Regime-Aware Conditional Neural Processes with Multi-Criteria Decision Support for Operational Electricity Price Forecasting

Pith reviewed 2026-05-19 02:20 UTC · model grok-4.3

The pith

A regime-aware conditional neural process model ranks as the most balanced for operational electricity price forecasting across multiple years.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

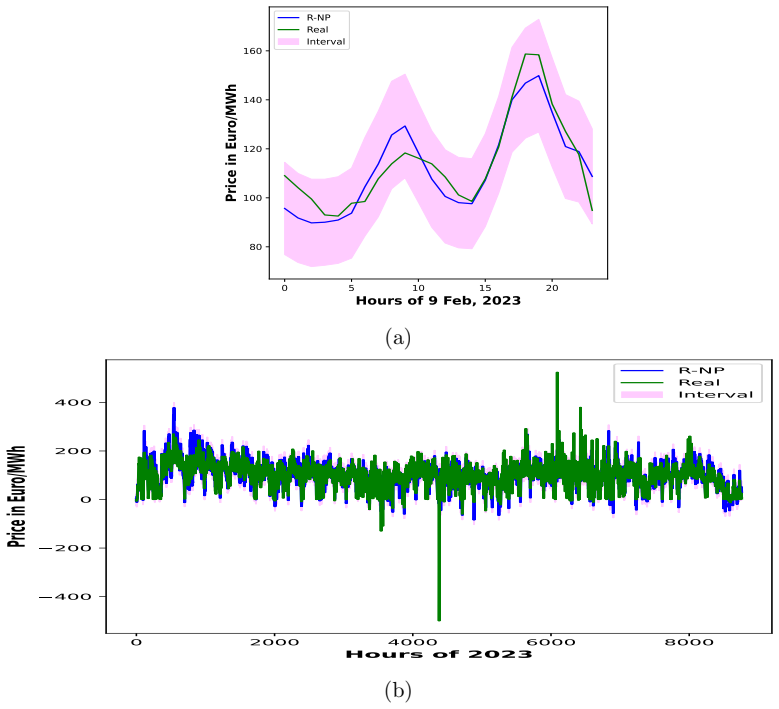

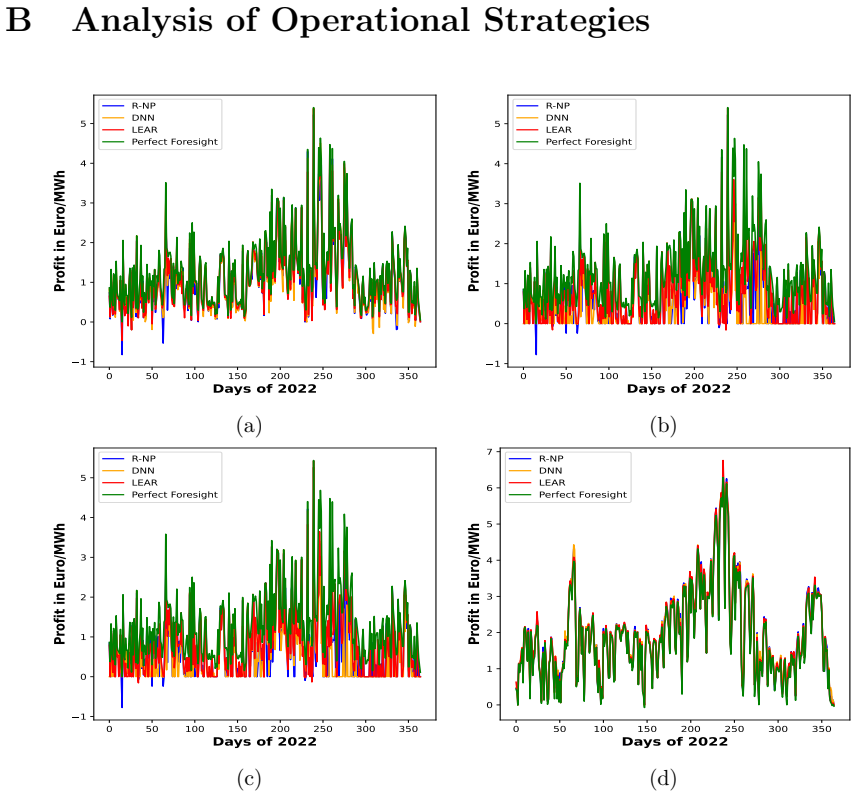

The central claim is that regime detection with DS-HDP-HMM followed by regime-specific conditional neural processes produces forecasts whose operational utility, when measured through battery optimization outcomes and TOPSIS ranking, makes the resulting R-NP model the most balanced solution for the German electricity market over 2021-2023.

What carries the argument

Regime-weighted mixture of conditional neural processes, where DS-HDP-HMM identifies price regimes and each independent CNP learns localized context-to-trajectory mappings.

If this is right

- Raw forecast accuracy is not sufficient; operational value must be judged through integration with downstream optimization tasks.

- Multi-criteria methods like TOPSIS are required to identify models that perform consistently rather than excelling in isolated metrics.

- Regime-aware modeling can deliver more reliable performance when market conditions shift across years.

- The approach highlights trade-offs where one model leads in profit but another maintains better overall balance.

Where Pith is reading between the lines

- Similar regime detection plus localized neural modeling could improve forecasts in other volatile series such as renewable output or demand.

- Extending TOPSIS criteria to include uncertainty quantification might further strengthen operational decision support.

- Testing the framework on additional markets would clarify whether the balance advantage generalizes beyond German prices.

Load-bearing premise

The detected regimes remain stable and distinct enough that training separate conditional neural processes on them yields useful localized predictions rather than noise or overfitting.

What would settle it

If disabling the regime detection step or shuffling the regime assignments causes the R-NP model to lose its top TOPSIS rank across the battery optimization scenarios, the benefit of the regime-aware structure would be refuted.

Figures

read the original abstract

This work integrates Bayesian regime detection with conditional neural processes for 24-hour electricity price prediction in the German market. Our methodology integrates regime detection using a disentangled sticky hierarchical Dirichlet process hidden Markov model (DS-HDP-HMM) applied to daily electricity prices. Each identified regime is subsequently modeled by an independent conditional neural process (CNP), trained to learn localized mappings from input contexts to 24-dimensional hourly price trajectories, with final predictions computed as regime-weighted mixtures of these CNP outputs. We rigorously evaluate R-NP against deep neural networks (DNN) and Lasso estimated auto-regressive (LEAR) models by integrating their forecasts into diverse battery storage optimization frameworks, including price arbitrage, risk management, grid services, and cost minimization. This operational utility assessment revealed complex performance trade-offs: LEAR often yielded superior absolute profits or lower costs, while DNN showed exceptional optimality in specific cost-minimization contexts. Recognizing that raw prediction accuracy doesn't always translate to optimal operational outcomes, we employed TOPSIS as a comprehensive multi-criteria evaluation layer. Our TOPSIS analysis identified LEAR as the top-ranked model for 2021, but crucially, our proposed R-NP model emerged as the most balanced and preferred solution for 2021, 2022 and 2023.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper introduces a regime-aware conditional neural process (R-NP) for 24-hour electricity price forecasting in the German market. It applies a disentangled sticky hierarchical Dirichlet process hidden Markov model (DS-HDP-HMM) to detect regimes in daily prices, trains separate conditional neural processes (CNPs) on data from each regime to learn localized mappings to 24-dimensional hourly trajectories, and computes final forecasts as regime-weighted mixtures. These forecasts are evaluated by embedding them into battery storage optimization frameworks for price arbitrage, risk management, grid services, and cost minimization. Multi-criteria ranking via TOPSIS is used to assess trade-offs, with the central claim that R-NP emerges as the most balanced and preferred model across 2021–2023, even though LEAR may achieve higher absolute profits in some scenarios.

Significance. If the reported results hold, the work makes a useful contribution by demonstrating how nonparametric Bayesian regime detection combined with per-regime neural processes can deliver more stable operational performance than single-model baselines in volatile electricity markets. The explicit use of TOPSIS together with four distinct battery optimization scenarios directly addresses the mismatch between raw forecast accuracy and downstream decision utility. Strengths include the provision of regime counts, transition matrices, per-regime CNP training details, explicit TOPSIS weights, and reproducible optimization setups, which support verification and extension of the claims.

major comments (2)

- §4 (Regime detection and mixture construction): the procedure for obtaining out-of-sample regime probabilities that weight the CNP outputs is described at a high level but lacks an explicit algorithmic statement (e.g., whether a forward pass on the sticky HDP-HMM transition matrix is performed or whether the last observed regime is used as a point estimate). This step is load-bearing for the claimed mixture predictions and for reproducing the reported rankings.

- §5.2 (TOPSIS evaluation): the conclusion that R-NP is the most balanced solution for 2021–2023 rests on a single set of criteria weights; no sensitivity analysis with respect to these weights or to the four optimization scenarios is presented. Because small perturbations in weights can reorder the TOPSIS ranking, the robustness of the central multi-criteria claim remains unverified.

minor comments (3)

- Abstract: quantitative TOPSIS scores or at least the number of identified regimes would make the performance claims more concrete for readers who do not reach the full results section.

- Figure captions and tables: several figures showing price trajectories or transition matrices would benefit from explicit axis labels indicating the time period and from accompanying numerical tables of the underlying values.

- Notation: the input context dimension and output trajectory dimension of the CNP are introduced late; defining them once in §3 would improve readability.

Simulated Author's Rebuttal

We thank the referee for the constructive feedback and positive evaluation of our work. We address each major comment in detail below and have updated the manuscript accordingly to enhance clarity and robustness.

read point-by-point responses

-

Referee: §4 (Regime detection and mixture construction): the procedure for obtaining out-of-sample regime probabilities that weight the CNP outputs is described at a high level but lacks an explicit algorithmic statement (e.g., whether a forward pass on the sticky HDP-HMM transition matrix is performed or whether the last observed regime is used as a point estimate). This step is load-bearing for the claimed mixture predictions and for reproducing the reported rankings.

Authors: We appreciate the referee pointing out the need for greater explicitness in this critical step. Upon review, the out-of-sample regime probabilities are computed via a forward pass through the DS-HDP-HMM using the posterior transition probabilities and the most recent context of daily prices to infer the regime distribution for the forecast day. This distribution then weights the outputs of the regime-specific CNPs. To improve the manuscript, we have inserted a precise algorithmic description, including pseudocode, in the revised version of Section 4. This addition directly addresses the reproducibility concern. revision: yes

-

Referee: §5.2 (TOPSIS evaluation): the conclusion that R-NP is the most balanced solution for 2021–2023 rests on a single set of criteria weights; no sensitivity analysis with respect to these weights or to the four optimization scenarios is presented. Because small perturbations in weights can reorder the TOPSIS ranking, the robustness of the central multi-criteria claim remains unverified.

Authors: The referee correctly identifies that our TOPSIS analysis relies on a fixed set of weights. These weights were chosen to reflect a balanced view across profit maximization, risk minimization, and operational feasibility based on domain expertise in electricity markets. However, to verify robustness, we have performed and now report a sensitivity analysis in the revised manuscript. Specifically, we re-computed TOPSIS rankings under perturbed weights (e.g., increasing emphasis on profit by 10-30%) and across the individual optimization scenarios. The analysis confirms that R-NP maintains its position as the most balanced model in the majority of cases, although LEAR can rank higher under strong profit-focused weightings, consistent with our original observations. We believe this addition substantiates the central claim. revision: yes

Circularity Check

No significant circularity; empirical pipeline is self-contained

full rationale

The paper presents an empirical workflow: DS-HDP-HMM regime detection on daily prices, followed by independent per-regime CNP training for 24-hour forecasts, mixture weighting, and downstream evaluation via battery optimization scenarios plus TOPSIS ranking. These steps are described with explicit regime counts, transition matrices, per-regime training details, TOPSIS weights, and four optimization scenarios. No equation or claim reduces a prediction to a fitted input by construction, nor does any load-bearing premise collapse to a self-citation chain or ansatz smuggled from prior author work. The reported rankings follow directly from the stated criteria and are externally falsifiable against real market outcomes.

Axiom & Free-Parameter Ledger

free parameters (2)

- DS-HDP-HMM concentration and stickiness parameters

- CNP architecture and training hyperparameters per regime

axioms (1)

- domain assumption Electricity price series contain latent regimes that a sticky HDP-HMM can identify in a way that improves downstream forecasting

Lean theorems connected to this paper

-

IndisputableMonolith/Foundation/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

Our methodology integrates regime detection using a disentangled sticky hierarchical Dirichlet process hidden Markov model (DS-HDP-HMM) ... Each identified regime is subsequently modeled by an independent conditional neural process (CNP) ... final predictions computed as regime-weighted mixtures ... TOPSIS as a comprehensive multi-criteria evaluation layer.

-

IndisputableMonolith/Foundation/AbsoluteFloorClosure.leanreality_from_one_distinction unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

The DS-HDP-HMM ... Sticky HDP-HMM ... Disentangled Sticky HDP-HMM

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

Dynamic Regime Switching Models, pages 111–156

Samit Ahlawat. Dynamic Regime Switching Models, pages 111–156. Apress, Berkeley, CA, 2025

work page 2025

-

[2]

A review on the selected applications of fore- casting models in renewable power systems

Adil Ahmed and Muhammad Khalid. A review on the selected applications of fore- casting models in renewable power systems. Renewable and Sustainable Energy Re- views, 100:9–21, 2019

work page 2019

-

[3]

Muneer M Alshater, Ilias Kampouris, Hazem Marashdeh, Osama F Atayah, and Hasanul Banna. Early warning system to predict energy prices: the role of artificial intelligence and machine learning. Annals of Operations Research, 345(2):1297–1333, 2025

work page 2025

-

[4]

pvlib python: 2023 project update

Kevin Anderson, Clifford Hansen, William Holmgren, Adam Jensen, Mark Mikofski, and Anton Driesse. pvlib python: 2023 project update. Journal of Open Source Software, 8:5994, 12 2023

work page 2023

-

[5]

James Bergstra, Daniel Yamins, and David Cox. Making a science of model search: Hyperparameter optimization in hundreds of dimensions for vision architectures. In Sanjoy Dasgupta and David McAllester, editors, Proceedings of the 30th Inter- national Conference on Machine Learning , volume 28 of Proceedings of Machine Learning Research, pages 115–123, Atla...

work page 2013

-

[6]

Modeling electricity prices with regime switching models

Michael Bierbrauer, Stefan Tr¨ uck, and Rafa l Weron. Modeling electricity prices with regime switching models. In Marian Bubak, Geert Dick van Albada, Peter M. A. Sloot, and Jack Dongarra, editors, Computational Science - ICCS 2004 , pages 859–867, Berlin, Heidelberg, 2004. Springer Berlin Heidelberg

work page 2004

-

[7]

PROMETHEE Methods , pages 187–219

Jean-Pierre Brans and Yves De Smet. PROMETHEE Methods , pages 187–219. Springer New York, New York, NY, 2016

work page 2016

-

[8]

Joshua C.C. Chan and Angelia L. Grant. Modeling energy price dynamics: Garch versus stochastic volatility. Energy Economics, 54:182–189, 2016

work page 2016

-

[9]

Extensions of the topsis for group decision-making under fuzzy environment

Chen-Tung Chen. Extensions of the topsis for group decision-making under fuzzy environment. Fuzzy Sets and Systems , 114(1):1–9, 2000

work page 2000

-

[10]

Methods and Applications A State-of-the-Art Survey, pages XI–269

Kwangsun Yoon Ching-Lai Hwang. Methods and Applications A State-of-the-Art Survey, pages XI–269. Springer Berlin, Heidelberg, Berkeley, CA, 1981

work page 1981

-

[11]

Arima models in electrical load forecasting and their robustness to noise

Ewa Chodakowska, Joanicjusz Nazarko, and Lukasz Nazarko. Arima models in electrical load forecasting and their robustness to noise. Energies, 14(23), 2021

work page 2021

-

[12]

Cameron Cornell, Nam Trong Dinh, and S. Ali Pourmousavi. A probabilistic fore- cast methodology for volatile electricity prices in the australian national electricity market. International Journal of Forecasting, 40(4):1421–1437, 2024

work page 2024

-

[13]

Abhinav Das, Stephan Schl¨ uter, and Lorenz Schneider. Electricity price prediction using multi-kernel gaussian process regression combined with kernel-based support vector regression, 2025. 42

work page 2025

-

[14]

Marcos de Castro Matias and Benjamin Miranda Tabak. Comparison of indica- tor saturation and markov regime-switching models for brazilian electricity prices. Energy Economics, 144:108341, 2025

work page 2025

-

[15]

Uncertainty measures and sector-specific reits in a regime-switching environment

Sercan Demiralay and Erhan Kilincarslan. Uncertainty measures and sector-specific reits in a regime-switching environment. The Journal of Real Estate Finance and Economics, 69(3):545–584, 2024

work page 2024

-

[16]

Forecasting electricity spot market prices with a k-factor gigarch process

Abdou Kˆ a Diongue, Dominique Gu´ egan, and Bertrand Vignal. Forecasting electricity spot market prices with a k-factor gigarch process. Applied Energy, 86(4):505–510, 2009

work page 2009

-

[17]

Negin Entezari and Jos´ e Alberto Fuinhas. Quantifying the impact of risk on market volatility and price: Evidence from the wholesale electricity market in portugal. Sustainability, 16(7), 2024

work page 2024

-

[18]

Assessment of the impacts of renewable energy variability in long-term decarbonization strategies

Francisco Flores, Felipe Feijoo, Paelina DeStephano, Luka Herc, Antun Pfeifer, and Neven Dui´ c. Assessment of the impacts of renewable energy variability in long-term decarbonization strategies. Applied Energy, 368:123464, 2024

work page 2024

-

[19]

Fraunhofer Institute for Solar Energy system. Public net electricity generation 2023 in germany: Renewables cover the majority of the electricity consumption for the first time. Press-release, pages 1–6., 2024. (Accessed: 23 Jan 2025)

work page 2023

-

[20]

Emily B. Fox, Erik B. Sudderth, Michael I. Jordan, and Alan S. Willsky. An hdp- hmm for systems with state persistence. In Proceedings of the 25th International Conference on Machine Learning , ICML ’08, page 312–319, New York, NY, USA,

-

[21]

Association for Computing Machinery

-

[22]

Data- driven modeling for long-term electricity price forecasting

Paolo Gabrielli, Moritz W¨ uthrich, Steffen Blume, and Giovanni Sansavini. Data- driven modeling for long-term electricity price forecasting. Energy, 244:123107, 2022

work page 2022

-

[23]

Marta Garnelo, Jonathan Schwarz, Dan Rosenbaum, Fabio Viola, Danilo J. Rezende, S. M. Ali Eslami, and Yee Whye Teh. Neural processes.CoRR, abs/1807.01622, 2018

work page internal anchor Pith review Pith/arXiv arXiv 2018

-

[24]

Deo, David Casillas-P´ erez, and Sancho Salcedo-Sanz

Sujan Ghimire, Ravinesh C. Deo, David Casillas-P´ erez, and Sancho Salcedo-Sanz. Two-step deep learning framework with error compensation technique for short-term, half-hourly electricity price forecasting. Applied Energy, 353:122059, 2024

work page 2024

-

[25]

Gonzalez, Antonio Mu˜ noz, and Javier Garc´ ıa-Gonz´ alez

A.M. Gonzalez, Antonio Mu˜ noz, and Javier Garc´ ıa-Gonz´ alez. Modeling and fore- casting electricity prices with input/output hidden markov models. Power Systems, IEEE Transactions on, 20:13 – 24, 03 2005

work page 2005

-

[26]

A regime switching long memory model for electricity prices

Niels Haldrup and Morten Ø rregaard Nielsen. A regime switching long memory model for electricity prices. J. Econometrics, 135(1-2):349–376, 2006

work page 2006

- [27]

-

[28]

Regime jumps in electricity prices

Ronald Huisman and Ronald Mahieu. Regime jumps in electricity prices. Energy Economics, 25(5):425–434, 2003. 43

work page 2003

-

[29]

Christian Huurman, Francesco Ravazzolo, and Chen Zhou. The power of weather. Computational Statistics & Data Analysis , 56(11):3793–3807, 2012. 1st issue of the Annals of Computational and Financial Econometrics Sixth Special Issue on Computational Econometrics

work page 2012

-

[30]

Inference for Markov regime-switching models of electricity spot prices

Joanna Janczura and Rafa lWeron. Inference for Markov regime-switching models of electricity spot prices. In Quantitative energy finance, pages 137–155. Springer, New York, 2014

work page 2014

-

[31]

Ping Jiang, Ying Nie, Jianzhou Wang, and Xiaojia Huang. Multivariable short-term electricity price forecasting using artificial intelligence and multi-input multi-output scheme. Energy Economics, 117:106471, 2023

work page 2023

-

[32]

Paul Johnson, D´ avid Zolt´ an Szab´ o, and Peter Duck. Optimal trading with regime switching: numerical and analytic techniques applied to valuing storage in an elec- tricity balancing market. European J. Oper. Res., 319(2):611–624, 2024

work page 2024

-

[33]

Gaurav Kapoor, Nuttanan Wichitaksorn, and Wenjun Zhang. Analyzing and fore- casting electricity price using regime-switching models: the case of New Zealand market. J. Forecast., 42(8):2011–2026, 2023

work page 2011

- [34]

-

[35]

Review of grid applications with the zurich 1mw battery energy storage system

Michael Koller, Theodor Borsche, Andreas Ulbig, and G¨ oran Andersson. Review of grid applications with the zurich 1mw battery energy storage system. Electric Power Systems Research , 120:128–135, 2015. Smart Grids: World’s Actual Imple- mentations

work page 2015

-

[36]

Jesus Lago, Grzegorz Marcjasz, Bart De Schutter, and Rafa l Weron. Forecasting day-ahead electricity prices: A review of state-of-the-art algorithms, best practices and an open-access benchmark. Applied Energy, 293:116983, 2021

work page 2021

-

[37]

Fran¸ cois Le Grand and Lorenz Schneider. The variance risk premium in crude oil futures markets: Incorporating the ovx time series in a stochastic volatility model. Available at SSRN 4013711 , 2022

work page 2022

- [38]

-

[39]

A hybrid SETARX model for spikes in tight electricity markets

Carlo Lucheroni. A hybrid SETARX model for spikes in tight electricity markets. Oper. Res. Decis., 22(1):13–49, 2012

work page 2012

-

[40]

Forecasting electric- ity prices, 07 2023

Katarzyna Maciejowska, Bartosz Uniejewski, and Rafal Weron. Forecasting electric- ity prices, 07 2023

work page 2023

-

[41]

The value of elec- tricity storage arbitrage on day-ahead markets across europe

Thomas Mercier, Mathieu Olivier, and Emmanuel De Jaeger. The value of elec- tricity storage arbitrage on day-ahead markets across europe. Energy Economics, 123:106721, 2023. 44

work page 2023

-

[42]

Ciaran O’Connor, Mohamed Bahloul, Roberto Rossi, Steven Prestwich, and Andrea Visentin. Conformal prediction for electricity price forecasting in the day-ahead and real-time balancing market. arXiv preprint arXiv:2502.04935 , 2025

-

[43]

Electricity price forecast- ing via statistical and deep learning approaches: The german case

Aurora Poggi, Luca Di Persio, and Matthias Ehrhardt. Electricity price forecast- ing via statistical and deep learning approaches: The german case. AppliedMath, 3(2):316–342, 2023

work page 2023

-

[44]

Alireza Pourdaryaei, Mohammad Mohammadi, Hamza Mubarak, Abdallah Abdel- latif, Mazaher Karimi, Elena Gryazina, and Vladimir Terzija. A new framework for electricity price forecasting via multi-head self-attention and cnn-based techniques in the competitive electricity market. Expert Systems with Applications, 235:121207, 2024

work page 2024

-

[45]

L. Rabiner and B. Juang. An introduction to hidden markov models. IEEE ASSP Magazine, 3(1):4–16, 1986

work page 1986

-

[46]

Control strategies for residential battery energy storage systems coupled with pv sys- tems

Iromi Ranaweera, Ole-Morten Midtg˚ ard, Magnus Korp˚ as, and Hossein Farahmand. Control strategies for residential battery energy storage systems coupled with pv sys- tems. In 2017 IEEE International Conference on Environment and Electrical Engi- neering and 2017 IEEE Industrial and Commercial Power Systems Europe (EEEIC / I&CPS Europe), pages 1–6, 2017

work page 2017

-

[47]

Powering the future: A comprehensive review of battery energy storage systems

Sergi Obrador Rey, Juan Alberto Romero, Lluis Trilla Romero,`Alber Filb` a Mart´ ınez, Xavier Sanchez Roger, Muhammad Attique Qamar, Jos´ e Luis Dom´ ınguez-Garc´ ıa, and Levon Gevorkov. Powering the future: A comprehensive review of battery energy storage systems. Energies, 16(17), 2023

work page 2023

-

[48]

Forecasting volatility by using wavelet transform, arima and garch models

Lihki Rubio, Adriana Palacio Pinedo, Adriana Mej´ ıa Casta˜ no, and Filipe Ramos. Forecasting volatility by using wavelet transform, arima and garch models. Eurasian Economic Review, 13(3):803–830, 2023

work page 2023

-

[49]

S. Schluter and C. Deuschle. Wavelet-based forecasting of arima time series - an empirical comparison of different methods. Managerial Economics, 15(1):107–131, 2014

work page 2014

-

[50]

Optimal control of a battery storage on the energy market

Stephan Schl¨ uter, Abhinav Das, and Matthew Davison. Optimal control of a battery storage on the energy market. In 2024 IEEE/IAS Industrial and Commercial Power System Asia (I&CPS Asia) , pages 102–107, 2024

work page 2024

-

[51]

Short-term variations and long-term dynamics in commodity prices

Eduardo Schwartz and James Smith. Short-term variations and long-term dynamics in commodity prices. Management Science, 46:893–911, 07 2000

work page 2000

-

[52]

Deepak Singhal and K.S. Swarup. Electricity price forecasting using artificial neural networks. International Journal of Electrical Power & Energy Systems , 33(3):550– 555, 2011

work page 2011

-

[53]

Sharing clusters among related groups: Hierarchical dirichlet processes

Yee Teh, Michael Jordan, Matthew Beal, and David Blei. Sharing clusters among related groups: Hierarchical dirichlet processes. Advances in neural information processing systems, 17, 2004. 45

work page 2004

-

[54]

Ashish Vaswani, Noam Shazeer, Niki Parmar, Jakob Uszkoreit, Llion Jones, Aidan N Gomez, Lukasz Kaiser, and Illia Polosukhin. Attention is all you need. Advances in neural information processing systems, 30, 2017

work page 2017

-

[55]

Almut E. D. Veraart. Modelling the impact of wind power production on electricity prices by regime-switching L´ evy semistationary processes. InStochastics of environ- mental and financial economics—Centre of Advanced Study, Oslo, Norway, 2014– 2015, volume 138 of Springer Proc. Math. Stat. , pages 321–340. Springer, Cham, 2016

work page 2014

-

[56]

A hybrid electricity price forecasting model for the nordic electricity spot market

Sergey Voronin, Jarmo Partanen, and Tuomo Kauranne. A hybrid electricity price forecasting model for the nordic electricity spot market. International Transactions on Electrical Energy Systems , 24(5):736–760, 2014

work page 2014

-

[57]

Heavy-tails and regime-switching in electricity prices

Rafa lWeron. Heavy-tails and regime-switching in electricity prices. Math. Methods Oper. Res., 69(3):457–473, 2009

work page 2009

-

[58]

The effects of reducing renewable power intermittency through port- folio diversification

Igor Westphal. The effects of reducing renewable power intermittency through port- folio diversification. Renewable and Sustainable Energy Reviews , 197:114415, 2024

work page 2024

-

[59]

Resilience of renewable power systems under climate risks

Luo Xu, Kairui Feng, Ning Lin, ATD Perera, H Vincent Poor, Le Xie, Chuanyi Ji, X Andy Sun, Qinglai Guo, and Mark O’Malley. Resilience of renewable power systems under climate risks. Nature reviews electrical engineering, 1(1):53–66, 2024

work page 2024

-

[60]

Yuqing Yang, Stephen Bremner, Chris Menictas, and Merlinde Kay. Modelling and optimal energy management for battery energy storage systems in renewable energy systems: A review. Renewable and Sustainable Energy Reviews , 167:112671, 2022

work page 2022

-

[61]

Disentangled sticky hierarchical dirichlet process hidden markov model

Ding Zhou, Yuanjun Gao, and Liam Paninski. Disentangled sticky hierarchical dirichlet process hidden markov model. In Joint European Conference on Machine Learning and Knowledge Discovery in Databases , pages 612–627. Springer, 2020. 46 Appendices A Theoretical Motivation for Transitioning from HDP- HMM to Sticky and Disentangled Sticky HDP- HMM In this s...

work page 2020

-

[62]

Expected self-transition: E[πDS jj ] = E[κj] + (1 − E[κj])βj = ρ1 ρ1 + ρ2 + 1 − ρ1 ρ1 + ρ2 βj

-

[63]

Expected transition to k ̸= j: E[πDS jk ] = (1 − E[κj])βk. Proof. The transition is a convex mixture. Taking expectations: E[πDS jj ] = E[κj] + (1 − E[κj])E[πjj] = E[κj] + (1 − E[κj])βj, E[πDS jk ] = (1 − E[κj])βk (k ̸= j). Remark 4 (Why DS-HDP-HMM is Preferable to sHDP-HMM). In DS-HDP-HMM, the persistence probability κj is modeled separately via a Beta d...

work page 2022

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.