Do Prediction Markets Match Option Prices? Bitcoin Threshold Evidence from Binance and Polymarket

Pith reviewed 2026-06-26 18:15 UTC · model grok-4.3

The pith

Bitcoin prediction markets price the same threshold events 5.6 percentage points away from matching option values on average.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

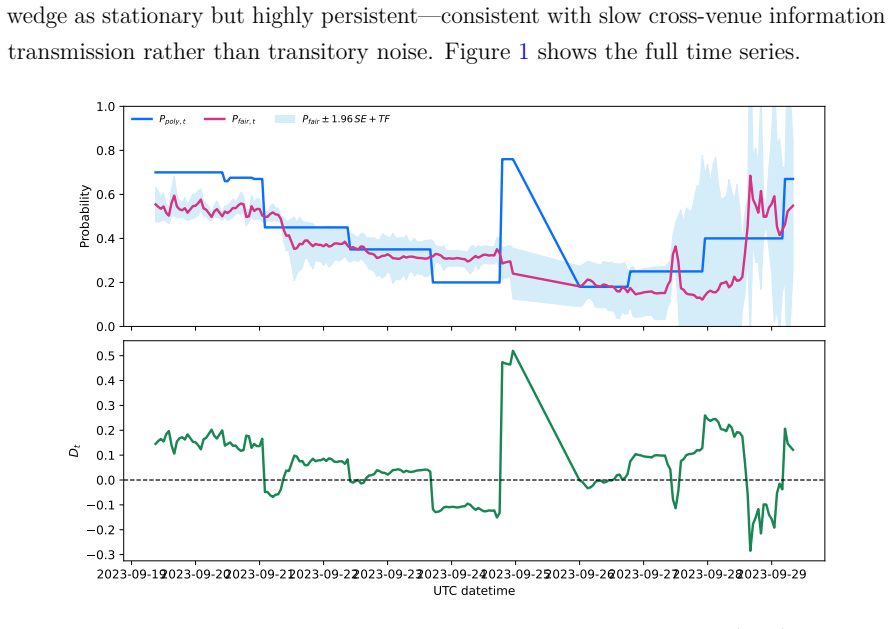

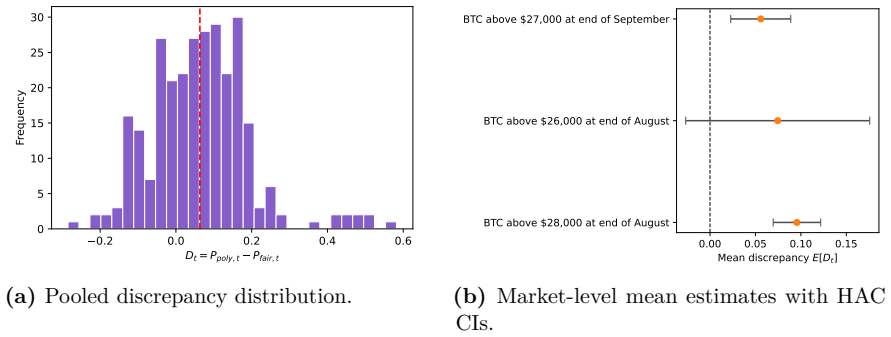

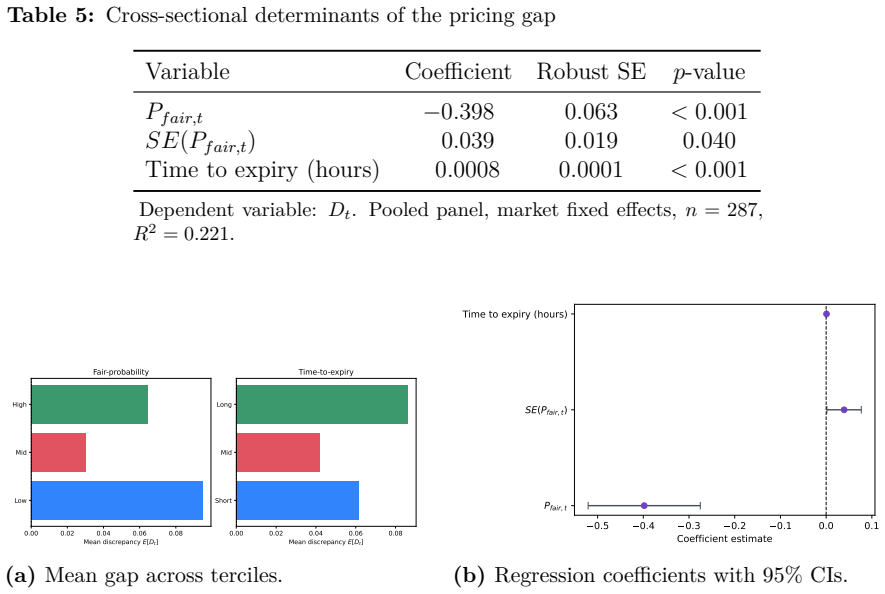

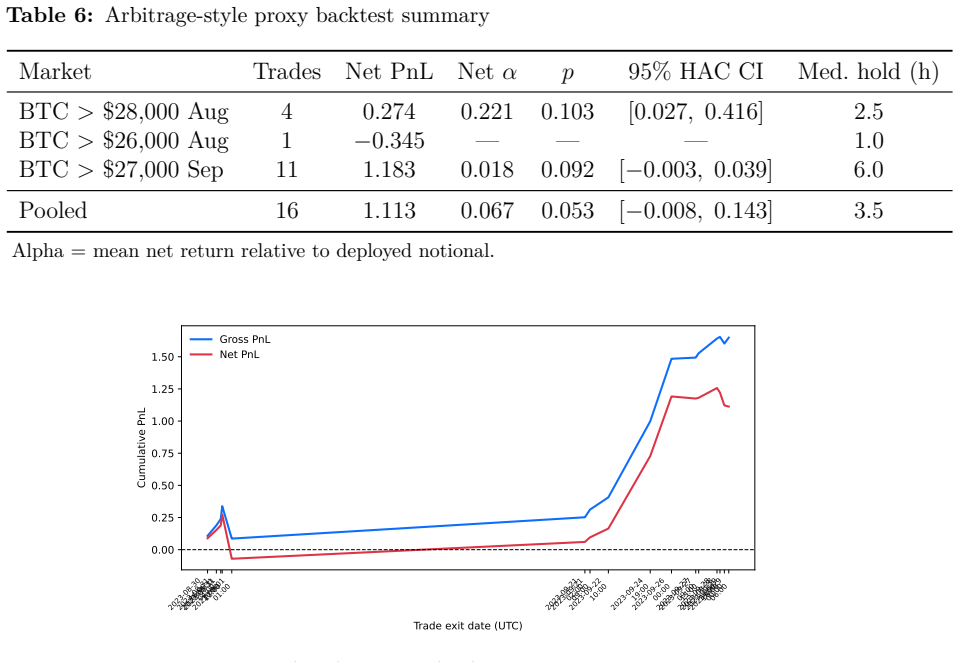

For each hour, the Polymarket Yes price differs from the discounted risk-neutral probability extracted from the matching Binance call by an average of 5.6 percentage points in the primary contract and 6.3 points when three contracts are pooled. The wedge is persistent yet mean-reverting, largest when the option-implied probability is low or maturity is long, and leaves a delta-hedged arbitrage proxy profitable after transaction costs. The same pattern appears, with a larger average gap, on Deribit.

What carries the argument

Hourly matched comparison of the Polymarket Yes price to the discounted risk-neutral binary value implied by the identical-strike, identical-maturity Binance call option.

If this is right

- The pricing wedge remains after HAC and block-bootstrap adjustments and survives pooling across contracts.

- Cross-sectional regressions show the gap widens at low option-implied probabilities and at longer maturities.

- A delta-hedged strategy that exploits the wedge stays positive after conservative costs, albeit with marginal precision.

- A parallel exercise on Deribit yields an 11-point pooled gap while the Ethereum case is mixed.

Where Pith is reading between the lines

- If the venues become more integrated, the observed gap should narrow measurably.

- The pattern implies that prediction-market participants may be bearing a liquidity or information premium not present in the option market.

- The same comparison method could be applied to other crypto underlyings or to non-crypto prediction markets to test whether segmentation is a general feature.

Load-bearing premise

The binary payoff of the Polymarket contract and the risk-neutral probability from the Binance option are directly comparable once discounted, with no material differences in liquidity, counterparty risk, or other frictions.

What would settle it

A data set that shows the gap shrinks to zero once the same contract is traded on a single integrated venue or after a large, simultaneous liquidity shock to both platforms.

Figures

read the original abstract

The digitization of financial markets has produced two classes of platforms that price, in principle, the same state - contingent payoffs: centralized crypto-option exchanges and blockchain-based prediction markets. This paper provides the first option-implied benchmark test of prediction-market pricing for cryptocurrency threshold contracts. For each hour in a matched sample, we compare the Polymarket Yes price with the discounted risk-neutral binary value implied by a listed Binance call option on the same underlying, strike, and maturity, and study the gap between them. In the main September 2023 Bitcoin contract, the mean pricing gap equals 5.6 percentage points across 214 hourly observations (t = 6.46, p < 10^{-9}). Pooling three Binance-compatible Bitcoin threshold markets yields a mean gap of 6.3 percentage points across 287 observations, robust to HAC and block-bootstrap inference. The gap is persistent - with an AR(1) half-life of roughly four hours - yet mean-reverting, consistent with slow information transmission between segmented venues rather than mechanical noise. Cross-sectional regressions reveal that the wedge is largest at low option-implied probabilities and long maturities, a pattern consistent with speculative demand for prediction-market contracts rather than measurement error. A delta-hedged arbitrage proxy remains profitable after conservative transaction costs, though with marginal statistical precision. A Deribit extension on the same three Bitcoin contracts produces a larger pooled gap of 11 percentage points, while a smaller Ethereum exercise yields mixed evidence. The results demonstrate that digital fragmentation of financial markets generates systematic, persistent pricing wedges even for economically identical payoffs.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper compares Polymarket prediction-market prices for Bitcoin threshold contracts against risk-neutral binary probabilities implied by matched Binance call options on the same underlying, strike, and maturity. It reports a mean gap of 5.6 percentage points (t=6.46) in the primary September 2023 contract over 214 hourly observations and 6.3 points when pooling three contracts over 287 observations. The gap is persistent (AR(1) half-life ~4 hours) yet mean-reverting, larger at low probabilities and long maturities, and accompanied by a marginally profitable delta-hedged arbitrage proxy after costs. Extensions to Deribit (larger gap) and Ethereum (mixed) are included. The results are interpreted as evidence of slow information transmission across segmented venues.

Significance. If the core comparison is valid, the study provides direct evidence of systematic pricing wedges between centralized crypto options and blockchain prediction markets for economically identical binary payoffs. The high-frequency matched design, robustness to HAC and block-bootstrap inference, and cross-sectional patterns add empirical weight to claims about market segmentation and information flow in digital assets. Reproducible hourly data construction and falsifiable predictions about gap size by probability and maturity are strengths.

major comments (1)

- [Abstract and §3] Abstract and §3 (implied-probability construction): the headline comparison requires recovering the discounted risk-neutral binary probability P(S_T > K) from the price of a single listed Binance call. A vanilla call equals the discounted risk-neutral expectation of (S_T - K)^+; this equals the binary probability only with a continuum of strikes or parametric assumptions (e.g., Black-Scholes inversion). The manuscript provides no description of the inversion method, approximation, or use of additional strikes. Because the largest reported gaps occur precisely where such an approximation is most fragile (low probabilities, longer maturities), any systematic bias in the implied probability would mechanically produce the observed wedge rather than reflect a true cross-venue difference. This is load-bearing for the central claim.

minor comments (2)

- The abstract states that a delta-hedged arbitrage proxy 'remains profitable after conservative transaction costs, though with marginal statistical precision.' The precise construction of the hedge ratio, the transaction-cost assumptions, and the exact p-value should be reported in the main text or a dedicated table for transparency.

- Table or figure labels for the pooled sample (287 observations) and the AR(1) half-life calculation should explicitly state the exact contract maturities and the estimation window used for the autocorrelation.

Simulated Author's Rebuttal

We thank the referee for the careful and constructive report. The single major comment raises a substantive methodological issue that we address below; we agree that additional detail is required and will revise accordingly.

read point-by-point responses

-

Referee: [Abstract and §3] Abstract and §3 (implied-probability construction): the headline comparison requires recovering the discounted risk-neutral binary probability P(S_T > K) from the price of a single listed Binance call. A vanilla call equals the discounted risk-neutral expectation of (S_T - K)^+; this equals the binary probability only with a continuum of strikes or parametric assumptions (e.g., Black-Scholes inversion). The manuscript provides no description of the inversion method, approximation, or use of additional strikes. Because the largest reported gaps occur precisely where such an approximation is most fragile (low probabilities, longer maturities), any systematic bias in the implied probability would mechanically produce the observed wedge rather than reflect a true cross-venue difference. This is load-bearing for the central claim.

Authors: We agree that the original manuscript omitted a clear description of how the risk-neutral binary probability is recovered from each single-strike Binance call price, and that this omission is material given the location of the largest gaps. In the revision we will expand §3 to state the exact procedure: for each matched observation we solve the Black-Scholes call-price equation for the implied probability P(S_T > K) using the option’s own implied volatility (backed out from the observed price and the prevailing risk-free rate and forward price). We will also report two robustness exercises: (i) an alternative that uses the nearest available strike to supply volatility when the target strike is sparse, and (ii) a non-parametric check that replaces the single-strike inversion with a simple linear interpolation across the two nearest strikes when both are observed. These additions will make the construction fully replicable and allow readers to assess whether the wedge survives alternative recoveries of the binary probability. revision: yes

Circularity Check

No significant circularity in empirical comparison

full rationale

The paper reports an empirical measurement of pricing gaps between two independent external data sources (Polymarket Yes prices and Binance call-option-implied binary probabilities). No load-bearing step reduces by construction to the paper's own inputs, fitted parameters, or self-citations; the gap is computed directly from observed market prices after the stated discounting step. The central claim therefore remains independent of the prediction-market data itself and is self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

doi: 10.1016/j.ijforecast.2008.03.007. Binance. Binance public data: Historical option and spot archives.https://data. binance.vision,

-

[2]

doi: 10.1086/260062. David A. Dickey and Wayne A. Fuller. Distribution of the estimators for autoregressive time series with a unit root.Journal of the American Statistical Association, 74 (366a):427–431,

-

[3]

doi: 10.2307/2286348. 19 Darrell Duffie. Asset price dynamics with slow-moving capital.Journal of Finance, 65 (4):1237–1267,

-

[4]

Denis Gromb and Dimitri Vayanos

doi: 10.1111/j.1540-6261.2010.01569.x. Denis Gromb and Dimitri Vayanos. Limits of arbitrage.Annual Review of Financial Economics, 2(1):251–275,

-

[5]

Bruno Jullien and Bernard Salanié

doi: 10.1146/annurev-financial-073009-104107. Bruno Jullien and Bernard Salanié. Estimating preferences under risk: The case of racetrack bettors.Journal of Political Economy, 108(3):503–530,

-

[6]

doi: 10.1086/262127. Péter Kondor. The more we know about the fundamental, the less we agree on the price. Review of Economic Studies, 79(3):1175–1207,

-

[7]

Andrew Leigh, Justin Wolfers, and Eric Zitzewitz

doi: 10.1093/restud/rdr055. Andrew Leigh, Justin Wolfers, and Eric Zitzewitz. What do financial markets think of War in Iraq? Working Paper 9587, National Bureau of Economic Research,

-

[8]

doi: 10.2307/1913610. Polymarket. Polymarket historical data.https://docs.polymarket.com,

-

[9]

Erik Snowberg, Justin Wolfers, and Eric Zitzewitz

doi: 10.1257/0895330041371461. Erik Snowberg, Justin Wolfers, and Eric Zitzewitz. Prediction markets for eco- nomic forecasting. In Graham Elliott and Allan Timmermann, editors,Hand- book of Economic Forecasting, volume 2, pages 657–687. Elsevier,

-

[10]

doi: 10.1016/B978-0-444-53683-9.00012-4. NBER Working Paper No. 18222 (2012). Richard H. Thaler and William T. Ziemba. Anomalies: Parimutuel betting markets: Racetracks and lotteries.Journal of Economic Perspectives, 2(2):161–174,

-

[11]

Justin Wolfers and Eric Zitzewitz

doi: 10.1257/jep.2.2.161. Justin Wolfers and Eric Zitzewitz. Prediction markets.Journal of Economic Perspectives, 18(2):107–126,

-

[12]

Justin Wolfers and Eric Zitzewitz

doi: 10.1257/0895330041371452. Justin Wolfers and Eric Zitzewitz. Interpreting prediction market prices as probabilities. Working Paper 12200, National Bureau of Economic Research,

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.