Recognition: unknown

EvoNash-MARL: A Closed-Loop Multi-Agent Reinforcement Learning Framework for Medium-Horizon Equity Allocation

Pith reviewed 2026-05-10 16:31 UTC · model grok-4.3

The pith

EvoNash-MARL combines multi-agent RL with game-theoretic aggregation to achieve 19.6 percent annualized returns in equity allocation outperforming SPY.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The central claim is that EvoNash-MARL integrates multi-agent policy populations, game-theoretic aggregation, and constraint-aware validation inside a unified walk-forward design to improve robustness in medium- to long-horizon equity allocation. Under a 120-window walk-forward protocol the final configuration records the highest robust score among internal baselines. On out-of-sample data from 2014 to 2024 it produces a 19.6 percent annualized return compared with 11.7 percent for SPY and stays stable through extended evaluation to 2026, showing consistent behavior under realistic constraints and across market settings, although strong global statistical significance is not obtained under W

What carries the argument

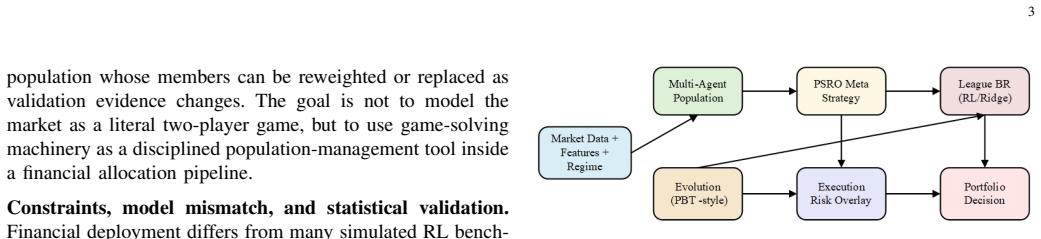

The closed-loop framework that unites multi-agent policy populations, game-theoretic aggregation, and constraint-aware validation inside a single walk-forward protocol, which works by enforcing execution realism and population-level competition to limit overfitting under distributional shift.

If this is right

- The framework records the highest robust score among all internal baselines under the 120-window protocol.

- It produces 19.6 percent annualized returns on 2014-2024 out-of-sample equity data versus 11.7 percent for SPY.

- Performance remains stable when evaluation is extended through 2026.

- Results hold under realistic trading constraints and across varying market regimes.

- The outcome supplies evidence of improved robustness without establishing definitive statistical superiority in market timing.

Where Pith is reading between the lines

- The same closed-loop structure could be tested on shorter-horizon or multi-asset problems to check whether the robustness benefit travels beyond equity allocation.

- The emphasis on execution-aware selection implies that real-world slippage and cost modeling may be more decisive for performance than the choice of learning algorithm itself.

- Absence of strong statistical significance under WRC and SPA-lite tests suggests that larger cross-market panels or additional reality-check procedures would be needed to elevate the result from robustness evidence to timing proof.

Load-bearing premise

The 120-window walk-forward protocol together with execution-aware selection and game-theoretic aggregation is assumed to remove selection bias and look-ahead effects while still reflecting realistic trading conditions.

What would settle it

A new out-of-sample test after 2026 in which the framework loses its return advantage over SPY or its top robust-score ranking among comparable methods would directly challenge the robustness claim.

Figures

read the original abstract

Medium- to long-horizon equity allocation is challenging due to weak predictive structure, non-stationary market regimes, and the degradation of signals under realistic trading constraints. Conventional approaches often rely on single predictors or loosely coupled pipelines, which limit robustness under distributional shift. This paper proposes EvoNash-MARL, a closed-loop framework that integrates reinforcement learning with population-based policy optimization and execution-aware selection to improve robustness in medium- to long-horizon allocation. The framework combines multi-agent policy populations, game-theoretic aggregation, and constraint-aware validation within a unified walk-forward design. Under a 120-window walk-forward protocol, the final configuration achieves the highest robust score among internal baselines. On out-of-sample data from 2014 to 2024, it delivers a 19.6% annualized return, compared to 11.7% for SPY, and remains stable under extended evaluation through 2026. While the framework demonstrates consistent performance under realistic constraints and across market settings, strong global statistical significance is not established under White's Reality Check (WRC) and SPA-lite tests. The results therefore provide evidence of improved robustness rather than definitive proof of superior market timing performance.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes EvoNash-MARL, a closed-loop multi-agent reinforcement learning framework for medium-horizon equity allocation. It integrates reinforcement learning with population-based policy optimization, game-theoretic aggregation, and execution-aware selection in a unified walk-forward design. The framework is evaluated under a 120-window walk-forward protocol, achieving the highest robust score among internal baselines and delivering 19.6% annualized returns on out-of-sample data from 2014 to 2024 compared to 11.7% for SPY, with stability through 2026. The authors note that strong global statistical significance is not established under White's Reality Check (WRC) and SPA-lite tests, positioning the results as evidence of improved robustness rather than definitive proof of superior performance.

Significance. Should the robustness under realistic constraints be confirmed, the framework could advance the application of multi-agent RL in finance by providing a closed-loop method for medium-horizon allocation. The manuscript deserves credit for employing a walk-forward protocol and for openly stating the limitations regarding statistical significance under WRC and SPA-lite tests. These elements strengthen the work's transparency.

major comments (2)

- [Abstract] Abstract: The central claim that the final configuration achieves the highest robust score and delivers 19.6% annualized return (vs. 11.7% for SPY) on 2014-2024 out-of-sample data is presented alongside the explicit statement that strong global statistical significance is not established under WRC and SPA-lite tests. This is load-bearing for the robustness interpretation, as the large number of internal baselines combined with free parameters (RL hyperparameters and population sizes) creates a substantial multiple-testing risk that the walk-forward protocol does not automatically correct for family-wise error rates.

- [Experimental setup (120-window walk-forward protocol)] 120-window walk-forward protocol: The protocol with execution-aware selection and game-theoretic aggregation is described as mitigating overfitting and capturing realistic trading conditions. However, the manuscript provides insufficient detail on how repeated tuning avoids incorporating in-sample information or introducing selection bias/look-ahead effects, which directly affects verification of the weakest assumption underlying the out-of-sample performance claims.

minor comments (1)

- [Abstract] The abstract states that the configuration 'remains stable under extended evaluation through 2026' without specifying the exact metrics, conditions, or comparison baselines used for this stability assessment, which reduces clarity.

Simulated Author's Rebuttal

We thank the referee for the constructive and balanced review, particularly for acknowledging the manuscript's transparency on statistical limitations. We address each major comment below and will incorporate revisions to strengthen the presentation of the framework and its evaluation protocol.

read point-by-point responses

-

Referee: [Abstract] The central claim that the final configuration achieves the highest robust score and delivers 19.6% annualized return (vs. 11.7% for SPY) on 2014-2024 out-of-sample data is presented alongside the explicit statement that strong global statistical significance is not established under WRC and SPA-lite tests. This is load-bearing for the robustness interpretation, as the large number of internal baselines combined with free parameters (RL hyperparameters and population sizes) creates a substantial multiple-testing risk that the walk-forward protocol does not automatically correct for family-wise error rates.

Authors: We agree that the multiple-testing risk arising from numerous internal baselines and free parameters is a substantive concern that the walk-forward protocol alone does not fully resolve. The manuscript already qualifies its central claim by explicitly stating that strong global statistical significance is not established under WRC and SPA-lite tests, framing the 19.6% annualized return as evidence of improved robustness rather than definitive superiority. To address this directly, we will revise the abstract to emphasize that the reported performance is the highest robust score among the internal baselines evaluated, and we will add a dedicated paragraph in the Discussion section analyzing the multiple-comparisons issue and the scope of the statistical tests used. revision: yes

-

Referee: [Experimental setup (120-window walk-forward protocol)] The protocol with execution-aware selection and game-theoretic aggregation is described as mitigating overfitting and capturing realistic trading conditions. However, the manuscript provides insufficient detail on how repeated tuning avoids incorporating in-sample information or introducing selection bias/look-ahead effects, which directly affects verification of the weakest assumption underlying the out-of-sample performance claims.

Authors: We concur that greater specificity is required to allow verification that the repeated tuning process introduces no look-ahead bias. In the revised manuscript we will expand the Experimental Setup section with a precise description of the 120-window protocol: hyperparameter tuning and population-based optimization are performed exclusively on the training portion of each window using only data available up to the window's end; model selection and game-theoretic aggregation occur on a strictly held-out validation segment within the same window; and execution-aware selection is applied using only information contemporaneous with the validation period. This structure ensures that out-of-sample evaluation draws on no future data. revision: yes

Circularity Check

No significant circularity detected in derivation or claims

full rationale

The paper presents an empirical multi-agent RL framework whose central results are measured performance on explicitly out-of-sample periods (2014-2024) under a 120-window walk-forward protocol. The abstract states that the configuration achieves the highest robust score among internal baselines and reports 19.6% annualized return versus 11.7% for SPY, while openly noting that strong global statistical significance is not established under WRC and SPA-lite tests. No equations or steps are shown that define a quantity in terms of itself, rename a fitted parameter as an independent prediction, or reduce the reported outperformance to a self-citation chain or ansatz. The walk-forward design and game-theoretic aggregation are standard methodological choices whose outputs are evaluated on held-out data rather than being tautological by construction. The derivation chain therefore remains self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

free parameters (1)

- RL hyperparameters and population sizes

axioms (1)

- domain assumption The market exhibits non-stationary regimes and weak predictive signals that degrade under trading constraints.

invented entities (1)

-

EvoNash-MARL

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Lopez de Prado,Advances in Financial Machine Learning

M. Lopez de Prado,Advances in Financial Machine Learning. Wiley, 2018

2018

-

[2]

The deflated sharpe ratio: Correcting for selection bias, backtest overfitting, and non-normality,

D. H. Bailey and M. L ´opez de Prado, “The deflated sharpe ratio: Correcting for selection bias, backtest overfitting, and non-normality,” Journal of Portfolio Management, vol. 40, no. 5, pp. 94–107, 2014

2014

-

[3]

A reality check for data snooping,

H. White, “A reality check for data snooping,”Econometrica, vol. 68, no. 5, pp. 1097–1126, 2000

2000

-

[4]

A test for superior predictive ability,

P. R. Hansen, “A test for superior predictive ability,”Journal of Business & Economic Statistics, vol. 23, no. 4, pp. 365–380, 2005

2005

-

[5]

Portfolio selection,

H. Markowitz, “Portfolio selection,”The Journal of Finance, vol. 7, no. 1, pp. 77–91, 1952

1952

-

[6]

Learning to trade via direct reinforcement,

J. Moody and M. Saffell, “Learning to trade via direct reinforcement,” IEEE Transactions on Neural Networks, vol. 12, no. 4, pp. 875–889, 2001

2001

-

[7]

Reinforcement learning for optimized trade execution,

Y . Nevmyvaka, Y . Feng, and M. Kearns, “Reinforcement learning for optimized trade execution,” inProceedings of the 23rd International Conference on Machine Learning, 2006, pp. 673–680

2006

-

[8]

Finrl: A deep reinforcement learning library for automated stock trading in quantitative finance

X.-Y . Liu, H. Yang, Q. Chen, R. Zhang, L. Yang, B. Xiao, and C. D. Wang, “FinRL: A deep reinforcement learning library for automated stock trading in quantitative finance,”arXiv preprint arXiv:2011.09607, 2020

-

[9]

FinRL-Meta: Market environments and benchmarks for data-driven financial reinforcement learning,

X.-Y . Liu, Z. Xia, J. Rui, J. Gao, H. Yang, M. Zhu, C. D. Wang, Z. Wang, and J. Guo, “FinRL-Meta: Market environments and benchmarks for data-driven financial reinforcement learning,” inAdvances in Neural Information Processing Systems, vol. 35,

-

[10]

Available: https://papers.neurips.cc/paper files/paper/ 2022/hash/0bf54b80686d2c4dc0808c2e98d430f7-Abstract-Datasets and Benchmarks.html

[Online]. Available: https://papers.neurips.cc/paper files/paper/ 2022/hash/0bf54b80686d2c4dc0808c2e98d430f7-Abstract-Datasets and Benchmarks.html

2022

-

[11]

AlphaStock: A buying-winners-and-selling-losers investment strategy using inter- pretable deep reinforcement attention networks,

J. Wang, Y . Zhang, K. Tang, J. Wu, and Z. Xiong, “AlphaStock: A buying-winners-and-selling-losers investment strategy using inter- pretable deep reinforcement attention networks,” inProceedings of the 25th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, 2019, pp. 1900–1908

2019

-

[12]

DeepTrader: A deep reinforcement learning approach for risk-return balanced portfolio management with market conditions embedding,

Z. Wang, B. Huang, S. Tu, K. Zhang, and L. Xu, “DeepTrader: A deep reinforcement learning approach for risk-return balanced portfolio management with market conditions embedding,”Proceedings of the AAAI Conference on Artificial Intelligence, vol. 35, no. 1, pp. 643–650, 2021

2021

-

[13]

AlphaQCM: Alpha discovery in finance with distributional reinforcement learning,

Z. Zhu and K. Zhu, “AlphaQCM: Alpha discovery in finance with distributional reinforcement learning,” inProceedings of the 42nd International Conference on Machine Learning, ser. Proceedings of Machine Learning Research, vol. 267. PMLR, 2025, pp. 80 463–80 479. [Online]. Available: https://proceedings.mlr.press/v267/zhu25ag.html

2025

-

[14]

Multi- agent actor-critic for mixed cooperative-competitive environments,

R. Lowe, Y . Wu, A. Tamar, J. Harb, P. Abbeel, and I. Mordatch, “Multi- agent actor-critic for mixed cooperative-competitive environments,” in Advances in Neural Information Processing Systems, 2017

2017

-

[15]

A unified game-theoretic approach to multiagent reinforcement learning,

M. Lanctot, V . Zambaldi, A. Gruslys, A. Lazaridou, K. Tuyls, J. Perolat, D. Silver, and T. Graepel, “A unified game-theoretic approach to multiagent reinforcement learning,” inAdvances in Neural Information Processing Systems, 2017

2017

-

[16]

M. Jaderberg, V . Dalibard, S. Osinderoet al., “Population based training of neural networks,”arXiv preprint arXiv:1711.09846, 2017

-

[17]

Sample-efficient robust multi-agent reinforcement learning in the face of environmental uncertainty,

L. Shi, E. Mazumdar, Y . Chi, and A. Wierman, “Sample-efficient robust multi-agent reinforcement learning in the face of environmental uncertainty,” inProceedings of the 41st International Conference on Machine Learning, ser. Proceedings of Machine Learning Research, vol. 235. PMLR, 2024, pp. 44 909–44 959. [Online]. Available: https://proceedings.mlr.pre...

2024

-

[18]

Near-optimal reinforcement learning with self-play under adaptivity constraints,

D. Qiao and Y .-X. Wang, “Near-optimal reinforcement learning with self-play under adaptivity constraints,” inProceedings of the 41st International Conference on Machine Learning, ser. Proceedings of Machine Learning Research, vol. 235. PMLR, 2024, pp. 41 430–41 455. [Online]. Available: https://proceedings.mlr.press/v235/qiao24b.html

2024

-

[19]

Explicit exploration for high-welfare equilibria in game-theoretic multiagent reinforcement learning,

A. A. Nguyen, A. Gu, and M. P. Wellman, “Explicit exploration for high-welfare equilibria in game-theoretic multiagent reinforcement learning,” inProceedings of the 42nd International Conference on Machine Learning, ser. Proceedings of Machine Learning Research, vol. 267. PMLR, 2025, pp. 45 988–46 007. [Online]. Available: https://proceedings.mlr.press/v2...

2025

-

[20]

Constrained reinforcement learning under model mismatch,

Z. Sun, S. He, F. Miao, and S. Zou, “Constrained reinforcement learning under model mismatch,” inProceedings of the 41st International Conference on Machine Learning, ser. Proceedings of Machine Learning Research, vol. 235. PMLR, 2024, pp. 47 017–47 032. [Online]. Available: https://proceedings.mlr.press/v235/sun24d.html

2024

-

[21]

The max-min formulation of multi-objective reinforcement learning: From theory to a model-free algorithm,

G. Park, W. Byeon, S. Kim, E. Havakuk, A. Leshem, and Y . Sung, “The max-min formulation of multi-objective reinforcement learning: From theory to a model-free algorithm,” inProceedings of the 41st International Conference on Machine Learning, ser. Proceedings of Machine Learning Research, vol. 235. PMLR, 2024, pp. 39 616–39 642. [Online]. Available: http...

2024

-

[22]

Equilibrium points in n-person games,

J. F. Nash, “Equilibrium points in n-person games,”Proceedings of the National Academy of Sciences, vol. 36, no. 1, pp. 48–49, 1950

1950

-

[23]

A survey on self-play methods in reinforcement learning,

R. Zhang, Z. Xu, C. Ma, C. Yu, W.-W. Tu, S. Huang, D. Ye, W. Ding, Y . Yang, and Y . Wang, “A survey on self-play methods in reinforcement learning,”arXiv preprint arXiv:2408.01072, 2024. [Online]. Available: https://arxiv.org/abs/2408.01072

-

[24]

A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix,

W. K. Newey and K. D. West, “A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix,” Econometrica, vol. 55, no. 3, pp. 703–708, 1987

1987

-

[25]

The stationary bootstrap,

D. N. Politis and J. P. Romano, “The stationary bootstrap,”Journal of the American Statistical Association, vol. 89, no. 428, pp. 1303–1313, 1994

1994

-

[26]

A decision-theoretic generalization of on-line learning and an application to boosting,

Y . Freund and R. E. Schapire, “A decision-theoretic generalization of on-line learning and an application to boosting,”Journal of Computer and System Sciences, vol. 55, no. 1, pp. 119–139, 1997

1997

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.