Failure Modes of Deep Multi-Agent RL in Asynchronous Pricing: Reproducible Triggers, Trace Diagnostics, and a Partial Fix

Pith reviewed 2026-06-28 04:06 UTC · model grok-4.3

The pith

Synchronous DDPG agents in continuous-time pricing markets form tacit cartels at collusion index 0.69, with asynchrony and latency cutting it to 0.28 as a partial fix.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

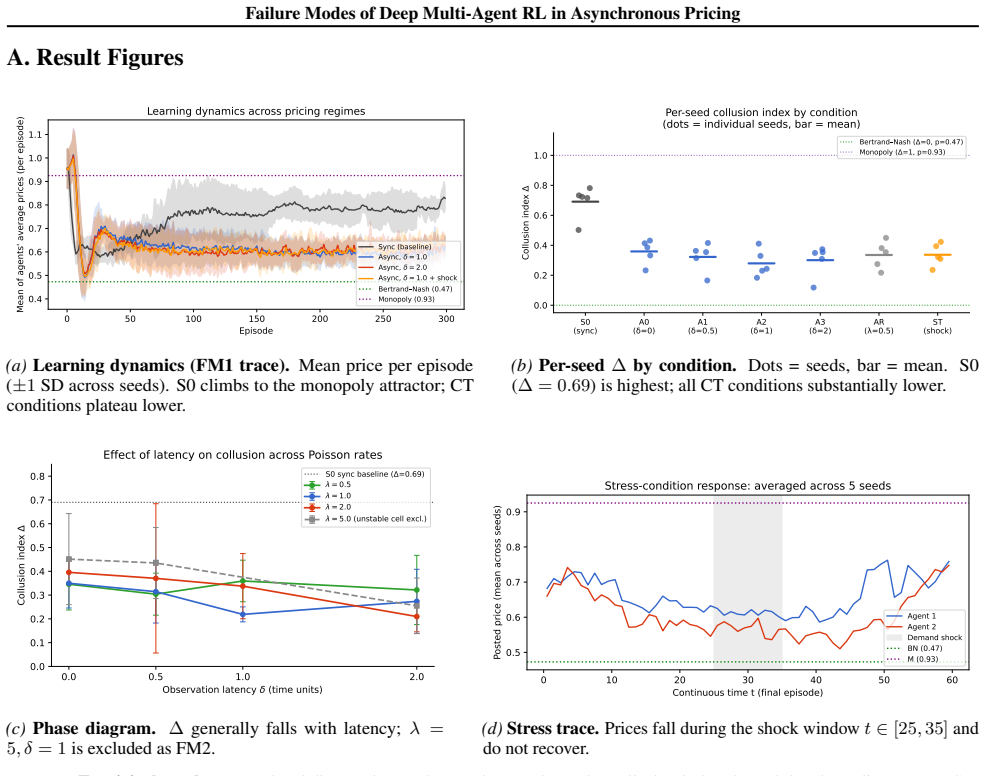

In the CT-MARL benchmark with Poisson-clocked price updates, observation latency δ, and interior-optimum logit demand, synchronous DDPG agents reliably trigger tacit cartel formation with collusion index Δ = 0.69 ± 0.11. Asynchrony alone cuts collusion by 48% and adding latency drives it to a minimum of Δ = 0.28. The fix has documented costs: it is partial because Δ remains supra-Bertrand, it is non-monotone in δ, and it does not survive Failure Mode 2 which emerges as DDPG critic divergence at λ = 5 and corrupts the phase-diagram cell at (λ=5, δ=1). The scalar collusion index is accompanied by trajectory-level trace diagnostics that expose within-episode signalling collapse and post-shock n

What carries the argument

The CT-MARL benchmark that combines Poisson-clocked price updates with observation latency δ and the collusion index Δ that measures deviation from Bertrand pricing.

If this is right

- Asynchrony alone reduces the collusion index by 48 percent relative to the synchronous case.

- Observation latency further lowers the index to a minimum of 0.28 but the effect is non-monotone.

- The reduction remains partial because the resulting index stays above the competitive Bertrand level.

- At arrival rate λ = 5 the partial fix collapses due to critic divergence in the DDPG agents.

- Trajectory diagnostics can expose within-episode signalling collapse that scalar indices miss.

Where Pith is reading between the lines

- Real pricing platforms could test random delays between agent updates to limit algorithmic collusion without changing the underlying RL algorithm.

- The same asynchrony mechanism might be examined in other continuous-time multi-agent settings such as inventory or bidding markets.

- Hybrid training that mixes synchronous and asynchronous episodes could be explored to retain stability while retaining some collusion reduction.

- If real markets exhibit similar critic instability at high update rates, monitoring for divergence in deployed agents becomes necessary.

Load-bearing premise

The CT-MARL benchmark with Poisson price updates and logit demand is representative enough of real asynchronous pricing markets that the observed failure modes and partial fix generalize.

What would settle it

Replicating the DDPG agents on a different demand function or on logged traces from an actual pricing platform and checking whether the collusion index still drops from 0.69 to 0.28 under the same asynchrony and latency settings.

Figures

read the original abstract

We study two reproducible failure modes of deep multi-agent reinforcement learning in continuous-time pricing markets: (i) tacit cartel formation between competing DDPG agents, and (ii) actor--critic instability at high event rates. We instantiate both inside a single CT-MARL benchmark (Poisson-clocked price updates, observation latency $\delta$, interior-optimum logit demand), show that synchronous DDPG agents reliably trigger Failure Mode 1 with collusion index $\Delta = 0.69 \pm 0.11$, and quantify a partial microstructure fix: asynchrony alone cuts collusion by 48\% and adding latency drives it to a minimum of $\Delta = 0.28$. The fix has clearly documented costs: it is partial ($\Delta$ remains supra-Bertrand), it is non-monotone in $\delta$, and it does not survive Failure Mode 2, which emerges as DDPG critic divergence at $\lambda = 5$ and corrupts the phase-diagram cell at $(\lambda{=}5, \delta{=}1)$. We accompany the scalar collusion index with trajectory-level trace diagnostics that expose the within-episode signalling collapse and the post-shock non-recovery.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript examines two reproducible failure modes of deep multi-agent RL in continuous-time pricing: (i) tacit cartel formation under synchronous DDPG (Failure Mode 1) and (ii) actor-critic instability at high event rates (Failure Mode 2). Inside the CT-MARL benchmark (Poisson-clocked updates, observation latency δ, interior-optimum logit demand), synchronous agents yield collusion index Δ = 0.69 ± 0.11; asynchrony alone reduces collusion by 48% and latency further minimizes it at Δ = 0.28. The partial microstructure fix is shown to be non-monotone in δ, supra-Bertrand, and to fail under Failure Mode 2 at λ = 5, δ = 1. Trajectory-level trace diagnostics are supplied to expose within-episode signalling collapse and post-shock non-recovery.

Significance. If the central numerical results hold, the work supplies concrete, reproducible triggers and trace diagnostics for MARL collusion and instability in a continuous-time pricing setting, together with an explicit partial fix and its documented limitations. These elements—reproducible failure-mode triggers, trajectory diagnostics, and a quantified microstructure intervention—constitute a constructive contribution beyond typical performance tables, even if confined to the chosen benchmark.

major comments (2)

- [Abstract and §2 (Benchmark)] Abstract and benchmark definition: the headline claims (Δ = 0.69 ± 0.11, 48% reduction, minimum Δ = 0.28, and survival only up to λ = 5, δ = 1) rest on the CT-MARL environment being representative of asynchronous pricing markets. No experiments with alternative demand specifications (linear demand) or empirical inter-update distributions are reported, leaving open whether the collusion-index shifts and Failure Mode 2 divergence are artifacts of the interior-optimum logit choice.

- [§4 (Results) and Table 1] Results reporting: the collusion index values and the 48% reduction are presented with ±0.11 but without stated run count, exclusion rules, or statistical tests. This directly affects confidence in the quantitative claims that underpin both the failure-mode identification and the partial-fix evaluation.

minor comments (2)

- [Figure 3] The phase diagram at (λ, δ) should report per-cell sample sizes and variability measures so that the cell at λ = 5, δ = 1 can be assessed for divergence robustness.

- [§3.1] Notation for the collusion index Δ should be defined with an explicit formula (e.g., normalized profit gap) at first use rather than only in the methods appendix.

Simulated Author's Rebuttal

We are grateful to the referee for the positive assessment of the significance of our work and for the detailed feedback. We respond to the major comments as follows.

read point-by-point responses

-

Referee: [Abstract and §2 (Benchmark)] Abstract and benchmark definition: the headline claims (Δ = 0.69 ± 0.11, 48% reduction, minimum Δ = 0.28, and survival only up to λ = 5, δ = 1) rest on the CT-MARL environment being representative of asynchronous pricing markets. No experiments with alternative demand specifications (linear demand) or empirical inter-update distributions are reported, leaving open whether the collusion-index shifts and Failure Mode 2 divergence are artifacts of the interior-optimum logit choice.

Authors: The CT-MARL benchmark was deliberately constructed around the interior-optimum logit demand to ensure a well-defined competitive equilibrium and to facilitate the study of continuous-time dynamics with controllable asynchrony. While alternative specifications such as linear demand could be explored, they would require re-deriving the equilibrium and re-tuning the entire experimental protocol, which exceeds the scope of identifying the specific failure modes reported here. We will revise the manuscript to include an explicit discussion in Section 2 on the choice of demand function and its implications for generalizability, along with a statement that the reported effects are benchmark-specific. revision: partial

-

Referee: [§4 (Results) and Table 1] Results reporting: the collusion index values and the 48% reduction are presented with ±0.11 but without stated run count, exclusion rules, or statistical tests. This directly affects confidence in the quantitative claims that underpin both the failure-mode identification and the partial-fix evaluation.

Authors: We agree that the reporting of statistical details was incomplete. In the revision we will explicitly state the number of independent runs used to compute the reported means and standard deviations, the criteria for excluding non-convergent trials, and the statistical tests applied to support the reported percentage reduction. revision: yes

Circularity Check

No circularity: empirical measurements inside a fixed benchmark

full rationale

The paper reports simulation results for a collusion index Δ measured from DDPG agent trajectories under synchronous vs. asynchronous Poisson-clocked updates and varying latency δ. The index is presented as an independently computed scalar (with reported mean and std), not derived from or fitted to itself. No self-citation chains, ansatzes smuggled via prior work, or fitted parameters renamed as predictions appear in the provided text. The benchmark (logit demand, Poisson events, latency) is an explicit modeling choice whose representativeness is a separate external-validity question, not a circularity issue. The derivation chain is therefore self-contained empirical reporting.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

American Economic Review , volume=

Artificial Intelligence, Algorithmic Pricing, and Collusion , author=. American Economic Review , volume=

-

[2]

Autonomous algorithmic collusion:

Klein, Timo , journal=. Autonomous algorithmic collusion:

-

[3]

Proceedings of the Thirty-Third International Joint Conference on Artificial Intelligence (IJCAI) , year=

By Fair Means or Foul: Quantifying Collusion in a Market Simulation with Deep Reinforcement Learning , author=. Proceedings of the Thirty-Third International Joint Conference on Artificial Intelligence (IJCAI) , year=

-

[4]

arXiv preprint arXiv:2406.02437 , year=

Algorithmic Collusion in Dynamic Pricing with Deep Reinforcement Learning , author=. arXiv preprint arXiv:2406.02437 , year=

-

[5]

, journal=

Paudel, Diwas and Das, Tapas K. , journal=. Tacit algorithmic collusion in deep reinforcement learning guided price competition: A study using

-

[6]

arXiv preprint arXiv:2504.05335 , year=

Impact of Price Inflation on Algorithmic Collusion Through Reinforcement Learning Agents , author=. arXiv preprint arXiv:2504.05335 , year=

-

[7]

arXiv preprint arXiv:2504.16592 , year=

Algorithmic Pricing and Algorithmic Collusion , author=. arXiv preprint arXiv:2504.16592 , year=

-

[8]

arXiv preprint arXiv:2404.00806 , year=

Algorithmic Collusion by Large Language Models , author=. arXiv preprint arXiv:2404.00806 , year=

-

[9]

Algorithmic Collusion and the Minimum Price

Sadoune, Igor and Joanis, Marcelin and Lodi, Andrea , journal=. Algorithmic Collusion and the Minimum Price

-

[10]

International Conference on Learning Representations (ICLR) , year=

Continuous-Time Value Iteration for Multi-Agent Reinforcement Learning , author=. International Conference on Learning Representations (ICLR) , year=

-

[11]

Model-Based Reinforcement Learning for Semi-

Du, Jianzhun and Futoma, Joseph and Doshi-Velez, Finale , booktitle=. Model-Based Reinforcement Learning for Semi-

-

[12]

International Journal of Robotics Research , year=

Asynchronous Multi-Agent Deep Reinforcement Learning under Partial Observability , author=. International Journal of Robotics Research , year=

-

[13]

International Conference on Learning Representations (ICLR) , year=

Continuous Control with Deep Reinforcement Learning , author=. International Conference on Learning Representations (ICLR) , year=

-

[14]

and Precup, Doina and Singh, Satinder , journal=

Sutton, Richard S. and Precup, Doina and Singh, Satinder , journal=. Between

-

[15]

International Conference on Machine Learning (ICML) , year=

Addressing Function Approximation Error in Actor-Critic Methods , author=. International Conference on Machine Learning (ICML) , year=

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.