Recommendation Engine for Lower Interest Borrowing on Peer to Peer Lending (P2PL) Platform

Pith reviewed 2026-05-24 19:02 UTC · model grok-4.3

The pith

A recommendation system advises P2PL borrowers on loan type to achieve lower interest rates and higher funding likelihood.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The central claim is that a model trained on historical loan outcomes by borrower grade and loan type can recommend the appropriate loan mechanism for any new borrower, enabling lower interest rates and a higher likelihood of the loan being funded.

What carries the argument

A recommendation model that classifies or predicts the better loan type (bidding versus traditional) for each borrower grade based on past interest rate and funding success data.

If this is right

- Any borrower following the recommendation pays a lower interest rate than they otherwise would.

- Recommended loans have a higher probability of being funded by lenders.

- The system applies to borrowers with no previous activity on the platform.

- Outcomes differ systematically by borrower grade across the two loan types.

Where Pith is reading between the lines

- Such a system could be integrated into P2PL platforms to automatically suggest loan types at application time.

- If market conditions change, retraining on recent data would be necessary to maintain accuracy.

- Extending the model to incorporate additional borrower features beyond grade might further improve recommendations.

Load-bearing premise

Past loan data grouped by borrower grade and type can reliably predict which choice will give better results for future borrowers.

What would settle it

Apply the trained model to a set of new loan applications, have borrowers follow or not follow the recommendation, and compare actual interest rates achieved and funding rates between the two groups.

Figures

read the original abstract

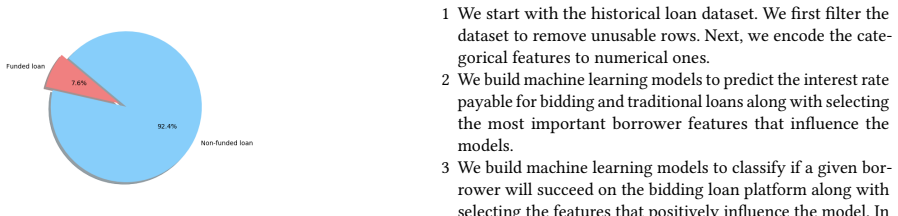

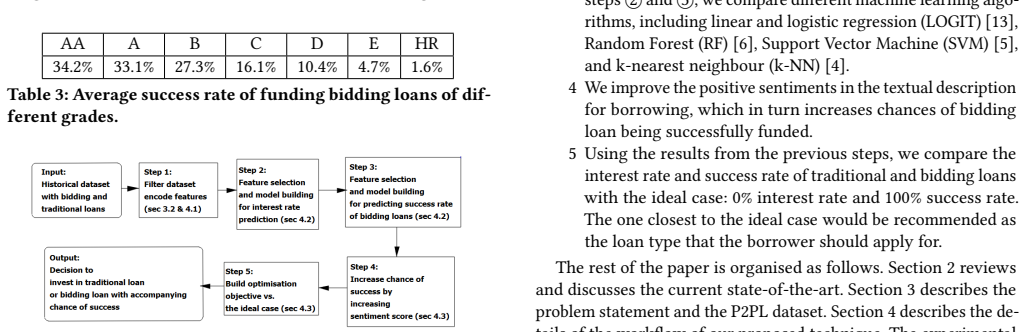

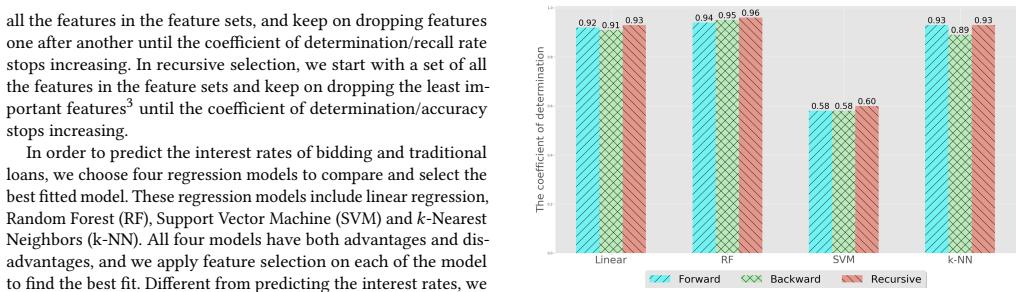

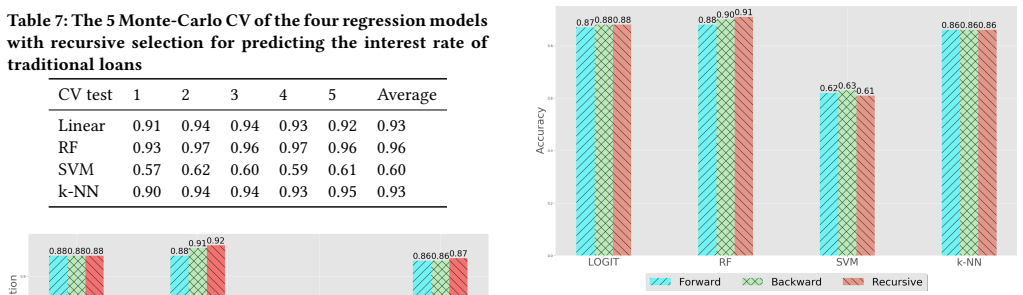

Online Peer to Peer Lending (P2PL) systems connect lenders and borrowers directly, thereby making it convenient to borrow and lend money without intermediaries such as banks. Many recommendation systems have been developed for lenders to achieve higher interest rates and avoid defaulting loans. However, there has not been much research in developing recommendation systems to help borrowers make wise decisions. On P2PL platforms, borrowers can either apply for bidding loans, where the interest rate is determined by lenders bidding on a loan or traditional loans where the P2PL platform determines the interest rate. Different borrower grades -- determining the credit worthiness of borrowers get different interest rates via these two mechanisms. Hence, it is essential to determine which type of loans borrowers should apply for. In this paper, we build a recommendation system that recommends to any new borrower the type of loan they should apply for. Using our recommendation system, any borrower can achieve lowered interest rates with a higher likelihood of getting funded.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes a recommendation system for borrowers on peer-to-peer lending (P2PL) platforms that advises whether to apply for bidding loans (where rates are set by lender bids) or traditional loans (where the platform sets the rate), with the goal of achieving lower interest rates and higher funding probability for any new borrower based on their grade.

Significance. A validated system of this type could have practical value for borrowers in P2PL markets by improving loan outcomes. However, the manuscript supplies no data description, model, training procedure, validation strategy, or quantitative results, so the claimed generalization from historical grade-and-type outcomes to new borrowers cannot be assessed and the significance remains unevaluable.

major comments (2)

- [Abstract] Abstract: the central claim that 'any borrower can achieve lowered interest rates with a higher likelihood of getting funded' is stated without any supporting description of the dataset, borrower features, recommendation algorithm, loss function, hold-out validation, or performance comparison between bidding and traditional loans.

- The manuscript contains no equations, tables, or sections detailing the model or empirical results, so the key assumption that historical loan outcomes by grade and type generalize to new borrowers without material distribution shift or selection bias cannot be checked.

Simulated Author's Rebuttal

We thank the referee for the report. The comments correctly identify that the submitted manuscript lacks the technical details needed to evaluate the recommendation system and its claims. We will revise the paper to supply these elements.

read point-by-point responses

-

Referee: [Abstract] Abstract: the central claim that 'any borrower can achieve lowered interest rates with a higher likelihood of getting funded' is stated without any supporting description of the dataset, borrower features, recommendation algorithm, loss function, hold-out validation, or performance comparison between bidding and traditional loans.

Authors: We agree the abstract and manuscript provide no such details. The initial version presented only the high-level motivation. In revision we will expand the abstract and add a methods section describing the P2PL dataset (borrower grades and historical outcomes for bidding vs. traditional loans), the features used, the recommendation procedure (comparison of per-grade historical interest rates and funding rates), any optimization criterion, the hold-out validation, and quantitative results comparing the two loan types. revision: yes

-

Referee: The manuscript contains no equations, tables, or sections detailing the model or empirical results, so the key assumption that historical loan outcomes by grade and type generalize to new borrowers without material distribution shift or selection bias cannot be checked.

Authors: We accept the point. The current text contains none of these elements. Revision will add equations formalizing the recommendation rule, tables of empirical rates and success probabilities by grade and loan type, and a validation section that applies the rule to held-out historical data while discussing potential shifts or biases. revision: yes

Circularity Check

No derivation chain or equations present; claim is unevaluable but not circular

full rationale

The manuscript presents only a high-level problem statement and a claim that a recommendation system was built to advise borrowers on loan type for lower interest and higher funding probability. No algorithms, feature sets, training procedures, loss functions, equations, validation strategies, or self-citations are supplied in the text. Without any derivation steps, fitted parameters, or load-bearing citations to inspect, no circularity of the enumerated kinds can be identified or quoted. The paper is self-contained only in the trivial sense that it contains no chain at all.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Historical loan records by borrower grade contain stable, generalizable signals for optimal loan-type choice.

Reference graph

Works this paper leans on

-

[1]

Tim Althoff, Cristian Danescu-Niculescu-Mizil, and Dan Jurafsky. 2014. How to ask for a favor: A case study on the success of altruistic requests. In Eighth International AAAI Conference on Weblogs and Social Media

work page 2014

-

[2]

Nataliya Barasinska and Dorothea Schäfer. 2014. Is crowdfunding different? Evidence on the relation between gender and funding success from a German peer-to-peer lending platform. German Economic Review 15, 4 (2014), 436–452

work page 2014

-

[3]

Simla Ceyhan, Xiaolin Shi, and Jure Leskovec. 2011. Dynamics of bidding in a P2P lending service: effects of herding and predicting loan success. InProceedings of the 20th international conference on World wide web . ACM, 547–556

work page 2011

-

[4]

Samprit Chatterjee and Seymour Barcun. 1970. A nonparametric approach to credit screening. Journal of the American statistical Association 65, 329 (1970), 150–154

work page 1970

-

[5]

Harris Drucker, Christopher JC Burges, Linda Kaufman, Alex J Smola, and Vladimir Vapnik. 1997. Support vector regression machines. In Advances in neural information processing systems . 155–161

work page 1997

-

[6]

David Feldman and Shulamith Gross. 2005. Mortgage default: classification trees analysis. The Journal of Real Estate Finance and Economics 30, 4 (2005), 369–396

work page 2005

-

[7]

Yanhong Guo, Wenjun Zhou, Chunyu Luo, Chuanren Liu, and Hui Xiong. 2016. Instance-based credit risk assessment for investment decisions in P2P lending. European Journal of Operational Research 249, 2 (2016), 417 – 426. https://doi. org/10.1016/j.ejor.2015.05.050

-

[8]

Michal Herzenstein, Rick L Andrews, Utpal M Dholakia, and Evgeny Lyandres

-

[9]

Boston University School of Management Research Paper 14, 6 (2008), 1–36

The democratization of personal consumer loans? Determinants of suc- cess in online peer-to-peer lending communities. Boston University School of Management Research Paper 14, 6 (2008), 1–36

work page 2008

-

[10]

Michal Herzenstein, Utpal M Dholakia, and Rick L Andrews. 2011. Strategic herding behavior in peer-to-peer loan auctions. Journal of Interactive Marketing 25, 1 (2011), 27–36

work page 2011

-

[11]

Michal Herzenstein, Scott Sonenshein, and Utpal M Dholakia. 2011. Tell me a good story and I may lend you money: The role of narratives in peer-to-peer lending decisions. Journal of Marketing Research 48, SPL (2011), S138–S149

work page 2011

-

[12]

Clayton J Hutto and Eric Gilbert. 2014. Vader: A parsimonious rule-based model for sentiment analysis of social media text. InEighth international AAAI conference on weblogs and social media

work page 2014

-

[13]

Milad Malekipirbazari and Vural Aksakalli. 2015. Risk assessment in social lending via random forests. Expert Systems with Applications 42, 10 (2015), 4621–

work page 2015

-

[14]

https://doi.org/10.1016/j.eswa.2015.02.001

-

[15]

John Neter, Michael H Kutner, Christopher J Nachtsheim, and William Wasser- man. 1996. Applied linear statistical models. Vol. 4. Irwin Chicago

work page 1996

-

[16]

Prosper. 2018. Prosper Marketplace. https://www.prosper.com/invest. last accessed - 7/4/2019

work page 2018

-

[17]

Ke Ren and Avinash Malik. 2019. Investment Recommendation System for Low- Liquidity Online Peer to Peer Lending (P2PL) Marketplaces. In Proceedings of the Twelfth ACM International Conference on Web Search and Data Mining . ACM, 510–518

work page 2019

-

[18]

Joe Ryan, Katya Reuk, and Charles Wang. 2007. To fund or not to fund: Deter- minants of loan fundability in the prosper. com marketplace. WP, The Standord Graduate School of Business (2007)

work page 2007

-

[19]

Joash Xu. 2015. Prosper Loan Data. https://github.com/joashxu/prosper-loan- data. last accessed - 15/9/2016

work page 2015

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.