Agent Security Meets Regulatory Reality -- A Practitioner Systematization of Autonomous-Agent Threats and Controls in Regulated Financial Systems

Pith reviewed 2026-06-30 02:48 UTC · model grok-4.3

The pith

Securing LLM agents in regulated finance requires production-scale auditability and boundary enforcement more than defenses against novel attacks.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Mapping six agent threat categories—prompt injection, identity and authorization, action auditability, tool abuse, data residency, and boundary policy enforcement—onto US and EU financial regulations shows legal accountability amplifies each threat compared with unregulated settings. Four patterns drawn from a production KYC system for consumer credit (A2A compliance choreography, grounded-RAG-for-audit, case-ID propagation, and inference-boundary redaction proxy) reduced a multi-day manual process to same-day automated resolution for roughly four in five cases. Three negative results include control failures detected only by internal audit and legitimate applicants the automated pipeline ca

What carries the argument

The mapping of six established agent threats to specific regulatory obligations, together with four production architectural patterns that enforce auditability and boundary controls in a KYC deployment.

If this is right

- Financial regulations raise the stakes of standard agent threats by adding legal accountability.

- The four patterns enable substantial automation while preserving traceability and least-privilege access.

- Internal audits can surface control failures that operational monitoring misses.

- Automated pipelines may systematically exclude segments of legitimate applicants.

- Current agent frameworks do not embed the controls needed for regulatory compliance.

Where Pith is reading between the lines

- The same emphasis on auditability and boundary enforcement could apply to agent use in other regulated domains such as insurance or payments.

- The negative results indicate that fully automated agent systems may still require hybrid human review for edge cases.

- Repeating the threat-to-regulation mapping across additional financial products would test whether the six categories remain sufficient.

- Agent development tools could incorporate the four patterns as default components rather than leaving them to individual engineers.

Load-bearing premise

The patterns and threat mappings from one KYC deployment for consumer credit represent the wider set of regulated financial systems and cover the main issues without further validation.

What would settle it

An independent deployment in a different regulated financial product that finds either that novel attack classes dominate security work or that the four patterns do not deliver compliant automation at scale.

Figures

read the original abstract

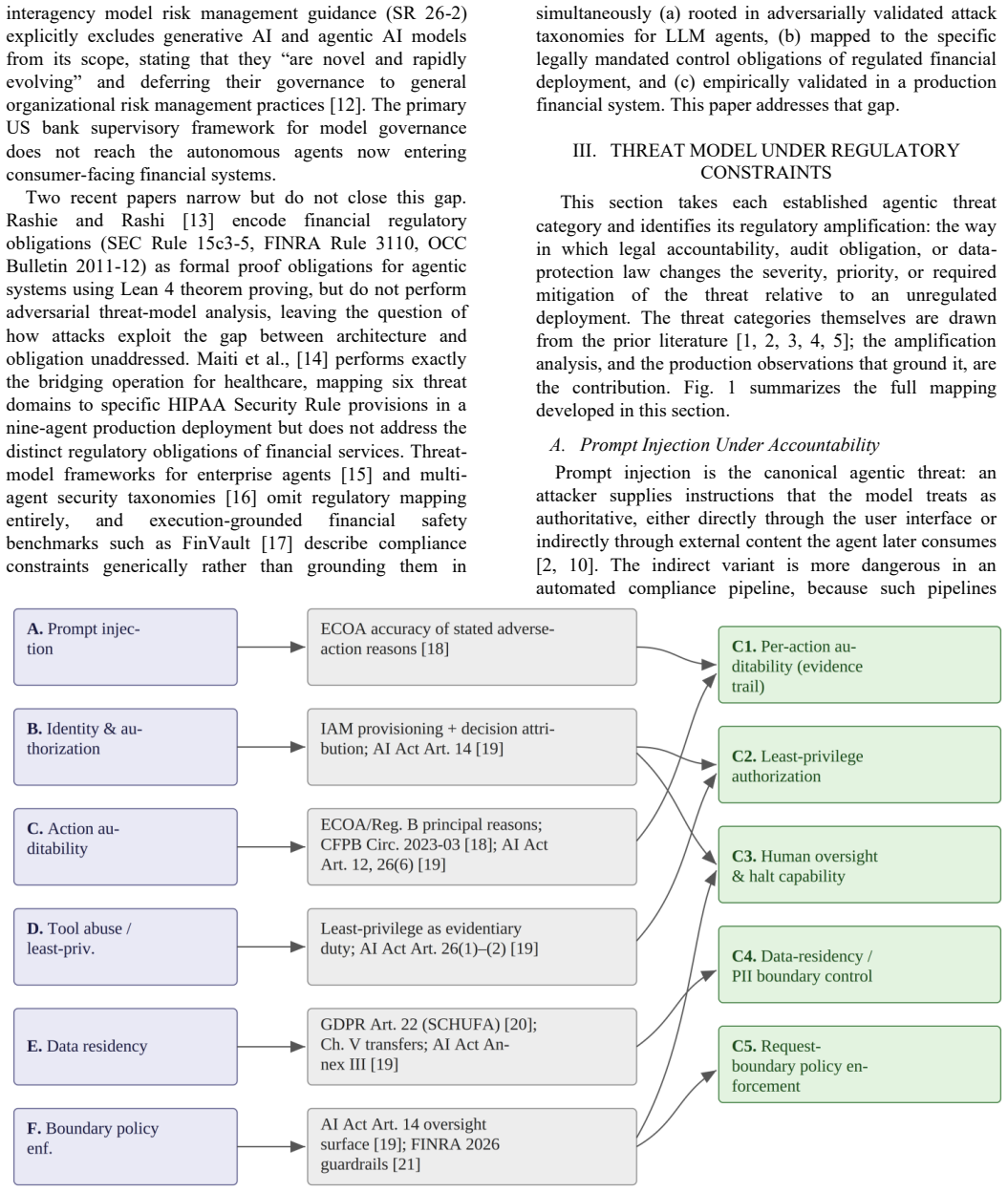

Large language model agents are entering regulated financial systems, yet the security literature characterizing their attack surface is almost entirely laboratory-based, and the practitioner guidance on regulated deployment is neither peer-reviewed nor connected to a formal threat model. We bridge the two from production experience. We map six established agentic threat categories namely prompt injection, identity and authorization, action auditability, tool abuse, data residency, and boundary policy enforcement onto the specific control obligations imposed by the US and the EU financial regulation (ECOA and Regulation B, the EU AI Act, GDPR Article 22, and FINRA's 2026 agent guidance), showing how legal accountability amplifies each threat relative to an unregulated deployment. We then document four architectural patterns from a production Know Your Customer deployment for a consumer credit product (A2A compliance choreography, grounded-RAG-for-audit, case-ID propagation, and an inference-boundary redaction proxy) that moved a multi-day manual process to same-day automated resolution for roughly four in five cases. Finally, we report three negative results, including two control failures surfaced only by internal audit and a population of legitimate applicants the automated pipeline cannot serve. Securing agents under regulation, we conclude, is less about novel attack classes than about making auditability, least-privilege authorization, and boundary policy enforcement real at production scale -- requirements current agent frameworks leave to the deploying engineer.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript systematizes threats to LLM-based autonomous agents in regulated financial systems by mapping six established categories (prompt injection, identity and authorization, action auditability, tool abuse, data residency, boundary policy enforcement) onto obligations under ECOA/Reg B, the EU AI Act, GDPR Article 22, and FINRA 2026 guidance. It presents four architectural patterns (A2A compliance choreography, grounded-RAG-for-audit, case-ID propagation, inference-boundary redaction proxy) drawn from a production KYC deployment for a consumer credit product that reduced a multi-day manual process to same-day automated resolution in roughly four in five cases, and reports three negative results including two control failures identified only by internal audit and a population of legitimate applicants the pipeline cannot serve. The central conclusion is that regulation amplifies these threats and that securing agents is primarily about making auditability, least-privilege authorization, and boundary enforcement operational at production scale—requirements that current agent frameworks leave to the deploying engineer.

Significance. If the reported patterns and mappings generalize, the work supplies a practitioner-oriented bridge between laboratory agent-security literature and regulatory requirements, with explicit mappings to named statutes and concrete implementation patterns accompanied by both positive deployment metrics and negative results. The grounding in an actual production deployment rather than synthetic or laboratory examples, together with the reporting of audit-surfaced failures, constitutes a strength for a systematization paper in this domain.

major comments (1)

- [Abstract; production experience and regulatory mapping sections] The central claim that the six threat categories are amplified by regulation and that the four patterns render auditability, least-privilege, and boundary enforcement practical at scale across regulated financial systems rests on a single KYC deployment for consumer credit. The production-experience section provides no evidence, discussion, or cross-validation addressing applicability to other regulated domains (e.g., securities execution or insurance underwriting) whose audit, residency, or decision-automation obligations may differ materially from those encountered in the reported case.

minor comments (2)

- [Abstract] The success rate is reported only as 'roughly four in five cases' without accompanying methodology, sample size, error bars, or breakdown by case type; adding these details would improve clarity of the quantitative claim.

- [Negative results paragraph] The three negative results are summarized at a high level; a brief enumeration of the specific control failures and the characteristics of the unservable applicant population would aid reader assessment of the patterns' limitations.

Simulated Author's Rebuttal

We thank the referee for the constructive comment on the scope of our empirical grounding. We respond to the major comment below.

read point-by-point responses

-

Referee: The central claim that the six threat categories are amplified by regulation and that the four patterns render auditability, least-privilege, and boundary enforcement practical at scale across regulated financial systems rests on a single KYC deployment for consumer credit. The production-experience section provides no evidence, discussion, or cross-validation addressing applicability to other regulated domains (e.g., securities execution or insurance underwriting) whose audit, residency, or decision-automation obligations may differ materially from those encountered in the reported case.

Authors: We agree that the reported patterns, metrics, and negative results derive exclusively from one production KYC deployment for consumer credit. The manuscript contains no cross-validation or discussion of applicability to other domains such as securities execution or insurance underwriting. This limitation follows directly from the work being a systematization drawn from the authors' direct experience with that specific deployment. The regulatory mappings reference obligations that appear across multiple financial statutes, but we accept that operational differences in audit, residency, and decision-automation requirements may affect how the patterns translate. We will revise the production-experience section and add an explicit limitations paragraph stating that the four patterns are illustrative of the reported case and that extension to other sub-domains would require separate production validation. This change clarifies scope without expanding the claims. revision: yes

Circularity Check

No significant circularity; systematization grounded in external production deployment

full rationale

The paper derives its mappings of six threat categories to regulations (ECOA/Reg B, EU AI Act, GDPR Art. 22, FINRA 2026) and its four architectural patterns directly from observed outcomes in one consumer-credit KYC deployment. No equations, fitted parameters, self-citations, or ansatzes appear in the provided text. Claims about auditability and least-privilege enforcement at scale are presented as practitioner observations rather than predictions that reduce to the input data by construction. The derivation chain is therefore self-contained as an empirical report.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption The six listed threat categories (prompt injection, identity and authorization, action auditability, tool abuse, data residency, boundary policy enforcement) fully characterize the agent attack surface in financial systems.

- ad hoc to paper The reported production patterns and negative results accurately reflect the deployed system without selection bias.

Reference graph

Works this paper leans on

-

[1]

K. Chu, “A Systematic Survey of Security Threats and Defenses in LLM-Based AI Agents: A Layered Attack Surface Framework,” arXiv:2604.23338, Apr. 2026

work page internal anchor Pith review Pith/arXiv arXiv 2026

-

[2]

The Landscape of Prompt Injection Threats in LLM Agents: From Taxonomy to Analysis,

P. Wang, X. Li, C. Xiang, J. Zhang, Y. Li, L. Zhang, X. Wang, and Y. Tian, “The Landscape of Prompt Injection Threats in LLM Agents: From Taxonomy to Analysis,” arXiv:2602.10453, Feb. 2026

-

[3]

Systematization of Knowledge: Security and Safety in the Model Context Protocol Ecosystem,

S. Gaire, S. Gyawali, S. Mishra, S. Niroula, D. Thakur, and U. Yadav, “Systematization of Knowledge: Security and Safety in the Model Context Protocol Ecosystem,” arXiv:2512.08290, Dec. 2025

-

[4]

T. South et al., “Identity Management for Agentic AI: The New Frontier of Authorization, Authentication, and Security for an AI Agent World,” OpenID Foundation Whitepaper, arXiv:2510.25819, Oct. 2025

-

[5]

From Storage to Steering: Memory Control Flow Attacks on LLM Agents

Z. Xu, X. Zhu, Y. Yao, M. Xue, and Y. Song, “From Storage to Steering: Memory Control Flow Attacks on LLM Agents,” arXiv:2603.15125, Mar. 2026

work page internal anchor Pith review Pith/arXiv arXiv 2026

-

[6]

E. Tabassi, “Artificial Intelligence Risk Management Framework (AI RMF 1.0),” NIST AI 100 -1, National Institute of Standards and Technology, Gaithersburg, MD, Jan. 2023, doi:10.6028/NIST.AI.100-1

-

[7]

International Organization for Standardization / International Electrotechnical Commission, “Information Technology —Artificial TABLE II NEGATIVE RESULTS FROM THE DEPLOYMENT: WHAT FAILED, HOW IT SURFACED, ITS ROOT CAUSE, AND THE OPEN PROBLEM OR GENERALIZABLE LESSON. TWO OF THE THREE WERE SURFACED BY INTERNAL AUDIT OR PRODUCTION OBSERVATION RATHER THAN BY ...

2023

-

[8]

Retrieval -Augmented Generation for Knowledge - Intensive NLP Tasks,

P. Lewis et al., “Retrieval -Augmented Generation for Knowledge - Intensive NLP Tasks,” in Proc. NeurIPS, 2020

2020

-

[9]

Agent2Agent (A2A) Protocol: A New Era of Agent Interoperability,

Google, “Agent2Agent (A2A) Protocol: A New Era of Agent Interoperability,” Google Developers Blog, 2025

2025

-

[10]

Not What You’ve Signed Up For: Compromising Real -World LLM -Integrated Applications with Indirect Prompt Injection,

K. Greshake et al., “Not What You’ve Signed Up For: Compromising Real -World LLM -Integrated Applications with Indirect Prompt Injection,” in Proc. ACM AISec, 2023

2023

-

[11]

OWASP Top 10 for LLM Applications,

OWASP Foundation, “OWASP Top 10 for LLM Applications,” 2024–2025

2024

-

[12]

Revised Guidance on Model Risk Management,

Board of Governors of the Federal Reserve System, Office of the Comptroller of the Currency, and Federal Deposit Insurance Corporation, “Revised Guidance on Model Risk Management,” SR Letter 26-2, Apr. 17, 2026 (superseding SR 11-7, 2011, and SR 21-8, 2021). [Online]. Available: https://www.federalreserve.gov/supervisionreg/srletters/SR2602.htm

2026

-

[13]

D. Rashie and V. Rashi, “Type -Checked Compliance: Deterministic Guardrails for Agentic Financial Systems Using Lean 4 Theorem Proving,” arXiv:2604.01483, Apr. 2026

-

[14]

Caging the Agents: A Zero Trust Security Architecture for Autonomous AI in Healthcare,

S. Maiti, “Caging the Agents: A Zero Trust Security Architecture for Autonomous AI in Healthcare,” arXiv:2603.17419, Mar. 2026

-

[15]

Securing Agentic AI: A Comprehensive Threat Model and Mitigation Framework for Generative AI Agents,

V. S. Narajala and O. Narayan, “Securing Agentic AI: A Comprehensive Threat Model and Mitigation Framework for Generative AI Agents,” arXiv:2504.19956, Apr. 2025

-

[16]

Open Challenges in Multi-Agent Security: Towards Secure Systems of Interacting AI Agents

C. Schroeder de Witt et al., “Open Challenges in Multi -Agent Security: Towards Secure Systems of Interacting AI Agents,” arXiv:2505.02077, 2025

work page internal anchor Pith review Pith/arXiv arXiv 2025

-

[17]

FinVault: Benchmarking Financial Agent Safety in Execution-Grounded Environments,

Z. Yang et al., “FinVault: Benchmarking Financial Agent Safety in Execution-Grounded Environments,” arXiv:2601.07853, Jan. 2026

-

[18]

CFPB Circular 2023 -03: Adverse Action Notification Requirements and the Equal Credit Opportunity Act (ECOA),

Consumer Financial Protection Bureau, “CFPB Circular 2023 -03: Adverse Action Notification Requirements and the Equal Credit Opportunity Act (ECOA),” Sep. 19, 2023

2023

-

[19]

Regulation (EU) 2024/1689 Laying Down Harmonised Rules on Artificial Intelligence (Artificial Intelligence Act),

European Parliament and Council of the European Union, “Regulation (EU) 2024/1689 Laying Down Harmonised Rules on Artificial Intelligence (Artificial Intelligence Act),” Official Journal of the European Union, Jun. 2024

2024

-

[20]

Judgment in Case C - 634/21, OQ v. Land Hessen (SCHUFA Holding),

Court of Justice of the European Union, “Judgment in Case C - 634/21, OQ v. Land Hessen (SCHUFA Holding),” ECLI:EU:C:2023:957, Dec. 2023

2023

-

[21]

2026 FINRA Annual Regulatory Oversight Report: Generative AI —Agents,

Financial Industry Regulatory Authority, “2026 FINRA Annual Regulatory Oversight Report: Generative AI —Agents,” FINRA, Dec. 2025

2026

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.