Temporal Coarse-Graining of Latent Default-Probability Paths Generates Effective Default Correlation

Pith reviewed 2026-06-28 18:03 UTC · model grok-4.3

The pith

Persistent dynamics in a latent default-probability path generate effective default correlation when monthly data is aggregated over longer horizons.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

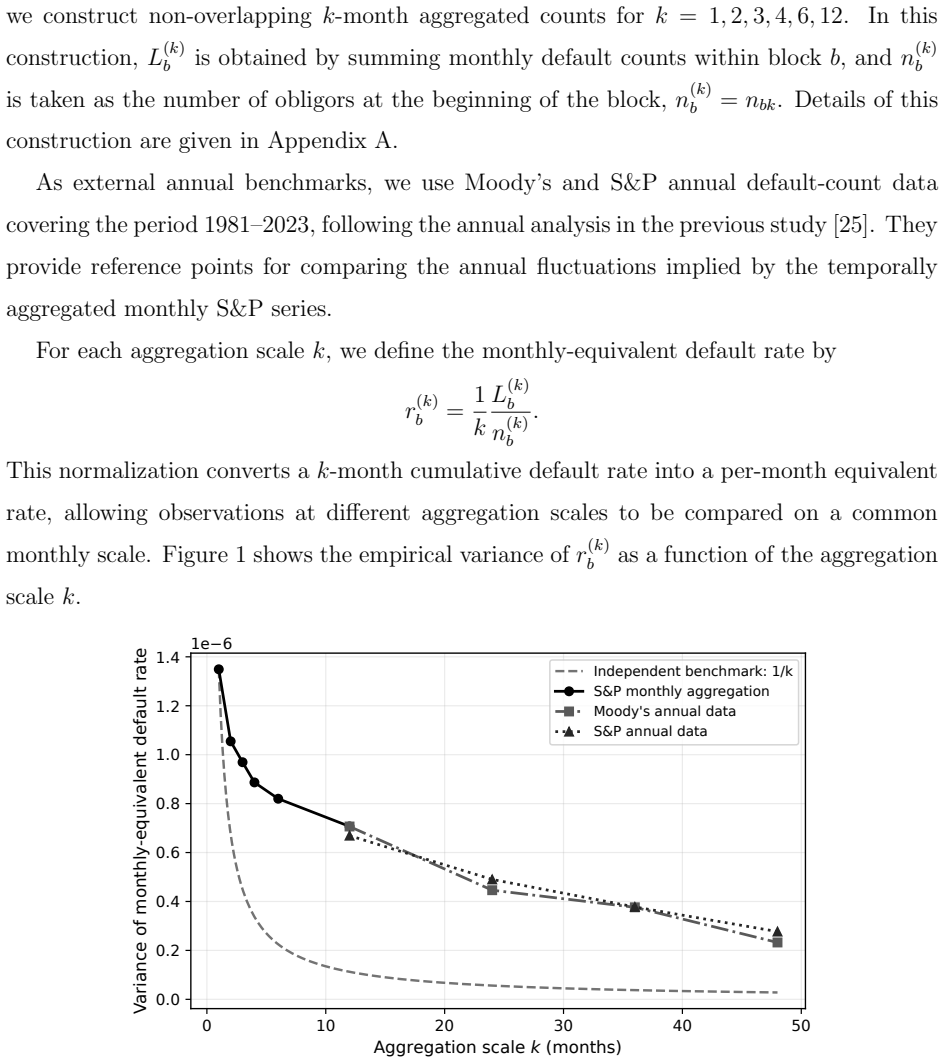

We show that persistent dynamics of a latent default-probability path can generate effective default correlation through temporal coarse-graining. In the OU--Binomial baseline, monthly defaults are conditionally independent given this latent path, but aggregating monthly default probabilities into long-horizon probabilities induces a scale-dependent effective mixing distribution for aggregated default counts. Applied to corporate default-count data, this mechanism explains long-horizon overdispersion, autocorrelation, and the emergence of effective default correlation. Direct fitting at each aggregation scale assigns increasing residual covariance shares to instantaneous dependence, but wors

What carries the argument

The OU-Binomial model with temporal coarse-graining of the persistent latent default-probability path, which induces a scale-dependent mixing distribution for aggregated default counts.

If this is right

- Explains long-horizon overdispersion in default counts.

- Generates autocorrelation in aggregated default counts.

- Produces effective default correlation through the induced mixing distribution.

- Keeps residual covariance contributions small when contagion or factor parameters are estimated conditional on coarse-grained paths.

- Improves per-block expected log predictive density compared to direct fitting at aggregate scales.

Where Pith is reading between the lines

- The same coarse-graining logic could apply to other persistent latent intensity processes that are observed only in aggregated counts.

- Credit risk models might separate horizon-dependent variance by first extracting monthly latent paths before fitting residual dependence.

- The approach suggests testing whether monthly default series show conditional independence once the latent path is accounted for.

Load-bearing premise

Monthly defaults are conditionally independent given the latent default-probability path.

What would settle it

Observing significant dependence between monthly defaults after conditioning on the estimated latent path would show that correlation does not arise purely from temporal coarse-graining.

Figures

read the original abstract

We show that persistent dynamics of a latent default-probability path can generate effective default correlation through temporal coarse-graining. In the OU--Binomial baseline, monthly defaults are conditionally independent given this latent path, but aggregating monthly default probabilities into long-horizon probabilities induces a scale-dependent effective mixing distribution for aggregated default counts. Applied to corporate default-count data, this mechanism explains long-horizon overdispersion, autocorrelation, and the emergence of effective default correlation. We then examine Davis--Lo-type contagion and Vasicek-type common-factor extensions. Direct fitting at each aggregation scale assigns increasing residual covariance shares to instantaneous dependence, but worsens the per-block expected log predictive density. In contrast, when monthly posterior latent paths are first coarse-grained and residual-dependence parameters are estimated conditional on these paths, the residual covariance contributions remain small while the predictive density improves. Thus, temporal coarse-graining provides a scale-consistent baseline that regularizes the attribution of variance and improves identifiability by suppressing the over-allocation of long-horizon fluctuations to contagion or asset-correlation parameters.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims that persistent dynamics of a latent default-probability path (modeled as an Ornstein-Uhlenbeck process) generate effective default correlation through temporal coarse-graining. In the OU-Binomial baseline, monthly defaults are conditionally independent given the latent path, but aggregation over longer horizons induces a scale-dependent mixing distribution that explains overdispersion, autocorrelation, and apparent correlation in corporate default-count data. Direct fitting at aggregate scales increases residual covariance attribution to instantaneous dependence and worsens predictive density, whereas extracting monthly posterior latent paths, coarse-graining them, and estimating residuals conditional on those paths keeps residual covariance small while improving per-block expected log predictive density, providing a scale-consistent baseline.

Significance. If the central mechanism holds, the work supplies a parsimonious explanation for scale-dependent default correlations arising purely from temporal aggregation of persistent latent dynamics rather than additional contagion or common-factor structures. This could regularize parameter attribution in credit-risk models and improve identifiability. The explicit comparison of direct versus coarse-grained fitting strategies, together with the emphasis on predictive density rather than in-sample fit alone, constitutes a clear methodological strength.

major comments (2)

- [Abstract] Abstract: the claim that aggregation 'induces a scale-dependent effective mixing distribution for aggregated default counts' is load-bearing for the central mechanism. The manuscript must supply the explicit derivation (presumably in the model section) showing how the OU parameters map to the mixing distribution and the resulting effective correlation, so that readers can verify it does not reduce to a reparameterization of the same data.

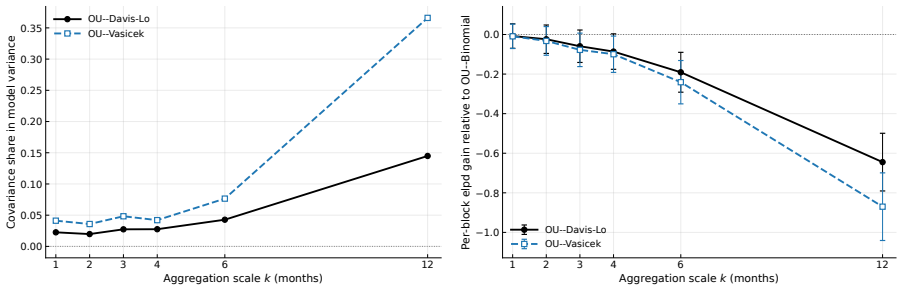

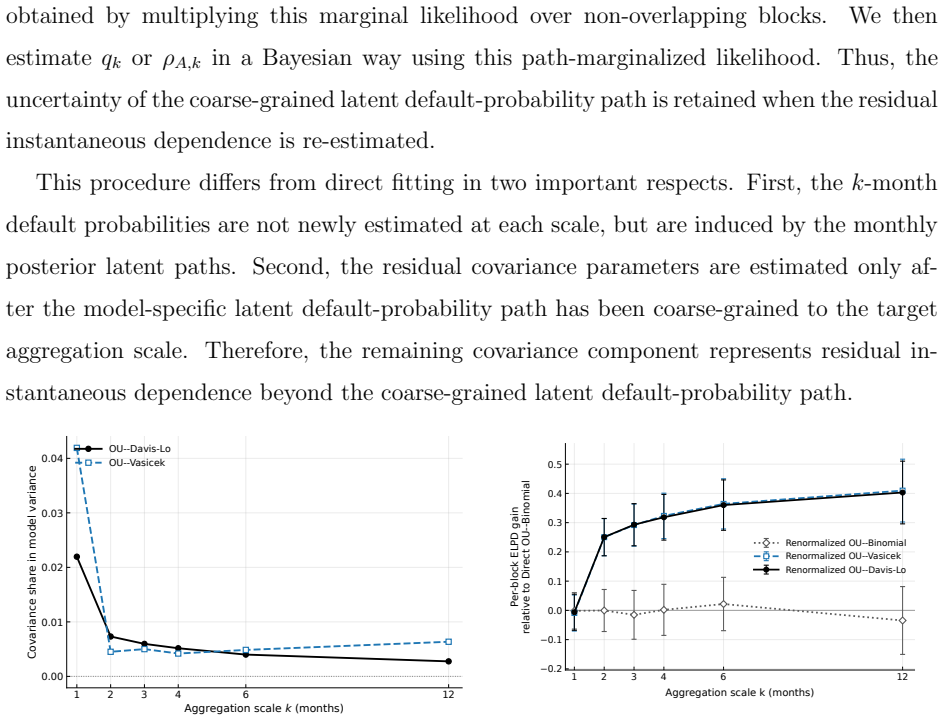

- [Abstract] Abstract / empirical section: the comparison asserting that coarse-graining keeps residual covariance small while direct fitting increases it and worsens per-block expected log predictive density is the key evidence against over-attribution to contagion or asset-correlation parameters. The specific numerical values (residual covariance shares and log predictive densities for each method and aggregation scale) must be reported in a table or figure to substantiate the claim.

minor comments (1)

- [Abstract] Abstract: the phrase 'OU--Binomial baseline' appears without a parenthetical gloss; a short definition on first use would aid readers outside the immediate subfield.

Simulated Author's Rebuttal

Thank you for the referee's constructive comments, which highlight key areas for strengthening the presentation of the central mechanism and empirical evidence. We address each major comment below and will incorporate revisions to improve clarity and substantiation without altering the core findings.

read point-by-point responses

-

Referee: [Abstract] Abstract: the claim that aggregation 'induces a scale-dependent effective mixing distribution for aggregated default counts' is load-bearing for the central mechanism. The manuscript must supply the explicit derivation (presumably in the model section) showing how the OU parameters map to the mixing distribution and the resulting effective correlation, so that readers can verify it does not reduce to a reparameterization of the same data.

Authors: We agree that an explicit derivation is necessary to allow verification of the mechanism. The model section already derives the scale-dependent mixing distribution from the OU process by integrating the latent path over the aggregation horizon, yielding an effective correlation that depends on the mean-reversion speed, volatility, and horizon length. To make this fully transparent and address the concern, we will revise the manuscript by expanding the model section with a self-contained step-by-step derivation (or a dedicated appendix) that maps the OU parameters directly to the mixing distribution parameters and the induced effective correlation, confirming the non-trivial aggregation effect. revision: yes

-

Referee: [Abstract] Abstract / empirical section: the comparison asserting that coarse-graining keeps residual covariance small while direct fitting increases it and worsens per-block expected log predictive density is the key evidence against over-attribution to contagion or asset-correlation parameters. The specific numerical values (residual covariance shares and log predictive densities for each method and aggregation scale) must be reported in a table or figure to substantiate the claim.

Authors: We acknowledge that explicit numerical values are required to substantiate the comparative claims. The empirical section presents the results of the direct-fitting versus coarse-graining strategies, including residual covariance attribution and predictive density comparisons, but these are not consolidated into a single table. We will revise the manuscript to include a new table (or augmented figure) that reports the precise residual covariance shares and per-block expected log predictive densities for each method across all aggregation scales examined. This will directly support the evidence regarding scale-consistent attribution. revision: yes

Circularity Check

No significant circularity; derivation self-contained

full rationale

The paper's core claim is that an OU latent default-probability path, under which monthly defaults are conditionally independent, produces effective correlation and overdispersion upon temporal aggregation; this follows directly from the mixing distribution induced by integrating the latent path over longer horizons. The reported comparison (direct scale-by-scale fitting versus first extracting monthly posterior paths, coarse-graining them, then fitting residuals) is an empirical diagnostic that contrasts two estimation procedures on the same data; neither procedure is shown to reduce to a tautological re-use of the same fitted values, and no load-bearing step invokes a self-citation, uniqueness theorem, or ansatz smuggled from prior work by the same author. The model assumptions and aggregation mathematics are stated explicitly and remain independent of the target quantities being explained.

Axiom & Free-Parameter Ledger

free parameters (1)

- OU process parameters (mean reversion speed, volatility, long-term mean)

axioms (1)

- domain assumption Monthly defaults are conditionally independent given the latent default-probability path

Reference graph

Works this paper leans on

-

[1]

The baseline default probabilityp t is inherited from the latent default-probability path of the OU–Binomial state-space model

Vasicek default-count distribution In the Vasicek specification, default dependence is generated by a common Gaussian factor. The baseline default probabilityp t is inherited from the latent default-probability path of the OU–Binomial state-space model. As in the main text, we write yt = Φ−1(pt), p t = Φ(yt), where Φ denotes the standard normal cumulative...

-

[2]

As in the main text, the baseline probabilityp t is generated by the latent default-probability path of the OU–Binomial state-space model

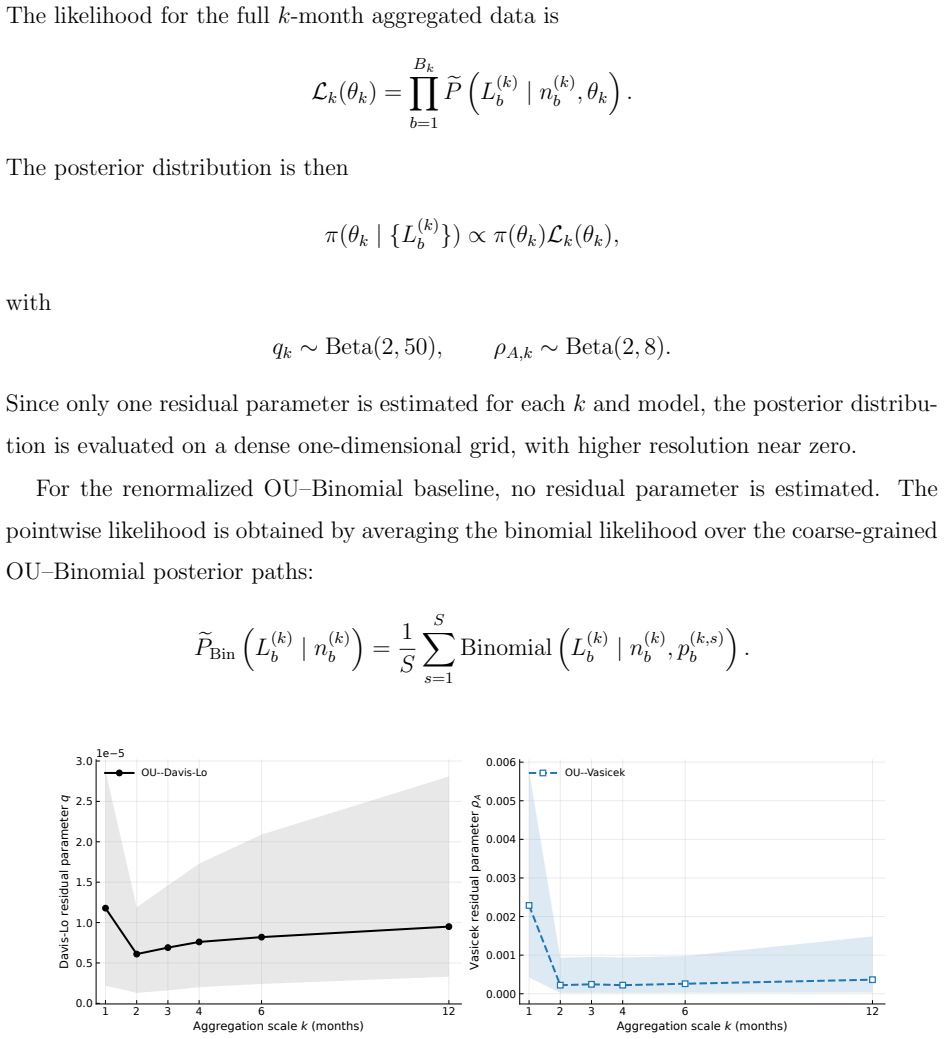

Davis–Lo default-count distribution In the Davis–Lo specification, default dependence is generated by a cumulative conta- gion mechanism. As in the main text, the baseline probabilityp t is generated by the latent default-probability path of the OU–Binomial state-space model. LetX it denote the idiosyn- cratic default indicator of obligoriin periodt, with...

-

[3]

The observation equation is Lt |p t, nt ∼Binomial(n t, pt), and the latent default probability is represented on the probit scale as yt = Φ−1(pt), p t = Φ(yt)

Bayesian estimation of the monthly OU–Binomial model The monthly OU–Binomial model was estimated by Bayesian inference using the monthly S&P default-count series from January 1981 to September 2021 (T= 489). The observation equation is Lt |p t, nt ∼Binomial(n t, pt), and the latent default probability is represented on the probit scale as yt = Φ−1(pt), p ...

1981

-

[4]

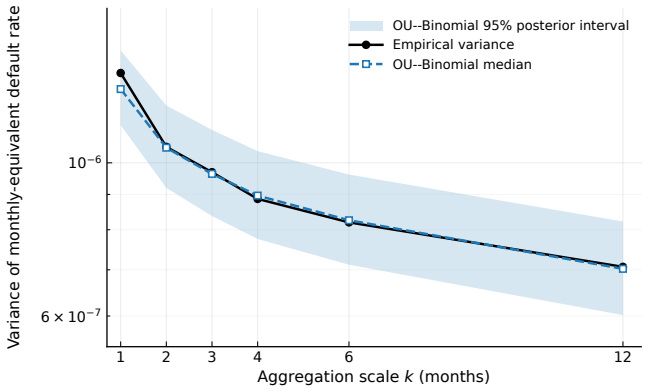

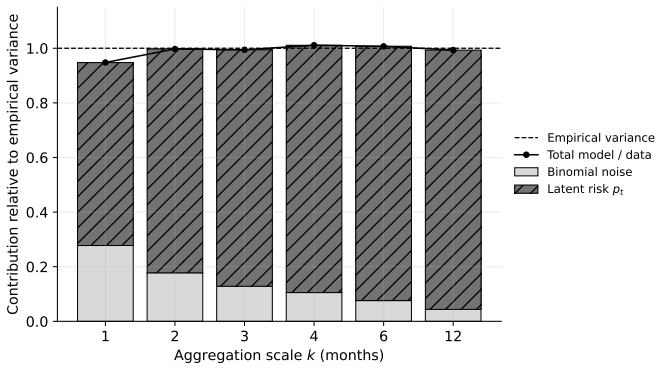

Variance decomposition of the coarse-grained OU–Binomial model We first examine how the variance of the coarse-grained OU–Binomial model is decom- posed into conditional binomial noise and fluctuations of the latent default-probability path. For each aggregation scalek, we decompose the posterior predictive variance of the monthly- equivalent default rate...

-

[5]

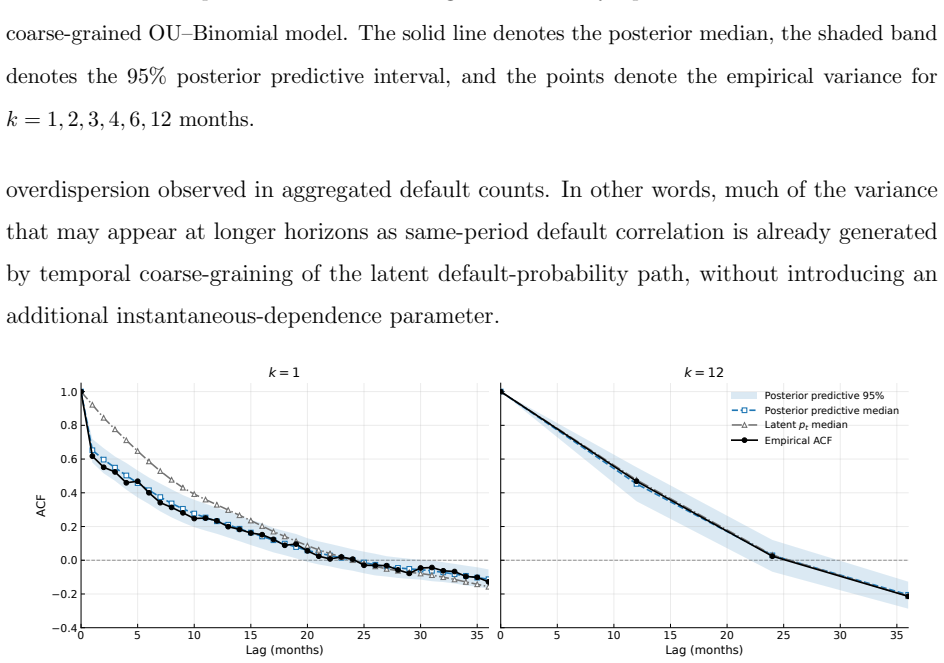

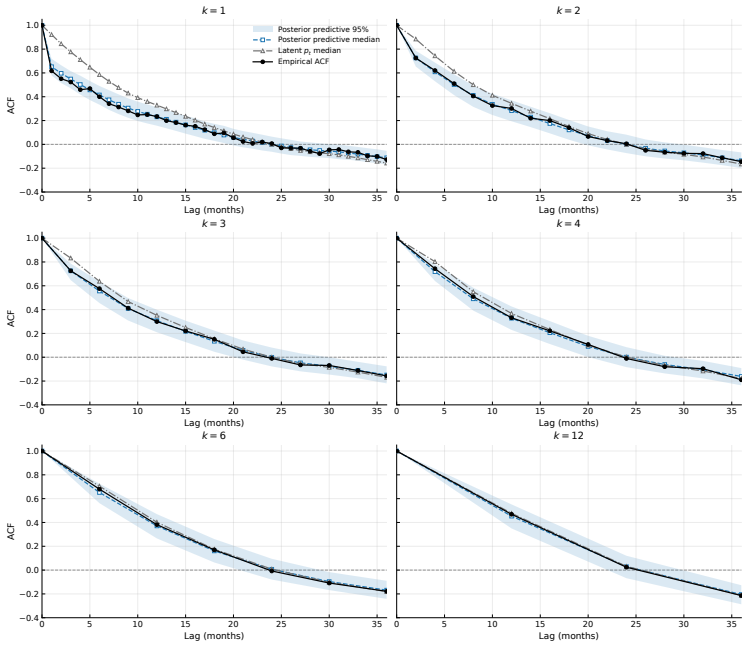

Autocorrelation diagnostics Figure 8 shows that the coarse-grained OU–Binomial posterior paths reproduce the em- pirical ACF over all aggregation scalesk= 1,2,3,4,6,12, confirming that the variance scaling is accompanied by a consistent representation of temporal persistence in the latent default-probability path. 30 0 5 10 15 20 25 30 35 Lag (months) −0....

-

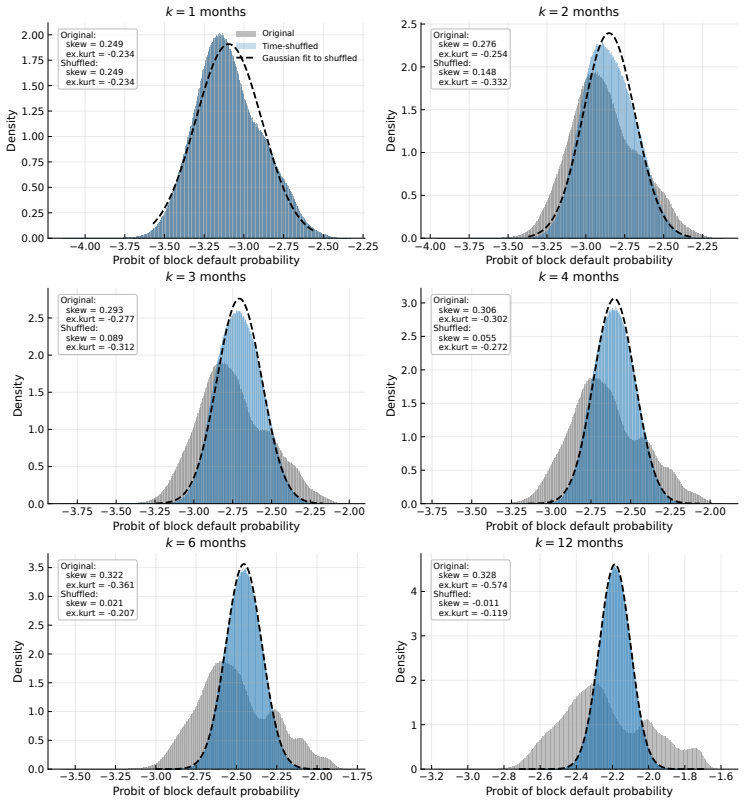

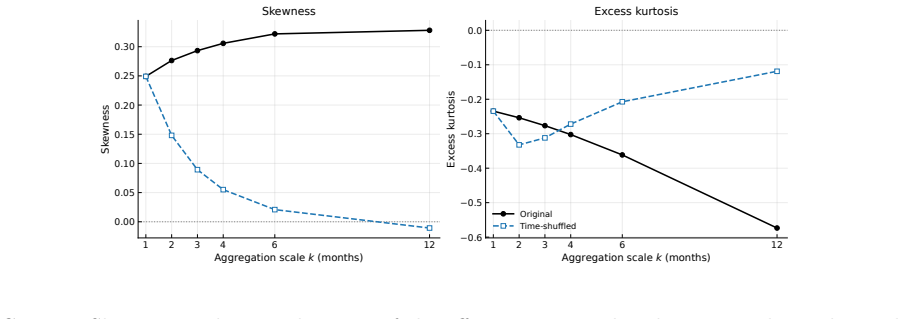

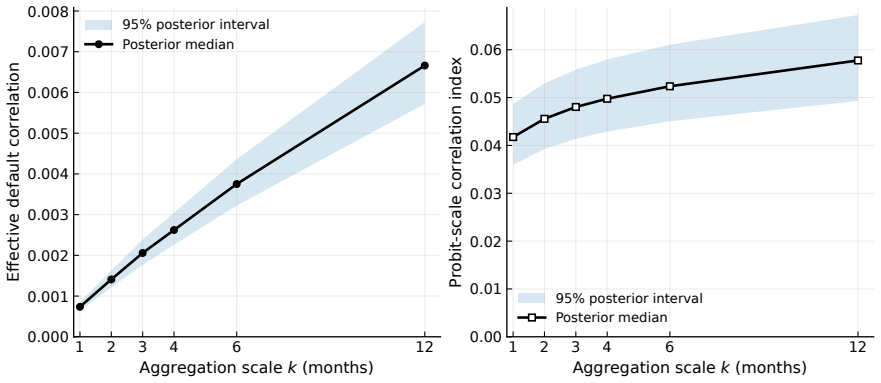

[6]

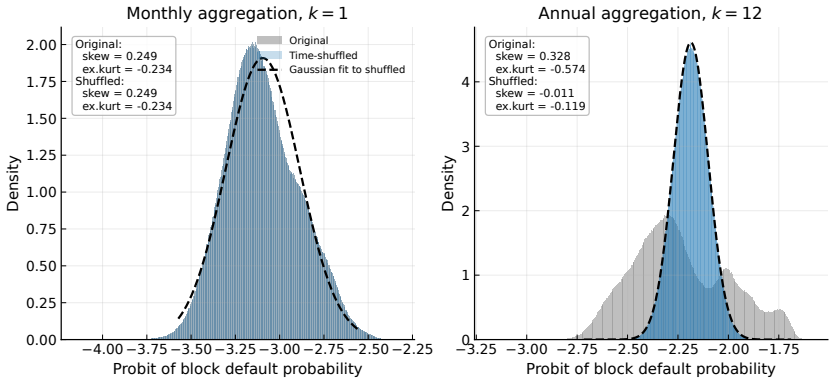

Effective mixing distributions Figures 9 and 10 provide additional diagnostics of the effective mixing distribution. The original posterior paths and the time-shuffled benchmark differ increasingly with the aggre- gation scale, indicating that the long-horizon distribution is shaped by the temporal ordering and persistence of the monthly latent default-pr...

-

[7]

R. N. Mantegna and H. E. Stanley,An Introduction to Econophysics: Correlations and Com- plexity in Finance(Cambridge University Press, 1999)

1999

-

[8]

Galam, Int

S. Galam, Int. J. Mod. Phys. C19, 409 (2008)

2008

-

[9]

Lux, Econ

T. Lux, Econ. J.105, 881 (1995)

1995

-

[10]

Lux and M

T. Lux and M. Marchesi, Nature397, 498 (1999)

1999

-

[11]

Alfarano, T

S. Alfarano, T. Lux, and F. Wagner, Comput. Econ.26, 19 (2005)

2005

-

[12]

Bouchaud, M

J.-P. Bouchaud, M. M´ ezard, and M. Potters, Quant. Finance2, 251 (2002)

2002

-

[13]

Fernandez-Gracia, K

J. Fernandez-Gracia, K. Suchecki, J. J. Ramasco, M. SanMiguel, and V. M. Egu´ ıluz, Phys. Rev. Lett.112, 158701 (2014)

2014

-

[14]

S. Mori, M. Hisakado, and T. Takahashi, Phys. Rev. E86, 026109 (2012)

2012

-

[15]

S. Mori, K. Nakayama, and M. Hisakado, Phys. Rev. E99, 052307 (2019)

2019

-

[16]

Smolyak and S

A. Smolyak and S. Havlin, Entropy24, 271 (2022)

2022

-

[17]

P. J. Sch¨ onbucher,Credit Derivatives Pricing Models: Models, Pricing and Implementation (John Wiley & Sons, 2003)

2003

-

[18]

M. H. A. Davis and V. Lo, Quant. Finance1, 382 (2001)

2001

-

[19]

O. A. Vasicek, KMV Corporation (1991), working paper

1991

-

[20]

O. A. Vasicek, Risk15, 160 (2002)

2002

-

[21]

S. R. Das, D. Duffie, N. Kapadia, and L. Saita, J. Finance62, 93 (2007). 42

2007

-

[22]

Duffie, A

D. Duffie, A. Eckner, G. Horel, and L. Saita, J. Finance64, 2089 (2009)

2089

-

[23]

Azizpour, K

S. Azizpour, K. Giesecke, and G. Schwenkler, J. Financ. Econ.129, 154 (2018)

2018

-

[24]

Sakata, M

A. Sakata, M. Hisakado, and S. Mori, J. Phys. Soc. Jpn.76, 054801 (2007)

2007

-

[25]

Torri, R

G. Torri, R. Giacometti, and G. Farina, Commun. Nonlinear Sci. Numer. Simul.159, 109886 (2026)

2026

-

[26]

Hisakado and S

M. Hisakado and S. Mori, Physica A: Statistical Mechanics and its Applications563, 125435 (2021)

2021

-

[27]

A. G. Hawkes, Biometrika58, 83 (1971)

1971

-

[28]

Errais, K

E. Errais, K. Giesecke, and L. R. Goldberg, SIAM J. Financial Math.1, 642 (2010)

2010

-

[29]

Kirchner, Quant

M. Kirchner, Quant. Finance17, 571 (2017)

2017

-

[30]

Hisakado, K

M. Hisakado, K. Hattori, and S. Mori, Phys. Rev. E106, 034106 (2022)

2022

-

[31]

S. Mori, Contagion or macroeconomic fluctuations? identifiability in aggregated default data (2026), arXiv preprint arXiv:2604.18118, arXiv:2604.18118 [q-fin.RM]. 43

Pith/arXiv arXiv 2026

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.