AI Premium

Pith reviewed 2026-06-30 03:11 UTC · model grok-4.3

The pith

Firms whose stock returns covary positively with AI consumption growth earn higher future returns, with a value-weighted long-short strategy delivering 64.1 basis points per week.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Using the unprecedented granularity of proprietary AI consumption data, the paper constructs a high-frequency AI factor from aggregate token, dollar, and user growth across hundreds of models. Firms with higher comovement to this factor earn higher subsequent returns, and a value-weighted long-short strategy based on AI betas earns 64.1 basis points per week. The premium is large for loadings on the intensive, frontier-oriented margin of AI consumption but absent for casual or open-weight use; it reaches beyond technology firms into consumer-facing and capital-heavy parts of the economy yet is absent in emerging markets including China; and AI exposure is more positive for nonroutine interac

What carries the argument

The AI factor, built from realized growth in tokens, dollars, and users across large language models, which isolates firm-level exposure through comovement in stock returns.

If this is right

- High AI-beta firms earn higher subsequent stock returns on average.

- The premium is concentrated on intensive, frontier AI consumption margins such as closed-source models and long prompts.

- AI exposure and its associated premium extend into non-technology sectors including consumer-facing and capital-heavy industries.

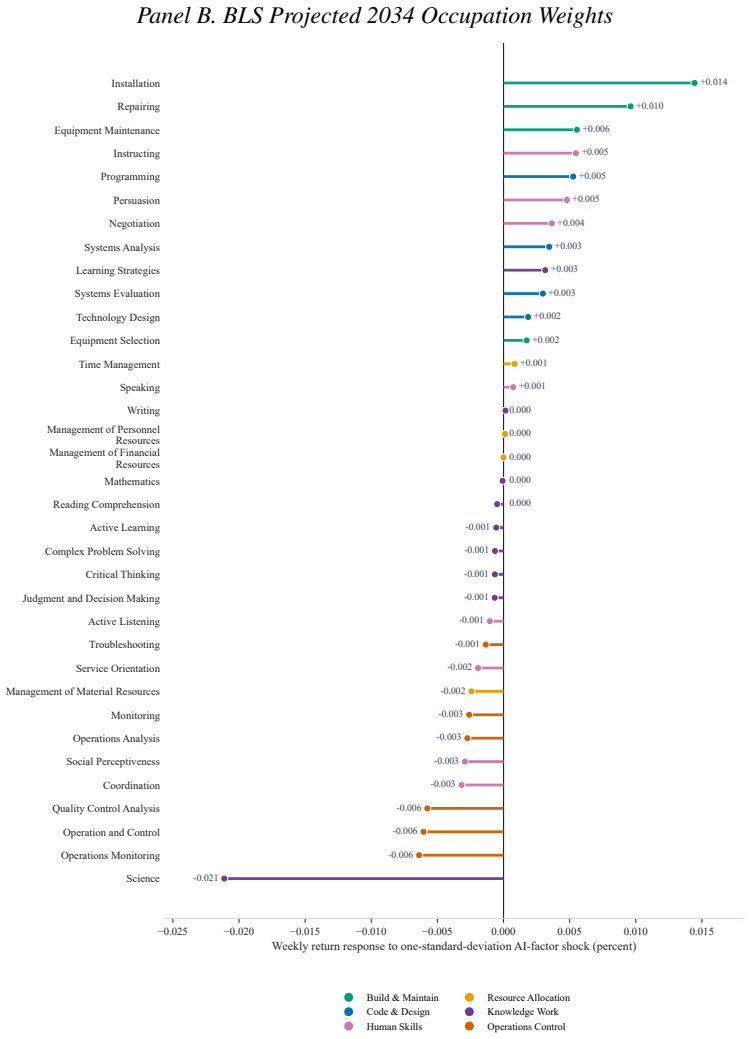

- Occupations with higher interaction-and-communication content carry a larger market-implied AI premium.

- The premium is absent in emerging markets including China.

Where Pith is reading between the lines

- Portfolio managers could construct tilts toward high AI-beta stocks using consumption-based betas rather than text-based measures.

- Wage and hiring differentials may emerge across occupations as markets price AI exposure differently by skill type.

- If consumption data continue to expand, the same factor construction could track how the premium evolves with broader agentic AI adoption.

Load-bearing premise

The AI factor constructed from aggregate token, dollar, and user growth isolates AI-specific exposure rather than capturing correlated movements from other economic or technological trends.

What would settle it

A hold-out test showing that the value-weighted long-short portfolio sorted on AI betas produces zero or negative returns after standard risk-factor controls would falsify the existence of a distinct AI premium.

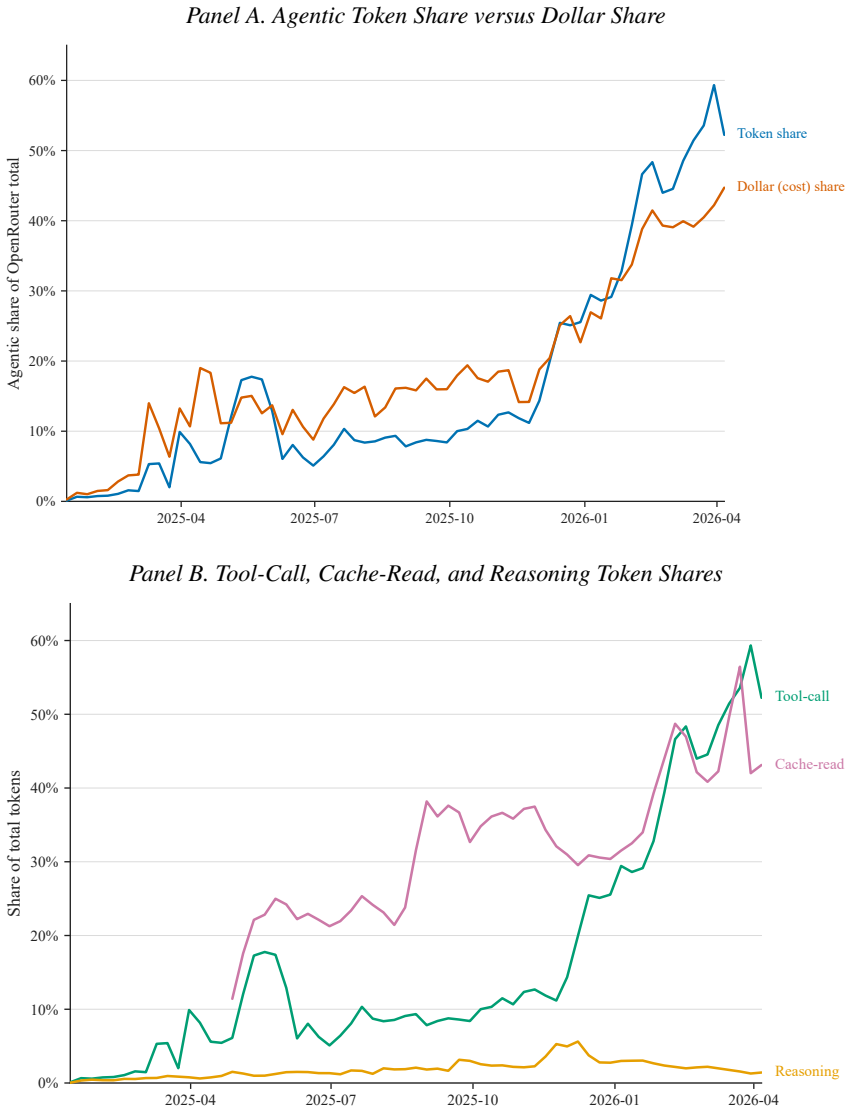

Figures

read the original abstract

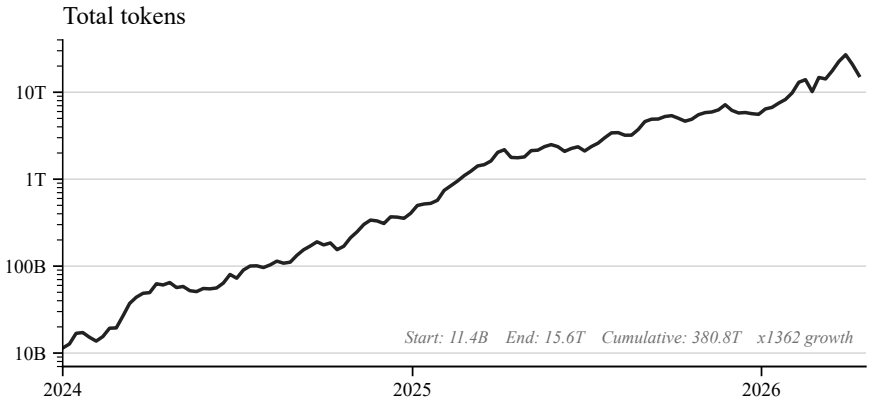

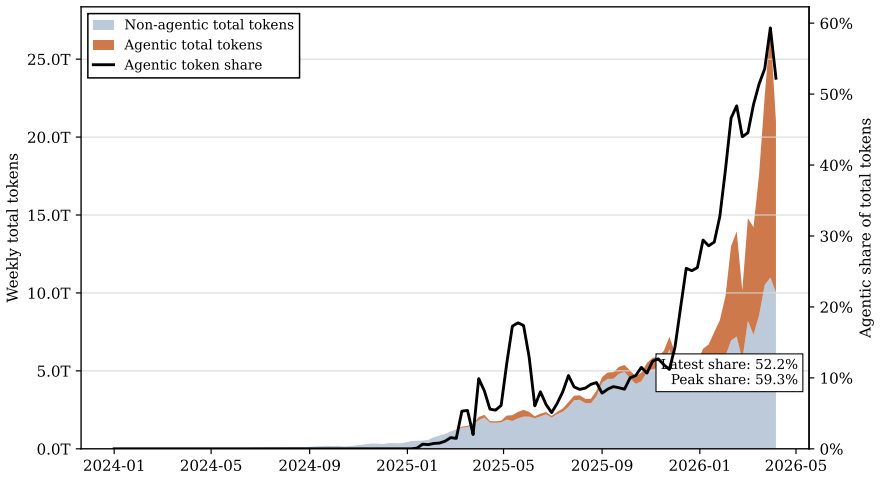

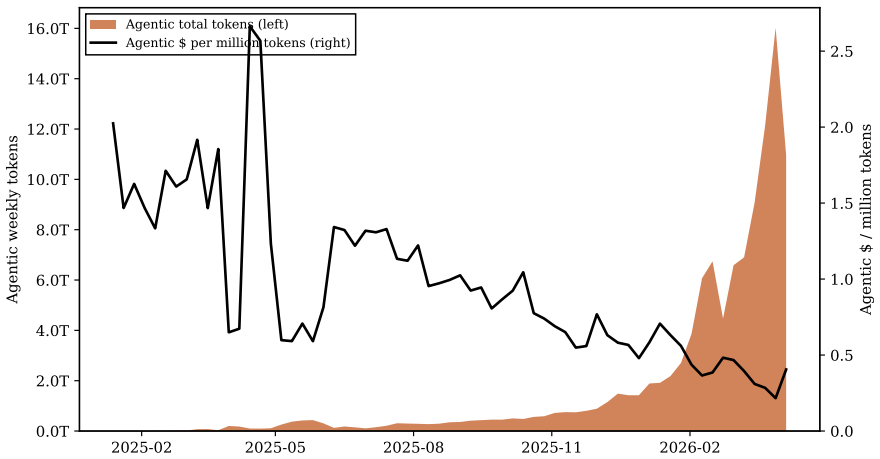

Using 380 trillion tokens of realized AI consumption across more than four hundred large language models from the licensed proprietary OpenRouter dataset covering approximately 2 percent of current global monthly AI token consumption, we analyze how AI affects firms, markets, and workers. Leveraging the unprecedented size, scope and granularity data, we construct the AI Factor from growth in tokens, dollars, and users, estimate firm-level AI Betas from stock return comovement, and characterize the \emph{AI Premium}. First, we build a high-frequency AI factor and decompose it into salient components. Second, we show that firms whose returns covary more positively with the AI factor -- high AI beta firms -- earn higher subsequent returns, and the AI premium is large and heterogeneous. A value-weighted long-short strategy earns 64.1 basis points per week, and the premium is large for loadings on the intensive, frontier-oriented margin of AI consumption -- closed-source models, paying and seasoned users, and long prompts -- but not on casual or open-weight use. Third, the premium reaches beyond technology firms into consumer-facing and capital-heavy parts of the economy, but is absent in emerging markets, including China. Fourth, the AI exposure is more positive in nonroutine interactive work and more negative in analytical, scientific, and operations-control skills -- an occupation one standard deviation higher in interaction-and-communication content has 0.36-standard-deviation higher market-implied AI exposure. Additionally, we provide early evidence of the rise of the agentic economy.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper constructs an AI factor from growth rates in tokens, dollars, and users using 380 trillion tokens of consumption data across >400 LLMs from the OpenRouter dataset. It estimates firm-level AI betas via stock-return comovement with this factor and documents an AI premium: high-beta firms earn higher subsequent returns, with a value-weighted long-short portfolio returning 64.1 bp per week. The premium is heterogeneous (stronger on frontier/closed-source/intensive margins, present outside pure tech sectors but absent in emerging markets) and correlates with occupation-level interaction skills.

Significance. If the AI factor isolates AI-specific exposure, the scale and granularity of the consumption data would represent a substantial advance for asset-pricing and labor-market studies of technological adoption. The out-of-sample return predictability, cross-sectional heterogeneity, and occupation-level patterns would provide falsifiable, economically large evidence on how realized AI use affects firm valuations and skill premia.

major comments (3)

- [Factor Construction] Factor-construction section: the AI factor is formed directly from aggregate token/dollar/user growth without reported orthogonalization to market returns, industry portfolios, or other innovation proxies (e.g., R&D intensity or patent-based factors). Because the central claim is that the 64.1 bp premium reflects AI-specific comovement rather than correlated tech or macro trends, this omission is load-bearing for interpretation.

- [Portfolio Sorts and Returns] Portfolio-formation and return section: the value-weighted long-short results on AI betas do not report alphas after controlling for Fama-French-Carhart factors or industry fixed effects in either beta estimation or portfolio returns. Without these controls, it remains unclear whether the premium is incremental to known risk factors.

- [Heterogeneity Analysis] Heterogeneity tests: while the paper distinguishes closed-source vs. open-weight margins, it does not test whether the factor loadings remain significant after including interactions with existing technology or innovation factors; this test is needed to confirm that the reported heterogeneity isolates AI-specific exposure.

minor comments (2)

- [Data and Factor Construction] Abstract and data section: state the precise sample period, rebalancing frequency of the factor, and any winsorization or standardization applied to the growth rates used in factor construction.

- [Results Tables] Table/figure captions: ensure all reported returns include t-statistics or standard errors and clarify whether the 64.1 bp figure is raw or risk-adjusted.

Simulated Author's Rebuttal

We thank the referee for the detailed and constructive comments. The suggestions for additional robustness checks on factor construction, portfolio returns, and heterogeneity tests will improve the clarity of our results. We address each major comment below and commit to incorporating the requested analyses in the revision.

read point-by-point responses

-

Referee: [Factor Construction] Factor-construction section: the AI factor is formed directly from aggregate token/dollar/user growth without reported orthogonalization to market returns, industry portfolios, or other innovation proxies (e.g., R&D intensity or patent-based factors). Because the central claim is that the 64.1 bp premium reflects AI-specific comovement rather than correlated tech or macro trends, this omission is load-bearing for interpretation.

Authors: We agree that showing the AI factor captures incremental variation is central. The factor is built from consumption growth (tokens, dollars, users), which is independent of returns by construction. In revision we will (i) report pairwise correlations of the AI factor with the market, Fama-French factors, and available innovation proxies, and (ii) produce an orthogonalized AI factor by regressing the raw factor on the market and Fama-French factors and re-estimate all betas and premiums with the residual series. These steps will directly address whether the documented premium reflects AI-specific exposure. revision: yes

-

Referee: [Portfolio Sorts and Returns] Portfolio-formation and return section: the value-weighted long-short results on AI betas do not report alphas after controlling for Fama-French-Carhart factors or industry fixed effects in either beta estimation or portfolio returns. Without these controls, it remains unclear whether the premium is incremental to known risk factors.

Authors: We will add the requested controls. In the revised manuscript we will report alphas from time-series regressions of the value-weighted long-short portfolio on the Fama-French-Carhart factors. We will also re-estimate firm-level AI betas after including industry fixed effects and repeat the portfolio sorts with industry-adjusted betas. These additions will demonstrate whether the 64.1 bp premium survives standard risk-factor and industry adjustments. revision: yes

-

Referee: [Heterogeneity Analysis] Heterogeneity tests: while the paper distinguishes closed-source vs. open-weight margins, it does not test whether the factor loadings remain significant after including interactions with existing technology or innovation factors; this test is needed to confirm that the reported heterogeneity isolates AI-specific exposure.

Authors: We will extend the heterogeneity analysis by adding interactions between AI betas and existing technology/innovation measures (R&D intensity and patent-based factors) in the cross-sectional return regressions. This will test whether the differential premia on closed-source versus open-weight margins, and on intensive versus casual use, remain significant after these interactions. The results will clarify whether the heterogeneity is incremental to broader tech exposure. revision: yes

Circularity Check

No circularity in AI factor construction or premium measurement

full rationale

The derivation chain uses an AI factor built directly from independent external consumption data (aggregate token, dollar, and user growth in the OpenRouter dataset), estimates firm betas via return comovement with that factor, and measures the premium via actual subsequent returns on a value-weighted long-short portfolio sorted on those betas. This is a standard empirical asset-pricing test that does not reduce any result to its inputs by construction, nor does it rely on self-citations, fitted parameters renamed as predictions, or imported uniqueness theorems. The central claim remains falsifiable against external return data and is not self-definitional.

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.