Quantum Monte Carlo algorithm for option pricing and its complexity analysis

Pith reviewed 2026-05-24 10:21 UTC · model grok-4.3

The pith

A quantum Monte Carlo algorithm solves multidimensional Black-Scholes PDEs for option pricing with polynomial complexity in dimension and accuracy.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

We provide a quantum Monte Carlo algorithm to solve multidimensional Black-Scholes PDEs with correlation for option pricing. The payoff function is continuous and piecewise affine. We prove that the computational complexity is bounded polynomially in the space dimension d and the reciprocal of the accuracy ε. For bounded payoffs the algorithm has a speed-up compared to classical Monte Carlo methods.

What carries the argument

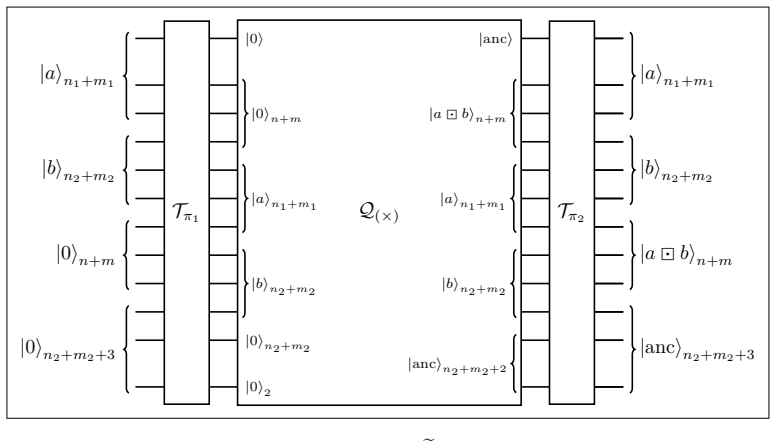

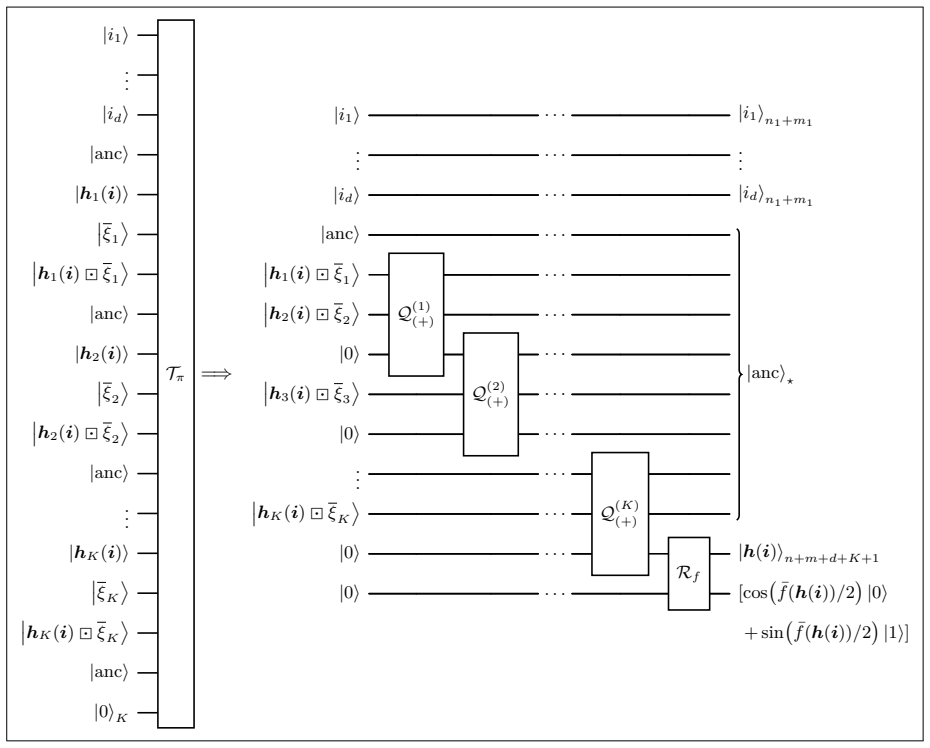

The quantum Monte Carlo algorithm based on quantum state preparation for the Black-Scholes dynamics and amplitude estimation to evaluate the expectation under the payoff.

Load-bearing premise

The payoff function must be continuous and piecewise affine to allow quantum state preparation and error analysis to succeed.

What would settle it

An explicit payoff that is continuous and piecewise affine yet requires superpolynomial resources in d, or a bounded-payoff case where the quantum resource count exceeds classical Monte Carlo.

Figures

read the original abstract

In this paper we provide a quantum Monte Carlo algorithm to solve multidimensional Black-Scholes PDEs with correlation for option pricing. The payoff function of the option is of general form and is only required to be continuous and piecewise affine, which covers most of the relevant payoff functions used in finance. We provide a rigorous error analysis and complexity analysis of our algorithm. In particular, we prove that the computational complexity of our algorithm is bounded polynomially in the space dimension $d$ of the PDE and the reciprocal of the prescribed accuracy $\varepsilon$. Moreover, we show that for payoff functions which are bounded, our algorithm indeed has a speed-up compared to classical Monte Carlo methods. Furthermore, we provide numerical simulations in two dimensions using our developed package within the Qiskit framework tailored to price continuous piecewise affine options with respect to the Black-Scholes model, as well as discuss the potential extension of the numerical simulations to arbitrary space dimension.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript presents a quantum Monte Carlo algorithm for solving multidimensional Black-Scholes PDEs with correlations to price options. The payoff functions are assumed to be continuous and piecewise affine. A rigorous error analysis is provided, along with a complexity analysis showing that the algorithm's complexity is polynomial in the space dimension d and the reciprocal of the accuracy ε. For bounded payoffs, a speedup over classical Monte Carlo is claimed. Numerical simulations in two dimensions are performed using a custom Qiskit package.

Significance. If the analysis holds, the work provides a concrete quantum algorithm for a practical finance problem with an explicit polynomial complexity bound in d and 1/ε, plus a claimed speedup for bounded payoffs. The rigorous error/complexity analysis and the open-source Qiskit implementation are strengths that support reproducibility and verifiability.

minor comments (3)

- [§1] §1 and abstract: the statement that the continuous piecewise affine assumption 'covers most of the relevant payoff functions used in finance' would benefit from one or two concrete examples (e.g., European calls vs. certain exotics) to clarify scope.

- [Numerical simulations] Numerical section: the 2D Qiskit implementation is described at a high level; adding pseudocode or a brief description of the state-preparation circuit for the piecewise-affine payoff would improve clarity and reproducibility.

- [Complexity analysis] The complexity proof sketch in the main text could explicitly flag where the piecewise-affine property is used to bound the state-preparation cost, even if the full derivation is in an appendix.

Simulated Author's Rebuttal

We thank the referee for their positive assessment of the manuscript, the recognition of its strengths in rigorous analysis and open-source implementation, and the recommendation for minor revision. No specific major comments were listed in the report.

Circularity Check

No significant circularity detected

full rationale

The paper states a quantum Monte Carlo algorithm for multidimensional Black-Scholes PDEs whose complexity is proven polynomial in dimension d and 1/ε under the explicit modeling assumption that payoffs are continuous and piecewise affine (with boundedness for the speedup claim). This is presented as a rigorous proof against external classical Monte Carlo benchmarks rather than any fitted parameter, self-definition, or self-citation chain. The abstract and reader's summary give no indication that any load-bearing step reduces by construction to the inputs; the derivation is therefore treated as self-contained.

Axiom & Free-Parameter Ledger

axioms (2)

- standard math Quantum amplitude estimation provides quadratic speedup over classical Monte Carlo sampling

- domain assumption The Black-Scholes PDE with correlation admits a Feynman-Kac representation that can be sampled quantum-mechanically

Reference graph

Works this paper leans on

-

[1]

Quantum approximate counting, simplified

Scott Aaronson and Patrick Rall. “Quantum approximate counting, simplified”. In: (2020), pp. 24–32

work page 2020

-

[2]

Yves Achdou and Olivier Pironneau.Computational methods for option pricing. SIAM, 2005

work page 2005

-

[3]

J. Aitchison and J.A.C. Brown. The Lognormal Distribution. Cambridge University Press, 1957

work page 1957

-

[4]

A quantum architecture for multiplying signed integers

JJ Alvarez-Sanchez, JV Álvarez-Bravo, and LM Nieto. “A quantum architecture for multiplying signed integers”. In:Journal of Physics: Conference Series128 (2008), p. 012013.doi: 10.1088/1742-6596/128/1/012013

-

[5]

Dong An, Noah Linden, Jin-Peng Liu, Ashley Montanaro, Changpeng Shao, and Jiasu Wang. “Quantum-accelerated multilevel Monte Carlo methods for stochastic differential equations in mathematical finance”. In:Quantum 5 (2021), p. 481

work page 2021

-

[6]

Quantum algorithm for nonhomogeneous linear partial differential equations

Juan Miguel Arrazola, Timjan Kalajdzievski, Christian Weedbrook, and Seth Lloyd. “Quantum algorithm for nonhomogeneous linear partial differential equations”. In:Physical Review A100.3 (2019), p. 032306

work page 2019

-

[7]

A quantum generative adversarial network for distributions

Amine Assouel, Antoine Jacquier, and Alexei Kondratyev. “A quantum generative adversarial network for distributions”. In: Quantum Machine Intelligence4.2 (2022), p. 28

work page 2022

-

[8]

Deep splitting method for parabolic PDEs

Christian Beck, Sebastian Becker, Patrick Cheridito, Arnulf Jentzen, and Ariel Neufeld. “Deep splitting method for parabolic PDEs”. In:SIAM Journal on Scientific Computing43.5 (2021), A3135–A3154

work page 2021

-

[9]

Julius Berner, Philipp Grohs, and Arnulf Jentzen. “Analysis of the generalization error: Empirical risk minimization over deep ar- tificial neural networks overcomes the curse of dimensionality in the numerical approximation of Black–Scholes partial differential equations”. In:SIAM Journal on Mathematics of Data Science2.3 (2020), pp. 631–657

work page 2020

-

[10]

The pricing of options and corporate liabilities

Fischer Black and Myron Scholes. “The pricing of options and corporate liabilities”. In:Journal of political economy81.3 (1973), pp. 637–654

work page 1973

-

[11]

Options: A monte carlo approach

Phelim P Boyle. “Options: A monte carlo approach”. In:Journal of financial economics4.3 (1977), pp. 323–338

work page 1977

-

[12]

Quantum amplitude amplification and estimation

Gilles Brassard, Peter Hoyer, Michele Mosca, and Alain Tapp. “Quantum amplitude amplification and estimation”. In:Contem- porary Mathematics305 (2002), pp. 53–74

work page 2002

-

[13]

Randal E. Bryant and David R. O’Hallaron. Computer Systems: A Programmer’s Perspective. Prentice Hall, 2003. isbn: 9780131784567

work page 2003

-

[14]

Makarov.Financial Mathematics: A Comprehensive Treatment

Giuseppe Campolieti and Roman N. Makarov.Financial Mathematics: A Comprehensive Treatment. Textbooks in Mathematics. CRC Press, 2014.isbn: 9781439892435. 55

work page 2014

-

[15]

A threshold for quantum advantage in derivative pricing

Shouvanik Chakrabarti, Rajiv Krishnakumar, Guglielmo Mazzola, Nikitas Stamatopoulos, Stefan Woerner, and William J Zeng. “A threshold for quantum advantage in derivative pricing”. In:Quantum 5 (2021), p. 463

work page 2021

-

[16]

A novel approach for quantum financial simulation and quantum state preparation

Yen-Jui Chang, Wei-Ting Wang, Hao-Yuan Chen, Shih-Wei Liao, and Ching-Ray Chang. “A novel approach for quantum financial simulation and quantum state preparation”. In:arXiv preprint arXiv:2308.01844(2023)

-

[17]

Marco Chiani, Davide Dardari, and Marvin K. Simon. “New exponential bounds and approximations for the computation of error probability in fading channels”. In:IEEE Transactions on Wireless Communications2.4 (2003), pp. 840–845.doi: 10.1109/TWC.2003.814350

-

[18]

High-precision quantum algorithms for partial differential equations

Andrew M Childs, Jin-Peng Liu, and Aaron Ostrander. “High-precision quantum algorithms for partial differential equations”. In: Quantum 5 (2021), p. 574

work page 2021

-

[19]

User’s guide to viscosity solutions of second order partial differential equations

Michael G Crandall, Hitoshi Ishii, and Pierre-Louis Lions. “User’s guide to viscosity solutions of second order partial differential equations”. In:Bulletin of the American mathematical society27.1 (1992), pp. 1–67

work page 1992

-

[20]

A new quantum ripple-carry addition circuit

Steven A. Cuccaro, Thomas G. Draper, Samuel A. Kutin, and David Petrie Moulton. “A new quantum ripple-carry addition circuit”. In: (2004). arXiv:quant-ph/0410184 [quant-ph]

work page internal anchor Pith review Pith/arXiv arXiv 2004

-

[21]

Unsupervised Random Quantum Networks for PDEs

Josh Dees, Antoine Jacquier, and Sylvain Laizet. “Unsupervised Random Quantum Networks for PDEs”. In:arXiv preprint arXiv:2312.14975 (2023)

-

[22]

Cirq Developers. Cirq. Version v1.1.0. See full list of authors on Github: https://github .com/quantumlib/Cirq/graphs/contrib- utors. Dec. 2022.doi: 10.5281/zenodo.7465577

-

[23]

Quantum algorithm for stochas- tic optimal stopping problems with applications in finance

João F Doriguello, Alessandro Luongo, Jinge Bao, Patrick Rebentrost, and Miklos Santha. “Quantum algorithm for stochas- tic optimal stopping problems with applications in finance”. In:17th Conference on the Theory of Quantum Computation, Communication and Cryptography (TQC 2022). Schloss Dagstuhl-Leibniz-Zentrum für Informatik. 2022

work page 2022

-

[24]

Addition on a Quantum Computer

Thomas Draper. “Addition on a Quantum Computer”. In: (Sept. 2000)

work page 2000

-

[25]

David S. Dummit and Rrichard M. Foote.Abstract Algebra. Wiley, 2003.isbn: 9780471433347

work page 2003

-

[26]

Quantum computing for finance: State-of-the-art and future prospects

Daniel J Egger, Claudio Gambella, Jakub Marecek, Scott McFaddin, Martin Mevissen, Rudy Raymond, Andrea Simonetto, Stefan Woerner, and Elena Yndurain. “Quantum computing for finance: State-of-the-art and future prospects”. In:IEEE Transactions on Quantum Engineering1 (2020), pp. 1–24

work page 2020

-

[27]

DNN expression rate analysis of high-dimensional PDEs: Application to option pricing

Dennis Elbrächter, Philipp Grohs, Arnulf Jentzen, and Christoph Schwab. “DNN expression rate analysis of high-dimensional PDEs: Application to option pricing”. In:Constructive Approximation55.1 (2022), pp. 3–71

work page 2022

-

[28]

A quantum algorithm for linear PDEs arising in finance

Filipe Fontanela, Antoine Jacquier, and Mugad Oumgari. “A quantum algorithm for linear PDEs arising in finance”. In:SIAM Journal on Financial Mathematics12.4 (2021), SC98–SC114

work page 2021

-

[29]

Modified iterative quantum amplitude estimation is asymptot- ically optimal

Shion Fukuzawa, Christopher Ho, Sandy Irani, and Jasen Zion. “Modified iterative quantum amplitude estimation is asymptot- ically optimal”. In:2023 Proceedings of the Symposium on Algorithm Engineering and Experiments (ALENEX). SIAM. 2023, pp. 135–147

work page 2023

-

[30]

Manfred Gilli, Dietmar Maringer, and Enrico Schumann.Numerical methods and optimization in finance. Academic Press, 2019

work page 2019

-

[31]

Low depth algorithms for quantum amplitude estimation

Tudor Giurgica-Tiron, Iordanis Kerenidis, Farrokh Labib, Anupam Prakash, and William Zeng. “Low depth algorithms for quantum amplitude estimation”. In:Quantum 6 (2022), p. 745

work page 2022

-

[32]

Universal approximation theorem and error bounds for quantum neural networks and quantum reservoirs

Lukas Gonon and Antoine Jacquier. “Universal approximation theorem and error bounds for quantum neural networks and quantum reservoirs”. In:arXiv preprint arXiv:2307.12904(2023)

-

[33]

Iterative quantum amplitude estimation

Dmitry Grinko, Julien Gacon, Christa Zoufal, and Stefan Woerner. “Iterative quantum amplitude estimation”. In:npj Quantum Information 7.1 (2021), pp. 1–6

work page 2021

-

[34]

Philipp Grohs, Fabian Hornung, Arnulf Jentzen, and Philippe von Wurstemberger.A proof that artificial neural networks over- come the curse of dimensionality in the numerical approximation of Black–Scholes partial differential equations. Vol. 284. 1410. American Mathematical Society, 2023

work page 2023

-

[35]

Creating superpositions that correspond to efficiently integrable probability distributions

Lov Grover and Terry Rudolph. “Creating superpositions that correspond to efficiently integrable probability distributions”. In: (Sept. 2002)

work page 2002

-

[36]

A Fast Quantum Mechanical Algorithm for Database Search

Lov K. Grover. “A Fast Quantum Mechanical Algorithm for Database Search.” In:STOC. Ed. by Gary L. Miller. ACM, 1996, pp. 212–219.isbn: 0-89791-785-5

work page 1996

-

[37]

Solving high-dimensional partial differential equations using deep learning

Jiequn Han, Arnulf Jentzen, and Weinan E. “Solving high-dimensional partial differential equations using deep learning”. In: Proceedings of the National Academy of Sciences115.34 (2018), pp. 8505–8510

work page 2018

-

[38]

Quantum Monte Carlo integration: the full advantage in minimal circuit depth

Steven Herbert. “Quantum Monte Carlo integration: the full advantage in minimal circuit depth”. In:Quantum 6 (2022), p. 823

work page 2022

-

[39]

Quantum State Preparation of Normal Distributions using Matrix Product States

Jason Iaconis, Sonika Johri, and Elton Yechao Zhu. “Quantum State Preparation of Normal Distributions using Matrix Product States”. In:arXiv preprint arXiv:2303.01562(2023)

-

[40]

Quantum Computing for Financial Mathematics

Antoine Jacquier, Oleksiy Kondratyev, Gordon Lee, and Mugad Oumgari. “Quantum Computing for Financial Mathematics”. In: arXiv preprint arXiv:2311.06621(2023)

-

[41]

Antoine Jacquier, Oleksiy Kondratyev, Alexander Lipton, and Marcos Lopez de Prado.Quantum Machine Learning and Opti- misation in Finance: On the Road to Quantum Advantage. Packt Publishing Ltd, 2022

work page 2022

-

[42]

Approximation by Quantum Circuits

Emanuel Knill. “Approximation by quantum circuits”. In:arXiv preprint quant-ph/9508006(1995)

work page internal anchor Pith review Pith/arXiv arXiv 1995

-

[43]

Pricing Multi-asset Derivatives by Variational Quantum Algorithms

Kenji Kubo, Koichi Miyamoto, Kosuke Mitarai, and Keisuke Fujii. “Pricing Multi-asset Derivatives by Variational Quantum Algorithms”. In:IEEE Transactions on Quantum Engineering(2023)

work page 2023

-

[44]

Quantum vs. classical algorithms for solving the heat equation

Noah Linden, Ashley Montanaro, and Changpeng Shao. “Quantum vs. classical algorithms for solving the heat equation”. In: Communications in Mathematical Physics395.2 (2022), pp. 601–641

work page 2022

-

[45]

D5. 7: Update of review of state-of-the-art for Pricing and Computation of VaR

Alberto Manzano, Andrés Gómez, and CESGA Carlos Vázquez. “D5. 7: Update of review of state-of-the-art for Pricing and Computation of VaR”. In: (2023)

work page 2023

-

[46]

Real quantum amplitude estimation

Alberto Manzano, Daniele Musso, and Álvaro Leitao. “Real quantum amplitude estimation”. In:EPJ Quantum Technology10.1 (2023), pp. 1–24

work page 2023

- [47]

-

[48]

Theory of rational option pricing

Robert C Merton. “Theory of rational option pricing”. In:The Bell Journal of economics and management science(1973), pp. 141–183

work page 1973

-

[49]

Quantum speedup of Monte Carlo methods

Ashley Montanaro. “Quantum speedup of Monte Carlo methods”. In:Proceedings of the Royal Society A: Mathematical, Physical and Engineering Sciences471.2181(2015),p.20150301. doi: 10.1098/rspa.2015.0301.eprint: https://royalsocietypublishing. org/doi/pdf/10.1098/rspa.2015.0301

-

[50]

Quantum algorithms and the finite element method

Ashley Montanaro and Sam Pallister. “Quantum algorithms and the finite element method”. In:Physical Review A93.3 (2016), p. 032324

work page 2016

-

[51]

Kouhei Nakaji. “Faster amplitude estimation”. In:Quantum Information and Computation20.13&14 (2020), pp. 1109–1122. doi: 10.26421/QIC20.13-14-2. url: https://doi.org/10.26421/QIC20.13-14-2

-

[52]

Ariel Neufeld, Antonis Papapantoleon, and Qikun Xiang. “Model-free bounds for multi-asset options using option-implied infor- mation and their exact computation”. In:Management Science(2022)

work page 2022

-

[53]

Michael A. Nielsen and Isaac L. Chuang. Quantum Computation and Quantum Information: 10th Anniversary Edition. 10th. USA: Cambridge University Press, 2011.isbn: 1107002176

work page 2011

-

[54]

Quantum computing for finance: Overview and prospects

Román Orús, Samuel Mugel, and Enrique Lizaso. “Quantum computing for finance: Overview and prospects”. In:Reviews in Physics 4 (2019), p. 100028

work page 2019

-

[55]

A variational eigenvalue solver on a photonic quantum processor

Alberto Peruzzo, Jarrod McClean, Peter Shadbolt, Man-Hong Yung, Xiao-Qi Zhou, Peter J Love, Alán Aspuru-Guzik, and Jeremy L O’brien. “A variational eigenvalue solver on a photonic quantum processor”. In:Nature communications5.1 (2014), pp. 1–7

work page 2014

-

[56]

Variational quantum amplitude estimation

Kirill Plekhanov, Matthias Rosenkranz, Mattia Fiorentini, and Michael Lubasch. “Variational quantum amplitude estimation”. In: Quantum 6 (2022), p. 670

work page 2022

-

[57]

Rafał Pracht. “Quantum Binomial Tree, an effective method for probability distribution loading for derivative pricing”. In: Available at SSRN 4216595(2023)

work page 2023

-

[58]

Qiskit: An Open-source Framework for Quantum Computing

Qiskit contributors. Qiskit: An Open-source Framework for Quantum Computing. 2023. doi: 10.5281/zenodo.2573505

-

[59]

Amplitude Estimation from Quantum Signal Processing

Patrick Rall and Bryce Fuller. “Amplitude Estimation from Quantum Signal Processing”. In:Quantum 7 (2023), p. 937

work page 2023

-

[60]

Quantum unary approach to option pricing

Sergi Ramos-Calderer, Adrián Pérez-Salinas, Diego García-Martín, Carlos Bravo-Prieto, Jorge Cortada, Jordi Planaguma, and José I Latorre. “Quantum unary approach to option pricing”. In:Physical Review A103.3 (2021), p. 032414

work page 2021

-

[61]

Quantum amplitude estimation algorithms on IBM quantum devices

Pooja Rao, Kwangmin Yu, Hyunkyung Lim, Dasol Jin, and Deokkyu Choi. “Quantum amplitude estimation algorithms on IBM quantum devices”. In:Quantum Communications and Quantum Imaging XVIII. Vol. 11507. SPIE. 2020, pp. 49–60

work page 2020

-

[62]

Quantum computational finance: Monte Carlo pricing of financial derivatives

Patrick Rebentrost, Brajesh Gupt, and Thomas R. Bromley. “Quantum computational finance: Monte Carlo pricing of financial derivatives”. In:Phys. Rev. A98 (2 2018), p. 022321.doi: 10.1103/PhysRevA.98.022321

-

[63]

Quantum computational finance: quantum algorithm for portfolio optimization

Patrick Rebentrost and Seth Lloyd. “Quantum computational finance: quantum algorithm for portfolio optimization”. In:arXiv preprint arXiv:1811.03975 (2018)

work page internal anchor Pith review Pith/arXiv arXiv 2018

-

[64]

Quantum arithmetic with the quantum Fourier transform

Lidia Ruiz-Perez and Juan Carlos Garcia-Escartin. “Quantum arithmetic with the quantum Fourier transform”. In:Quantum Information Processing16.6 (2017). issn: 1573-1332. doi: 10.1007/s11128-017-1603-1

-

[65]

Linear-depth quantum circuits for n-qubit Toffoli gates with no ancilla

Mehdi Saeedi and Massoud Pedram. “Linear-depth quantum circuits for n-qubit Toffoli gates with no ancilla”. In:Physical Review A87.6 (2013), p. 062318

work page 2013

-

[66]

Quantum arithmetic operations based on quantum fourier transform on signed integers

Engin Şahin. “Quantum arithmetic operations based on quantum fourier transform on signed integers”. In:International Journal of Quantum Information18.06 (2020), p. 2050035

work page 2020

-

[67]

RectangularConfidenceRegionsfortheMeansofMultivariateNormalDistributions

ZbyněkŠidák.“RectangularConfidenceRegionsfortheMeansofMultivariateNormalDistributions”.In: Journal of the American Statistical Association62.318 (1967), pp. 626–633.doi: 10.1080/01621459.1967.10482935. eprint: https://doi.org/10.1080/ 01621459.1967.10482935

-

[68]

Option pricing using quantum computers

Nikitas Stamatopoulos, Daniel J Egger, Yue Sun, Christa Zoufal, Raban Iten, Ning Shen, and Stefan Woerner. “Option pricing using quantum computers”. In:Quantum 4 (2020), p. 291

work page 2020

-

[69]

Amplitude estimation without phase estimation

Yohichi Suzuki, Shumpei Uno, Rudy Raymond, Tomoki Tanaka, Tamiya Onodera, and Naoki Yamamoto. “Amplitude estimation without phase estimation”. In:Quantum Information Processing19.2 (2020), pp. 1–17

work page 2020

-

[70]

Quantum state preparation for bell-shaped probability distributions using deconvolution methods

Camille de Valk, Ankur Raina, Julian van Velzen, et al. “Quantum state preparation for bell-shaped probability distributions using deconvolution methods”. In:arXiv preprint arXiv:2310.05044(2023)

-

[71]

Quantum networks for elementary arithmetic operations

Vlatko Vedral, Adriano Barenco, and Artur Ekert. “Quantum networks for elementary arithmetic operations”. In:Physical Review A 54.1 (1996), 147–153.issn: 1094-1622. doi: 10.1103/physreva.54.147

-

[72]

Chu-Ryang Wie. “Simpler quantum counting”. In:Quantum Information and Computation19.11 and 12 (), pp. 0967–0983

-

[73]

Stefan Woerner and Daniel J. Egger. “Quantum risk analysis”. In:npj Quantum Information5.1 (2019). issn: 2056-6387. doi: 10.1038/s41534-019-0130-6

-

[74]

Adaptive Algorithm for Quantum Amplitude Estimation

Yunpeng Zhao, Haiyan Wang, Kuai Xu, Yue Wang, Ji Zhu, and Feng Wang. “Adaptive Algorithm for Quantum Amplitude Estimation”. In:arXiv preprint arXiv:2206.08449(2022)

-

[75]

Quantum Generative Adversarial Networks for learning and loading random distributions

Christa Zoufal, Aurélien Lucchi, and Stefan Woerner. “Quantum Generative Adversarial Networks for learning and loading random distributions”. In:npj Quantum Information5.1 (2019), p. 103.issn: 2056-6387. doi: 10.1038/s41534-019-0223-2. 57

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.