Revenue Maximization Under Sequential Price Competition Via The Estimation Of s-Concave Demand Functions

Pith reviewed 2026-05-22 22:45 UTC · model grok-4.3

The pith

A semi-parametric least-squares policy lets competing sellers converge to Nash prices at rate O(T^{-1/7}) while incurring O(T^{5/7}) regret each.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Under s-concave demand functions, the proposed semi-parametric least-squares dynamic pricing policy drives prices to the full-information Nash equilibrium at rate O(T^{-1/7}) and bounds each seller's regret by O(T^{5/7}).

What carries the argument

s-concavity of demand functions, which guarantees equilibrium existence and supplies the shape constraint used both for estimation and for deriving the convergence and regret rates via semi-parametric least-squares.

If this is right

- Sellers can approach competitive equilibrium prices without observing rivals' demands or knowing the demand mapping explicitly.

- The same policy yields both asymptotic price convergence and sublinear regret against a dynamic benchmark.

- New concentration inequalities hold for least-squares estimators under shape constraints.

- Equilibrium existence follows directly from the s-concavity assumption on the demand system.

Where Pith is reading between the lines

- The approach may extend to other shape restrictions that also guarantee equilibrium existence, such as log-concavity.

- The rates could be tested in laboratory experiments where human subjects play the pricing game with unknown demand.

- Similar semi-parametric methods might apply to other repeated strategic interactions such as quantity competition or auction bidding.

Load-bearing premise

The demand function of each seller is s-concave.

What would settle it

A numerical simulation in which demand functions violate s-concavity while all other modeling assumptions hold and the observed convergence rate is slower than O(T^{-1/7}).

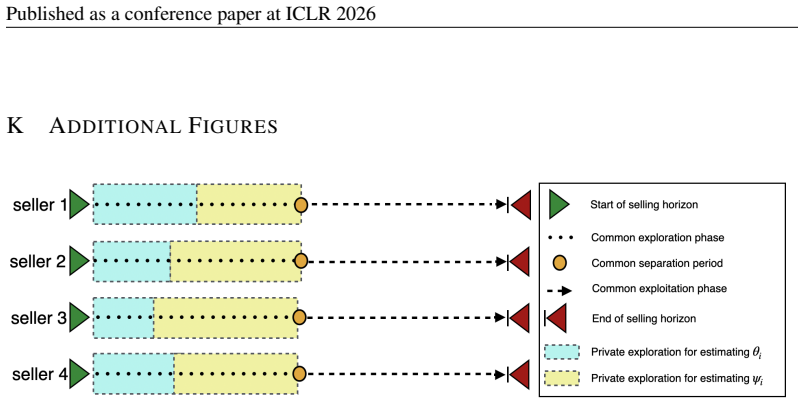

Figures

read the original abstract

We consider price competition among multiple sellers over a selling horizon of $T$ periods. In each period, sellers simultaneously offer their prices (which are made public) and subsequently observe their respective demand (not made public). The demand function of each seller depends on all sellers' prices through a private, unknown, and nonlinear relationship. We propose a dynamic pricing policy that uses semi-parametric least-squares estimation and show that when the sellers employ our policy, their prices converge at a rate of $O(T^{-1/7})$ to the Nash equilibrium prices that sellers would reach if they were fully informed. Each seller incurs a regret of $O(T^{5/7})$ relative to a dynamic benchmark policy. A theoretical contribution of our work is proving the existence of equilibrium under shape-constrained demand functions via the concept of $s$-concavity and establishing regret bounds of our proposed policy. Technically, we also establish new concentration results for the least squares estimator under shape constraints. Our findings offer significant insights into dynamic competition-aware pricing and contribute to the broader study of non-parametric learning in strategic decision-making.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript considers multi-seller sequential price competition over a horizon of T periods, where each seller's demand is an unknown nonlinear function of all prices. It proposes a semi-parametric least-squares dynamic pricing policy and claims that, when all sellers adopt it, prices converge to the fully-informed Nash equilibrium at rate O(T^{-1/7}) while each seller incurs regret O(T^{5/7}) against a dynamic benchmark. The paper proves existence of equilibrium under the maintained s-concavity shape constraint on demands and derives new concentration inequalities for the shape-constrained least-squares estimator.

Significance. If the central claims hold, the work supplies the first explicit convergence and regret rates for competitive dynamic pricing under a shape constraint that simultaneously guarantees equilibrium existence and enables the statistical bounds. The new concentration results for shape-constrained estimation constitute a technical contribution with potential applicability to other non-parametric learning problems in games.

minor comments (2)

- [Abstract] Abstract: the statement of the convergence rate O(T^{-1/7}) and regret O(T^{5/7}) would benefit from a parenthetical note on the dependence (or independence) of the hidden constants on the s-concavity parameter and the dimension of the price vector.

- [Regret analysis] The manuscript would be strengthened by an explicit statement, in the section deriving the regret bound, of how the s-concavity parameter enters the final O(T^{5/7}) expression (or why it does not).

Simulated Author's Rebuttal

We thank the referee for their positive assessment of the manuscript, accurate summary of the contributions on s-concave demand estimation in sequential price competition, and recommendation for minor revision. The significance statement correctly highlights the novelty of the convergence rates, regret bounds, and new concentration inequalities for shape-constrained estimators.

Circularity Check

No significant circularity identified

full rationale

The paper maintains s-concavity as an explicit shape constraint on demand functions and derives equilibrium existence plus new concentration inequalities for the semi-parametric least-squares estimator directly from that assumption. The stated O(T^{-1/7}) convergence and O(T^{5/7}) regret bounds are obtained from these new technical results rather than by renaming fitted quantities or reducing to self-citations. No load-bearing step equates a claimed prediction to an input by construction; the derivation chain is self-contained against the maintained assumptions and external benchmarks.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Demand functions satisfy s-concavity

Forward citations

Cited by 2 Pith papers

-

Harnessing Unimodality in Semiparametric Contextual Pricing via Oracle Price Map Learning

ORBIT learns the (β-1)-smooth oracle price map via local polynomial approximation and bandit convex optimization in a semiparametric contextual pricing model, achieving regret Õ(T^{(2β-1)/(4β-3)} + √(dT)) with a match...

-

Equilibrium and Pricing in Consumer Networks with Nonlinear Utilities: An Online Shape-Constrained Learning Approach

The paper establishes equilibrium existence and uniqueness for nonlinear utility consumer networks under contraction conditions and proposes a shape-constrained isotonic regression approach with strict no-regret conve...

Reference graph

Works this paper leans on

-

[1]

The requirement that exploration prices follow an elliptically symmetric distribution is used to guarantee the consistency of the estimator of θi in the single-index model. In particular, this assumption is invoked in Lemma E.2 to derive the normal equations (the same assumption can be found in Balabdaoui et al. (2019) and Brillinger (2012)). If the explo...

work page 2019

-

[2]

As we will discuss in Appendix D.2, the property that g(x + y) = g(x)g(y) (satisfied, for example, by Gaussian distributions) supports the estimation of ψi. It ensures that ψi,θ(u) (defined in (18)) depends on u solely through the argument of ψi rather than that of g (see Equation (29)). This decoupling guarantees that ψi,θ inherits key properties from ψi...

work page 2026

-

[3]

From the constraint in Equation (27): u − θ⊤m = v⊤ v ∥v∥2 y1 + α ⇒ u − θ⊤m = ∥v∥2y1 ⇒ y1 = u − θ⊤m ∥v∥2 . Since the original density in the y-space is fy(y) ∝ g(y2 1 + ∥α∥2 2), when conditioning on y1, the conditional density on the (N − 1)-dimensional space of α is: fα|v⊤y=u−θ⊤m(α) ∝ g u − θ⊤m ∥v∥2 2 + ∥α∥2 2 ! . Now, using the assumption that g(x + y) =...

work page 2026

-

[4]

(37) Lemma G.1. If Assumptions in the Theorem hold, for T sufficiently large we have E[supp∈P |ψi(θ⊤ i p) − bψi, eθi (eθ⊤ i p)|] ≲ Xi √ N( log τ τ )2/5, where Xi = max {Ci, Bi}, and Bi and Ci are defined in (17) and (21), respectively. Moreover, there exists a unique valueκ⋆ i ∈ (0, 1) that minimizes E[supp∈P |ψi(θ⊤ i p) − bψi, eθi (eθ⊤ i p)|]. This value...

work page 2026

-

[5]

< β 2 1 ⇐ ⇒ β2 1 > N − 1 N . Thus, LΓ ↑ 1 as β1 ↓ q N −1 N . In particular, we have the following scheme: N = 2 : β1 ↓ q 1 2 ≈ 0.707 = ⇒ LΓ ↑ 1, N = 4 : β1 ↓ q 3 4 ≈ 0.866 = ⇒ LΓ ↑ 1, N = 6 : β1 ↓ q 5 6 ≈ 0.913 = ⇒ LΓ ↑ 1. A summary of the two extreme cases can be found in Table 3. Simulation design. Given the discussion above, and the table in Table 3, f...

work page 2026

-

[6]

The Cauchy PDF is (−1/2)-optimal-concave (independently of scaling and location param- eters)

-

[7]

The Pareto PDF is − 1 α+1 -optimal-concave, (independently of the location), where α > 0 is the scaling factor

-

[8]

The log-normal PDF with parameters (µ, σ2) is − σ2 4 -optimal-concave, (independently of µ). L.3.2 s-CONCAVE CDF S AND SURVIVAL FUNCTIONS Let F be a CDF and ¯F = 1 − F its survival function, and let f = F ′. When {u : f(u) > 0} = R, for similar reasoning as in Remark L.5, a necessary condition for having ϕ = ds ◦ F or ϕ = ds ◦ ¯F concave, is that s ≤ 0. I...

-

[9]

56 Published as a conference paper at ICLR 2026

If f(a) = 0, f ′(a) = 0 and F is s-concave, then s ≤ 1/2. 56 Published as a conference paper at ICLR 2026

work page 2026

-

[10]

If f(b) = 0, f ′(b) = 0 and ¯F is s-concave, then s ≤ 1/2. In the following proposition, we prove that, under certain conditions, when a density function is s-concave, then the CDF and the survival function is µ-concave for some µ = µ(s). The proof of Proposition L.8 is deferred to Appendix L.3.7. Proposition L.8. Fix a function f : (a, b) 7→ (0, ∞) conti...

-

[11]

If f is s-concave on (a, b) with f(a) ̸= 0 and s > −1, then F is µ-concave for all µ ≤ 1 − 1 s+1

-

[12]

If f is s-concave on (a, b) with f(a) = 0 and s ̸= −1, then F is µ-concave for all µ ≤ 1 − 1 s+1

-

[13]

The proof of Proposition L.9 is deferred to Appendix L.3.8

If f is monotone decreasing, then F is s-concave for any s < 1. The proof of Proposition L.9 is deferred to Appendix L.3.8. Proposition L.9. Fix a function f : (a, b) 7→ [0, ∞) continuously differentiable, and let F (u) =R u a f(t)dt for all x ∈ (a, b) and define f(b) = limu→b f(u). Then:

-

[14]

If f is s-concave on (a, b) with f(b) ̸= 0 and s > −1, then ¯F is µ-concave for all µ ≤ 1 − 1 s+1

-

[15]

If f is s-concave on (a, b) with f(b) = 0 and s ̸= −1, then ¯F is µ-concave for all µ ≤ 1 − 1 s+1

-

[16]

The special case s = 0 was proved by Bagnoli & Bergstrom (2006)

If f is monotone decreasing, then ¯F is s-concave for any s < 1. The special case s = 0 was proved by Bagnoli & Bergstrom (2006). L.3.3 s-CONCAVE CDF S THAT ARE NOT LOG -CONCAVE From Figure 11 we already know that the CDFs of thePareto, Lognormal. Student’s t, Cauchyare not log-concave. However, by our Proposition L.9 we immediately get that they are s∗-o...

work page 2006

-

[17]

The Cauchy CDF and survival function are µ-concave for any µ ≤ 1 (independently of scaling and location parameters)

-

[18]

The Pareto CDF and survival function areµ-concave for any µ ≤ − 1 α, (independently of the location), where α is the scaling factor

-

[19]

The log-normal CDF and survival function are with parameters (µ, σ2) are µ-concave for any µ ≤ σ2 σ2−4, (independently of µ). From Proposition L.8 (and Proposition L.9), if f is µ⋆-optimal-concave it does not necessarily means that F (and ¯F ) is s(µ∗) = 1 − 1 µ∗+1 -optimal concave. Indeed, the optimal concave value can be larger than s(µ∗). However, for ...

work page 2026

-

[20]

Power function example. Fix α > 1 and set ϑ(x) = xα. Then ϑ′(x) = αxα−1, ϑ ′′(x) = α(α − 1)xα−2, and ϑ′′(x) + s(ϑ′(x))2 = αxα−2 h (α − 1) + sαxα i . Since xα ≤ 1 on (0, 1), a sufficient (and sharp) condition is s ≤ − α−1 α . Hence F (x) = exp(xα) is s∗-concave for s∗ = − α−1 α , but not log-concave because ϑ′′(x) > 0

-

[21]

4x2 ν2 − ν + 1 2 − ν + 1 2 − 1 1 + x2 ν − ν+1 2 −2 + 2 ν − ν + 1 2 1 + x2 ν − ν+1 2 −1# + (s − 1)

Exponential example. Fix k > 0 and set ϑ(x) = ekx. Then ϑ′(x) = kekx, ϑ ′′(x) = k2ekx, and ϑ′′(x) + s(ϑ′(x))2 = k2ekx 1 + sekx . Since ekx ≤ ek on (0, 1), a sufficient and sharp condition is s ≤ −e−k. Thus F (x) = exp ekx is s∗-concave for s∗ = −e−k, but not log-concave since ϑ′′(x) > 0. L.3.5 P ROOF OF PROPOSITION L.6 Proof of a). We have that f(x) = Γ( ...

work page 2026

-

[22]

However, since this inequality has to hold for all x, we can assume x0 = 0. The characterization translates to 1 + x2 γ2 −1" (−1) 2 γ2 1 + x2 γ2 −2 + 8x2 γ4 1 + x2 γ2 −3# + (s − 1) (−1)2x γ2 1 + x2 γ2 −2!2 ≤ 0 iff (−1) 2 γ2 1 + x2 γ2 −2 + 8x2 γ4 1 + x2 γ2 −3 + (s − 1)4x2 γ4 1 + x2 γ2 −3 ≤ 0 iff (−1) 2 γ2 1 + x2 γ2 + 8x2 γ4 + (s − 1)4x2 γ4 ≤ 0 iff −2x2 γ4 ...

work page 2026

-

[23]

L.3.7 P ROOF OF PROPOSITION L.8 Proof

Similar proof hold for ¯F . L.3.7 P ROOF OF PROPOSITION L.8 Proof. We need to prove thatF · f ′ + (µ − 1)f2 ≤ 0. Using that f s−1 · f ′ is non-increasing (because (ds ◦ f)′′ ≤ 0 i.e. (ds ◦ f)′ = f s−1 · f is non-increasing) we have f ′(u) f(u) F (u) = f s−1(u) f(u) f ′(u) f s−1(u) Z u a f(t)dt ≤ 1 f(u)f s−1(u) Z u a f s−1(t)f ′(t)f(t)dt = 1 f(u)f s−1(u) f...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.