The Privacy Subsidy: Kyle's λ under Noise-Perturbed Order-Flow Observation

Pith reviewed 2026-05-20 16:39 UTC · model grok-4.3

The pith

Derives closed-form linear Kyle equilibrium under Gaussian privacy noise on order flow observation, with rescaled price-impact coefficient and informed-trader strategy but invariant product, plus welfare decomposition giving the privacy subsidy as break-even fee for privacy-aggregated exchanges.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

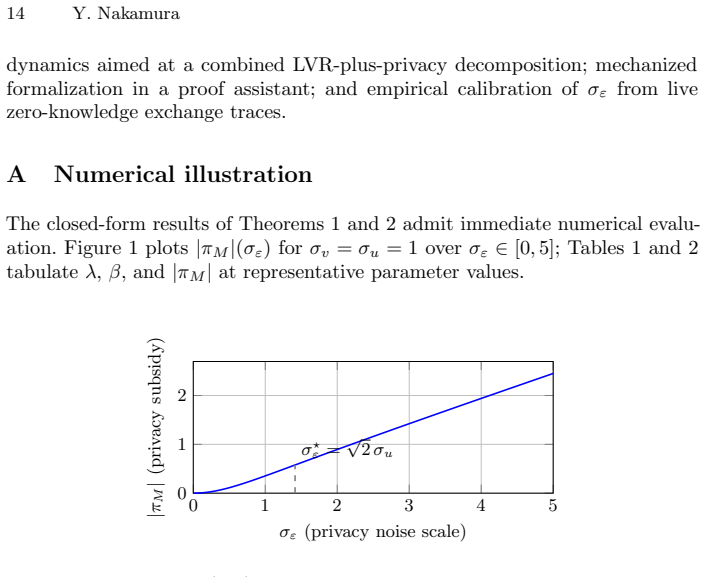

We derive the unique linear Kyle equilibrium when a committed Bayesian market maker observes order flow perturbed by independent Gaussian privacy noise. The price-impact coefficient and informed-trader strategy both rescale by a single factor in the privacy parameter, and their product is invariant. A welfare decomposition then identifies a closed-form per-period transfer from the protocol's LP pool to traders -- the 'privacy subsidy'.

Load-bearing premise

The equilibrium is linear, the market maker is committed and Bayesian, and the privacy perturbation is independent Gaussian noise; these modeling choices are required to obtain the claimed closed-form rescaling and invariant product.

Figures

read the original abstract

Privacy-preserving cryptocurrency exchanges (shielded AMMs, batched swap auctions, sealed-bid order-flow auctions) alter what the pricing mechanism observes about order flow. We derive the unique linear Kyle equilibrium when a committed Bayesian market maker observes order flow perturbed by independent Gaussian privacy noise. The price-impact coefficient and informed-trader strategy both rescale by a single factor in the privacy parameter, and their product is invariant. A welfare decomposition then identifies a closed-form per-period transfer from the protocol's LP pool to traders -- the "privacy subsidy", the break-even fee any privacy-aggregated exchange must charge. The result is the single-period closed-form privacy-noise analog of Loss-Versus-Rebalancing (Milionis et al. 2022). The primary application is shielded AMMs with explicit additive-noise injection (e.g., differential privacy); related designs (batched swaps, sealed-bid auctions, oracle-pegged crossings) require separate frameworks that we leave to future work.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript derives the unique linear Kyle equilibrium when a committed Bayesian market maker observes order flow y = x + u + ε with ε ~ N(0, σ_ε²) independent of (v, u). The equilibrium price-impact coefficient λ and informed-trader intensity β both rescale by the single factor σ_total / σ_u (where σ_total = sqrt(σ_u² + σ_ε²)), their product λβ remains invariant at 1/4, and a welfare decomposition identifies the closed-form per-period privacy subsidy as the expected transfer -E[(v - p)ε] from the LP pool to traders. The result is positioned as the single-period privacy-noise analog of Loss-Versus-Rebalancing.

Significance. If the derivation holds, the paper supplies a parameter-free closed-form extension of the classic Kyle model to additive privacy noise on order flow. The exact rescaling rule, the invariance of the product λβ, and the explicit Gaussian-moment expression for the privacy subsidy provide a direct benchmark for break-even fees in shielded AMMs and related privacy-preserving mechanisms. The work is grounded in standard joint-normality assumptions, delivers falsifiable predictions without new free parameters, and mirrors the structure of the LVR literature.

minor comments (3)

- [Abstract] Abstract: the main claims are stated clearly but without any displayed equations for the rescaling factor or the privacy-subsidy expression; adding the key formulas (e.g., λ' = σ_v / (2 σ_total) and the subsidy -E[(v-p)ε]) would improve immediate accessibility.

- [Introduction] The baseline Kyle (1985) reference should be cited explicitly in the introduction and equilibrium section when the standard formulas are invoked before the noise perturbation is introduced.

- [§3] Notation for the privacy-noise variance should be introduced once and used consistently when defining σ_total and when evaluating the joint-Gaussian moments for the subsidy.

Simulated Author's Rebuttal

We thank the referee for the supportive summary, significance assessment, and recommendation of minor revision. The manuscript's positioning as a single-period privacy-noise analog of LVR is accurately captured, and we appreciate the recognition of the closed-form rescaling rule and invariant product λβ.

Circularity Check

No significant circularity; derivation is a direct extension of standard Kyle model

full rationale

The paper starts from the classic one-period Kyle setup with joint normality of (v, u) and replaces the market maker's observation with y = x + u + ε where ε ~ N(0, σ_ε²) is independent. The linear equilibrium is obtained by solving the informed trader's optimization and the market maker's Bayesian pricing rule under the modified signal; this produces the explicit rescalings λ' = σ_v / (2 σ_total) and β' = σ_total / (2 σ_v) with σ_total = sqrt(σ_u² + σ_ε²) and the invariant product λ'β' = 1/4. The privacy subsidy is then identified as the closed-form term -E[(v - p)ε] arising from the Gaussian cross moments. None of these steps reduce to a fitted parameter renamed as a prediction, a self-definitional loop, or a load-bearing self-citation; the Milionis et al. (2022) reference is used only for loose analogy to LVR and is not invoked to justify any uniqueness or ansatz. The derivation remains self-contained against the maintained assumptions.

Axiom & Free-Parameter Ledger

axioms (3)

- domain assumption The market maker is a committed Bayesian updater who knows the noise distribution.

- domain assumption Privacy perturbation is independent Gaussian noise added to order flow.

- domain assumption Equilibrium strategies are linear in the observed (noisy) order flow.

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

The unique price-impact coefficient is λ = σv/(2 √(σu² + σε²)) with informed-trader linear coefficient β = √(σu² + σε²)/σv (Theorem 1). ... λβ = 1/2 for all σε ≥ 0.

-

IndisputableMonolith/Foundation/BranchSelection.leanbranch_selection unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

A welfare decomposition then identifies a closed-form per-period transfer ... the 'privacy subsidy'

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.