Restoring Incentive Compatibility in Two-Stage Energy Markets with Prosumers

Pith reviewed 2026-06-25 19:54 UTC · model grok-4.3

The pith

Prosumers retain a positive lower-bounded incentive to under-report demand in two-stage energy markets even as the day-ahead market scales large.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

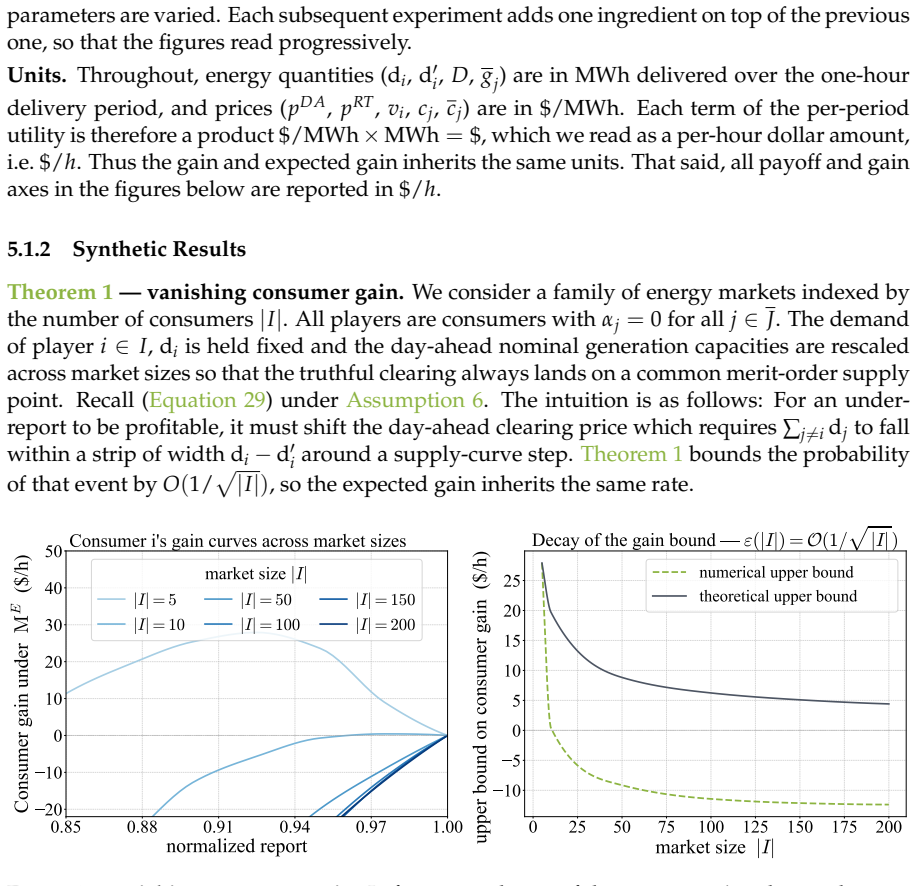

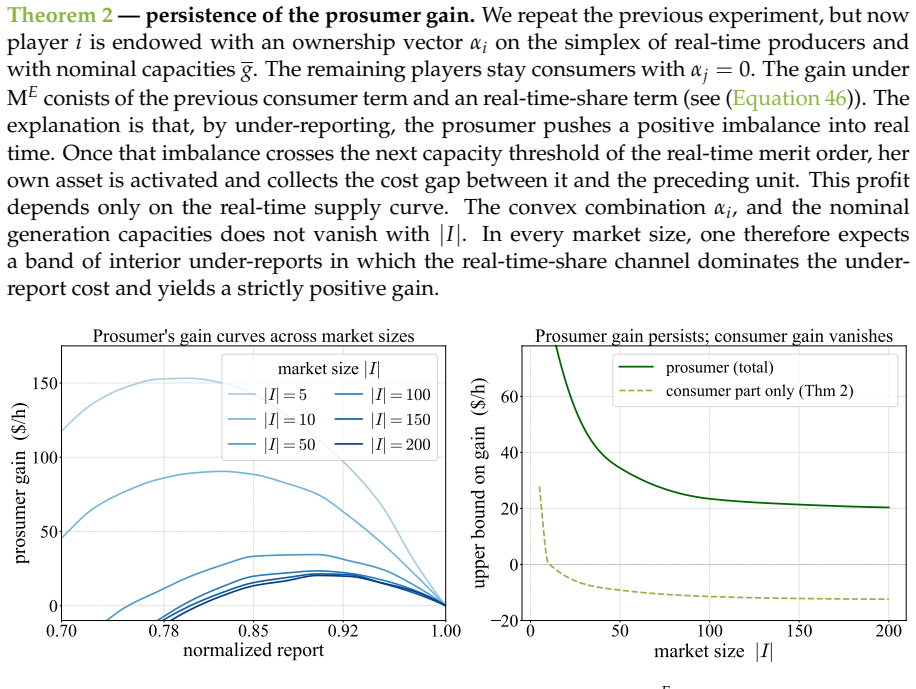

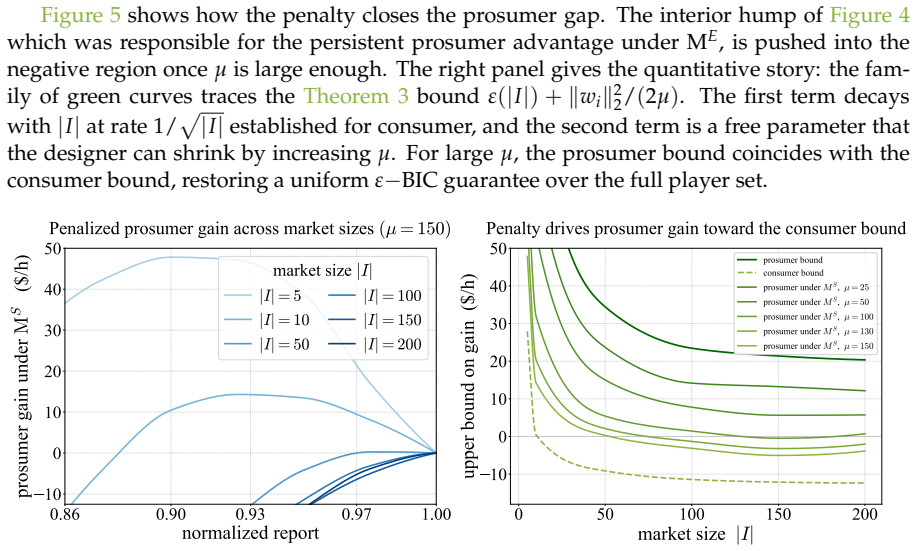

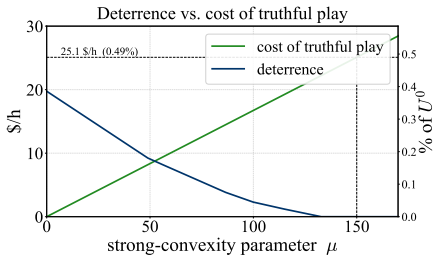

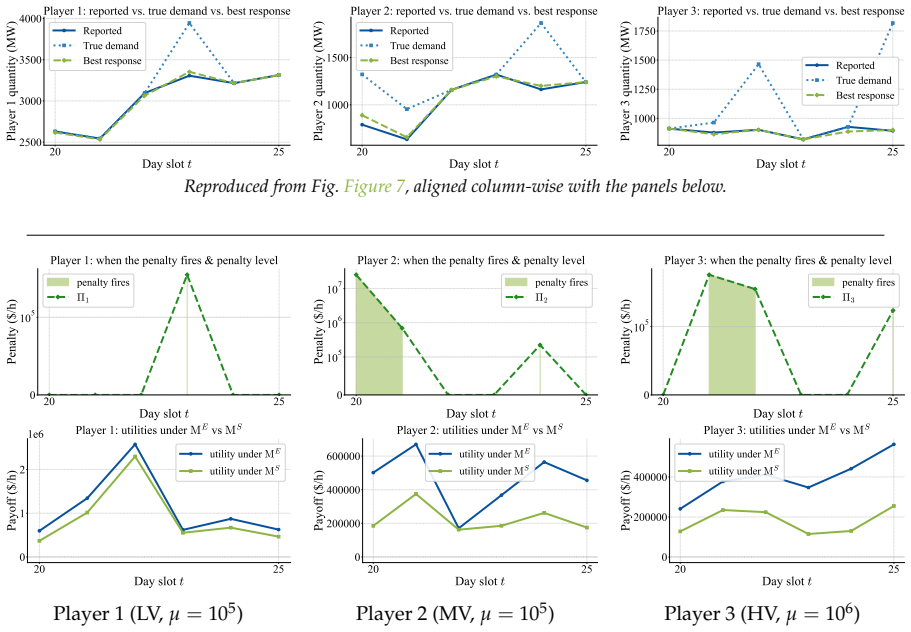

In two-stage energy markets under linear preferences, prosumers have an incentive to under-report day-ahead demand in order to inflate real-time imbalances and dispatch their generation assets more profitably under uniform pricing. Unlike consumers, this incentive does not vanish with day-ahead market scaling and remains lower bounded by a positive value that depends solely on the real-time generation stack and the prosumers' shares over it. A leave-one-out contrastive scoring rule-based penalty, implemented by the day-ahead market operator under existing informational constraints, restores incentive compatibility and ensures only small charges for honest participation.

What carries the argument

Leave-one-out contrastive scoring rule-based penalty, which scores each prosumer's report against the reports of all others to create charges that align individual incentives with truthful demand reporting.

If this is right

- The day-ahead operator can apply the penalty without collecting any additional private information from participants.

- Honest prosumers face only small charges from the mechanism.

- The design maintains the economic efficiency of the overall market institution.

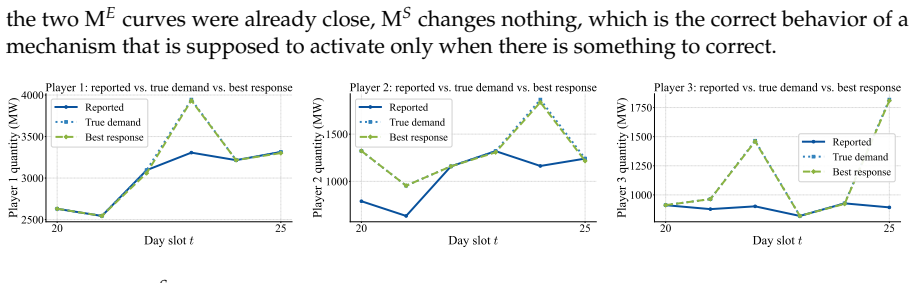

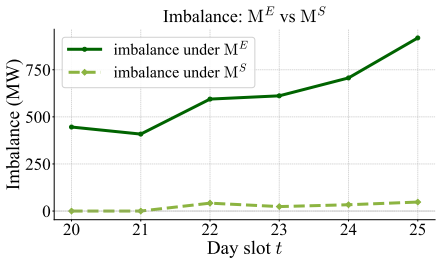

- Numerical simulations on both synthetic and real-market data confirm that the penalty produces strong incentive alignment.

Where Pith is reading between the lines

- The penalty structure might transfer to other sequential markets in which agents hold both consumption and production assets.

- If agent preferences deviate from linearity, the size of the persistent incentive could increase or decrease depending on the curvature.

- Regulators could run controlled pilots that measure changes in reported demand before and after introducing the penalty.

- The dependence on real-time generation shares suggests the mechanism could be tuned to focus charges on the largest prosumers.

Load-bearing premise

All agents have linear preferences and the day-ahead operator can implement the penalty using only the reports and market outcomes already available without any extra private data.

What would settle it

A simulation or market dataset in which the modeled prosumers' incentive to under-report drops to zero once the day-ahead market is scaled up, or in which the proposed penalty produces large charges even for truthful reports.

Figures

read the original abstract

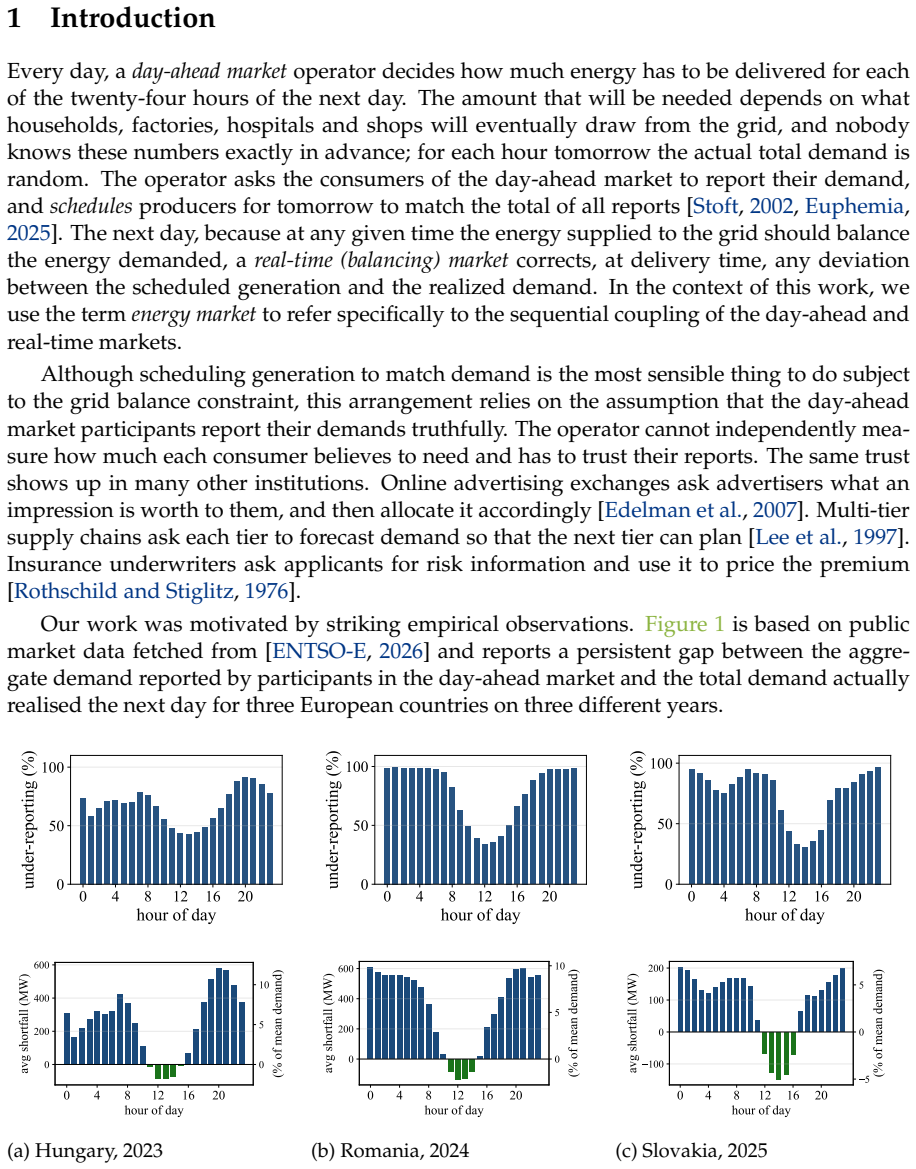

A central challenge in modern energy market design is the formulation of a strategy-proof imbalance settlement layer that secures both the economic efficiency of the institution and the stability of the power grid. Public data reveals that the day-ahead market is strategically biased below actual consumer demand. Such empirical observations are explained by active prosumers which provide implementable incentives for demand under-reporting. Active prosumers buy energy in the day-ahead market and sell energy in the real-time market for balancing real-time energy deviations. By under-reporting their demand for the day ahead they inflate real-time imbalances and, under uniform pricing, they dispatch their generation assets more profitably. We model the two-stage institution under linear preferences and benchmark it against its associated competitive equilibria. We show that although consumers' incentives for demand under-reporting vanish when the day-ahead market scales, prosumers' incentives remain lower bounded by a positive gain which depends only on the real-time market generation stack and their shares over it. To restore incentive compatibility under the existing informational constraints, we design a leave-one-out contrastive scoring rule-based penalty that is implemented by the day-ahead market operator, incentivizes prosumers to report their demand truthfully and ensures small charges when participating honestly. We illustrate these results with numerical simulations on synthetic data and evaluate our mechanism on real-market data by first rationalizing demand reports as subjective equilibria of the induced game. Our mechanism demonstrates strong incentive alignment while retaining a low cost for honest participation.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper models two-stage energy markets where prosumers buy in the day-ahead (DA) market and sell in real-time (RT) to balance deviations. Under linear preferences and benchmarking against competitive equilibria, it shows consumers' incentives to under-report DA demand vanish as the DA market scales, but prosumers retain a positive lower bound on gains from under-reporting that depends only on the RT generation stack and their shares over it. To restore incentive compatibility under existing informational constraints, the authors design a leave-one-out contrastive scoring rule-based penalty implemented by the DA operator that incentivizes truthful demand reporting by prosumers while keeping charges small for honest participation. Claims are supported by synthetic simulations and evaluation on real-market data after rationalizing reports as subjective equilibria.

Significance. If the mechanism is feasible under the stated constraints, the work addresses a documented strategic bias in DA markets by providing an incentive-aligned imbalance settlement layer without new data requirements, which could improve efficiency and grid stability in practice. The incentive bound's dependence solely on observable RT stack quantities (rather than fitted parameters) and the contrastive scoring approach are strengths. The real-data evaluation after rationalizing equilibria adds empirical grounding. This could influence mechanism design for multi-stage markets with prosumers.

major comments (1)

- [Mechanism design section] Mechanism design section (description of the leave-one-out contrastive scoring rule penalty): the central claim that this penalty restores incentive compatibility under existing informational constraints is load-bearing but rests on the operator being able to isolate individual prosumer reports, identify which agents are prosumers (to apply the penalty selectively), and compute per-prosumer contrastive scores from submitted demand reports alone. The manuscript does not explicitly demonstrate how this is possible when DA markets typically supply only aggregated bids or treat participants anonymously; this assumption is not secured by the linear-preference model or the RT-stack bound alone.

minor comments (2)

- [Introduction] The abstract and introduction refer to 'existing informational constraints' without a dedicated subsection enumerating exactly what information the DA operator has access to (e.g., aggregated vs. disaggregated bids, prosumer identities). Adding this would clarify the feasibility claim.

- [Numerical simulations section] Numerical simulations section: the synthetic data generation process and the exact procedure for rationalizing real-market demand reports as subjective equilibria are described at a high level; more explicit pseudocode or parameter values would improve reproducibility.

Simulated Author's Rebuttal

We thank the referee for highlighting an important implementation detail in the mechanism design section. We address the concern below and will revise the manuscript accordingly to strengthen the exposition of informational assumptions.

read point-by-point responses

-

Referee: [Mechanism design section] Mechanism design section (description of the leave-one-out contrastive scoring rule penalty): the central claim that this penalty restores incentive compatibility under existing informational constraints is load-bearing but rests on the operator being able to isolate individual prosumer reports, identify which agents are prosumers (to apply the penalty selectively), and compute per-prosumer contrastive scores from submitted demand reports alone. The manuscript does not explicitly demonstrate how this is possible when DA markets typically supply only aggregated bids or treat participants anonymously; this assumption is not secured by the linear-preference model or the RT-stack bound alone.

Authors: We agree that the manuscript would benefit from an explicit discussion of these operational assumptions. Our model is formulated at the level of individual participants submitting demand reports directly to the DA operator (as is standard in mechanism-design analyses of prosumer markets), which permits isolation of reports, computation of leave-one-out contrastive scores from the vector of submitted demands alone, and selective application of the penalty to agents identified as prosumers via registration or reported generation capacity. No additional private information beyond the bids themselves is required, preserving the "existing informational constraints" claim. That said, we acknowledge that many real-world DA markets operate with aggregated bids submitted by retailers or virtual power plants. We will revise the mechanism-design section to (i) state the individual-submission assumption clearly, (ii) note that the contrastive penalty can be applied at the aggregator level when bids are aggregated (with the aggregator then incentivizing its constituent prosumers), and (iii) discuss how prosumer identification can leverage existing registration data without new reporting requirements. These clarifications do not alter the incentive or equilibrium results but make the feasibility claim more robust. revision: yes

Circularity Check

No significant circularity; derivation benchmarks against independent competitive equilibria.

full rationale

The paper models the two-stage institution under linear preferences and explicitly benchmarks against associated competitive equilibria. It derives that consumer incentives vanish at scale while prosumer incentives are lower-bounded by a quantity depending on the real-time generation stack and shares. The leave-one-out contrastive scoring rule penalty is then designed to restore compatibility. No quoted step reduces a claimed prediction or bound to a fitted input by construction, nor does any load-bearing premise rest on a self-citation chain; the central results are presented as consequences of the model and equilibrium benchmark rather than tautological redefinitions.

Axiom & Free-Parameter Ledger

free parameters (2)

- prosumers' shares over real-time generation stack

- scoring rule contrast parameters

axioms (3)

- domain assumption Agents have linear preferences

- domain assumption Uniform pricing applies in the real-time market

- domain assumption Day-ahead market can be scaled while preserving the two-stage structure

invented entities (1)

-

leave-one-out contrastive scoring rule-based penalty

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Official Journal of the European Union, L158, 14 June 2019, pp.54-124, June

Regulation (EU) 2019/943 of the European Parliament and of the Council of 5 June 2019 on the internal market for electricity (recast). Official Journal of the European Union, L158, 14 June 2019, pp.54-124, June

2019

-

[2]

Ofer Dekel, Felix Fischer, and Ariel D

Translated as ’Foresight: Its Logical Laws, Its Subjective Sources’ in Kyburg and Smokler (1964). Ofer Dekel, Felix Fischer, and Ariel D. Procaccia. Incentive compatible regression learning. Journal of Computer and System Sciences, 76(8):759–777,

1964

-

[3]

Benjamin Edelman, Michael Ostrovsky, and Michael Schwarz

doi: 10.1016/j.jcss.2010.03.003. Benjamin Edelman, Michael Ostrovsky, and Michael Schwarz. Internet advertising and the generalized second-price auction: Selling billions of dollars worth of keywords.Ameri- can Economic Review, 97(1):242–259, March

-

[4]

URLhttps: //www.aeaweb.org/articles?id=10.1257/aer.97.1.242

doi: 10.1257/aer.97.1.242. URLhttps: //www.aeaweb.org/articles?id=10.1257/aer.97.1.242. ENTSO-E. ENTSO-E Mission Statement, a. URLhttps://www.entsoe.eu/about/inside- entsoe/mission-statement/. About page (mission statement). ENTSO-E. Total load – greece (25 may 2025), b.https://transparency.entsoe.eu/ load-domain/r2/totalLoadR2/show?name=&defaultValue=fal...

-

[5]

EU. Directive (eu) 2019/944 of the european parliament and of the council of 5 june 2019 on common rules for the internal market for electricity and amending directive 2012/27/eu (recast). Official Journal of the European Union,

2019

-

[6]

Accessed: 2025-01-07

URLhttps: //www.nemo-committee.eu/. Accessed: 2025-01-07. European Commission. Third energy package. Legislative package, Directives 2009/72/EC and 2009/73/EC; Regulations (EC) No 713/2009, 714/2009, and 715/2009,

2025

-

[7]

Commission regulation (eu) 2015/1222 of 24 july 2015 establish- ing a guideline on capacity allocation and congestion management,

53 European Commission. Commission regulation (eu) 2015/1222 of 24 july 2015 establish- ing a guideline on capacity allocation and congestion management,

2015

-

[8]

OJ L 197, 25.7.2015, pp

URLhttps: //eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32015R1222. OJ L 197, 25.7.2015, pp. 24–72. European Commission. Commission regulation (eu) 2017/2195 of 23 november 2017 estab- lishing a guideline on electricity balancing. Official Journal of the European Union, Novem- ber 2017a. URLhttps://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri...

2015

-

[9]

News item, 1 Oct

URLhttps://energy.ec.europa.eu/news/eu-electricity-trading-day- ahead-markets-becomes-more-dynamic-2025-10-01 en. News item, 1 Oct

2025

-

[10]

Directive (eu) 2019/944 of 5 june 2019 on common rules for the internal market for electricity and amending di- rective 2012/27/eu, 2019a

European Parliament and Council of the European Union. Directive (eu) 2019/944 of 5 june 2019 on common rules for the internal market for electricity and amending di- rective 2012/27/eu, 2019a. URLhttps://eur-lex.europa.eu/legal-content/EN/TXT/ PDF/?uri=CELEX:32019L0944. OJ L 158, 14.6.2019, pp. 125–199. European Parliament and Council of the European Uni...

2019

-

[11]

Tilmann Gneiting and Adrian E. Raftery. Strictly proper scoring rules, prediction, and estimation.Journal of the American Statistical Association, 102(477):359–378, 2007a. doi: 10.1198/016214506000001437. Tilmann Gneiting and Adrian E. Raftery. Strictly proper scoring rules, prediction, and estima- tion.Journal of the American Statistical Association, 102...

-

[12]

Irving John Good, AJ Mayne, JM Smith, and Thornton Page

URLhttps://www.jstor.org/stable/2984087. Irving John Good, AJ Mayne, JM Smith, and Thornton Page. The scientist speculates: an anthology of partly-baked ideas.American Journal of Physics, 32(4):322–322,

-

[13]

Moritz Hardt, Nimrod Megiddo, Christos Papadimitriou, and Mary Wootters

doi: 10.5750/jpm.v1i1.417. Moritz Hardt, Nimrod Megiddo, Christos Papadimitriou, and Mary Wootters. Strategic clas- sification. InProceedings of the 2016 ACM Conference on Innovations in Theoretical Computer Science (ITCS), pages 111–122. ACM,

-

[14]

doi: 10.1145/2840728.2840730. HENEX. Hellenic energy exchange (henex): Day-ahead market report.https:// www.enexgroup.gr/web/guest/markets-publications-el-day-ahead-market. HEnEx. Hellenic energy exchange,

-

[15]

Accessed: 2025- 01-07

URLhttps://www.enexgroup.gr/. Accessed: 2025- 01-07. ISO New England Inc. Regulation (Settlement item description), n.d. URL https://www.iso-ne.com/markets-operations/settlements/understand-bill/item- descriptions/regulation. Webpage describing regulation as an ancillary service provided based on regulation supply offers. Ehud Kalai and Ehud Lehrer. Subje...

2025

-

[16]

URL http://www.jstor.org/stable/2634565

ISSN 00251909, 15265501. URL http://www.jstor.org/stable/2634565. 55 Paul L´evy.Th´ eorie de l’addition des variables al´ eatoires. Gauthier-Villars, Paris,

-

[17]

doi: 10.1016/j.artint.2012.03.008. Monitoring Analytics. 2023 State of the Market Report for PJM, Section 3: Energy Mar- ket. Technical report, March

-

[18]

URLhttps://www.monitoringanalytics.com/reports/ PJM State of the Market/2023/2023-som-pjm-sec3.pdf. See pp. 130–132, Figs. 3-1 and 3- 2 (day-ahead supply curves); pp. 143–148 (LMP fuel cost component decomposition). Roger B. Myerson. Optimal auction design.Mathematics of Operations Research, 6(1):58–73,

2023

-

[19]

URLhttp://www.jstor.org/stable/3689266

ISSN 0364765X, 15265471. URLhttp://www.jstor.org/stable/3689266. Yurii Nesterov et al.Lectures on convex optimization, volume

-

[20]

Committee document dated April 12, 2023 (PDF)

URLhttps://www.pjm.com/-/media/ DotCom/committees-groups/committees/mic/2023/20230412/20230412-item-02-3--- real-time-values-manual-11-revisions---redline.ashx. Committee document dated April 12, 2023 (PDF). PJM Interconnection.Manual 11: Energy & Ancillary Services Market Operations, revision 129 edi- tion, February 2024a. URLhttps://www.pjm.com/library/...

2023

-

[21]

URLhttps://insidelines.pjm.com/pjm-publishes-annual-planning-report- for-2023/

PJM Inside Lines, 2024b. URLhttps://insidelines.pjm.com/pjm-publishes-annual-planning-report- for-2023/. Documents over 1,400 generators and approximately 65,000 MW of natural gas capacity interconnection rights in PJM. PJM Interconnection. Ancillary Services Fact Sheet, January

2023

-

[22]

56 Michael Rothschild and Joseph Stiglitz

doi: 10.1137/1106007. 56 Michael Rothschild and Joseph Stiglitz. Equilibrium in competitive insurance markets: An essay on the economics of imperfect information.The Quarterly Journal of Economics, 90(4): 629–649,

-

[23]

URLhttp://www.jstor.org/stable/1885326

ISSN 00335533, 15314650. URLhttp://www.jstor.org/stable/1885326. Leonard J Savage. Elicitation of personal probabilities and expectations. In V . P . Godambe and D. A. Sprott, editors,Foundations of statistical inference, pages 159–175. Holt, Rinehart and Winston,

-

[24]

Press release dated 01 Oct 2025; go-live on trading day 30 Sep 2025 for delivery day 1 Oct

URLhttps://eepublicdownloads.blob.core.windows.net/public-cdn-container/ clean-documents/Network%20codes%20documents/NC%20CACM/SDAC%202025/SDAC 15- Minute MTU Was Implemented.pdf. Press release dated 01 Oct 2025; go-live on trading day 30 Sep 2025 for delivery day 1 Oct

2025

-

[25]

Backgrounder (docu- ment label: 2022; formatted 2023-04-17 per filename)

URLhttps://www.energy.gov/sites/default/files/2023-08/Balancing% 20Authority%20Backgrounder 2022-Formatted 041723 508.pdf. Backgrounder (docu- ment label: 2022; formatted 2023-04-17 per filename). U.S. Energy Information Administration. Newer-technology natural gas-fired generators are utilized more than older units in PJM. Today in Energy, April

2023

-

[26]

Documents fleet-wide average heat rate of 6,960 BTU/kWh for CCGT plants built 2010–2022

URLhttps:// www.eia.gov/todayinenergy/detail.php?id=60984. Documents fleet-wide average heat rate of 6,960 BTU/kWh for CCGT plants built 2010–2022. William Vickrey. Counterspeculation, auctions, and competitive sealed tenders.The Journal of finance, 16(1):8–37,

2010

-

[27]

doi: 10.1016/ j.egyr.2023.09.069. See p. 2778 (Abstract: headline results); p. 2780, Section 3 (methodology based on day-ahead market data); p. 2785, Fig. 5 (country-level marginal shares in 2021). 57

2023

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.