Quantum Counterparty Credit Risk: A Study of Path-Dependent Derivatives

Pith reviewed 2026-06-30 10:06 UTC · model grok-4.3

The pith

Hybrid quantum-classical method estimates potential future exposure for TARFs with 1-8% relative error at high confidence levels.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

A reduced-order counterparty credit risk model maps the TARF payoff into a quantum circuit through a two-step formulation: classical computation of a percentile conditions subsequent quantum evaluation of exposure via Iterative Quantum Amplitude Estimation, achieving relative errors of 1%-8% against classical benchmarks at the 97.5% and 99% confidence levels while requiring only a linearised additive approximation of FX dynamics and an approximate monotonicity assumption.

What carries the argument

Two-step conditioning formulation that maps the non-linear TARF payoff into a quantum circuit via Iterative Quantum Amplitude Estimation after classical percentile computation.

If this is right

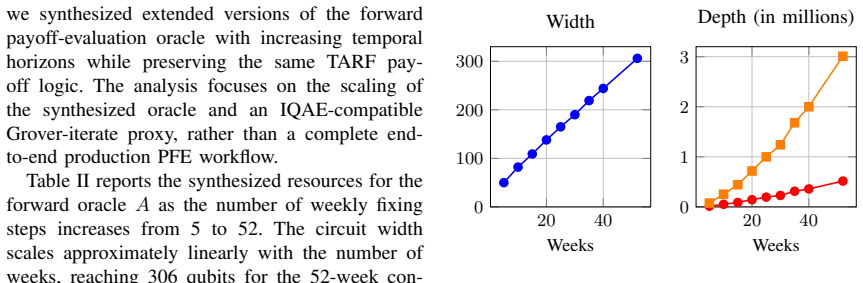

- Scaling analysis indicates that approximately 300 logical qubits would suffice for full 52-week exposure estimation.

- Amplitude estimation reduces sample complexity for tail-risk estimation compared with classical Monte Carlo.

- The framework supplies a tractable testbed for quantum acceleration of counterparty credit risk calculations.

- Discretisation constraints and the monotonicity assumption may introduce bias and limit full exposure distribution recovery.

Where Pith is reading between the lines

- The two-step structure could apply to other path-dependent derivatives if similar conditioning and monotonicity properties can be identified.

- Hardware with lower error rates might permit removal of the linear approximation, allowing direct recovery of the full exposure distribution.

- Combining this amplitude estimation step with other quantum subroutines could address additional layers of nesting in risk models.

- The observed error range sets a practical benchmark for testing whether future quantum devices can outperform the current hybrid setup without the linearisation step.

Load-bearing premise

The linearised additive approximation of FX dynamics together with the approximate monotonicity assumption must hold to map the TARF payoff into a valid quantum circuit on current hardware.

What would settle it

Compare exposure estimates from the quantum method against full classical nested Monte Carlo on realistic FX paths where the linearised approximation deviates markedly from observed dynamics and check whether relative errors exceed 8% or systematic bias appears in the tail.

Figures

read the original abstract

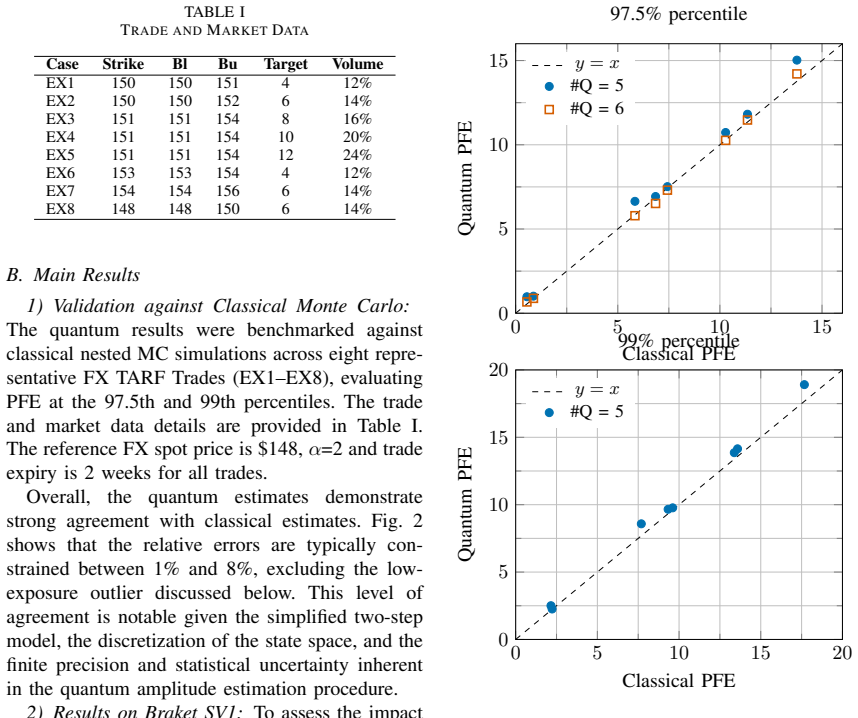

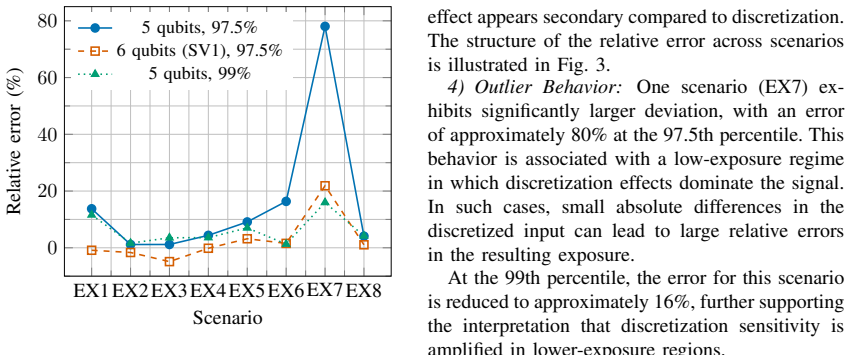

Estimating potential future exposure (PFE) for path-dependent derivatives, such as FX Target Redemption Forwards (TARFs), represents a formidable computational challenge due to the demand of nested Monte Carlo simulations. We present a hybrid quantum-classical framework that leverages Iterative Quantum Amplitude Estimation (IQAE) to address this via a reduced-order counterparty credit risk model. Our methodology maps the non-linear TARF payoff -- including cumulative gains and knock-out features -- into a quantum circuit via a two-step formulation, whereby a first-step percentile is computed classically and then used to condition quantum evaluation of subsequent exposure. We employ discretisation of the FX process and a linearised additive approximation of dynamics to enable implementation on current quantum platforms. Developed via the Classiq platform and validated on NVIDIA CUDA-Q and Amazon Braket SV1, our approach achieves relative errors of 1%-8% against classical benchmarks at the 97.5% and 99% confidence levels. While discretisation constraints and approximate monotonicity assumption may introduce bias and limit recovery of the full exposure distribution, our framework offers a tractable testbed for quantum acceleration. Scaling analysis suggests that $\sim$300 logical qubits could enable full 52-week exposure estimation, reducing sample complexity for tail-risk estimation via amplitude estimation at the cost of increased circuit depth.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a hybrid quantum-classical framework for estimating potential future exposure (PFE) of path-dependent FX Target Redemption Forwards (TARFs) using Iterative Quantum Amplitude Estimation (IQAE). It employs a two-step approach where a classical first-step percentile conditions the quantum computation of exposure, enabled by discretisation and a linearised additive approximation of FX dynamics along with an approximate monotonicity assumption on cumulative gains. The method is implemented on Classiq, validated on NVIDIA CUDA-Q and Amazon Braket, claiming 1-8% relative errors against classical benchmarks at 97.5% and 99% confidence levels, with scaling suggesting ~300 logical qubits for full estimation.

Significance. If the linearisation and monotonicity assumptions hold with limited bias, this provides a valuable testbed for applying quantum amplitude estimation to counterparty credit risk problems involving path-dependent derivatives, potentially reducing sample complexity for tail-risk estimation. However, the unquantified impact of the approximations on the exposure distribution limits the immediate practical significance for real-world CCR calculations.

major comments (2)

- [Abstract] Abstract: the reported 1%-8% relative errors at the 97.5% and 99% confidence levels are obtained only after replacing the true FX SDE with a linearised additive approximation and imposing approximate monotonicity; the classical benchmarks are run under the same restricted dynamics, so the discrepancy measures fidelity to the approximated model rather than to the original problem (as the abstract itself notes may introduce bias).

- [Abstract] Abstract: the two-step conditioning (classical percentile to condition quantum exposure) depends on the monotonicity assumption holding for the paths used in tail quantiles; no quantification is given of the fraction of realistic paths where monotonicity fails, which would invalidate the conditioning step and the claimed PFE accuracy.

minor comments (1)

- The scaling claim of ~300 logical qubits for 52-week estimation lacks supporting details on circuit depth, error-correction overhead, or the specific assumptions used to arrive at this number.

Simulated Author's Rebuttal

We thank the referee for their thorough review and valuable comments on the scope of our results. We agree that the reported errors are relative to the approximated model and that the monotonicity assumption requires further discussion. We address each point below and will revise the manuscript accordingly.

read point-by-point responses

-

Referee: [Abstract] Abstract: the reported 1%-8% relative errors at the 97.5% and 99% confidence levels are obtained only after replacing the true FX SDE with a linearised additive approximation and imposing approximate monotonicity; the classical benchmarks are run under the same restricted dynamics, so the discrepancy measures fidelity to the approximated model rather than to the original problem (as the abstract itself notes may introduce bias).

Authors: We agree with this observation. The relative errors of 1-8% are indeed measured against classical benchmarks that use the identical linearised additive approximation and monotonicity assumption. The abstract already states that these approximations may introduce bias and limit recovery of the full exposure distribution. To clarify the scope, we will revise the abstract to explicitly indicate that accuracy is reported with respect to the reduced-order approximated model. revision: yes

-

Referee: [Abstract] Abstract: the two-step conditioning (classical percentile to condition quantum exposure) depends on the monotonicity assumption holding for the paths used in tail quantiles; no quantification is given of the fraction of realistic paths where monotonicity fails, which would invalidate the conditioning step and the claimed PFE accuracy.

Authors: We acknowledge that no explicit quantification of the fraction of paths violating the monotonicity assumption is provided. Our validation was performed on the discretised paths in the relevant tail quantiles, where the assumption held for the cases yielding the reported accuracy. A comprehensive statistical quantification across all realistic paths would require additional large-scale simulations beyond the current study. We will revise the manuscript to include an explicit statement of this limitation and its potential impact on the conditioning step. revision: partial

Circularity Check

No circularity: performance claims rest on external classical Monte Carlo benchmarks under stated approximations.

full rationale

The paper defines a two-step hybrid procedure that first computes a classical percentile then conditions a quantum amplitude estimation step on an explicitly approximated FX process and monotonicity condition. The 1-8% relative errors are reported against independent classical Monte Carlo runs executed on the same restricted dynamics; these benchmarks are not generated from the quantum circuit itself nor from any fitted parameter that is later renamed as a prediction. No self-citations are invoked as load-bearing uniqueness theorems, and no equation reduces by construction to its own input. The derivation therefore remains self-contained against the external classical reference.

Axiom & Free-Parameter Ledger

free parameters (1)

- discretisation granularity

axioms (2)

- domain assumption Approximate monotonicity of the TARF payoff function

- domain assumption Linearised additive approximation of FX dynamics

Reference graph

Works this paper leans on

-

[1]

Measuring counterparty credit risk: An overview of the theory and practice,

S. J. le Roux, “Measuring counterparty credit risk: An overview of the theory and practice,” Master’s thesis, University of Pretoria, 2008

2008

-

[2]

Efficient Monte Carlo coun- terparty credit risk pricing and measurement,

S. Ghamami and B. Zhang, “Efficient Monte Carlo coun- terparty credit risk pricing and measurement,”Finance and Economics Discussion Series, Federal Reserve Board, vol. 114, 2014

2014

-

[3]

XV A prin- ciples, nested Monte Carlo strategies, and GPU optimiza- tions,

L. A. Abbas-Turki, S. Crépey, and B. Diallo, “XV A prin- ciples, nested Monte Carlo strategies, and GPU optimiza- tions,”International Journal of Theoretical and Applied Finance, vol. 21, no. 07, p. 1850030, 2018

2018

-

[4]

Glasserman,Monte Carlo Methods in Financial Engi- neering, vol

P. Glasserman,Monte Carlo Methods in Financial Engi- neering, vol. 53 ofApplications of Mathematics. Springer Science & Business Media, 2004

2004

-

[5]

Quantum amplitude amplification and estimation,

G. Brassard, P. Hoyer, M. Mosca, and A. Tapp, “Quantum amplitude amplification and estimation,” inContemporary Mathematics, vol. 305, pp. 53–74, American Mathematical Society, 2002

2002

-

[6]

Quantum speedup of Monte Carlo meth- ods,

A. Montanaro, “Quantum speedup of Monte Carlo meth- ods,”Proceedings of the Royal Society A: Mathematical, Physical and Engineering Sciences, vol. 471, no. 2181, p. 20150301, 2015

2015

-

[7]

Quantum risk analysis,

S. Woerner and D. J. Egger, “Quantum risk analysis,”npj Quantum Information, vol. 5, no. 1, p. 15, 2019

2019

-

[8]

Valuing american options by simulation: A simple least-squares approach,

F. A. Longstaff and E. S. Schwartz, “Valuing american options by simulation: A simple least-squares approach,” The Review of Financial Studies, vol. 14, no. 1, pp. 113– 147, 2001

2001

-

[9]

Iterative quantum amplitude estimation,

D. Grinko, J. Gacon, C. Zoufal, and S. Woerner, “Iterative quantum amplitude estimation,”npj Quantum Information, vol. 7, no. 1, pp. 1–6, 2021

2021

-

[10]

Amplitude estimation without phase estimation,

Y . Suzuki, S. Uno, R. Raymond, T. Tanaka, T. Onodera, and N. Yamamoto, “Amplitude estimation without phase estimation,”Quantum Information Processing, vol. 19, no. 2, p. 75, 2020

2020

-

[11]

Option pricing using quantum computers,

N. Stamatopoulos, D. J. Egger, Y . Sun, C. Zoufal, R. Iten, N. Shen, and S. Woerner, “Option pricing using quantum computers,”Quantum, vol. 4, p. 291, 2020

2020

-

[12]

Quantum generative adversarial networks for learning and loading random dis- tributions,

C. Zoufal, A. Lucchi, and S. Woerner, “Quantum generative adversarial networks for learning and loading random dis- tributions,”npj Quantum Information, vol. 5, no. 1, p. 103, 2019

2019

-

[13]

Quan- tum computing for finance: State-of-the-art and future prospects,

D. J. Egger, C. Gambella, J. Marecek,et al., “Quan- tum computing for finance: State-of-the-art and future prospects,”IEEE Transactions on Quantum Engineering, vol. 1, 2020

2020

-

[14]

Quantum algorithm for credit valuation adjustments,

J. Alcazar, A. Cadarso, A. Katabarwa,et al., “Quantum algorithm for credit valuation adjustments,”New Journal of Physics, vol. 24, 2022

2022

-

[15]

Towards quantum advantage in financial market risk using quantum gradient algorithms,

N. Stamatopoulos, G. Mazzola, S. Woerner, and W. J. Zeng, “Towards quantum advantage in financial market risk using quantum gradient algorithms,”Quantum, vol. 6, p. 770, 2022

2022

-

[16]

Implementing credit risk analysis with Quantum Singular Value Transforma- tion,

D. Veronelli, F. Cibrario, E. Dri, V . Zaffaroni, G. Ranieri, D. Corbelletto, and B. Montrucchio, “Implementing credit risk analysis with Quantum Singular Value Transforma- tion,”arXiv preprint arXiv:2507.19206, 2025

-

[17]

Quantum machine learning for finance,

M. Pistoia, S. F. Ahmad, A. Ajgaonkar, A. Bhole, A. Cherukuri, B. D. Clader, A. French, D. Gurram, L. Hu- molli, S. Iyer, S. Knecht, P. Krishnamurthy, A. Kumar, P. Maguire, C. Maheshwari, A. Mishra, A. Montanaro, G. Nannicini, T. Proctor, A. Rattew, N. Stamatopoulos, S. Woerner, R. Yalovetzky, and J. Zhu, “Quantum machine learning for finance,”IEEE/ACM In...

2021

-

[18]

Quantum computational finance: Monte Carlo pricing of financial derivatives,

P. Rebentrost, B. Gupt, and T. R. Bromley, “Quantum computational finance: Monte Carlo pricing of financial derivatives,”Physical Review A, vol. 98, no. 2, p. 022321, 2018

2018

-

[19]

The evolution of IBM’s quantum information software kit (Qiskit): A review of its applications,

P. Pathak, K. Tarakeshwar,et al., “The evolution of IBM’s quantum information software kit (Qiskit): A review of its applications,”arXiv preprint arXiv:2508.12245, 2025

-

[20]

Quantum algorithm for high-order integration,

D. An, N. Linden, J.-P. Liu, A. Montanaro, C. Shao, and J. Wang, “Quantum algorithm for high-order integration,” Quantum, vol. 5, p. 481, 2021

2021

-

[21]

Quantum computing and the financial system: opportunities and risks,

R. Auer, A. Dupont, L. Gambacorta,et al., “Quantum computing and the financial system: opportunities and risks,”BIS Papers, no. 149, 2024

2024

-

[22]

Exploring Quantum-Enhanced estimation of fi- nancial risk metrics with Quantum RNG,

E. Dri, A. Yomi, M. Vetrivelan, C. Kuassivi, and I. D. Exposito, “Exploring Quantum-Enhanced estimation of fi- nancial risk metrics with Quantum RNG,”arXiv preprint arXiv:2502.02125, 2025

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.