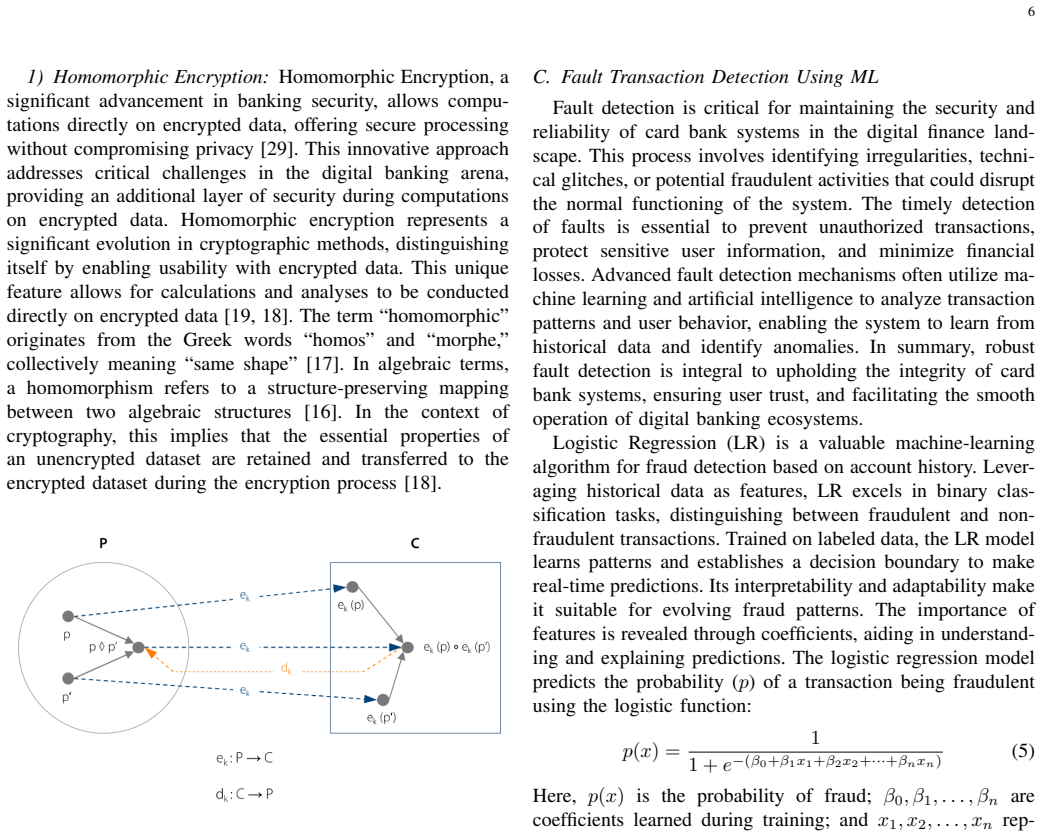

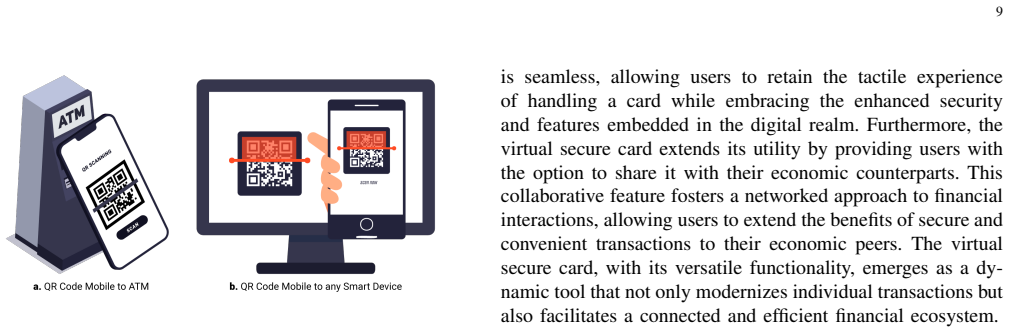

Innovations in Cardless Artificial Intelligence Banking: A Comprehensive Framework for Cyber Secure and Fraud Mitigation using Machine Learning Algorithms

Pith reviewed 2026-05-22 04:44 UTC · model grok-4.3

The pith

A framework for cardless AI banking uses machine learning to create secure virtual cards and mitigate fraud.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The proposed framework establishes a holistic cybersecurity and fraud-mitigation paradigm for cardless AI banking systems. It employs AI-powered data cryptography to create secure virtual cards, ensures secure communication, and uses AI-based authorization and machine learning to authenticate transactions and identify fraud, thereby minimizing information exposure and reducing risks.

What carries the argument

The comprehensive framework that integrates AI-driven feature-based banking with machine learning algorithms to generate encrypted virtual cards and detect fraud.

If this is right

- Financial institutions can address security concerns associated with traditional banking.

- Paves the way for a future banking landscape that is fraud-resistant, secure, and convenient for users.

- Ensures the integrity of financial activities among banking systems, cardholders, and third-party vendors through secure communication channels.

- Minimizes information exposure and reduces fraud risks by generating virtual cards with encrypted data.

Where Pith is reading between the lines

- The framework's effectiveness could be tested by deploying it in a controlled environment with real transaction data to measure actual fraud reduction.

- Similar AI cryptography methods might apply to securing other digital payment systems like mobile wallets.

- Practical validation would require comparing fraud rates before and after adopting the virtual card approach in live banking operations.

Load-bearing premise

The assumption that AI-powered data cryptography and machine learning algorithms can reliably authenticate transactions and proactively identify fraud without any described methods or validation data.

What would settle it

Running the proposed machine learning algorithm on a dataset of historical banking transactions and checking if it achieves high accuracy in fraud identification compared to existing methods.

Figures

read the original abstract

The advent of cardless artificial intelligence (AI) banking heralds a paradigm shift in the financial landscape, offering users unprecedented security and convenience. This paper outlines a comprehensive framework designed to enhance cybersecurity, introduce auto-generated virtual cards, and mitigate fraud risks within cardless AI banking systems. The framework envisions a future banking architecture that employs AI-powered data cryptography to create secure virtual cards for seamless transactions. By emphasizing secure communication channels, it ensures the integrity of financial activities among banking systems, cardholders, and third-party vendors. AI-based authorization methodologies play a pivotal role in authenticating each transaction while proactively identifying potential fraud, demonstrating the framework's efficacy in fortifying cardless AI banking security. The initial approach, featuring an AI-driven, feature-based banking system, ensures the generation of virtual cards with encrypted data, minimizing information exposure and reducing fraud risks. Integrating a machine learning algorithm adds an additional layer of protection against potential fraudulent activities. In conclusion, the proposed framework establishes a holistic cybersecurity and fraud-mitigation paradigm for cardless AI banking systems. Its implementation empowers financial institutions to address security concerns associated with traditional banking, paving the way for a future banking landscape that is not only fraud-resistant but also secure and convenient for users.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper outlines a conceptual framework for cardless AI banking that employs AI-powered data cryptography to generate secure virtual cards, AI-based authorization to authenticate transactions, and an additional machine learning layer to proactively detect and mitigate fraud, with the goal of establishing a holistic cybersecurity paradigm that reduces information exposure and fraud risks compared to traditional systems.

Significance. If the high-level concepts were expanded with named cryptographic primitives, specific ML architectures, training protocols, and empirical results showing measurable fraud reduction, the work could contribute to practical advancements in secure financial systems; as presented, the lack of technical substance limits its value to the field.

major comments (2)

- Abstract: The claims that the framework 'demonstrating the framework's efficacy in fortifying cardless AI banking security' and 'establishes a holistic cybersecurity and fraud-mitigation paradigm' rest on unspecified AI cryptography and ML components without any algorithms, feature sets, model details, training procedures, or evaluation metrics, rendering the central efficacy assertion unsupported.

- Abstract (and implied methodology): No comparison to existing cardless systems, baseline fraud rates, or quantitative results (e.g., precision, recall, or false-positive rates) is provided to substantiate that the proposed virtual-card encryption and ML layer reduces fraud exposure, which is load-bearing for the fraud-mitigation claim.

minor comments (1)

- Abstract: Repetitive phrasing around 'security,' 'fraud mitigation,' and 'convenience' could be condensed to improve readability and focus.

Simulated Author's Rebuttal

We thank the referee for the constructive feedback on our manuscript. The comments correctly identify that the work is presented at a high conceptual level without detailed technical specifications or empirical validation. We address each major comment below and outline the revisions we will incorporate.

read point-by-point responses

-

Referee: Abstract: The claims that the framework 'demonstrating the framework's efficacy in fortifying cardless AI banking security' and 'establishes a holistic cybersecurity and fraud-mitigation paradigm' rest on unspecified AI cryptography and ML components without any algorithms, feature sets, model details, training procedures, or evaluation metrics, rendering the central efficacy assertion unsupported.

Authors: We agree that the abstract asserts efficacy without supporting technical details or metrics. The manuscript is a high-level conceptual framework rather than an implemented system. In revision, we will qualify the abstract language to describe the framework as a proposed architecture for future development and validation, removing unsupported efficacy assertions. We will also add illustrative examples of potential cryptographic approaches (e.g., symmetric encryption for virtual card data) and ML techniques (e.g., supervised classification for anomaly detection) in the methodology section, while explicitly stating that full algorithms, training protocols, and evaluations are beyond the current scope. revision: partial

-

Referee: Abstract (and implied methodology): No comparison to existing cardless systems, baseline fraud rates, or quantitative results (e.g., precision, recall, or false-positive rates) is provided to substantiate that the proposed virtual-card encryption and ML layer reduces fraud exposure, which is load-bearing for the fraud-mitigation claim.

Authors: We acknowledge the absence of quantitative comparisons and results. As a conceptual paper, we lack access to proprietary transaction datasets needed for metrics such as precision, recall, or false-positive rates, and no such experiments were conducted. We will revise the manuscript to include a qualitative discussion comparing the proposed framework to existing cardless approaches (e.g., token-based systems) at the architectural level, highlighting design differences in information exposure. Claims will be adjusted to present fraud mitigation as a potential outcome of the framework's layered design rather than a demonstrated reduction, with empirical testing noted as future work. revision: partial

- Provision of specific quantitative performance metrics (precision, recall, false-positive rates) or empirical results on real banking data, as the manuscript is a conceptual framework without experimental components or dataset access.

Circularity Check

No circularity detected; high-level framework proposal lacks derivations or self-referential elements

full rationale

The paper describes a conceptual architecture for cardless AI banking with AI-powered cryptography, virtual card generation, and ML-based fraud detection, but supplies no equations, mathematical derivations, fitted parameters, predictions, or self-citations. All claims remain at the level of high-level component descriptions without any load-bearing steps that could reduce to inputs by construction. The absence of quantitative models or uniqueness theorems means the content is self-contained as a framework proposal rather than a derived result.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

https://www.cyber.gc.ca/sites/default/files/ ncta-2023-24-web.pdf

Canadian Centre for Cyber Security, National Cyber Threat Assessment 2023–2024. https://www.cyber.gc.ca/sites/default/files/ ncta-2023-24-web.pdf

work page 2023

-

[2]

https://home.treasury.gov/system/files/136/ 2022-National-Money-Laundering-Risk-Assessment.pdf

Department of the Treasury, National Money Laundering Risk As- sessment, February 2022. https://home.treasury.gov/system/files/136/ 2022-National-Money-Laundering-Risk-Assessment.pdf

work page 2022

-

[3]

Mastercard, Ecommerce fraud trends and statistics merchants need to know in 2024. https://b2b.mastercard.com/news-and-insights/blog/ ecommerce-fraud-trends-and-statistics-merchants-need-to-know-in-2024/

work page 2024

-

[4]

https://merchantriskcouncil.org/learning/mrc-exclusive-reports/ global-payments-and-fraud-report

merchantriskcouncil.org, 2023 Global Payments and Fraud Report. https://merchantriskcouncil.org/learning/mrc-exclusive-reports/ global-payments-and-fraud-report

work page 2023

-

[5]

FFIEC Authentication and Access to Financial Institution Services and Systems Guidance, August 2021. https://www.ffiec.gov/press/pdf/ Authentication-and-Access-to-Financial-Institution-Services-and-Systems. pdf

work page 2021

-

[6]

Secure Mobile Payment Architecture Enabling Multi-factor Authentica- tion,

H. Alamleh, A. A. S. AlQahtani and B. Al Smadi, “Secure Mobile Payment Architecture Enabling Multi-factor Authentica- tion,” 2023 Systems and Information Engineering Design Sym- posium (SIEDS), Charlottesville, V A, USA, 2023, pp. 19–24, doi: 10.1109/SIEDS58326.2023.10137778

-

[7]

Comprehensive Analysis for Fraud Detection of Credit Card through Machine Learning,

P. Roy, P. Rao, J. Gajre, K. Katake, A. Jagtap and Y . Gajmal, “Comprehensive Analysis for Fraud Detection of Credit Card through Machine Learning,” 2021 International Conference on Emerging Smart Computing and Informatics (ESCI), Pune, India, 2021, pp. 765–769, doi: 10.1109/ESCI50559.2021.9397029

-

[8]

The safety risks related to bank cards and cyber attacks,

A. Koraus, J. Dobrovi ˇc, R. Rajnoha, and I. Brezina, “The safety risks related to bank cards and cyber attacks,”Journal of Security and Sustain- ability Issues, vol. 6, pp. 563–574, 2017, doi: 10.9770/jssi.2017.6.4(3)

-

[9]

M. Al Rousan and B. Intrigila, “Multi-Factor Authentication for e- Government Services using a Smartphone Application and Biometric Identity Verification,”Journal of Computer Science, vol. 16, pp. 217– 224, 2020, doi: 10.3844/jcssp.2020.217.224

-

[10]

J. M. Ashfield, “Method and apparatus for using at least a portion of a one-time password as a dynamic card verification value,” U.S. Patent 9,251,637, Feb. 2, 2016

work page 2016

-

[11]

A Secure and Efficient Multi-Factor Authentication Algorithm for Mobile Money Applications,

G. Ali, M. A. Dida, and A. Elikana Sam, “A Secure and Efficient Multi-Factor Authentication Algorithm for Mobile Money Applications,” Future Internet, vol. 13, no. 12, p. 299, 2021, doi: 10.3390/fi13120299

-

[12]

J. S. Kiernan and A. Comoreanu, “Credit Card Fraud Statistics,” WalletHub, Oct. 2023. https://wallethub.com/edu/cc/ credit-card-fraud-statistics/25725

work page 2023

-

[13]

Identity Theft and Credit Card Fraud Statistics for 2023,

J. Caporal, “Identity Theft and Credit Card Fraud Statistics for 2023,” The Motley Fool. https://www.fool.com/the-ascent/research/ identity-theft-credit-card-fraud-statistics/

work page 2023

-

[14]

Secure and Fraud Proof Online Payment System for Credit Cards,

B. A. Smadi, A. A. S. AlQahtani and H. Alamleh, “Secure and Fraud Proof Online Payment System for Credit Cards,” 2021 IEEE 12th Annual Ubiquitous Computing, Electronics & Mobile Communication Conference (UEMCON), New York, NY , USA, 2021, pp. 0264–0268, doi: 10.1109/UEMCON53757.2021.9666549

-

[15]

Computing arbitrary functions of encrypted data,

C. Gentry, “Computing arbitrary functions of encrypted data,”Commu- nications of the ACM, vol. 53, pp. 97–105, 2010

work page 2010

-

[16]

F. Modler and M. Kreh,Tutorium Analysis 1 und Lineare Algebra 1. Springer: Berlin/Heidelberg, Germany, 2011

work page 2011

-

[17]

M. Ogburn, C. Turner, and P. Dahal, “Homomorphic Encryption,” Procedia Computer Science, vol. 20, pp. 502–509, 2013

work page 2013

-

[18]

Schulze,Homomorphe Verschl ¨usselung und Europas Cloud

M. Schulze,Homomorphe Verschl ¨usselung und Europas Cloud. Stiftung Wissenschaft und Politik, Berlin, Germany, 2021

work page 2021

-

[19]

A Guide to Fully Homomorphic Encryption,

F. Armknecht et al., “A Guide to Fully Homomorphic Encryption,” Cryptology ePrint Archive, 2015. https://eprint.iacr.org/2015/1192.pdf

work page 2015

-

[20]

Cybersource,2023 Global Ecommerce Payments and Fraud Report,

work page 2023

-

[21]

https://www.cybersource.com/content/dam/documents/campaign/ fraud-report/global-fraud-report-2023-en.pdf

work page 2023

-

[22]

New FTC Data Show Consumers Reported Losing Nearly $8.8 Billion to Scams in 2022,

Federal Trade Commission, “New FTC Data Show Consumers Reported Losing Nearly $8.8 Billion to Scams in 2022,” Feb. 2023. https://www.ftc.gov/news-events/news/press-releases/2023/02/ new-ftc-data-show-consumers-reported-losing-nearly-88-billion-scams-2022

work page 2022

-

[23]

https://nilsonreport.com/articles/ card-fraud-losses-worldwide/

Nilson Report, December 2021. https://nilsonreport.com/articles/ card-fraud-losses-worldwide/

work page 2021

-

[24]

E-commerce payment fraud losses worldwide 2020–2023

Statista, “E-commerce payment fraud losses worldwide 2020–2023.” https://www.statista.com/statistics/1273177/ ecommerce-payment-fraud-losses-globally/

-

[25]

E-commerce fraud to cost $48 billion globally as attacks skyrocket, report says

Old National Bank, “E-commerce fraud to cost $48 billion globally as attacks skyrocket, report says.” https://www.oldnational.com/resources/insights/ e-commerce-fraud-to-cost-48-billion-globally-this-year-as-attacks-skyrocket-report-says/

-

[26]

Online Payment Fraud Losses to Exceed $343 Billion Globally Over the Next 5 Years,

Juniper Research, “Online Payment Fraud Losses to Exceed $343 Billion Globally Over the Next 5 Years,” 2022. https://www.juniperresearch. com/press/online-payment-fraud-losses-to-exceed-343bn/

work page 2022

-

[27]

Federal Deposit Insurance Corporation,Risk Review 2023. https://fdic. gov/analysis/risk-review/2023-risk-review/2023-risk-review-full.pdf

work page 2023

-

[28]

E. A. L. Marazqah Btoush et al., “A systematic review of literature on credit card cyber fraud detection using machine and deep learning,” PeerJ Computer Science, vol. 9, p. e1278, Apr. 2023, doi: 10.7717/peerj- cs.1278

-

[29]

Cybersource,Global Fraud and Payments Survey Report 2022. https://www.cybersource.com/content/dam/documents/campaign/ fraud-report/global-fraud-report-2022.pdf

work page 2022

-

[30]

Data Privacy and System Security for Banking on Clouds using Homomorphic Encryption,

S. Mittal, P. Jindal, and K. R. Ramkumar, “Data Privacy and System Security for Banking on Clouds using Homomorphic Encryption,” 2021 2nd International Conference for Emerging Technology (INCET), Bela- gavi, India, 2021, pp. 1–6, doi: 10.1109/INCET51464.2021.9456345

-

[31]

A survey on homomorphic encryption schemes: Theory and implementation,

A. Acar, H. Aksu, A. S. Uluagac, and M. Conti, “A survey on homomorphic encryption schemes: Theory and implementation,”ACM Computing Surveys, vol. 51, pp. 1–35, 2018

work page 2018

-

[32]

https://www.mass.gov/info-details/ understand-cybersecurity-for-financial-institutions

Mass.gov,Handbook: Cybersecurity for the Financial Services Industry, 2017. https://www.mass.gov/info-details/ understand-cybersecurity-for-financial-institutions

work page 2017

-

[33]

Department of Justice,Financial Fraud in the United States, 2017

U.S. Department of Justice,Financial Fraud in the United States, 2017. https://bjs.ojp.gov/content/pub/pdf/ffus17.pdf

work page 2017

-

[34]

Juniper Research,Online Payment Fraud: Emerging Threats, Segment Analysis, and Market Forecasts 2022–2027. https: //www.juniperresearch.com/research/fintech-payments/fraud-identity/ online-payment-fraud-research-report/

work page 2022

-

[35]

Enhance Luhn algorithm for validation of credit card numbers,

K. W. Hussein et al., “Enhance Luhn algorithm for validation of credit card numbers,” 2013

work page 2013

-

[36]

Potential of Homomorphic Encryption for Cloud Computing Use Cases in Manufacturing,

R. Kiesel et al., “Potential of Homomorphic Encryption for Cloud Computing Use Cases in Manufacturing,”Journal of Cybersecurity and Privacy, vol. 3, pp. 44–60, 2023, doi: 10.3390/jcp3010004. 14 Md. IsrafeelMd Israfeel achieved his master’s degrees in electrical and computer engineering from the University of Central Florida, Florida, in 2024, and another ...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.