Interdependent Hitting Times

Pith reviewed 2026-06-27 22:47 UTC · model grok-4.3

The pith

Equilibrium outcomes in synchronization games can be represented as interdependent hitting times of a common shock process.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Equilibrium outcomes of the synchronization game can be represented as interdependent hitting times and this representation establishes the game's nonparametric identification from data on stopping times and covariates.

What carries the argument

The representation of equilibrium stopping profiles as interdependent hitting times of the spectrally negative Lévy common shock process.

If this is right

- The payoffs and distributions of the synchronization game are nonparametrically identified from stopping times and covariates.

- Maximum simulated likelihood and method of simulated moments estimators recover the identified objects.

- The framework applies directly to any interdependent duration data generated by strategic complementarities in stopping.

Where Pith is reading between the lines

- The same hitting-time representation may apply to other continuous-time games with strategic complementarities once the shock process satisfies the required properties.

- Empirical work on joint technology adoption or market-entry timing could use the estimators once stopping times and covariates are observed.

Load-bearing premise

The common shocks follow a spectrally negative Lévy process.

What would settle it

A data set in which observed stopping patterns cannot be expressed as hitting times of any spectrally negative Lévy process would falsify the representation.

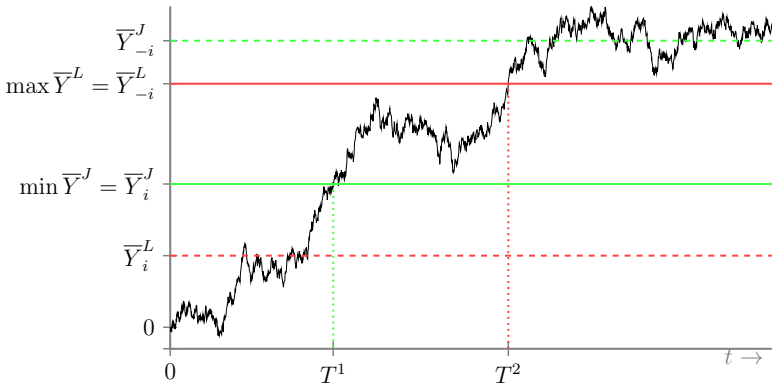

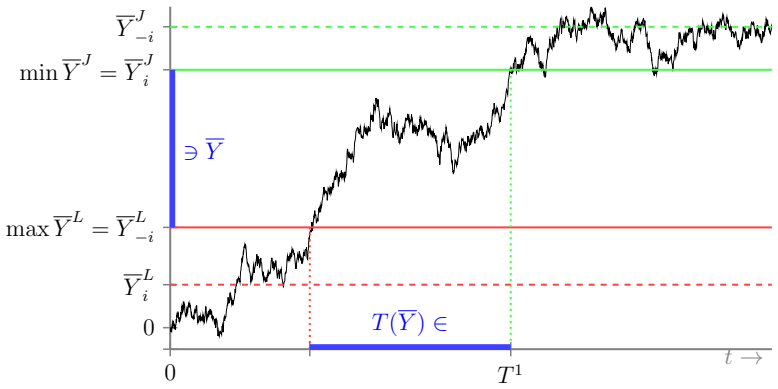

Figures

read the original abstract

This paper studies interdependent durations as equilibrium outcomes of a synchronization game, a continuous-time stopping game in which the incentive to stop increases when other players stop. We allow the payoffs to vary with both common shocks and observed and unobserved agent characteristics. The common shocks follow a spectrally negative L\'evy process, a semiparametric process that includes Brownian motion as a special case but may also have jumps. We show that equilibrium outcomes can be represented as interdependent hitting times and use this to establish the game's nonparametric identification from data on stopping times and covariates. We develop maximum simulated likelihood and method of simulated moments estimators and evaluate their finite-sample and computational performance in Monte Carlo experiments. The results provide a tractable framework for identifying and estimating synchronization games from interdependent duration data.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. This paper studies interdependent durations as equilibrium outcomes of a synchronization game, a continuous-time stopping game in which the incentive to stop increases when other players stop. Payoffs vary with common shocks (modeled as a spectrally negative Lévy process, including Brownian motion as a special case), observed covariates, and unobserved agent characteristics. The central claim is that equilibrium outcomes admit a representation as interdependent hitting times, which is then used to establish nonparametric identification of the game from data on stopping times and covariates. The authors develop maximum simulated likelihood and method of simulated moments estimators and evaluate their finite-sample and computational performance via Monte Carlo experiments.

Significance. If the representation and identification results hold, the paper supplies a tractable semiparametric framework for modeling and recovering parameters of synchronization games from interdependent duration data. The explicit use of spectrally negative Lévy processes to accommodate jumps alongside diffusion is a constructive extension beyond standard Brownian-motion setups in duration models. The combination of a hitting-time representation, nonparametric identification, and practical estimators with Monte Carlo validation offers both theoretical and applied value for empirical work on technology adoption, market timing, or other synchronized decisions.

minor comments (3)

- The Monte Carlo section would benefit from explicit reporting of the number of replications, the exact parameter values in the data-generating process, and quantitative measures of computational time or convergence for the MSL and MSM estimators.

- In the identification argument, the mapping from the scale function of the Lévy process to the observed joint distribution of stopping times could be stated more explicitly (e.g., the precise inversion step that recovers the payoff parameters from the hitting-time distribution).

- Notation for the scale function and the interdependence operator should be cross-referenced to standard Lévy-process references to improve accessibility for readers outside the immediate subfield.

Simulated Author's Rebuttal

We thank the referee for the positive and accurate summary of our paper, the assessment of its significance, and the recommendation for minor revision. We are pleased that the contributions on the hitting-time representation, nonparametric identification, and the estimators are viewed as valuable.

Circularity Check

No significant circularity

full rationale

The paper states the spectrally negative Lévy process assumption explicitly as a modeling choice required for the scale-function arguments, then derives the interdependent hitting-times representation and nonparametric identification result from the equilibrium conditions inside that class. No load-bearing step reduces by construction to a fitted input, self-citation, or redefinition of the target quantity; the identification claim is presented as nonparametric from observed stopping times and covariates within the maintained assumptions. The argument is therefore self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Common shocks follow a spectrally negative Lévy process

Reference graph

Works this paper leans on

-

[1]

Abbring, J. H. (2010). Identification of dynamic discrete choice models. Annual Review of Economics\/ 2 , 367--394

2010

-

[2]

Abbring, J. H. (2012). Mixed hitting-time models. Econometrica\/ 80\/ (2), 783--819

2012

-

[3]

Abbring, J. H. and T. Salimans (2021). The likelihood of mixed hitting times. Journal of Econometrics\/ 223\/ (2), 361--375

2021

-

[4]

Abbring, J. H. and G. J. van den Berg (2003). The nonparametric identification of treatment effects in duration models. Econometrica\/ 71\/ (5), 1491--1517

2003

-

[5]

Abbring, J. H. and Y. Yu (2026). Supplement to `` I nterdependent hitting times''. Working paper, Tilburg University. arXiv:2606.06251 https://arxiv.org/abs/2606.06251 [econ.EM]

Pith/arXiv arXiv 2026

-

[6]

Bayer, J

Arcidiacono, P., P. Bayer, J. R. Blevins, and P. B. Ellickson (2016). Estimation of dynamic discrete choice models in continuous time with an application to retail competition. Review of Economic Studies\/ 83\/ (3), 889--931

2016

-

[7]

Boyarchenko, S. and S. Levendorski (2005). American options: The EPV pricing model. Annals of Finance\/ 1 , 267--292

2005

-

[8]

Boyarchenko, S. and S. Levendorski (2007). Irreversible Decisions under Uncertainty: O ptimal Stopping Made Easy . Berlin: Springer-Verlag

2007

-

[9]

Chen, S. (2010). Non-parametric identification and estimation of truncated regression models. Review of Economic Studies\/ 77\/ (1), 127--153

2010

-

[10]

Cont, R. and P. Tankov (2004). Financial Modelling with Jump Processes , Volume 2. Chapman & Hall

2004

-

[11]

de Paula , A. (2009). Inference in a synchronization game with social interactions. Journal of Econometrics\/ 148\/ (1), 56--71

2009

-

[12]

Dixit, A. and R. Pindyck (1994). Investment under Uncertainty . Princeton University Press

1994

-

[13]

Doraszelski, U. and K. L. Judd (2012). Avoiding the curse of dimensionality in dynamic stochastic games. Quantitative Economics\/ 3\/ (1), 53--93

2012

-

[14]

Feller, W. (1971). An Introduction to Probability Theory and its Applications , Volume II. New York: Wiley

1971

-

[15]

Fudenberg, D. and J. Tirole (1985). Preemption and rent equalization in the adoption of new technology. Review of Economic Studies\/ 52\/ (3), 383--401

1985

-

[16]

Fudenberg, D. and J. Tirole (1986). A theory of exit in duopoly. Econometrica\/ 54\/ (4), 943--960

1986

-

[17]

Gourieroux, C. and A. Monfort (1996). Simulation-Based Econometric Methods . Oxford University Press

1996

-

[18]

Hajivassiliou, V. A. and P. A. Ruud (1994). Classical estimation methods for LDV models using simulation. In Handbook of Econometrics , Volume 4, pp.\ 2383--2441. Elsevier

1994

-

[19]

Honor\' e , B. and A. de Paula (2010). Interdependent durations. Review of Economic Studies\/ 77\/ (3), 1138--1163

2010

-

[20]

Honor\' e , B. E. and A. de Paula (2018). A new model for interdependent durations. Quantitative Economics\/ 9\/ (3), 1299--1333

2018

-

[21]

Kyprianou, A. (2006). Introductory Lectures on Fluctuations of L \' e vy Processes with Applications . Springer Verlag

2006

-

[22]

Lin, Z. and R. Liu (2021). A mulitplex interdependent durations model. Econometric Theory\/ 37\/ (6), 1238--1266

2021

-

[23]

Manski, C. (1993). Identification of endogenous social effects: T he reflection problem. Review of Economic Studies\/ 60\/ (3), 531--542

1993

-

[24]

Murto, P. (2004). Exit in duopoly under uncertainty. The RAND Journal of Economics\/ 35\/ (1), 111--127

2004

-

[25]

Ridder, G. (1990). The non-parametric identification of generalized accelerated failure-time models. Review of Economic Studies\/ 57\/ (2), 167--181

1990

-

[26]

Simon, L. K. and M. B. Stinchcombe (1989). Extensive form games in continuous time: Pure strategies. Econometrica\/ 57\/ (5), 1171--1214

1989

-

[27]

Stokey, N. (2009). The Economics of Inaction: S tochastic Control Models with Fixed Costs . Princeton University Press

2009

-

[28]

Tamer, E. (2003). Incomplete simultaneous discrete response model with multiple equilibria. Review of Economic Studies\/ 70\/ (1), 147--165

2003

-

[29]

Vitorino, M. A. (2012). Empirical entry games with complementarities: A n application to the shopping center industry. Journal of Marketing Research\/ 49\/ (2), 175--191

2012

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.