The Market Crystal: A Spin-Lattice Model for Collective Cryptocurrency States

Pith reviewed 2026-06-26 11:18 UTC · model grok-4.3

The pith

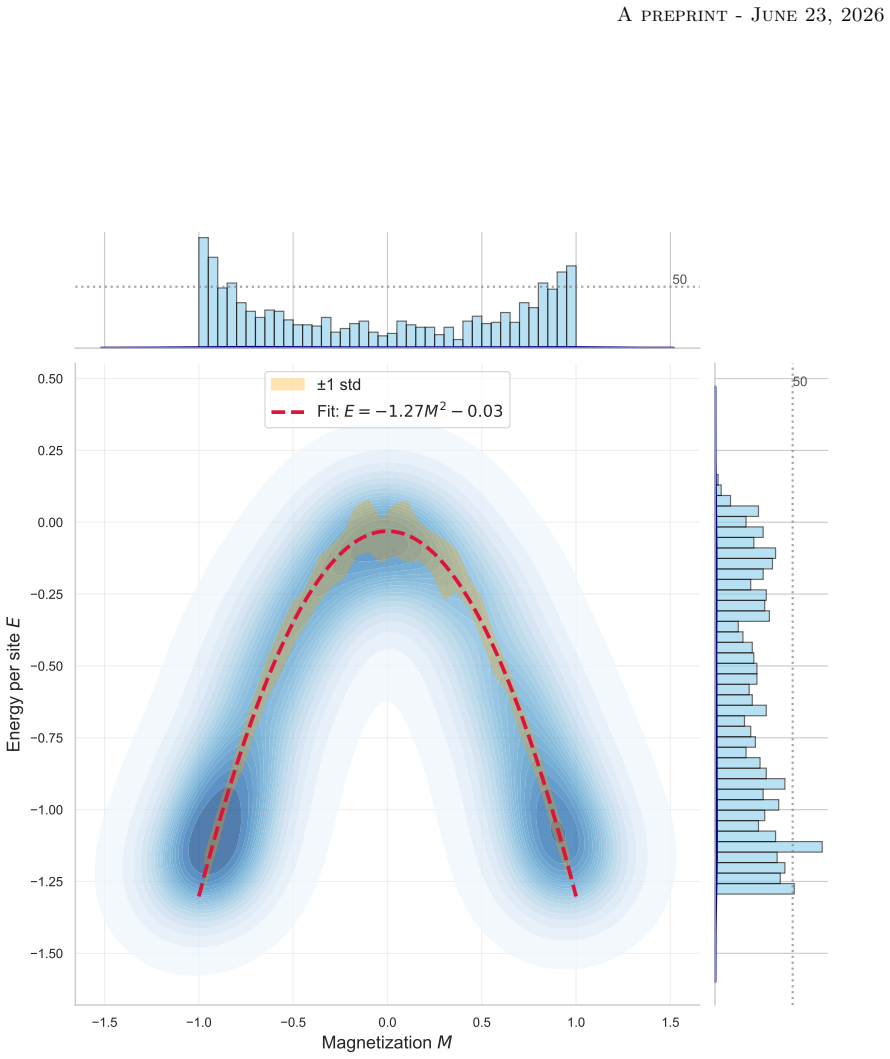

Cryptocurrency returns are encoded as spins on a 13x13 lattice whose Ising Hamiltonian produces an energy-magnetization diagram consistent with predominantly ferromagnetic interactions.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

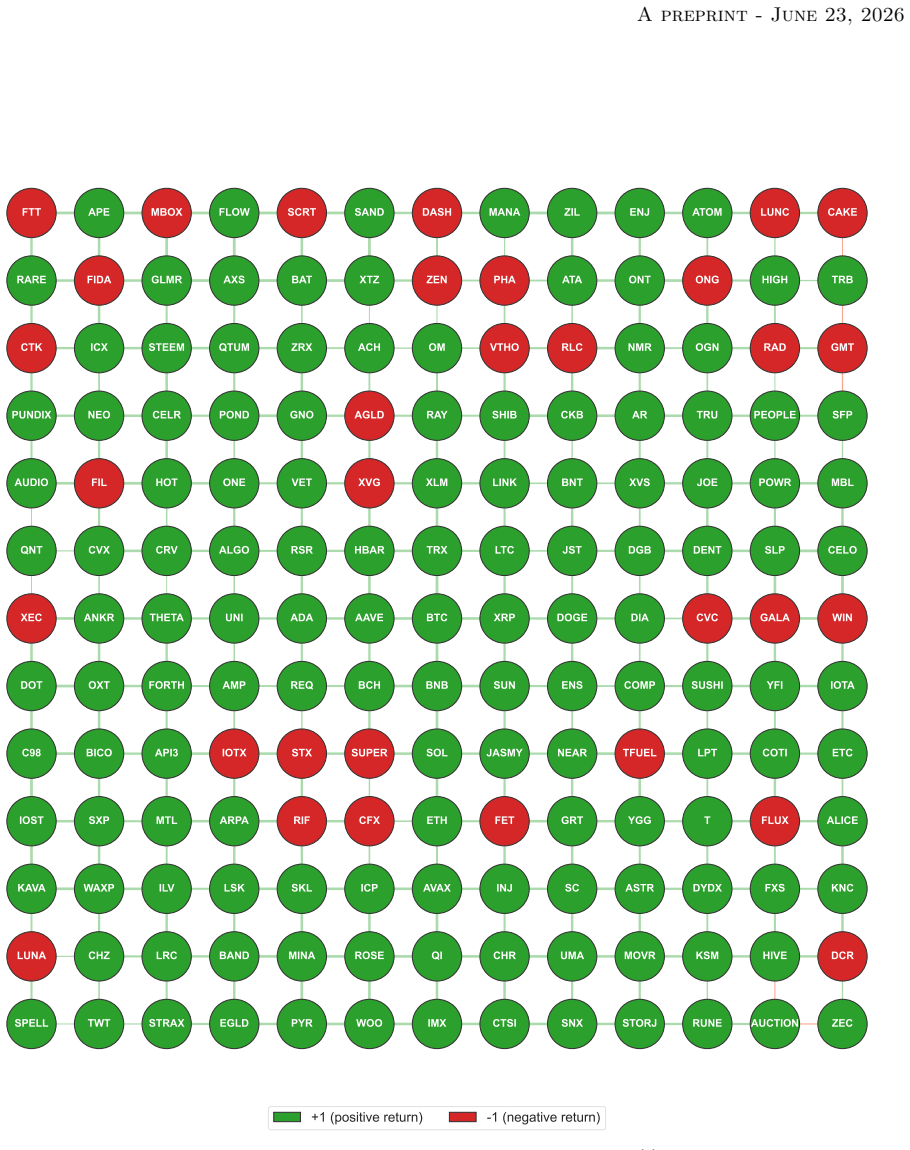

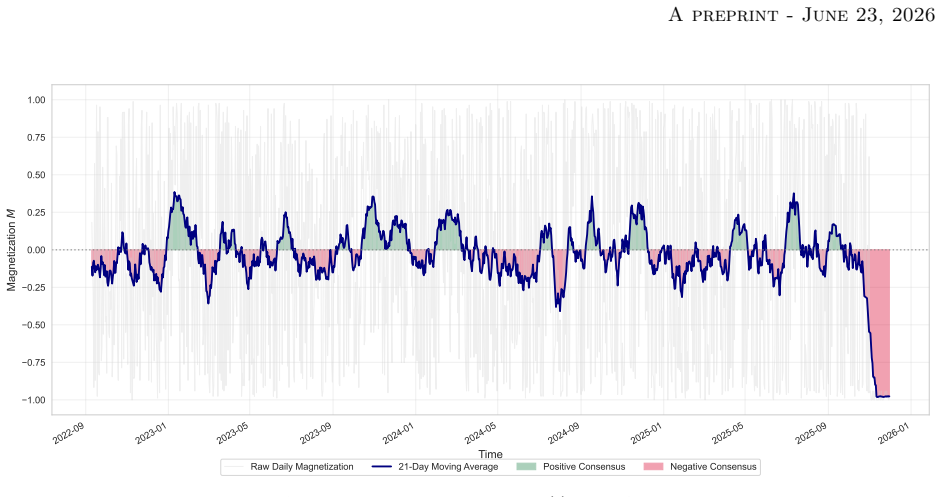

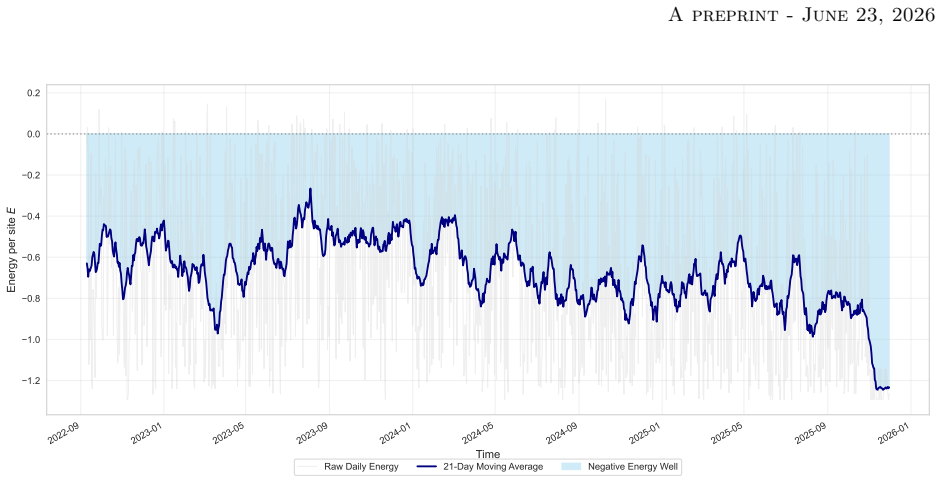

By mapping asset returns to spins and embedding the assets via correlation-guided breadth-first search into a 13x13 lattice, the authors construct an Ising Hamiltonian (the Market Crystal) whose phase-space structure exhibits regimes of high magnetization and an energy-magnetization pattern suggestive of net ferromagnetic interactions among the cryptocurrencies.

What carries the argument

The Market Crystal, the Ising-like Hamiltonian obtained after correlation-based breadth-first search embedding of 169 cryptocurrency return signs into a 13x13 lattice.

If this is right

- Market states can be tracked in real time by computing the instantaneous magnetization of the lattice.

- Periods of high magnetization correspond to synchronized price movements across many assets.

- The predominance of ferromagnetic couplings implies that positive return correlations outweigh negative ones in the collective dynamics.

- Fragmented states appear as low-magnetization, high-energy configurations in the same diagram.

Where Pith is reading between the lines

- The lattice representation could be used to define quantitative early-warning signals when magnetization begins to drop rapidly.

- The same embedding method might be applied to equity or commodity markets to test whether ferromagnetic patterns appear outside cryptocurrencies.

- If the ferromagnetic character persists, interventions that break positive feedback loops would be required to reduce systemic synchronization.

Load-bearing premise

The correlation-based breadth-first search procedure produces an interaction graph whose Ising Hamiltonian faithfully reproduces the collective dynamics of the original market data.

What would settle it

Out-of-sample cryptocurrency price series whose observed pairwise co-movements deviate systematically from the spin configurations that minimize or maximize the Market Crystal Hamiltonian.

Figures

read the original abstract

Collective dynamics in financial markets can emerge through synchronized movements of large groups of assets. Motivated by analogies with interacting many-body systems, we introduce a spin-lattice representation for analyzing collective states in cryptocurrency markets. In this framework, assets are encoded as binary spin variables according to the sign of their returns, while correlations between assets determine effective interaction strengths. A correlation-based breadth-first search (CBFS) procedure embeds 169 cryptocurrencies into a $13 \times 13$ lattice, enabling the construction of an Ising-like Hamiltonian describing the market configuration, which we call the \emph{Market Crystal}. Macroscopic observables such as magnetization and energy provide a statistical-mechanical characterization of collective market states. The resulting phase-space structure highlights regimes of strong alignment and fragmentation among assets, with an energy--magnetization pattern suggestive of predominantly ferromagnetic interactions. This framework offers a statistical-mechanical viewpoint for studying collective behavior in financial systems.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes modeling collective cryptocurrency dynamics using a spin-lattice representation. 169 assets are mapped to a 13×13 lattice via a correlation-based breadth-first search (CBFS) embedding, with correlations determining Ising-like interaction strengths. The resulting Hamiltonian is analyzed through magnetization and energy observables to identify regimes of alignment and fragmentation, with the energy-magnetization pattern interpreted as evidence for predominantly ferromagnetic interactions.

Significance. If the CBFS embedding is shown to preserve key correlation features and the observables are not circular, this framework could provide a useful statistical-mechanical lens for studying market synchronization. The approach is novel in its application but currently lacks the empirical validation needed to establish its utility.

major comments (2)

- Abstract, CBFS procedure paragraph: The central assumption that the CBFS embedding produces a lattice whose nearest-neighbor couplings dominate the collective behavior is not validated; no evidence is provided that the lattice Hamiltonian reproduces the original correlation matrix's eigenvalues, connected components, or time-series synchronization statistics.

- Abstract: The energy-magnetization pattern is presented as suggestive of ferromagnetic interactions, but since both the lattice structure and couplings are derived from the correlation matrix, and observables are computed from the same data, the pattern may be an artifact of the embedding rather than an independent characterization of market states.

minor comments (1)

- Abstract: The abstract mentions no numerical results, error bars, or comparisons to shuffled data, which would strengthen the claims even if presented in the main text.

Simulated Author's Rebuttal

We thank the referee for their constructive comments, which identify key areas for strengthening the validation and interpretation of the Market Crystal framework. We respond to each major comment below.

read point-by-point responses

-

Referee: Abstract, CBFS procedure paragraph: The central assumption that the CBFS embedding produces a lattice whose nearest-neighbor couplings dominate the collective behavior is not validated; no evidence is provided that the lattice Hamiltonian reproduces the original correlation matrix's eigenvalues, connected components, or time-series synchronization statistics.

Authors: We agree that explicit validation of the CBFS embedding's fidelity is required. In the revised manuscript we will add a dedicated section (or appendix) that compares the eigenvalue spectrum of the original correlation matrix with that of the lattice interaction matrix, verifies preservation of connected components, and reports synchronization statistics (e.g., average pairwise correlation and collective mode amplitudes) computed from the original time series versus those implied by the embedded Hamiltonian. These additions will directly test whether nearest-neighbor couplings capture the dominant collective features. revision: yes

-

Referee: Abstract: The energy-magnetization pattern is presented as suggestive of ferromagnetic interactions, but since both the lattice structure and couplings are derived from the correlation matrix, and observables are computed from the same data, the pattern may be an artifact of the embedding rather than an independent characterization of market states.

Authors: The lattice geometry and coupling signs are indeed derived from correlations, yet the spin variables themselves are the signs of individual asset returns, which are statistically independent of the pairwise correlation values used for embedding. The energy and magnetization are therefore evaluated on configurations that are not directly dictated by the embedding procedure. The resulting E-M pattern therefore reflects the market's realized collective states. We will revise the abstract and main text to make this distinction explicit and to discuss the degree to which the observed ferromagnetic-like structure follows from the predominantly positive correlations present in the data. revision: partial

Circularity Check

No significant circularity detected in derivation chain

full rationale

The paper constructs a descriptive mapping: correlations determine both the CBFS lattice embedding and the effective J couplings in an Ising-like Hamiltonian, after which magnetization and energy are evaluated on spin configurations (signs of returns). This is a re-expression of the input data in new coordinates rather than a derivation claiming independent predictions or first-principles results that reduce to the inputs by construction. No equations are shown that equate an output observable to a fitted parameter or input correlation by definition. No self-citation load-bearing steps, uniqueness theorems, or ansatzes smuggled via citation appear in the provided text. The energy-magnetization pattern is presented as an observed characterization of the market states under the model, not as a forced or tautological result. The framework remains self-contained as a modeling tool without violating the enumerated circularity patterns.

Axiom & Free-Parameter Ledger

free parameters (1)

- lattice dimension 13x13

axioms (2)

- domain assumption Pairwise return correlations can be interpreted as effective spin-spin interaction strengths without further renormalization or sign checks.

- ad hoc to paper The CBFS embedding produces a lattice whose nearest-neighbor couplings dominate the collective behavior.

invented entities (1)

-

Market Crystal

no independent evidence

Reference graph

Works this paper leans on

-

[1]

An introduction to the Ising model.The American Mathematical Monthly, 94(10), pp.937–959

Cipra, B.A., 1987. An introduction to the Ising model.The American Mathematical Monthly, 94(10), pp.937–959

1987

-

[2]

and Marchesi, M., 1999

Lux, T. and Marchesi, M., 1999. Scaling and criticality in a stochastic multi-agent model of a financial market.Nature, 397(6719), pp.498–500

1999

-

[3]

Hierarchical structure in financial markets.The European Physical Journal B, 11(1), pp.193–197

Mantegna, R.N., 1999. Hierarchical structure in financial markets.The European Physical Journal B, 11(1), pp.193–197

1999

-

[4]

and Bouchaud, J.P., 2000

Cont, R. and Bouchaud, J.P., 2000. Herd behavior and aggregate fluctuations in financial markets. Macroeconomic Dynamics, 4(2), pp.170–196

2000

-

[5]

and Bouchaud, J.P., 2000

Laloux, L., Cizeau, P., Potters, M. and Bouchaud, J.P., 2000. Random matrix theory and financial correlations.International Journal of Theoretical and Applied Finance, 3(3), pp.391–397

2000

-

[6]

and Aizawa, Y., 2000

Ponzi, A. and Aizawa, Y., 2000. Criticality and punctuated equilibrium in a spin system model of a financial market.Chaos, Solitons & Fractals, 11(11), pp.1739–1746

2000

-

[7]

and Stanley, H.E., 2001

Gopikrishnan, P., Rosenow, B., Plerou, V. and Stanley, H.E., 2001. Quantifying and interpreting collective behavior in financial markets.Physical Review E, 64(3), p.035106

2001

-

[8]

and Stanley, H.E., 2002

Plerou, V., Gopikrishnan, P., Rosenow, B., Amaral, L.A.N., Guhr, T. and Stanley, H.E., 2002. Random matrix approach to cross correlations in financial data.Physical Review E, 65(6), p.066126

2002

-

[9]

and Fujiwara, Y., 2002

Kaizoji, T., Bornholdt, S. and Fujiwara, Y., 2002. Dynamics of price and trading volume in a spin model of stock markets with heterogeneous agents.Physica A, 316(1–4), pp.441–452

2002

-

[10]

and Kanto, A., 2003

Onnela, J.P., Chakraborti, A., Kaski, K., Kertész, J. and Kanto, A., 2003. Asset trees and asset graphs in financial markets.Physica Scripta, T106, pp.48–54

2003

-

[11]

and Kertész, J., 2003

Onnela, J.P., Chakraborti, A., Kaski, K. and Kertész, J., 2003. Dynamic asset trees and Black Monday. Physica A, 324(1–2), pp.247–252

2003

-

[12]

Cambridge University Press

McCauley, J.L., 2004.Dynamics of Markets: Econophysics and Finance. Cambridge University Press

2004

-

[13]

Microscopic spin model for the stock market with attractor bubbling and heteroge- neous agents.International Journal of Modern Physics C, 16(4), pp.549–559

Krawiecki, A., 2005. Microscopic spin model for the stock market with attractor bubbling and heteroge- neous agents.International Journal of Modern Physics C, 16(4), pp.549–559

2005

-

[14]

Berlin, Heidelberg: Springer

Voit, J., 2005.The Statistical Mechanics of Financial Markets. Berlin, Heidelberg: Springer

2005

-

[15]

and Sinha, S., 2007

Pan, R.K. and Sinha, S., 2007. Collective behavior of stock price movements in an emerging market. Physical Review E, 76(4), p.046116

2007

-

[16]

and Mantegna, R.N., 2007

Tumminello, M., Di Matteo, T., Aste, T. and Mantegna, R.N., 2007. Correlation based networks of equity returns sampled at different time horizons.The European Physical Journal B, 55(2), pp.209–217

2007

-

[17]

and Sornette, D., 2007

Zhou, W.X. and Sornette, D., 2007. Self-organizing Ising model of financial markets.The European Physical Journal B, 55(2), pp.175–181

2007

-

[18]

and Gabaix, X., 2008

Stanley, H.E., Plerou, V. and Gabaix, X., 2008. A statistical physics view of financial fluctuations: Evidence for scaling and universality.Physica A, 387(15), pp.3967–3981

2008

-

[19]

Bouchaud, J.P. and Potters, M., 2009. Financial applications of random matrix theory: a short review. arXiv:0910.1205

Pith/arXiv arXiv 2009

-

[20]

and Chakrabarti, B.K., 2010.Econophysics: An Introduction

Sinha, S., Chatterjee, A., Chakraborti, A. and Chakrabarti, B.K., 2010.Econophysics: An Introduction. John Wiley & Sons

2010

-

[21]

and Abergel, F., 2011

Chakraborti, A., Toke, I.M., Patriarca, M. and Abergel, F., 2011. Econophysics review: I. Empirical facts.Quantitative Finance, 11(7), pp.991–1012

2011

-

[22]

and Jones, N.S., 2011

Fenn, D.J., Porter, M.A., Williams, S., McDonald, M., Johnson, N.F. and Jones, N.S., 2011. Temporal evolution of financial-market correlations.Physical Review E, 84(2), p.026109

2011

-

[23]

and Stanley, H.E., 2012

Münnix, M.C., Shimada, T., Schäfer, R., Leyvraz, F., Seligman, T.H., Guhr, T. and Stanley, H.E., 2012. Identifying states of a financial market.Scientific Reports, 2, p.644

2012

-

[24]

and Bornholdt, S., 2013

Krause, S.M. and Bornholdt, S., 2013. Spin models as microfoundation of macroscopic market models. Physica A, 392(18), pp.4048–4054

2013

-

[25]

and Balatsky, A.V., 2015

Borysov, S.S., Roudi, Y. and Balatsky, A.V., 2015. US stock market interaction network as learned by the Boltzmann machine.The European Physical Journal B, 88(12), p.321. x A preprint - June 23, 2026

2015

-

[26]

and Morgenstern, I., 2016

Eckrot, A., Jurczyk, J. and Morgenstern, I., 2016. Ising model of financial markets with many assets. Physica A, 462, pp.250–254

2016

-

[27]

Modeling of the financial market using the two-dimensional anisotropic Ising model

Lima, L.S., 2017. Modeling of the financial market using the two-dimensional anisotropic Ising model. Physica A, 482, pp.544–551

2017

-

[28]

and Martínez-Ibañez, O., 2019

Aslanidis, N., Bariviera, A.F. and Martínez-Ibañez, O., 2019. An analysis of cryptocurrencies conditional cross correlations.Finance Research Letters, 31, pp.130–137

2019

-

[29]

The Ising model: Brief introduction and its application

Singh, S.P., 2020. The Ising model: Brief introduction and its application. In:Solid State Physics – Metastable, Spintronics Materials and Mechanics of Deformable Bodies – Recent Progress. IntechOpen

2020

-

[30]

and Donnat, P., 2021

Marti, G., Nielsen, F., Bińkowski, M. and Donnat, P., 2021. A review of two decades of correlations, hierarchies, networks and clustering in financial markets.Progress in Information Geometry, pp.245–274

2021

-

[31]

and Stanuszek, M., 2021

Wątorek, M., Drożdż, S., Kwapień, J., Minati, L., Oświęcimka, P. and Stanuszek, M., 2021. Multiscale characteristics of the emerging global cryptocurrency market.Physics Reports, 901, pp.1–82

2021

-

[32]

and Shakhnov, K., 2022

Borri, N. and Shakhnov, K., 2022. The cross-section of cryptocurrency returns.Review of Asset Pricing Studies, 12(3), pp.667–705

2022

-

[33]

Ising model: Recent developments and exotic applications.Entropy, 24(12), p.1834

Lipowski, A., 2022. Ising model: Recent developments and exotic applications.Entropy, 24(12), p.1834

2022

-

[34]

and Sornette, D., 2023

Cividino, D., Westphal, R. and Sornette, D., 2023. Multiasset financial bubbles in an agent-based model with noise traders’ herding described by an n-vector Ising model.Physical Review Research, 5(1), p.013009

2023

-

[35]

and Hosseini-Farzad, M., 2023

Oliaei-Moghadam, H., Moodley, C. and Hosseini-Farzad, M., 2023. Patterns for all-digital quantum ghost imaging generated by the Ising model.Optics & Laser Technology, 163, p.109392

2023

-

[36]

and TabeBordbar, N., 2025

Oliaei-Moghadam, H., Hosseini-Farzad, M. and TabeBordbar, N., 2025. Single-pixel quantum ghost imaging using generalized Ising model.Scientific Reports, 15(1), p.22677. xi

2025

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.