Recognition: 2 theorem links

· Lean TheoremGeomHerd: A Forward-looking Herding Quantification via Ricci Flow Geometry on Agent Interactive Simulations

Pith reviewed 2026-05-13 01:22 UTC · model grok-4.3

The pith

Ollivier-Ricci curvature on agent action graphs detects herding coordination hundreds of steps before prices correlate.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

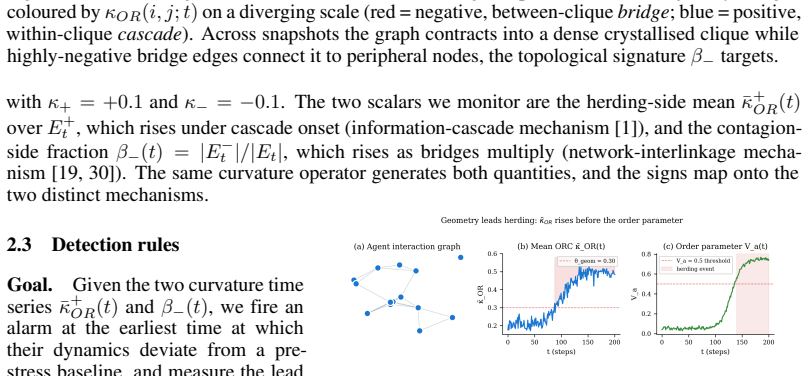

By computing the discrete Ollivier-Ricci curvature of action graphs built from heterogeneous multi-agent financial simulations, GeomHerd identifies the topological onset of collective behavior well in advance of aggregate price statistics, with a median lead of 272 steps over order-parameter onset and a 40-step lead over price-correlation graphs on co-firing trajectories.

What carries the argument

Discrete Ollivier-Ricci curvature on time-evolving graphs whose nodes are agents and whose edges encode observed action choices, which registers local geometric tightening that precedes global coordination.

If this is right

- A curvature-based detector can issue early warnings of market fragility hundreds of steps before conventional price measures activate.

- Agent-action vocabulary contracts during the same windows where curvature signals cascade formation.

- The geometric indicator remains informative when transferred to non-financial self-propelled particle models such as Vicsek.

- Conditioning a forecasting head on curvature values reduces mean-absolute error for log returns inside the detected cascade windows.

Where Pith is reading between the lines

- If the simulator-to-real gap can be closed with calibration data, the same curvature pipeline could run on live order-flow feeds without waiting for price realizations.

- Curvature thresholds might be tuned per asset class to give sector-specific lead times for regulatory alerts.

- Combining curvature with other graph invariants could sharpen the distinction between transient coordination and sustained herding.

Load-bearing premise

The coordination patterns that arise among LLM-instantiated traders in the simulator are close enough to real-market interactions that curvature changes observed in the model will appear in actual trading data.

What would settle it

Extracting comparable action graphs from real limit-order-book or trade-tape data and testing whether curvature drops systematically precede documented herding episodes or volatility spikes by hundreds of steps.

Figures

read the original abstract

Herding -- where agents align their behaviors and act collectively -- is a central driver of market fragility and systemic risk. Existing approaches to quantify herding rely on price-correlation statistics, which inherently lag because they only detect coordination after it has already moved realised returns. We propose GeomHerd, a forward-looking geometric framework that bypasses this observability lag by quantifying coordination directly on upstream agent-interaction graphs. To generate these graphs, we treat a heterogeneous LLM-driven multi-agent simulator -- each financial trader instantiated by a persona-conditioned LLM call -- as a forecastable world, and evaluate the geometric pipeline on the Cividino--Sornette continuous-spin agent-based substrate as our headline financial testbed. By tracking the discrete Ollivier--Ricci curvature of these action graphs, GeomHerd captures the structural topology of emerging coordination. Theoretically, we establish a mean-field bridge mapping our graph-theoretic metric to CSAD, the classical macroscopic herding statistic, linking GeomHerd to downstream price-dispersion measurement. Empirically, GeomHerd anticipates herding long before aggregate market baselines: on the continuous-spin substrate, our primary detector fires a median of 272 steps before order-parameter onset; a contagion detector ($\beta_{-}$) recalls 65% of critical trajectories 318 steps early; and on co-firing trajectories the agent-graph signal precedes price-correlation-graph baselines by 40 steps. As a complementary indicator, the effective vocabulary of agent actions contracts during cascades. The geometric signature transfers out-of-domain to the Vicsek self-driven-particle model, and a curvature-conditioned forecasting head reduces cascade-window log-return MAE over detector-conditioned and price-only baselines.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes GeomHerd, a geometric framework that constructs agent-interaction graphs from LLM-driven multi-agent financial trader simulations and the Cividino-Sornette continuous-spin substrate, then tracks discrete Ollivier-Ricci curvature to detect emerging herding earlier than price-based methods. It derives a mean-field bridge from the graph metric to the classical CSAD herding statistic, reports a median 272-step lead time before order-parameter onset, 65% recall at 318 steps for a contagion detector, and 40-step precedence over price-correlation baselines on co-firing trajectories. The signature transfers to the Vicsek model, and a curvature-conditioned head improves cascade-window log-return MAE.

Significance. If the simulation faithfully reproduces upstream interaction patterns, the curvature-based early-warning approach could advance coordination detection in multi-agent systems and provide earlier signals than lagged price statistics. The mean-field link to CSAD and successful out-of-domain transfer to the Vicsek model are concrete strengths that ground the method beyond a single substrate. The forecasting improvement further demonstrates practical utility within the simulated setting.

major comments (3)

- [§4] §4 (Experimental Results): All quantitative lead-time claims (median 272 steps, 65% recall at 318 steps, 40-step precedence) are demonstrated exclusively on the Cividino-Sornette continuous-spin substrate and Vicsek model; no experiments on historical market data, order-book logs, or real trader traces are reported, leaving the generalization to actual financial herding untested and load-bearing for the market-fragility motivation stated in the introduction.

- [§3] §3 (Theoretical Mapping): The mean-field bridge from Ollivier-Ricci curvature on action graphs to the macroscopic CSAD statistic is asserted, yet the manuscript provides no explicit derivation, parameter count, or proof that the mapping is free of fitted parameters or substrate-specific assumptions, which is required to confirm the claimed independence from the simulation details.

- [§4.3] §4.3 (Forecasting Head): The reported reduction in cascade-window log-return MAE for the curvature-conditioned forecaster is presented without ablation on the number of trajectories, confidence intervals, or statistical tests against the detector-conditioned and price-only baselines, making it impossible to assess whether the improvement is robust or merely an artifact of the chosen simulation parameters.

minor comments (2)

- [Title and §2] The title references 'Ricci Flow Geometry' while the abstract and methods focus exclusively on discrete Ollivier-Ricci curvature; a brief clarifying sentence in §2 would resolve the apparent mismatch.

- [Figures] Figure captions for curvature time-series plots should explicitly state the number of independent runs, the definition of the shaded bands, and the precise definition of the order-parameter onset threshold used for lead-time measurement.

Simulated Author's Rebuttal

We are grateful to the referee for the insightful comments, which have helped us identify areas for improvement in clarity and rigor. Below we provide point-by-point responses to the major comments.

read point-by-point responses

-

Referee: [§4] §4 (Experimental Results): All quantitative lead-time claims (median 272 steps, 65% recall at 318 steps, 40-step precedence) are demonstrated exclusively on the Cividino-Sornette continuous-spin substrate and Vicsek model; no experiments on historical market data, order-book logs, or real trader traces are reported, leaving the generalization to actual financial herding untested and load-bearing for the market-fragility motivation stated in the introduction.

Authors: We fully acknowledge that our quantitative results are derived from controlled simulations rather than real financial data. The manuscript is positioned as a methodological contribution demonstrating the potential of geometric methods on agent-based models, with the Cividino-Sornette substrate serving as a stylized financial testbed. We agree that claims regarding market applications should be tempered. In the revised manuscript, we will update the introduction to emphasize that the framework is validated in simulation and that empirical validation on historical data is an important direction for future work. This addresses the load-bearing concern by clarifying the scope without overclaiming generalization. revision: partial

-

Referee: [§3] §3 (Theoretical Mapping): The mean-field bridge from Ollivier-Ricci curvature on action graphs to the macroscopic CSAD statistic is asserted, yet the manuscript provides no explicit derivation, parameter count, or proof that the mapping is free of fitted parameters or substrate-specific assumptions, which is required to confirm the claimed independence from the simulation details.

Authors: We regret that the explicit derivation was not included in the main text. The mean-field mapping is obtained by taking the continuum limit of the discrete graph Laplacian induced by the Ollivier-Ricci curvature, which converges to the divergence term in the continuous-spin model; this in turn is proportional to the CSAD measure under mean-field assumptions. The mapping involves no fitted parameters and holds for any substrate where agent actions can be represented as a graph with the same interaction kernel. We will add a dedicated subsection in §3 with the full derivation, including the parameter count (zero free parameters) and a discussion of the assumptions, to make the independence from specific simulation details clear. revision: yes

-

Referee: [§4.3] §4.3 (Forecasting Head): The reported reduction in cascade-window log-return MAE for the curvature-conditioned forecaster is presented without ablation on the number of trajectories, confidence intervals, or statistical tests against the detector-conditioned and price-only baselines, making it impossible to assess whether the improvement is robust or merely an artifact of the chosen simulation parameters.

Authors: We agree that the forecasting experiment requires more statistical support to be convincing. In the revision, we will expand §4.3 to include: (i) ablations varying the number of simulated trajectories (e.g., 100, 250, 500), (ii) bootstrap-derived 95% confidence intervals for the MAE values, and (iii) results of statistical significance tests (paired t-test and Wilcoxon signed-rank test) comparing the curvature-conditioned head against the baselines. These additions will allow readers to evaluate the robustness of the reported improvement. revision: yes

Circularity Check

No significant circularity; derivation remains self-contained.

full rationale

The paper's central theoretical step is a mean-field bridge mapping discrete Ollivier-Ricci curvature on agent graphs to the classical CSAD herding statistic; this is presented as an independent derivation linking graph topology to macroscopic price dispersion rather than a redefinition or fit. Empirical lead-time claims (272-step median, 65% recall, 40-step precedence) are computed directly on the Cividino-Sornette and Vicsek substrates without evidence that any detector parameter is fitted to the target lead times and then relabeled as a prediction. No self-citations, uniqueness theorems, or ansatzes from prior author work are invoked as load-bearing premises in the abstract or described pipeline. The LLM simulator and continuous-spin testbed are treated as generative sources for graphs, not as fitted inputs whose outputs are tautologically recovered. The derivation chain therefore does not reduce to its own inputs by construction.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Ollivier-Ricci curvature on discrete action graphs captures the structural topology of emerging agent coordination

- domain assumption A mean-field approximation maps the graph-theoretic curvature metric to the macroscopic CSAD herding statistic

Lean theorems connected to this paper

-

IndisputableMonolith/Foundation/AlexanderDuality.leanalexander_duality_circle_linking unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

By tracking the discrete Ollivier--Ricci curvature of these action graphs, GeomHerd captures the structural topology of emerging coordination.

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

we establish a mean-field bridge mapping our graph-theoretic metric to CSAD

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

Sushil Bikhchandani, David Hirshleifer, and Ivo Welch. A theory of fads, fashion, custom, and cultural change as informational cascades.Journal of Political Economy, 100(5):992--1026, 1992

work page 1992

-

[2]

Herd behavior in financial markets.IMF Staff Papers, 47(3):279--310, 2001

Sushil Bikhchandani and Sunil Sharma. Herd behavior in financial markets.IMF Staff Papers, 47(3):279--310, 2001

work page 2001

-

[3]

A simple model of herd behavior.The Quarterly Journal of Economics, 107(3):797--817, 1992

Abhijit V Banerjee. A simple model of herd behavior.The Quarterly Journal of Economics, 107(3):797--817, 1992

work page 1992

-

[4]

Christopher Avery and Peter Zemsky. Multidimensional uncertainty and herd behavior in financial markets.American Economic Review, 88(4):724--748, 1998

work page 1998

-

[5]

David S. Scharfstein and Jeremy C. Stein. Herd behavior and investment.American Economic Review, 80(3):465--479, 1990

work page 1990

-

[6]

William G. Christie and Roger D. Huang. Following the pied piper: Do individual returns herd around the market?Financial Analysts Journal, 51(4):31--37, 1995

work page 1995

-

[7]

Eric C. Chang, Joseph W. Cheng, and Ajay Khorana. An examination of herd behavior in equity markets: An international perspective.Journal of Banking & Finance, 24(10):1651-- 1679, 2000

work page 2000

-

[8]

Market stress and herding.Journal of Empirical Finance, 11(4):585--616, 2004

Soosung Hwang and Mark Salmon. Market stress and herding.Journal of Empirical Finance, 11(4):585--616, 2004

work page 2004

-

[9]

Josef Lakonishok, Andrei Shleifer, and Robert W. Vishny. The impact of institutional trading on stock prices.Journal of Financial Economics, 32(1):23--43, 1992. 10

work page 1992

-

[10]

Richard W. Sias. Institutional herding.Review of Financial Studies, 17(1):165--206, 2004

work page 2004

-

[11]

Romeil S. Sandhu, Tryphon T. Georgiou, and Allen R. Tannenbaum. Ricci curvature: An economic indicator for market fragility and systemic risk.Science Advances, 2(5):e1501495, 2016

work page 2016

-

[12]

Pharasi, Sarath Jyotsna Ramaia, Harish Kannan, Emil Saucan, Jür- gen Jost, and Anirban Chakraborti

Areejit Samal, Hirdesh K. Pharasi, Sarath Jyotsna Ramaia, Harish Kannan, Emil Saucan, Jür- gen Jost, and Anirban Chakraborti. Network geometry and market instability.Royal Society Open Science, 8(2):201734, 2021

work page 2021

-

[13]

Xinyu Wang, Liang Zhao, Ning Zhang, Liu Feng, and Haibo Lin. Stability of China’s stock market: Measure and forecast by Ricci curvature on network.arXiv preprint arXiv:2204.06692, 2022

-

[14]

Joaquín Sánchez García and Sebastian Gherghe. On the Ollivier-Ricci curvature as fragility indicator of the stock markets.arXiv preprint arXiv:2405.07134, 2024

-

[15]

Intrinsic geometry of the stock market from graph ricci flow.arXiv preprint arXiv:2510.15942, 2026

Bhargavi Srinivasan. Intrinsic geometry of the stock market from graph ricci flow.arXiv preprint arXiv:2510.15942, 2026

-

[16]

Ömer Akgüller, Mehmet Ali Balcı, Larissa M. Batrancea, and Lucian Gaban. Network geom- etry of Borsa Istanbul: Analyzing sectoral dynamics with Forman--Ricci curvature.Entropy, 27(3):271, 2025

work page 2025

-

[17]

Financial contagion.Journal of Political Economy, 108(1):1- -33, 2000

Franklin Allen and Douglas Gale. Financial contagion.Journal of Political Economy, 108(1):1- -33, 2000

work page 2000

-

[18]

Systemic risk and stability in financial networks.American Economic Review, 105(2):564--608, 2015

Daron Acemoglu, Asuman Ozdaglar, and Alireza Tahbaz-Salehi. Systemic risk and stability in financial networks.American Economic Review, 105(2):564--608, 2015

work page 2015

-

[19]

Matthew Elliott, Benjamin Golub, and Matthew O. Jackson. Financial networks and contagion. American Economic Review, 104(10):3115--3153, 2014

work page 2014

-

[20]

Brunnermeier and Lasse Heje Pedersen

Markus K. Brunnermeier and Lasse Heje Pedersen. Market liquidity and funding liquidity. Review of Financial Studies, 22(6):2201--2238, 2009

work page 2009

-

[21]

Twinmarket: A scalable behavioral and socialsimulation for financial markets,

Yuzhe Yang, Yifei Zhang, Minghao Wu, Kaidi Zhang, Yunmiao Zhang, Honghai Yu, Yan Hu, and Benyou Wang. TwinMarket: A scalable behavioral and social simulation for fi- nancial markets. InAdvances in Neural Information Processing Systems (NeurIPS), 2025. arXiv:2502.01506

-

[22]

Agent-based simulation of a financial market with large language models

Ryuji Hashimoto, Takehiro Takayanagi, Masahiro Suzuki, and Kiyoshi Izumi. Agent-based simulation of a financial market with large language models. InInternational Conference on Principles and Practice of Multi-Agent Systems, pages 20--28. Springer, 2025

work page 2025

-

[23]

Mass: Muli-agent simulation scaling for portfolio construction.arXiv preprint arXiv:2505.10278, 2025

Taian Guo, Haiyang Shen, Jinsheng Huang, Zhengyang Mao, Junyu Luo, Binqi Chen, Zhuoru Chen, Luchen Liu, Bingyu Xia, Xuhui Liu, Yun Ma, and Ming Zhang. Mass: Muli-agent simulation scaling for portfolio construction.arXiv preprint arXiv:2505.10278, 2025

-

[24]

Yangyang Yu, Zhiyuan Yao, Haohang Li, Zhiyang Deng, Yuechen Jiang, Yupeng Cao, Zhi Chen, Jordan W Suchow, Zhenyu Cui, Rong Liu, et al. Fincon: A synthesized llm multi- agent system with conceptual verbal reinforcement for enhanced financial decision making. Advances in Neural Information Processing Systems, 37:137010--137045, 2024

work page 2024

-

[25]

Davide Cividino, Rebecca Westphal, and Didier Sornette. Multiasset financial bubbles in an agent-based model with noise traders’ herding described by ann-vector Ising model.Physical Review Research, 5(1):013009, 2023

work page 2023

-

[26]

Tamás Vicsek, András Czirók, Eshel Ben-Jacob, Inon Cohen, and Ofer Shochet. Novel type of phase transition in a system of self-driven particles.Physical Review Letters, 75(6):1226-- 1229, 1995

work page 1995

-

[27]

Rémi Flamary, Nicolas Courty, Alexandre Gramfort, Mokhtar Z. Alaya, Aurélie Boisbunon, Stanislas Chambon, Laetitia Chapel, Adrien Corenflos, Kilian Fatras, Nemo Fournier, et al. POT: Python optimal transport.Journal of Machine Learning Research, 22(78):1--8, 2021. 11

work page 2021

-

[28]

Jayson Sia, Edmond Jonckheere, and Paul Bogdan. Ollivier-Ricci curvature-based method to community detection in complex networks.Scientific Reports, 9:9800, 2019

work page 2019

-

[29]

Community detection on networks with Ricci flow.Scientific Reports, 9:9984, 2019

Chien-Chun Ni, Yu-Yao Lin, Feng Luo, and Jie Gao. Community detection on networks with Ricci flow.Scientific Reports, 9:9984, 2019

work page 2019

-

[30]

Hao Jiang, Min Zhao, Zhicheng Zhang, and Tianyi Luo. Evaluating financial contagion through Ricci curvature on multivariate reactive point processes.Finance Research Letters, 58, Part A:104248, 2023

work page 2023

-

[31]

E. S. Page. Continuous inspection schemes.Biometrika, 41(1/2):100--115, 1954

work page 1954

-

[32]

Brock, Victor Brovkin, Stephen R

Marten Scheffer, Jordi Bascompte, William A. Brock, Victor Brovkin, Stephen R. Carpenter, Vasilis Dakos, Hermann Held, Egbert H. van Nes, Max Rietkerk, and George Sugihara. Early- warning signals for critical transitions.Nature, 461:53--59, 2009

work page 2009

-

[33]

Finite scalar quantization: VQ-VAE made simple

Fabian Mentzer, David Minnen, Eirikur Agustsson, and Michael Tschannen. Finite scalar quantization: VQ-VAE made simple. InInternational Conference on Learning Representa- tions (ICLR), 2024

work page 2024

-

[34]

Mutual fund herding and the impact on stock prices.Journal of Finance, 54(2):581--622, 1999

Russ Wermers. Mutual fund herding and the impact on stock prices.Journal of Finance, 54(2):581--622, 1999

work page 1999

-

[35]

Rama Cont. Empirical properties of asset returns: stylized facts and statistical issues.Quanti- tative Finance, 1(2):223--236, 2001

work page 2001

-

[36]

Chuangxia Huang, Yaqian Cai, Xiaoguang Yang, Yanchen Deng, and Xin Yang. Laplacian- energy-like measure: Does it improve the Cross-Sectional Absolute Deviation herding model? Economic Modelling, 127:106505, 2023

work page 2023

-

[37]

Probing Dec-POMDP reasoning in cooperative MARL

Kale-ab Tessera, Leonard Hinckeldey, Riccardo Zamboni, David Abel, and Amos Storkey. Probing Dec-POMDP reasoning in cooperative MARL. InProceedings of the 25th In- ternational Conference on Autonomous Agents and Multiagent Systems (AAMAS), 2026. arXiv:2602.20804

-

[38]

Ecaterina Guritanu, Enrico Barbierato, and Alice Gatti. Topological machine learning for financial crisis detection: Early warning signals from persistent homology.Computers, 14(10):408, 2025

work page 2025

-

[39]

Thomas M. Bury, R. I. Sujith, Induja Pavithran, Marten Scheffer, Timothy M. Lenton, Mad- hur Anand, and Chris T. Bauch. Deep learning for early warning signals of tipping points. Proceedings of the National Academy of Sciences, 118(39):e2106140118, 2021

work page 2021

-

[40]

Sotirios D. Nikolopoulos. An imbalance-robust evaluation framework for extreme risk fore- casts.arXiv preprint arXiv:2512.00916, 2025

-

[41]

Rishabh Agarwal, Max Schwarzer, Pablo Samuel Castro, Aaron C. Courville, and Marc G. Bellemare. Deep reinforcement learning at the edge of the statistical precipice. InAdvances in Neural Information Processing Systems, volume 34, pages 29304--29320, 2021

work page 2021

-

[42]

Stefan Frey, Patrick Herbst, and Andreas Walter. Measuring mutual fund herding --- a struc- tural approach.Journal of International Financial Markets, Institutions and Money, 32:219-- 239, 2014. Original working paper 2007

work page 2014

-

[43]

Yann Ollivier. Ricci curvature of Markov chains on metric spaces.Journal of Functional Analysis, 256(3):810--864, 2009

work page 2009

-

[44]

Predicting discrete-time bifurcations with deep learning.Nature Communica- tions, 14(1):6331, 2023

Thomas M Bury, Daniel Dylewsky, Chris T Bauch, Madhur Anand, Leon Glass, Alvin Shrier, and Gil Bub. Predicting discrete-time bifurcations with deep learning.Nature Communica- tions, 14(1):6331, 2023. A Related Work (Extended) This appendix gives the full version of the related-work review summarised in §4. 12 Classical herding measurement.The herding-meas...

work page 2023

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.