101151

-

[4]

Cong, L. W., Y. Li, and N. Wang. 2021. Tokenomics: Dynamic adoption and valuation.The Review of Financial Studies34(3):1105–1155.https://doi.org/10.1093/rfs/hhaa089

-

[5]

O’Hara, and S

Easley, D., M. O’Hara, and S. Basu. 2019. From mining to markets: The evolution of bitcoin transaction fees.Journal of Financial Economics134(1):91–109.https://doi.org/10.1 016/j.jfineco.2019.03.004

2019

-

[6]

Gorton, G. B., and J. Y. Zhang. 2023. Taming wildcat stablecoins.University of Chicago Law Review90:909.https://doi.org/10.2139/ssrn.3888752

-

[7]

Huberman, G., J. D. Leshno, and C. C. Moallemi. 2021. Monopoly without a monopolist: An economic analysis of the Bitcoin payment system.The Review of Economic Studies 88(6):3011–3040.https://doi.org/10.1093/restud/rdab014

-

[8]

Jacobides, M. G., C. Cennamo, and A. Gawer. 2018. Towards a theory of ecosystems. Strategic Management Journal39(8):2255–2276.https://doi.org/10.1002/smj.2904

-

[9]

Kiayias, A., B. Livshits, A. Monteoliva Mosteiro, and O. S. Thyfronitis Litos. 2019. A puff of Steem: Security analysis of decentralized content curation.OASIcs Tokenomics 2019. https://doi.org/10.4230/OASIcs.Tokenomics.2019.3

-

[10]

Kim, M. S., and J. Y. Chung. 2019. Sustainable growth and token economy design: The case of Steemit.Sustainability11(1):167.https://doi.org/10.3390/su11010167

-

[11]

Li, C., and B. Palanisamy. 2019. Incentivized blockchain-based social media platforms: A case study of Steemit.Proceedings of WebSci ’19.https://doi.org/10.1145/3292522.33 26041

-

[12]

Li, C., B. Palanisamy, R. Xu, J. Xu, and J. Wang. 2021. SteemOps: Extracting and analyzing key operations in Steemit blockchain-based social media platform.Proceedings of CODASPY ’21.https://doi.org/10.1145/3422337.3447845

-

[13]

Liu, Z., Y. Li, Q. Min, and M. Chang. 2022. User incentive mechanism in blockchain-based online community: An empirical study of Steemit.Information & Management59(7):103596. https://doi.org/10.1016/j.im.2022.103596

-

[14]

Monegro, J. 2016. Fat protocols.Union Square Ventures.https://www.usv.com/writing/ 2016/08/fat-protocols/

2016

- [15]

-

[16]

Schär, F. 2021. Decentralized finance: On blockchain- and smart contract-based financial markets.Federal Reserve Bank of St. Louis Review103(2):153–174.https://doi.org/10 .20955/r.103.153-74

2021

-

[17]

Teece, D. J. 2010. Business models, business strategy and innovation.Long Range Planning 43(2–3):172–194.https://doi.org/10.1016/j.lrp.2009.07.003

-

[18]

Tokenomics.com. 2025. Value creation, value capture and value accrual.https://tokeno mics.com/articles/tokenomics-value-capture. 13

2025

-

[19]

Weking, J., M. Mandalenakis, A. Hein, S. Hermes, M. Böhm, and H. Krcmar. 2020. The impact of blockchain technology on business models: A taxonomy and archetypal patterns. Electronic Markets30(2):285–305.https://doi.org/10.1007/s12525-019-00386-3

-

[20]

GoodDollar. 2026. Architecture and value flow.GoodDocs.https://docs.gooddollar.or g/how-gooddollar-works/architecture-and-value-flow. 14

2026

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.