Portfolio Choice with Competing Precautionary and Accumulation Goals

Pith reviewed 2026-06-28 07:41 UTC · model grok-4.3

The pith

The value function for a household with both a random emergency goal and a fixed retirement goal need not increase with wealth under forced funding.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

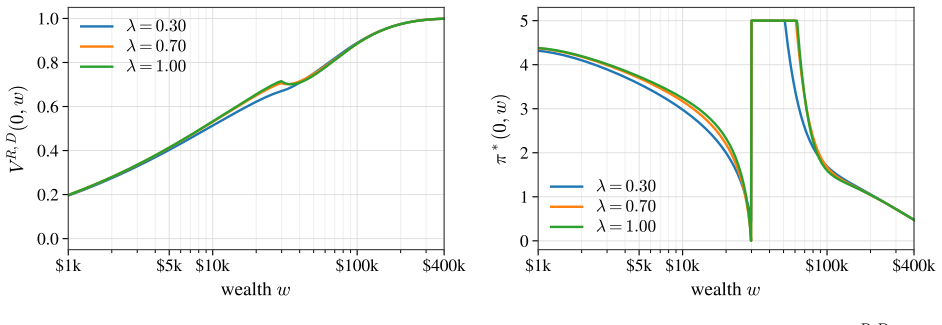

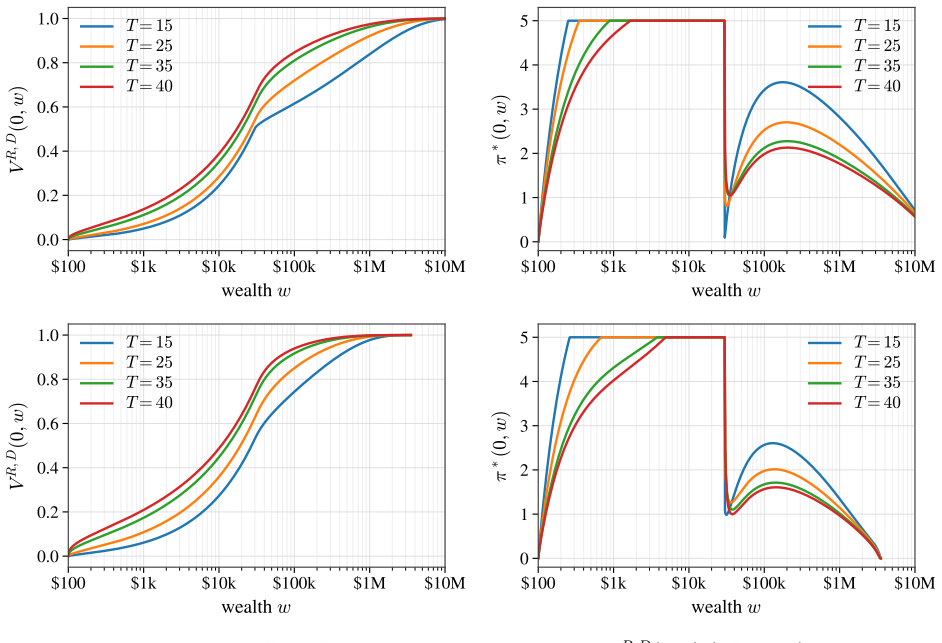

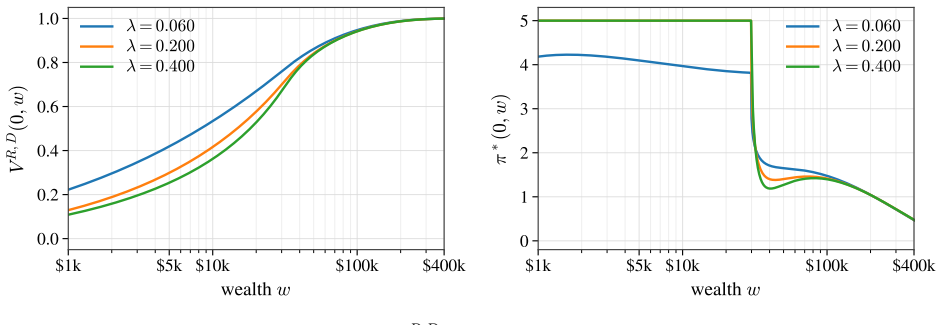

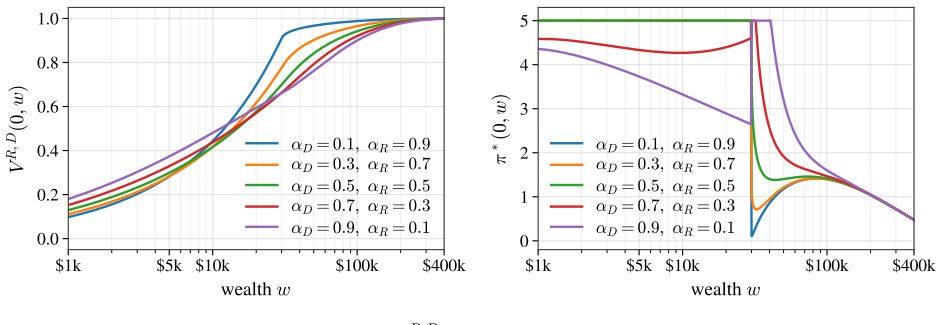

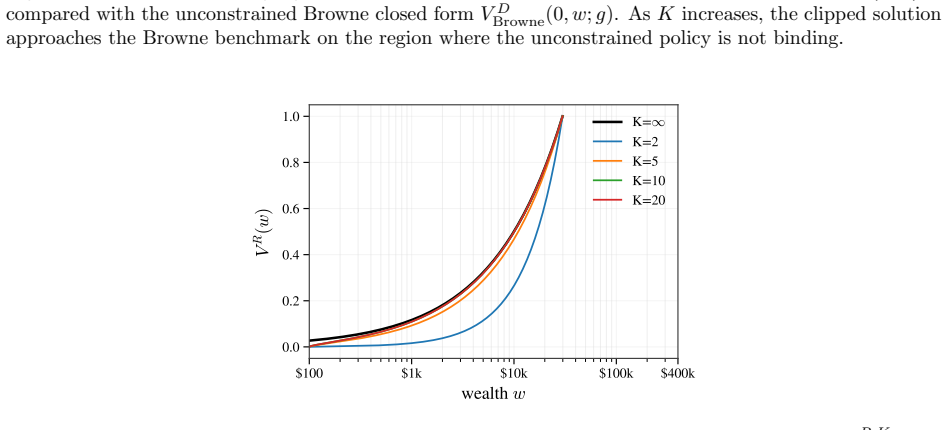

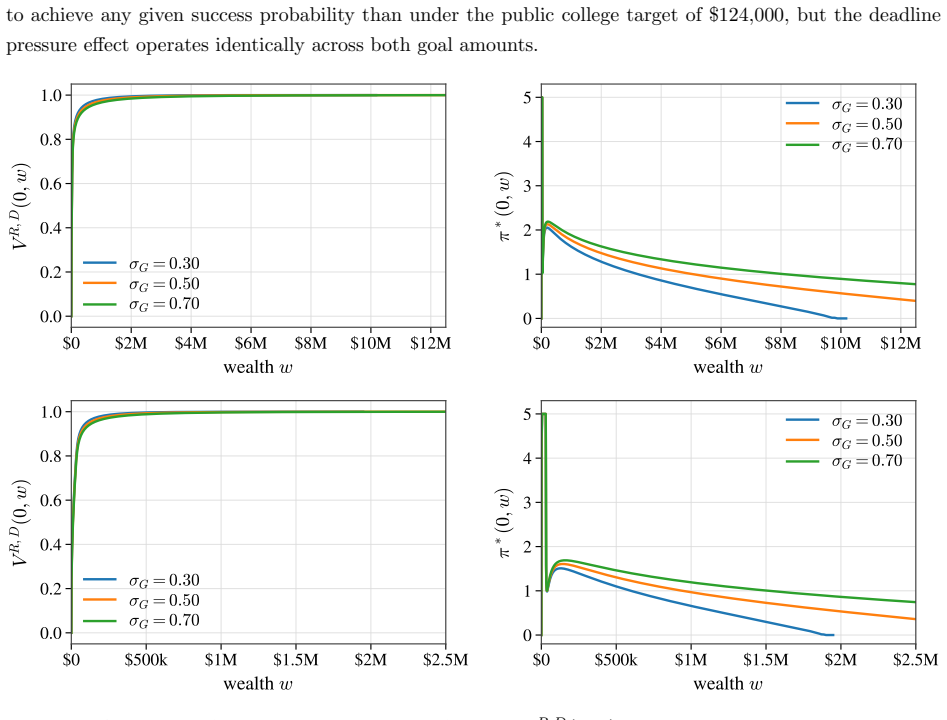

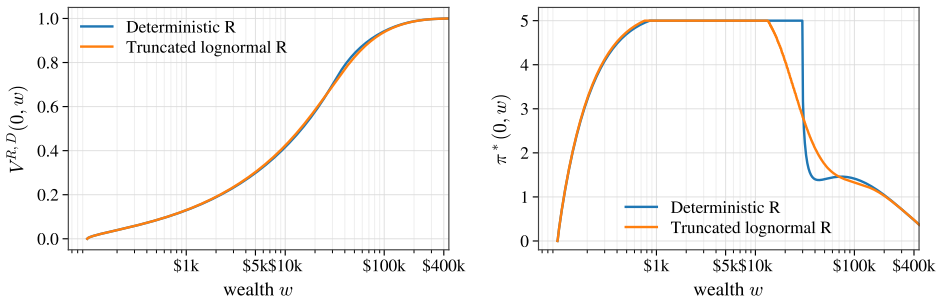

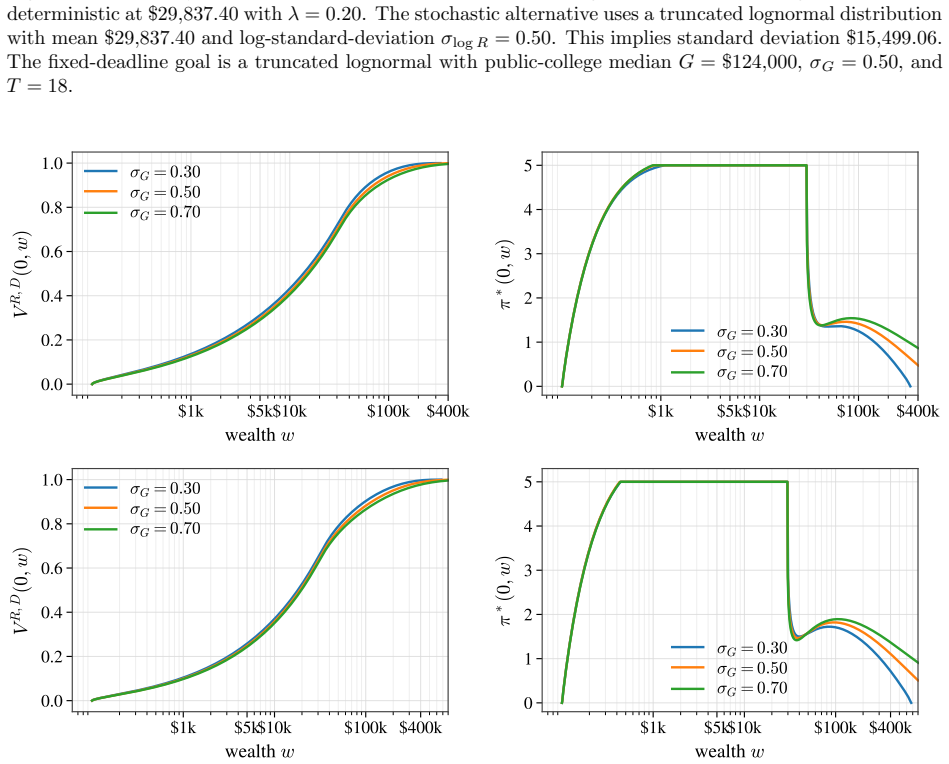

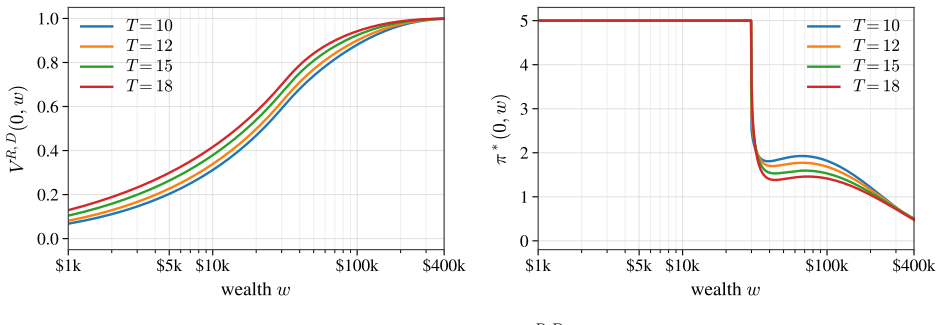

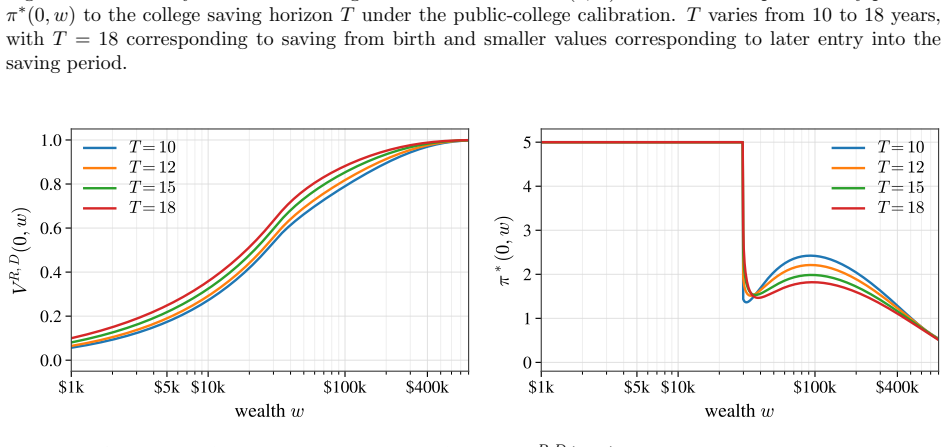

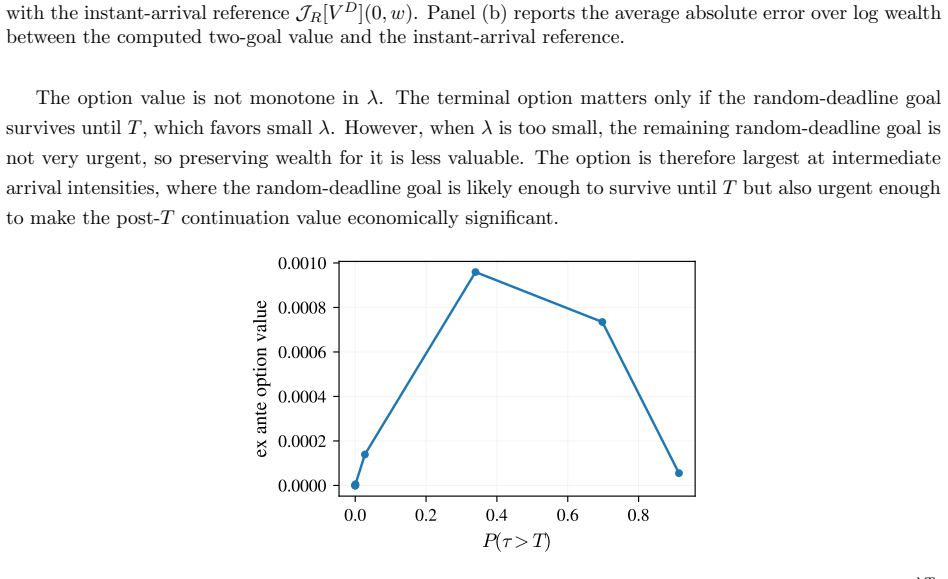

Under forced funding of both a random-deadline goal and a fixed-deadline goal, the household maximizes a weighted sum of the probabilities of fully funding each goal. The resulting value function is not monotone in wealth: a household just above the random-goal threshold is forced to pay it when the shock arrives, depleting its wealth for the fixed goal and ending up worse off than a slightly poorer household that missed the random goal. This non-monotonicity is absent from single-goal benchmarks and arises purely from the interaction between the two goal types. The model also identifies a growth crowding-out effect in which precautionary saving distorts investment and a deadline pressure ef

What carries the argument

The forced funding rule, under which each goal is paid in full whenever the household's wealth meets or exceeds the required amount at shock arrival or deadline.

If this is right

- The value function exhibits non-monotonicity in wealth near the random-goal threshold.

- Precautionary saving for the random goal crowds out investment suited to the fixed goal.

- A shorter effective saving horizon forces households to accept higher risk.

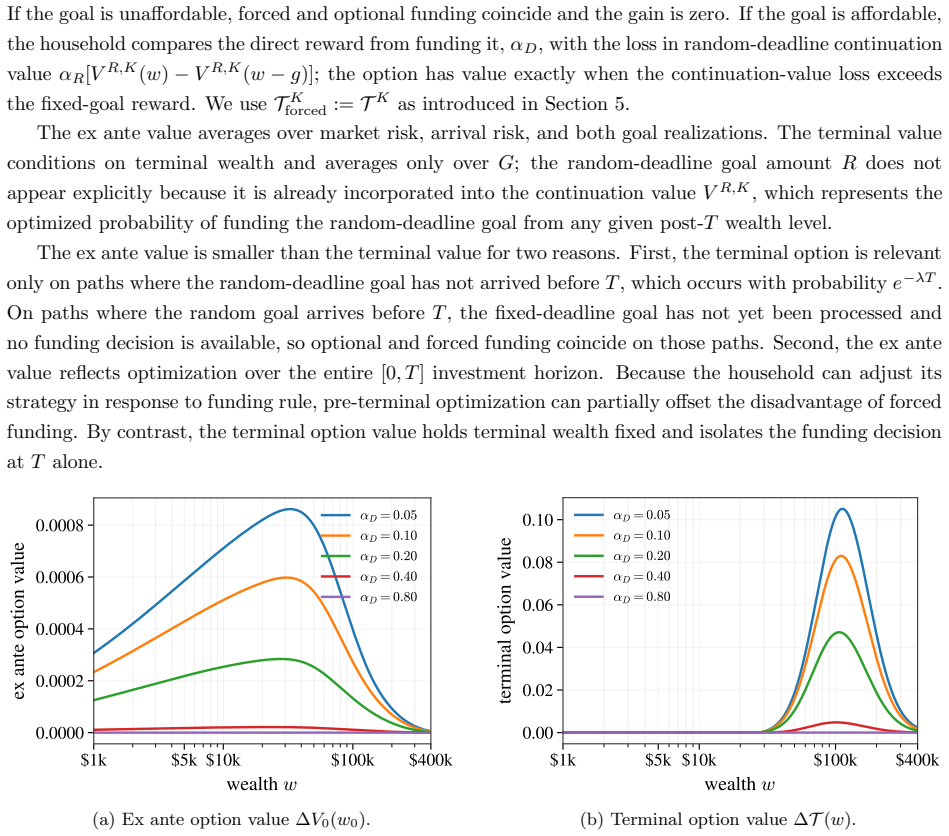

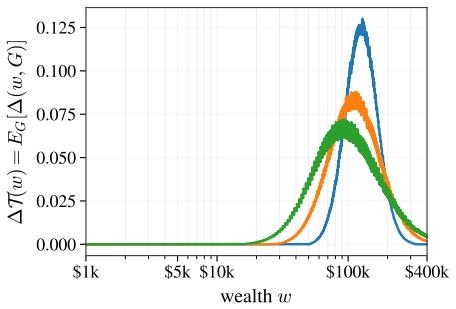

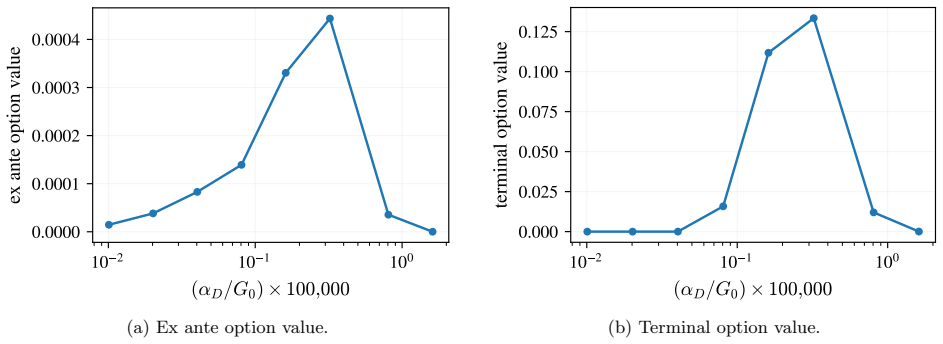

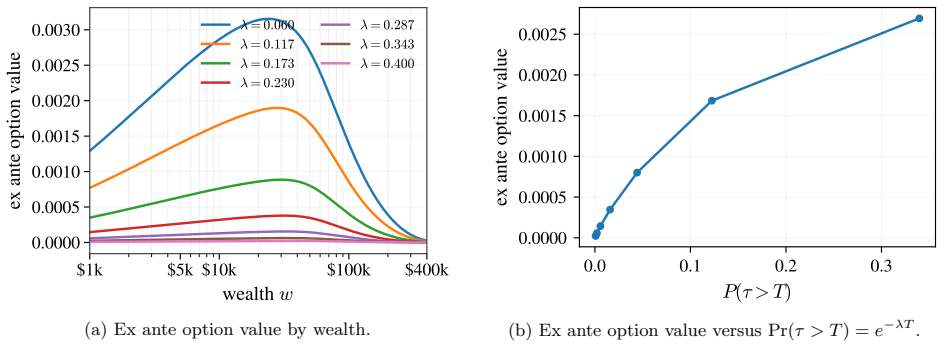

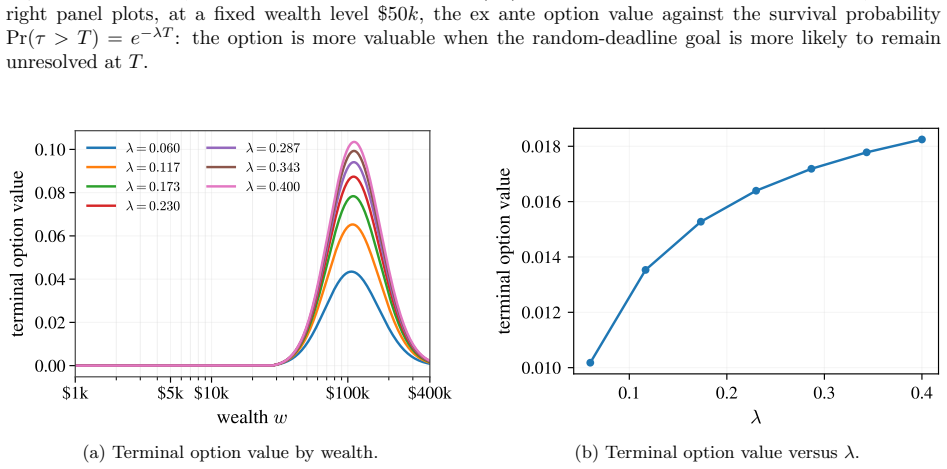

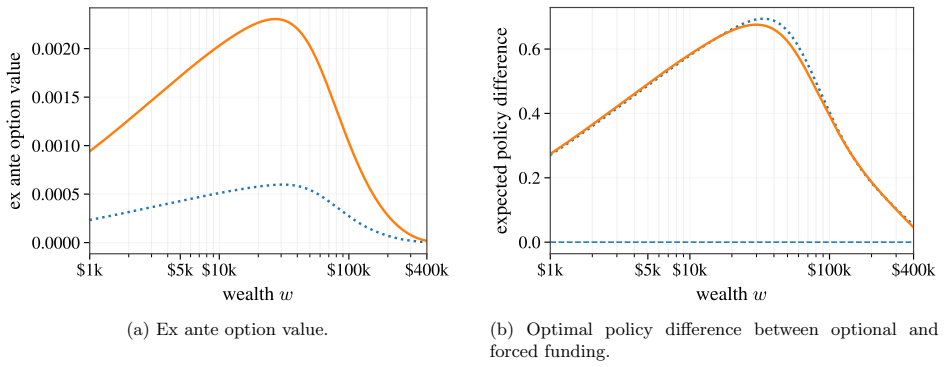

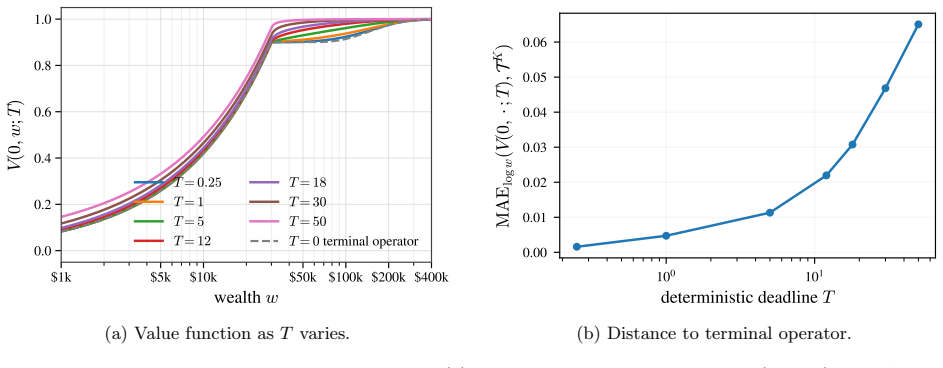

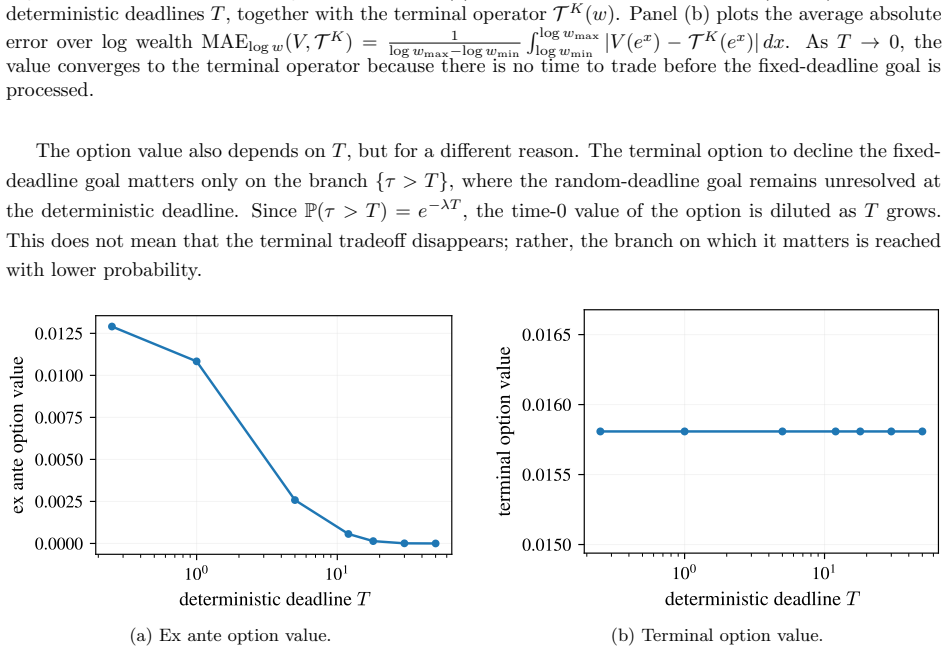

- The option to decline the fixed goal at the terminal date is most valuable at intermediate wealth levels.

Where Pith is reading between the lines

- Allowing households to choose the timing or size of goal payments could eliminate the non-monotonicity.

- Empirical tests of household portfolios should separate single-goal from dual-goal cases to detect crowding-out patterns.

- Policy designs that provide flexibility in goal funding may raise welfare by avoiding forced depletion effects.

Load-bearing premise

The forced funding rule is imposed exogenously rather than chosen by the household itself.

What would settle it

A numerical solution or controlled simulation that tracks the value function across wealth levels straddling the random-goal threshold and checks whether it decreases when crossing the threshold under forced funding.

Figures

read the original abstract

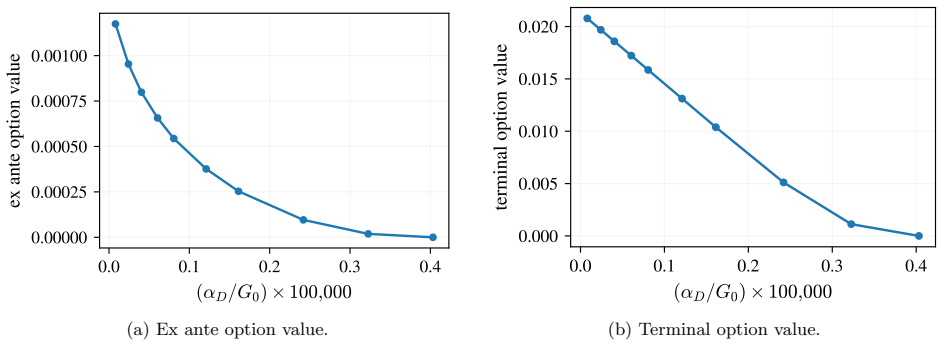

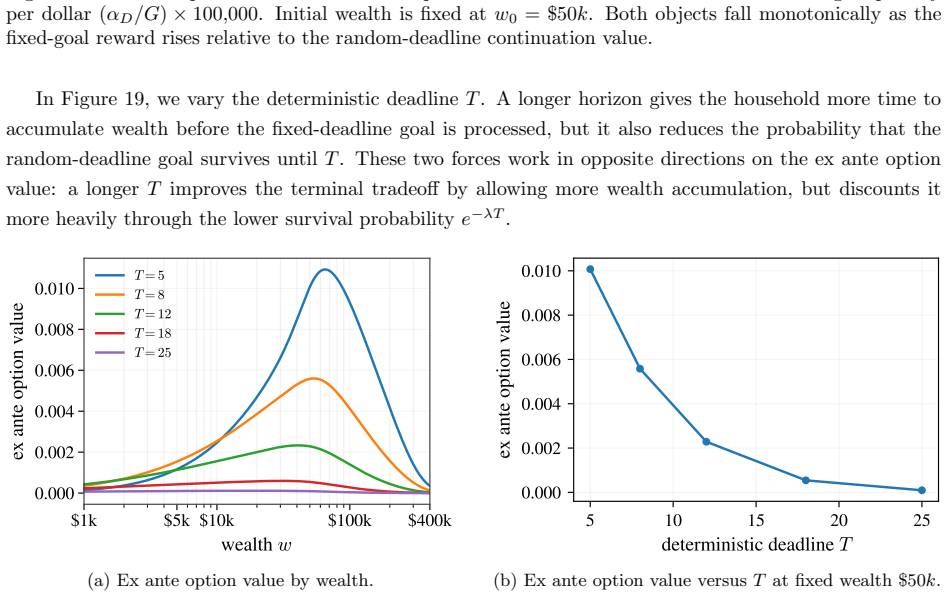

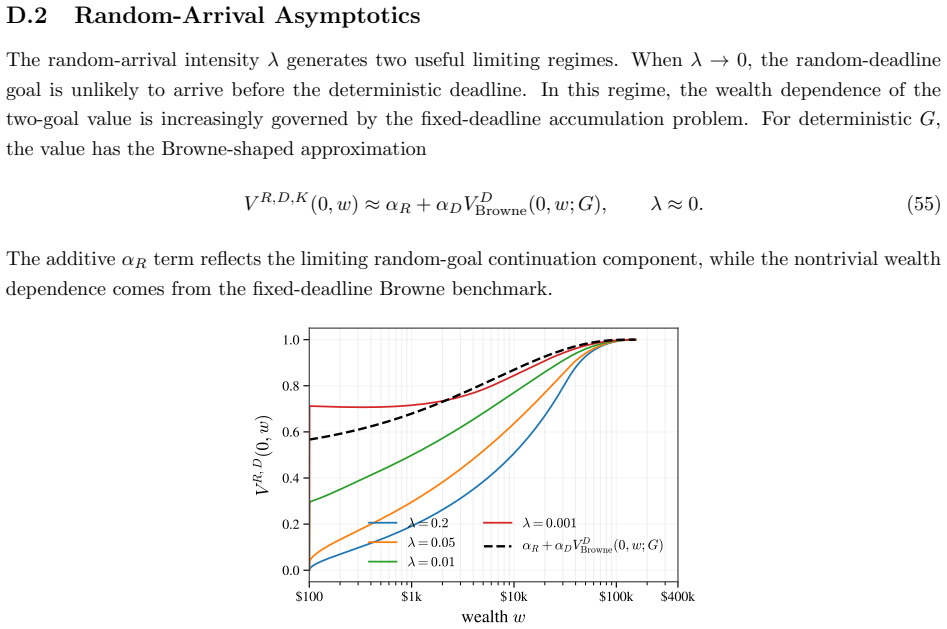

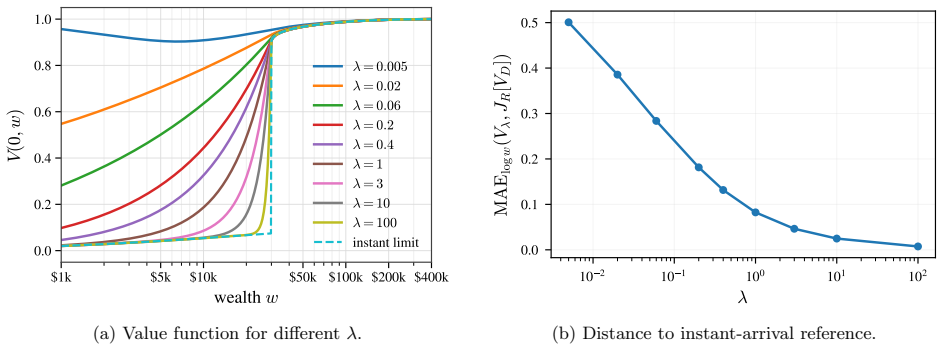

We study optimal portfolio choice for a household simultaneously managing a random-deadline goal, such as a medical emergency or job loss, and a fixed-deadline goal such as retirement or college tuition. Under a forced funding rule, in which each goal is paid in full whenever affordable, the household maximizes a weighted sum of the probabilities of fully funding both goals in a Black--Scholes market. We identify two novel effects absent from single-goal models: a growth crowding-out effect, in which precautionary saving for the random goal distorts investment toward the fixed goal, and a deadline pressure effect, in which a compressed saving horizon forces excess risk-taking. A striking implication is that the value function need not be monotone in wealth: a household just above the random-goal threshold is forced to pay it when the shock arrives, depleting its wealth for the fixed goal, and ends up worse off than a slightly poorer household that missed the random goal but kept its wealth intact. This non-monotonicity is absent from all single-goal benchmarks and arises purely from the interaction between the two goal types under forced funding. We further study an optional funding variant in which the household may decline the fixed-deadline goal at time $T$ rather than being required to fund it. We characterize the ex ante option value, i.e., the full time-$0$ value of this flexibility and the terminal option value, i.e., its value at the funding decision node. We find that both options are most valuable at intermediate wealth levels where paying the fixed-deadline goal would substantially reduce the continuation value of the random-deadline problem.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper studies optimal portfolio choice in a Black-Scholes market for a household simultaneously pursuing a random-deadline goal (e.g., medical emergency) and a fixed-deadline goal (e.g., retirement), maximizing a weighted sum of funding probabilities under an exogenous forced full-funding rule. It identifies a growth crowding-out effect and a deadline pressure effect, shows that the value function is non-monotone in wealth due to the interaction of the two goals, and analyzes the ex ante and terminal option values of an optional-funding variant for the fixed goal.

Significance. If the modeling assumptions hold, the work contributes to multi-goal portfolio choice by isolating interaction effects absent from single-goal benchmarks, including the novel non-monotonicity result and the characterization of option values being highest at intermediate wealth levels. The first-principles stochastic-control derivation in a standard market setting is a strength.

major comments (2)

- [§2] §2: The forced full-funding rule for the random goal is imposed exogenously rather than derived from the household's optimization problem. This rule is load-bearing for the central non-monotonicity claim (a household just above the threshold ends up worse off than one below), yet the paper provides no robustness analysis under endogenous choice, delay, or partial funding for the random goal (the optional variant in §5 applies only to the fixed goal at T).

- [Abstract, §5] Abstract and §5: The non-monotonicity and crowding-out results are presented as arising purely from the goal interaction under forced funding, but without reported verification that the non-monotonicity survives reasonable perturbations to parameters such as goal sizes, arrival intensities, or risk aversion (as would be needed to confirm it is not an artifact of specific modeling choices).

minor comments (1)

- [§2] Notation for the two value functions and the weighting parameter could be introduced more explicitly at the start of §2 to improve readability.

Simulated Author's Rebuttal

We thank the referee for the constructive comments. We address the two major comments point by point below. We agree that additional discussion and robustness checks would strengthen the paper and will revise accordingly.

read point-by-point responses

-

Referee: §2: The forced full-funding rule for the random goal is imposed exogenously rather than derived from the household's optimization problem. This rule is load-bearing for the central non-monotonicity claim (a household just above the threshold ends up worse off than one below), yet the paper provides no robustness analysis under endogenous choice, delay, or partial funding for the random goal (the optional variant in §5 applies only to the fixed goal at T).

Authors: The forced full-funding rule is an exogenous modeling assumption that captures situations where goals like medical emergencies require immediate full funding if affordable. This assumption is central to the non-monotonicity because it triggers wealth depletion upon goal arrival. The paper's focus is on analyzing the portfolio choice and value function under this rule, which is a standard approach in goal-based portfolio optimization. An endogenous funding model would be a valuable extension but would require a different setup. We will revise the manuscript to include a discussion of this limitation and potential implications of relaxing the assumption in the concluding section. revision: partial

-

Referee: Abstract and §5: The non-monotonicity and crowding-out results are presented as arising purely from the goal interaction under forced funding, but without reported verification that the non-monotonicity survives reasonable perturbations to parameters such as goal sizes, arrival intensities, or risk aversion (as would be needed to confirm it is not an artifact of specific modeling choices).

Authors: While the non-monotonicity is a structural consequence of the forced funding interaction—specifically, the forced payment depleting resources for the fixed goal—we acknowledge the value of explicit robustness checks. The analytical derivation shows the effect holds generally, but to address the referee's concern, we will add numerical sensitivity analysis in the revised version, varying key parameters like goal sizes, arrival rates, and risk aversion to confirm the persistence of non-monotonicity and crowding-out effects. revision: yes

Circularity Check

No significant circularity; first-principles stochastic-control derivation

full rationale

The paper sets up a stochastic control problem in Black-Scholes with an exogenous forced-funding rule as a modeling assumption, then derives the value function, crowding-out and deadline-pressure effects, and non-monotonicity as consequences of the interaction between the two goal types. No fitted parameters are renamed as predictions, no self-citations are invoked as load-bearing uniqueness theorems, and no ansatz is smuggled via prior work. The non-monotonicity result follows directly from the state jumps induced by the rule and is not equivalent to the inputs by construction. The derivation is self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Black-Scholes market dynamics with constant coefficients

- domain assumption Forced funding rule is imposed exogenously

Reference graph

Works this paper leans on

-

[1]

Brookings Papers on Economic Activity , year =

Lusardi, Annamaria and Schneider, Daniel and Tufano, Peter , title =. Brookings Papers on Economic Activity , year =

-

[2]

, title =

Fulford, Scott L. , title =. Journal of Monetary Economics , year =

-

[3]

and Natvik, Gisle J

Fagereng, Andreas and Holm, Martin B. and Natvik, Gisle J. , title =. American Economic Journal: Macroeconomics , year =

-

[4]

2025 , url =

Real-Life Data: An Innovative Approach to Calculating Income Replacement Rates , institution =. 2025 , url =

2025

-

[5]

arXiv preprint arXiv:2506.06654 , year=

Goal-based portfolio selection with mental accounting , author=. arXiv preprint arXiv:2506.06654 , year=

-

[6]

Advances in Applied Probability , year =

Sid Browne , title =. Advances in Applied Probability , year =

-

[7]

Jean L. P. Brunel , title =

-

[8]

Management Science , year =

Agostino Capponi and Yuchong Zhang , title =. Management Science , year =

-

[9]

Chhabra , title =

Ashvin B. Chhabra , title =. The Journal of Wealth Management , year =

-

[10]

Rossi , title =

Francesco D'Acunto and Alberto G. Rossi , title =. Annual Review of Financial Economics , year =

-

[11]

Journal of Financial and Quantitative Analysis , year =

Sanjiv Das and Harry Markowitz and Jonathan Scheid and Meir Statman , title =. Journal of Financial and Quantitative Analysis , year =

-

[12]

Das and Daniel Ostrov and Anand Radhakrishnan and Deep Srivastav , title =

Sanjiv R. Das and Daniel Ostrov and Anand Radhakrishnan and Deep Srivastav , title =. Journal of Banking and Finance , year =

-

[13]

Rossi , title =

Francesco D'Acunto and Nagpurnanand Prabhala and Alberto G. Rossi , title =. Review of Financial Studies , year =

-

[14]

The Journal of Finance , year =

Harry Markowitz , title =. The Journal of Finance , year =

-

[15]

Journal of Financial Economics , year =

Michael Reher and Stanislav Sokolinski , title =. Journal of Financial Economics , year =

-

[16]

Journal of Financial and Quantitative Analysis , year =

Hersh Shefrin and Meir Statman , title =. Journal of Financial and Quantitative Analysis , year =

-

[17]

The Journal of Finance , year =

Lettau, Martin and Ludvigson, Sydney , title =. The Journal of Finance , year =

-

[18]

2025 , month =

Ma, Jennifer and Pender, Matea and Hu, Xiaowen , title =. 2025 , month =

2025

-

[19]

, title =

Lusardi, Annamaria and Mitchell, Olivia S. , title =. Journal of Monetary Economics , year =

-

[20]

Consumer Expenditure Survey Anthology, 2003 , publisher =

Duly, Abby , title =. Consumer Expenditure Survey Anthology, 2003 , publisher =. 2003 , pages =

2003

-

[21]

Journal of Political Economy , year =

Scholz, John Karl and Seshadri, Ananth and Khitatrakun, Surachai , title =. Journal of Political Economy , year =

-

[22]

, title =

Mehra, Rajnish and Prescott, Edward C. , title =. Journal of Monetary Economics , year =

-

[23]

The Real Deal: 2012 Retirement Income Adequacy at Large Companies , institution =

2012

-

[24]

Foundations of modern probability , author=

-

[25]

2017 , publisher=

Enlargement of filtration with finance in view , author=. 2017 , publisher=

2017

-

[26]

Lifetime ruin under ambiguous hazard rate , journal =. 2016 , issn =. doi:https://doi.org/10.1016/j.insmatheco.2016.06.007 , url =

-

[27]

, title =

D'Acunto, Francesco and Rossi, Alberto G. , title =. Machine Learning and Data Sciences for Financial Markets: A Guide to Contemporary Practices , editor =

-

[28]

North American Actuarial Journal , year=2004, volume=

Virginia Young , title=. North American Actuarial Journal , year=2004, volume=. doi:10.1080/10920277.2004.10596174 , url=

-

[29]

Insurance: Mathematics and Economics , volume=

Optimally investing to reach a bequest goal , author=. Insurance: Mathematics and Economics , volume=. 2016 , publisher=

2016

-

[30]

Bulletin of the American mathematical society , volume=

User’s guide to viscosity solutions of second order partial differential equations , author=. Bulletin of the American mathematical society , volume=

-

[31]

Mathematics of Operations Research , volume=

Survival and growth with a liability: Optimal portfolio strategies in continuous time , author=. Mathematics of Operations Research , volume=. 1997 , publisher=

1997

-

[32]

2009 , publisher=

Continuous-time stochastic control and optimization with financial applications , author=. 2009 , publisher=

2009

-

[33]

Optimal stochastic control, stochastic target problems, and backward

Touzi, Nizar , volume=. Optimal stochastic control, stochastic target problems, and backward. 2013 , publisher=

2013

-

[34]

and Border, Kim C

Aliprantis, Charalambos D. and Border, Kim C. , title =

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.