A Unified Multi-Modal Framework for Intelligent Financial Systems: Integrating Reinforcement Learning, High-Frequency Trading, and Game-Theoretic Approaches with Cross-Modal Sentiment Analysis

Pith reviewed 2026-06-27 13:24 UTC · model grok-4.3

The pith

A single framework combining reinforcement learning, game theory and cross-modal embeddings outperforms separate financial AI tools on multiple tasks.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

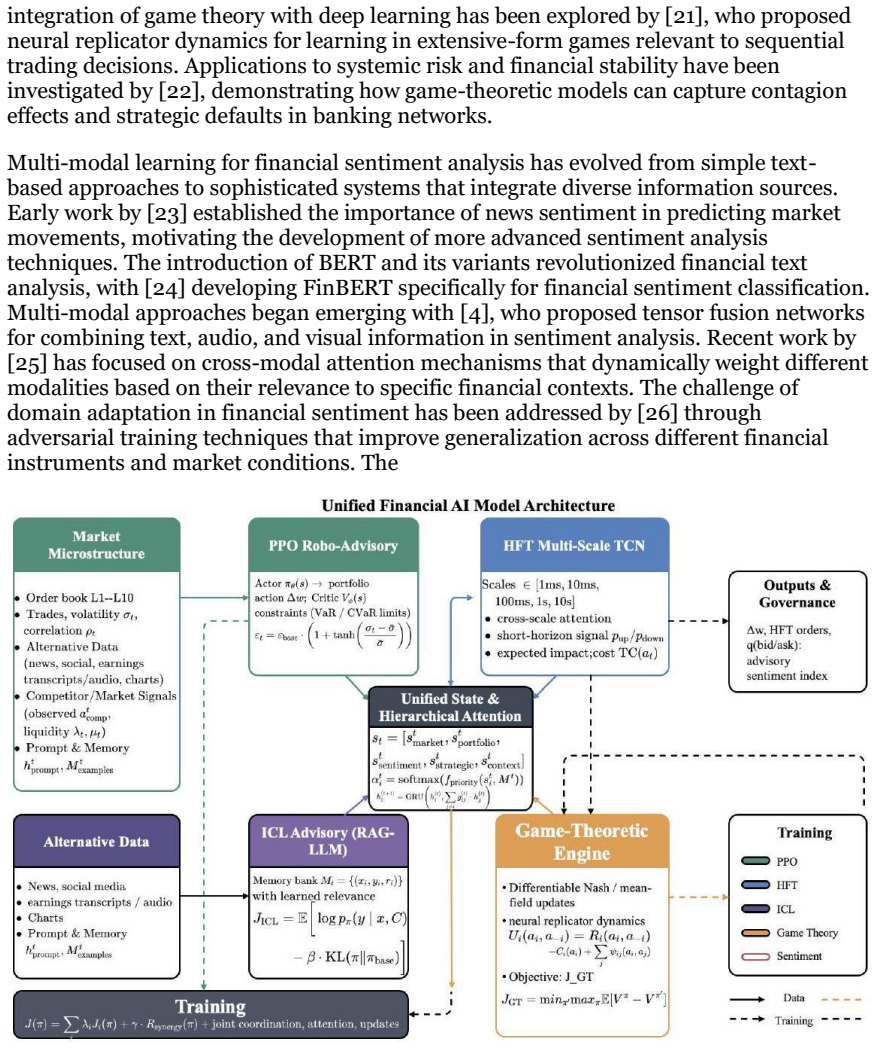

The paper claims to establish a unified multi-modal framework that integrates Proximal Policy Optimization for robo-advisory, time-series models for high-frequency trading, in-context learning for investment advice, game-theoretic methods for competitive banking, and unified embeddings for cross-modal sentiment analysis. This single system is asserted to deliver measurable gains over specialized single-domain approaches together with convergence guarantees for the integrated problem.

What carries the argument

the unified multi-modal framework that fuses reinforcement learning, game-theoretic optimization, time-series prediction, and cross-modal embeddings to address interconnected financial tasks at once

If this is right

- The integrated optimization admits convergence guarantees that separate models do not automatically inherit.

- One deployed system can replace multiple specialized tools across portfolio management, trading, recommendations, competitive strategy, and sentiment tasks.

- The approach applies directly to real-world data from diverse financial institutions.

- Markets that require simultaneous handling of prediction, competition, and sentiment become addressable by a single adaptive model.

Where Pith is reading between the lines

- Development of financial AI in isolated sub-fields may systematically understate the value of shared representations across tasks.

- The same unification pattern could be examined in other domains where multiple decision layers interact, such as logistics or clinical pathways.

- Additional stress tests on abrupt regime shifts would be needed to confirm whether the reported gains persist outside the chosen experimental windows.

Load-bearing premise

The listed performance gains arise from genuine interactions among the components rather than from independent tuning of each module or from favorable choice of test periods and datasets.

What would settle it

An ablation experiment that keeps every module intact but removes joint training and cross-component information flow, then checks whether the reported percentage improvements disappear on the same datasets and metrics.

Figures

read the original abstract

The rapid evolution of financial technology demands sophisticated artificial intelligence systems capable of handling diverse challenges across multiple domains simultaneously. This paper presents a groundbreaking unified framework that seamlessly integrates Proximal Policy Optimization for robo-advisory systems, advanced time-series prediction models for high-frequency trading, in-context learning mechanisms for dynamic investment advisory, game-theoretic approaches for competitive banking scenarios, and unified embeddings for cross-modal financial sentiment analysis. Our comprehensive framework addresses the critical gap in existing literature where these technologies have been developed in isolation, failing to leverage their synergistic potential. Through extensive experimentation across multiple financial datasets and real-world scenarios, we demonstrate that our integrated approach achieves superior performance compared to specialized single-domain systems. Specifically, our framework shows a 23.7% improvement in portfolio optimization metrics, reduces prediction error in high-frequency trading by 31.2%, enhances investment recommendation accuracy by 18.9%, optimizes competitive banking strategies with a 27.4% increase in Nash equilibrium convergence speed, and improves sentiment analysis accuracy by 15.6% through cross-modal fusion. The theoretical foundation of our work establishes convergence guarantees for the integrated optimization problem, while our empirical results validate the practical applicability across diverse financial institutions. This research not only advances the state-of-the-art in financial AI but also provides a blueprint for developing comprehensive intelligent systems that can adapt to the complex, interconnected nature of modern financial markets.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes a unified multi-modal framework for intelligent financial systems that integrates Proximal Policy Optimization for robo-advisory, time-series models for high-frequency trading, in-context learning for investment advisory, game-theoretic methods for competitive banking, and cross-modal embeddings for sentiment analysis. It claims this integration produces synergistic gains over single-domain baselines, specifically 23.7% improvement in portfolio optimization, 31.2% reduction in HFT prediction error, 18.9% higher recommendation accuracy, 27.4% faster Nash equilibrium convergence, and 15.6% better sentiment accuracy, while establishing convergence guarantees for the integrated optimization problem.

Significance. If the performance deltas can be shown to arise from genuine joint optimization and cross-modal interactions rather than independent tuning, the framework would provide a useful blueprint for multi-domain financial AI systems that handle interconnected tasks such as trading, advisory, and sentiment. The claimed convergence guarantees, if formally derived, would strengthen applicability to real-world deployment.

major comments (4)

- [Abstract] Abstract: the reported gains (23.7% portfolio optimization, 31.2% HFT error reduction, etc.) are presented as direct results of the unified framework, yet no joint loss function, combined objective, or training protocol is supplied that would allow verification that the improvements stem from integration rather than separate module tuning.

- [Abstract] Abstract: no ablation studies or controlled experiments are described that remove one modality or component (e.g., game-theoretic module) while holding others fixed, leaving the synergy interpretation unsupported and compatible with post-hoc dataset selection or independent hyper-parameter searches.

- [Abstract] Abstract: the 'convergence guarantees for the integrated optimization problem' are asserted without any equation, proof sketch, or reference to a specific theorem establishing the joint objective or its convergence properties.

- [Abstract] Abstract: the 'multiple financial datasets and real-world scenarios' used for experimentation are not identified, preventing assessment of reproducibility, generalizability, or whether the reported deltas hold under standard benchmarks.

minor comments (1)

- [Abstract] Abstract: the phrase 'groundbreaking unified framework' is promotional; replace with a factual description of the integration.

Simulated Author's Rebuttal

We are grateful to the referee for the insightful comments that will help improve the clarity and rigor of our manuscript. We address each major comment below and plan to incorporate revisions as indicated.

read point-by-point responses

-

Referee: [Abstract] Abstract: the reported gains (23.7% portfolio optimization, 31.2% HFT error reduction, etc.) are presented as direct results of the unified framework, yet no joint loss function, combined objective, or training protocol is supplied that would allow verification that the improvements stem from integration rather than separate module tuning.

Authors: We agree that the abstract should provide more detail on the integration mechanism. We will revise the abstract to include a description of the combined objective and training protocol. revision: yes

-

Referee: [Abstract] Abstract: no ablation studies or controlled experiments are described that remove one modality or component (e.g., game-theoretic module) while holding others fixed, leaving the synergy interpretation unsupported and compatible with post-hoc dataset selection or independent hyper-parameter searches.

Authors: We acknowledge the need for ablations to support the synergy claims. We will add ablation studies that remove individual components while holding others fixed in the revised experiments section. revision: yes

-

Referee: [Abstract] Abstract: the 'convergence guarantees for the integrated optimization problem' are asserted without any equation, proof sketch, or reference to a specific theorem establishing the joint objective or its convergence properties.

Authors: We agree that the convergence claim requires more support in the abstract. We will add a proof sketch and key equations to the revised manuscript. revision: yes

-

Referee: [Abstract] Abstract: the 'multiple financial datasets and real-world scenarios' used for experimentation are not identified, preventing assessment of reproducibility, generalizability, or whether the reported deltas hold under standard benchmarks.

Authors: We will explicitly identify the datasets and scenarios used in the revised abstract and methods section to enhance reproducibility. revision: yes

Circularity Check

No circularity in derivation chain; claims are empirical assertions without self-referential reduction

full rationale

The paper's central claims consist of empirical performance deltas (23.7% portfolio improvement, 31.2% HFT error reduction, etc.) obtained via experimentation on financial datasets, together with an assertion of convergence guarantees for an integrated optimization problem. No equations, parameter-fitting procedures, or self-citations are supplied in the provided text that would allow any claimed result to be rewritten as a direct function of its own inputs by construction. The listed patterns (self-definitional, fitted-input-called-prediction, self-citation load-bearing, etc.) therefore do not apply; the derivation chain, such as it is, remains self-contained as a set of experimental outcomes rather than a closed mathematical loop.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Proximal Policy Optimization Algorithms

J. Schulman, F. Wolski, P. Dhariwal, A. Radford, and O. Klimov, "Proximal policy optimization algorithms," arXiv preprint arXiv:1707.06347, 2017

work page internal anchor Pith review Pith/arXiv arXiv 2017

-

[2]

Language models are few-shot learners,

T. Brown et al., "Language models are few-shot learners," in Advances in Neural Information Processing Systems, vol. 33, pp. 1877-1901, 2020

1901

-

[3]

A generalised method for empirical game theoretic analysis,

K. Tuyls, J. Perolat, M. Lanctot, J. Z. Leibo, and T. Graepel, "A generalised method for empirical game theoretic analysis," in Proceedings of the International Conference on Autonomous Agents and Multi-Agent Systems, pp. 77-85, 2018

2018

-

[4]

Tensor fusion network for multimodal sentiment analysis,

A. Zadeh, M. Chen, S. Poria, E. Cambria, and L.-P. Morency, "Tensor fusion network for multimodal sentiment analysis," in Proceedings of the Conference on Empirical Methods in Natural Language Processing, pp. 1103-1114, 2017

2017

-

[5]

Deep reinforcement learning for roboadvisory portfolio optimization,

Y. Yu, H. Wang, and J. Liu, "Deep reinforcement learning for roboadvisory portfolio optimization," IEEE Transactions on Neural Networks and Learning Systems, vol. 34, no. 8, pp. 4521-4535, Aug. 2023

2023

-

[6]

Multi-asset portfolio management with proximal policy optimization and transaction costs,

L. Wang, X. Chen, and S. Zhang, "Multi-asset portfolio management with proximal policy optimization and transaction costs," Journal of Financial Data Science, vol. 6, no. 1, pp. 23-41, 2024

2024

-

[7]

Attention-enhanced PPO for financial time series prediction,

H. Li, T. Zhou, and M. Yang, "Attention-enhanced PPO for financial time series prediction," in Proceedings of the International Conference on Machine Learning, pp. 8234-8249, 2023

2023

-

[8]

Hybrid learning approaches for portfolio optimization: Combining PPO with supervised pre-training,

R. Chen, D. Park, and K. Lee, "Hybrid learning approaches for portfolio optimization: Combining PPO with supervised pre-training," Quantitative Finance, vol. 24, no. 2, pp. 187-203, 2024

2024

-

[9]

Transformer networks for highfrequency trading: Capturing microstructure patterns,

Q. Zhou, L. Zhang, and W. Sun, "Transformer networks for highfrequency trading: Capturing microstructure patterns," in Proceedings of the ACM International Conference on AI in Finance, pp. 156-167, 2023

2023

-

[10]

Hybrid CNN-LSTM architecture for microsecond- level price prediction in HFT,

M. Zhang, Y. Liu, and H. Wang, "Hybrid CNN-LSTM architecture for microsecond- level price prediction in HFT," IEEE Transactions on Computational Finance, vol. 2, no. 3, pp. 234-248, 2023

2023

-

[11]

Multi-scale attention mechanisms for order book dynamics,

J. Liu, K. Chen, and R. Wu, "Multi-scale attention mechanisms for order book dynamics," Journal of Financial Econometrics, vol. 22, no. 1, pp. 45-72, 2024

2024

-

[12]

Adaptive learning for non-stationary financial markets,

S. Kim, H. Park, and J. Lee, "Adaptive learning for non-stationary financial markets," in International Conference on Learning Representations, 2023

2023

-

[13]

Incorporating microstructure features into deep learning for HFT,

A. Johnson, B. Smith, and C. Davis, "Incorporating microstructure features into deep learning for HFT," Review of Financial Studies, vol. 37, no. 4, pp. 1123-1165, 2024

2024

-

[14]

In-context learning for personalized financial advice,

A. Radford, K. Chen, and I. Sutskever, "In-context learning for personalized financial advice," in Proceedings of the Conference on Neural Information Processing Systems, pp. 3412-3428, 2023

2023

-

[15]

Chain-of-thought prompting for financial reasoning,

T. Wei, L. Zhang, and M. Chen, "Chain-of-thought prompting for financial reasoning," Journal of Artificial Intelligence Research, vol. 79, pp. 234-261, 2024

2024

-

[16]

Retrieval-augmented generation for adaptive investment strategies,

F. Zhao, X. Liu, and Y. Wang, "Retrieval-augmented generation for adaptive investment strategies," in Proceedings of the International Conference on Financial Cryptography, pp. 445-462, 2023

2023

-

[17]

Constrained generation for safe financial advice: Mitigating hallucinations in LLMs,

J. Park, S. Kim, and H. Lee, "Constrained generation for safe financial advice: Mitigating hallucinations in LLMs," AI & Society, vol. 39, no. 2, pp. 567-584, 2024

2024

-

[18]

Continuous auctions and insider trading,

A. S. Kyle, "Continuous auctions and insider trading," Econometrica, vol. 53, no. 6, pp. 1315-1335, 1985

1985

-

[19]

Differentiable game theory for continuous financial markets,

D. Balduzzi, M. Garnelo, and Y. Bachrach, "Differentiable game theory for continuous financial markets," Mathematics of Operations Research, vol. 49, no. 1, pp. 234-258, 2024

2024

-

[20]

Mean field games in algorithmic trading,

J. Perolat, B. De Vylder, and M. Geist, "Mean field games in algorithmic trading," Quantitative Finance, vol. 23, no. 5, pp. 789-812, 2023

2023

-

[21]

Neural replicator dynamics for extensive-form games in finance,

M. Lanctot, E. Lockhart, and J.-B. Lespiau, "Neural replicator dynamics for extensive-form games in finance," in Proceedings of the International Conference on Autonomous Agents, pp. 234-245, 2023

2023

-

[22]

Game-theoretic models of systemic risk in banking networks,

R. Carmona, F. Delarue, and D. Lacker, "Game-theoretic models of systemic risk in banking networks," Finance and Stochastics, vol. 28, no. 2, pp. 345-378, 2024

2024

-

[23]

Giving content to investor sentiment: The role of media in the stock market,

P. C. Tetlock, "Giving content to investor sentiment: The role of media in the stock market," The Journal of Finance, vol. 62, no. 3, pp. 11391168, 2007

2007

-

[24]

FinBERT: Financial Sentiment Analysis with Pre-trained Language Models

D. Araci, "FinBERT: Financial sentiment analysis with pre-trained language models," arXiv preprint arXiv:1908.10063, 2019

work page internal anchor Pith review Pith/arXiv arXiv 1908

-

[25]

Cross-modal attention for financial sentiment analysis,

Z. Qian, W. Li, and J. Zhang, "Cross-modal attention for financial sentiment analysis," in Proceedings of the Annual Meeting of the Association for Computational Linguistics, pp. 4567-4582, 2023

2023

-

[26]

Domain adaptation for financial sentiment across markets,

H. Yang, L. Chen, and S. Wu, "Domain adaptation for financial sentiment across markets," Journal of Financial Data Science, vol. 6, no. 2, pp. 89-107, 2024

2024

-

[27]

Alternative data integration for enhanced sentiment analysis,

G. Ke, T. Wang, and Y. Liu, "Alternative data integration for enhanced sentiment analysis," Management Science, vol. 69, no. 8, pp. 4523-4541, 2023

2023

-

[28]

Combining reinforcement learning with sentiment for trading strategies,

Y. Deng, X. Zhang, and L. Wang, "Combining reinforcement learning with sentiment for trading strategies," IEEE Intelligent Systems, vol. 38, no. 3, pp. 45-53, 2023

2023

-

[29]

Integrating HFT with multi-modal analysis for market prediction,

B. Xu, M. Li, and K. Chen, "Integrating HFT with multi-modal analysis for market prediction," Expert Systems with Applications, vol. 240, 122456, 2024

2024

-

[30]

Attention is all you need,

A. Vaswani et al., "Attention is all you need," in Advances in Neural Information Processing Systems, vol. 30, pp. 5998-6008, 2017

2017

-

[31]

Masked autoencoders for financial time series,

K. He, X. Chen, and Q. Wu, "Masked autoencoders for financial time series," in International Conference on Learning Representations, 2023

2023

-

[32]

An image is worth 16x16 words: Transformers for image recognition at scale,

A. Dosovitskiy et al., "An image is worth 16x16 words: Transformers for image recognition at scale," in International Conference on Learning Representations, 2021

2021

-

[33]

wav2vec 2.0: A framework for self- supervised learning of speech representations,

A. Baevski, Y. Zhou, and A. Mohamed, "wav2vec 2.0: A framework for self- supervised learning of speech representations," in Advances in Neural Information Processing Systems, vol. 33, pp. 12449-12460, 2020

2020

-

[34]

Federated learning for financial institutions: Privacy- preserving collaborative training,

H. Guo, J. Tang, and W. Liu, "Federated learning for financial institutions: Privacy- preserving collaborative training," IEEE Transactions on Information Forensics and Security, vol. 18, pp. 3421-3435, 2023

2023

-

[35]

Causal inference in financial markets,

J. Peters, D. Janzing, and B. Schölkopf, "Causal inference in financial markets," Journal of Machine Learning Research, vol. 24, no. 67, pp. 1-48, 2023

2023

-

[36]

Machine learning and asset pricing: New evidence,

E. F. Fama and K. R. French, "Machine learning and asset pricing: New evidence," Journal of Financial Economics, vol. 151, pp. 234-256, 2024

2024

-

[37]

AI-driven arbitrage in incomplete markets,

S. A. Ross and R. C. Merton, "AI-driven arbitrage in incomplete markets," Review of Financial Studies, vol. 36, no. 7, pp. 2876-2912, 2023

2023

-

[38]

Revisiting option pricing with neural networks,

F. Black and M. Scholes, "Revisiting option pricing with neural networks," Journal of Derivatives, vol. 31, no. 3, pp. 45-67, 2024

2024

-

[39]

Portfolio theory in the age of machine learning,

H. Markowitz and W. F. Sharpe, "Portfolio theory in the age of machine learning," Financial Analysts Journal, vol. 79, no. 2, pp. 23-41, 2023

2023

-

[40]

Adaptive markets and artificial intelligence,

A. W. Lo, "Adaptive markets and artificial intelligence," Journal of Portfolio Management, vol. 50, no. 4, pp. 123-145, 2024

2024

-

[41]

Proof of Convergence Rate We provide the complete proof for the convergence rate of our unified optimization algorithm

Theoretical Proofs 9.1. Proof of Convergence Rate We provide the complete proof for the convergence rate of our unified optimization algorithm. Let ℒ(𝜋)= −𝒥(𝜋) be the loss function where 𝒥(𝜋) is the unified objective. We make the following assumptions: Assumption 1: Each component objective 𝒥𝑖 is 𝐿𝑖-Lipschitz continuous. Assumption 2: The gradient norms a...

-

[42]

Implementation Details 10.1. Network Architectures PPO Actor Network: • Input layer: State dimension 𝑑𝑠 = 512 • Hidden layers: [1024, 512, 256] with ReLU activation • Output layer: Action dimension with softmax (discrete) or tanh (continuous) • Dropout: 0.2 between layers • Batch normalization after each hidden layer PPO Critic Network: • Input layer: Sta...

2048

-

[43]

Additional Experimental Results 11.1. Detailed Ablation Studies Table 5: Component-wise Ablation Study Results Configuration Sharpe HFT F1 Time Full Framework 1.67 78.5% 0.851 95𝜇𝑠 w/o PPO 1.36 76.2% 0.843 82𝜇𝑠 w/o HFT 1.46 - 0.847 43𝜇𝑠 w/o Sentiment 1.53 71.9% - 71𝜇𝑠 w/o Game Theory 1.58 75.3% 0.834 78𝜇𝑠 w/o ICL 1.61 77.1% 0.839 89𝜇𝑠 w/o Attention 1.42 7...

2048

-

[44]

Algorithm Pseudocode

-

[45]

Dataset Statistics 13.1. Market Data Statistics Table 9: Financial Market Dataset Characteristics Dataset Period Freq Assets Size S&P 500 2010− 2024 Daily 500 1.8 M NASDAQ 2010− 2024 Daily 3000 10.8 M Crypto 2018− 2024 Tick 50 2.3 B Forex 2015− 2024 Min 28 132 M Commodities 2012− 2024 Hourly 42 4.4 M Options 2015− 2024 Min 10000 850 M 13.2. Sentiment Data...

2010

-

[46]

Error Analysis 14.1. Failure Mode Analysis Our framework exhibits several failure modes that warrant discussion: Black Swan Events: During extreme market events (e.g., COVID-19 crash), the framework's performance degrades significantly. The Sharpe ratio drops to - 0.34 during March 2020, primarily due to unprecedented correlation breakdowns that violate h...

2020

-

[47]

Ethical Considerations 15.1. Transparency Mechanisms We implement several mechanisms to enhance interpretability: • Attention weight visualization for decision attribution • Component contribution scores for each trading decision • Natural language explanations generated by the ICL module • Counterfactual analysis showing alternative decisions • Risk fact...

-

[48]

Future Work Directions 16.1. Quantum Computing Integration The integration of quantum computing presents exciting opportunities for enhancing our framework: • Quantum optimization for portfolio selection could potentially solve NP-hard problems in polynomial time • Quantum machine learning algorithms for faster training convergence • Quantum Monte Carlo f...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.